Industry: Chemicals and Materials

Published Date: March-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 186

Report ID: PMRREP35154

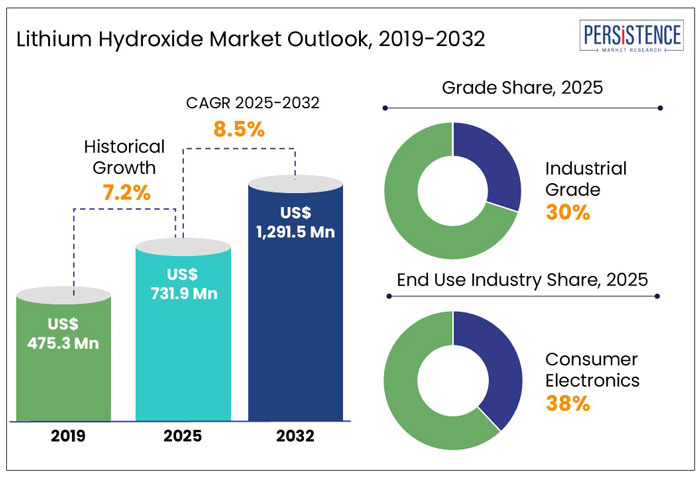

The global lithium hydroxide market size is anticipated to rise from US$ 731.9 Mn in 2025 to US$ 1,291.5 Mn by 2032. It is projected to witness a CAGR of 8.5% from 2025 to 2032. The increase in the manufacture of electric vehicles and the rise in worldwide EV sales, which surpassed 14 million units in 2023, are driving up demand for lithium hydroxide.

Government incentives, such as the U.S. Inflation Reduction Act and the EU Green Deal, are accelerating EV adoption and lithium hydroxide investments. The consumer electronics market, with over 1.5 billion smartphones shipped annually, also fuels demand. Mining companies like Albemarle and Ganfeng Lithium are expanding production to address supply concerns due to improved efficiency in lithium extraction technology.

Key Highlights of the Lithium Hydroxide Market

|

Global Market Attributes |

Key Insights |

|

Lithium Hydroxide Market Size (2025E) |

US$ 731.9 Mn |

|

Market Value Forecast (2032F) |

US$ 1,291.5 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

8.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.2% |

Spur in Production of Lithium Hydroxide Presents Novel Prospects

As per Persistence Market Research, the global lithium hydroxide industry witnessed a CAGR of 7.2% in the historical period between 2019 and 2024. In the observed period, global lithium production experienced steady growth, driven by rising demand for electric vehicles and energy storage systems. In 2019, lithium production was 77,000 metric tons, increasing to 130,000 metric tons by 2022 and further reaching 180,000 metric tons in 2023.

The expansion of lithium hydroxide refining capacity in China, Australia, and the U.S. has contributed to the growth. Australia, the largest lithium producer, accounted for 86,000 metric tons in 2023, while Chile and China ramped up production.

Companies like Albemarle and Tianqi Lithium expanded operations to meet demand, ensuring a stable lithium hydroxide supply for battery manufacturers.

Trend of Electric Vehicles Boost the Production of Lithium Hydroxide

In the estimated timeframe from 2025 to 2032, the global market for Lithium Hydroxide is likely to showcase a CAGR of 8.5%. As majority of lithium production is estimated to cater to the growth of EV production, owing to its crucial role for high-performance cathode materials.

The rising electric vehicle production is increasing demand for lithium hydroxide, a key component in high-nickel cathodes for long-range, high-performance batteries. In 2023, global EV sales exceeded 14 million units, a 35% increase from 2022, with China leading at 8 million sales, followed by Europe at 3.2 million and the U.S. at 1.4 million.

In 2024, the sales are expected to exceed 17 million units. Major automakers such as Tesla, BYD, and Volkswagen are increasing their production of electric vehicles. Meanwhile, battery manufacturers like CATL and LG Energy Solution are securing supplies of lithium hydroxide, which is driving investment in lithium extraction and refining capacities globally.

Growth Driver

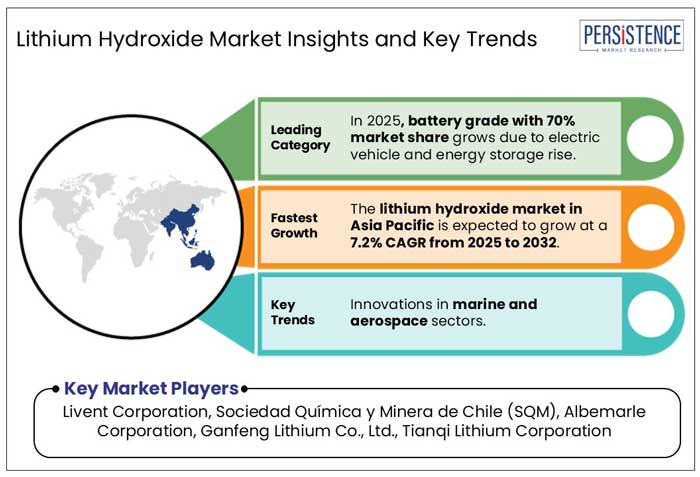

Innovations in Marine and Aerospace Sectors Shows Avenues for Investment

The growing output in the marine and aerospace industries is responsible for the market's expansion for lithium hydroxide. High-performance, lightweight lithium-ion batteries are crucial for these sectors' increased operational range and improved fuel economy.

In 2023, global aircraft production achieved an impressive total of 1,520 units, with Airbus delivering 735 aircraft and Boeing contributing 528 units. This trend reflects a robust demand for advanced energy storage solutions. Similarly, the marine sector has shown remarkable expansion, with shipbuilding output exceeding 40 million gross tons in 2023, largely driven by the rising interest in hybrid and fully electric vessels.

Furthermore, investments from companies such as Rolls-Royce, General Electric, and Northrop Grumman into electric propulsion technologies are indicative of a growing commitment to sustainable aviation and marine electrification initiatives. As a result, the demand for lithium hydroxide-based batteries is projected to continue its upward trajectory, aligning with these critical industry developments.

Market Restraining Factor

Rise in Toxicity Concerns Impedes the Sustainable Extraction Technology

Since over 5,000 cases of lithium poisoning are recorded worldwide each year, mostly because of accidental consumption and industrial exposure, toxicity concerns and high manufacturing costs are impeding the growth of the lithium hydroxide market.

Chronic exposure can lead to neurological damage, kidney dysfunction, and cardiovascular issues, raising concerns among regulatory bodies. Additionally, the cost of lithium hydroxide production remains high, driven by energy-intensive extraction methods and limited global reserves.

In 2024, lithium hydroxide production costs averaged US$ 6,000 to US$8,000 per metric ton, impacting profit margins for battery manufacturers. Despite growing EV demand, price volatility due to fluctuating supply from key producers like Australia, Chile, and China further complicates market expansion.

Investment in sustainable extraction technologies and recycling initiatives is crucial to reducing environmental and health risks and ensuring stable long-term growth for the lithium hydroxide industry.

Key Market Opportunity

Development of Lithium Resources Paves the Way for Investment with Surge of Portable Devices

Key players in the lithium hydroxide sector are expected to benefit greatly from the development of lithium resources along with the rising demand for portable electronics. Based on the studies, lithium prices have fluctuated, reaching US$ 13,500 per metric ton in Q1 of 2024, influenced by demand and new mining projects. Countries like Australia, Chile, and China dominate lithium extraction, with Australia alone producing 86,000 metric tons in 2023, supplying the booming electronics and battery industries in the projected period.

The demand for portable devices such as smartphones, tablets, and laptops continues to surge, with over 1.4 billion smartphones shipped in 2023. Lithium-ion batteries using lithium hydroxide offer higher energy density, making them essential for high-performance consumer electronics.

In addition, the rising investments in lithium refining projects aim to increase global supply and ensure price stability in the developed and developing regions. Companies like Albemarle and SQM are expanding operations to meet future demand, creating opportunities for innovation and market expansion in lithium hydroxide production.

Grade Insights

Rise in EV Production Boost the Demand for Battery Grade Lithium Hydroxide with Specialized Advances

On the basis of grade, the lithium hydroxide market is categorized into battery grade and industrial grade, with battery grade lithium hydroxide holding the largest market share of 70% in 2025. The increasing production of electric vehicles and energy storage systems is driving demand for high-purity lithium hydroxide used in nickel-rich cathodes for lithium-ion batteries.

Companies like Albemarle Corporation, SQM, and Ganfeng Lithium are expanding their lithium hydroxide production capacity to meet the growing demand in the projected years. With EV battery demand projected to exceed 6 TWh by 2030, battery-grade lithium hydroxide will remain the dominant segment, driving technical advances in refining and production efficiency.

On the other hand, industrial-grade lithium hydroxide, which holds 30% of the market share in 2025, is widely used in lubricants, ceramics, and chemical applications. It is an essential ingredient in high-temperature greases and glass manufacturing. The demand for ceramic materials and industrial lubricants in aerospace, automotive, and chemical processing industries continues to support industrial-grade consumption.

End Use Industry Type

Need for High-purity Nickel-rich Lithium-Ion Battery Cathodes Attains Prevalence in Consumer Electronics Industry

In 2025, consumer electronics is expected to lead the lithium hydroxide market, holding a market share of 38%. The rising demand for lithium-ion batteries in smartphones, laptops, wearables, and IoT devices is driving growth. With over 1.5 billion smartphones shipped globally in 2023, demand for high-purity battery-grade lithium hydroxide continues to rise. Companies like Apple, Samsung, and Xiaomi are incorporating high-energy-density batteries, increasing lithium consumption.

Following that, the industrial and manufacturing sector, accounting for 22% of the industry, heavily relies on lithium hydroxide for various applications such as lubricants, glass, ceramics, and greases. The global glass industry utilizes lithium for thermal resistance and durability. Additionally, the grease and lubricant industry, growing at 3.8% per annum, uses lithium hydroxide for high-temperature stability in machinery.

As industrial automation and energy storage expand, lithium hydroxide's role in consumer electronics and manufacturing will remain pivotal, ensuring sustained market demand.

Asia Pacific Lithium Hydroxide Market

Rise in Energy Storage Manufacturing in Asia Pacific Fuels the Stabilized Power Grids

Asia Pacific is predicted to lead the global lithium hydroxide market with a 42% share in 2025, driven by increasing demand for lithium-ion batteries in energy storage and EV production. The lithium hydroxide market in Asia Pacific is expected to report a CAGR of 7.2% from 2025 to 2032.

Countries like China, Japan, and South Korea are leading lithium-ion battery manufacturing, with China producing over 75% of the world's lithium-ion batteries in 2023. The rapid expansion of grid-scale energy storage projects to stabilize power grids and support renewable energy sources is fueling demand.

Governments in the region are investing in energy storage solutions. China’s 14th Five-Year Plan aims for over 30 GW of battery storage capacity by 2025, while India plans to install 50 GWh of battery storage by 2030. Such initiatives are boosting lithium hydroxide demand in the forthcoming period.

North America Lithium Hydroxide Market

Innovation in Lithium Extraction and Processing Presents Avenues in North America

In 2025, North America is expected to hold a market share of 27% in the global lithium hydroxide market, driven by advancements in lithium extraction and processing. The region is investing in direct lithium extraction technology, which enhances efficiency and reduces environmental impact compared to traditional mining methods.

U.S. lithium production surged to 5,000 metric tons in 2023, up 25% from 2022, as companies like Albemarle Corporation and Lithium Americas ramp up operations. The U.S. Department of Energy (DOE) has allocated US$ 3.1 Bn for domestic battery material processing, boosting lithium hydroxide output.

Additionally, Tesla’s Texas lithium refinery, opening in 2024, aims to produce 50,000 metric tons of battery-grade lithium hydroxide annually. Such advancements ensure higher resource utilization, reducing reliance on imports and strengthening North America's lithium supply chain. With rising demand for EV batteries and energy storage, the region remains a key growth hub for lithium processing technologies.

Europe Lithium Hydroxide Market

Surge in Consumer Electronics in Europe Support the Demand for Lithium-Ion Batteries

In 2025, Europe remains a key player in the lithium-ion battery market, driven by the growing consumer electronics sector. The demand for lithium hydroxide is rising due to its role in enhancing battery performance and lifespan. Europe’s smartphone shipments reached 195 million units in 2023, while laptop and tablet sales surged due to remote work trends. The region is also seeing increased demand for wearables, with smartwatch shipments growing by 18% year-over-year.

Leading companies like Samsung, Apple, and Xiaomi continue expanding their presence in the region, boosting lithium-ion battery consumption. The EU’s Battery Regulation, implemented in 2024, promoting sustainable and high-performance battery production, is driving demand for lithium hydroxide. This underscores Europe's growing consumer electronics and battery market on a global scale.

Leading manufacturers of lithium hydroxide are projected to significantly increase their production capabilities by strategically establishing factories and supply chain outlets in regions experiencing high demand.

As the electric vehicle industry is poised for substantial growth, driving the need for lithium-based products in battery component manufacturing, several companies are likely to broaden their consumer engagement by expanding their distribution networks closer to EV production facilities.

Such a proactive approach not only aims to meet the rising demand but also enhances logistical efficiency, ensuring timely delivery of essential materials to support the burgeoning electric vehicle market.

Key Industry Developments

|

Report Attributes |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Grade

By End Use Industry

By Region

To know more about delivery timeline for this report Contact Sales

The market is set to reach US$ 25.15 Bn in 2025.

In 2023, Australia, the world's largest lithium producer, produced 86,000 metric tons.

Livent Corporation, Sociedad Química y Minera de Chile (SQM), Albemarle Corporation, and Ganfeng Lithium Co., Ltd. are a few leading players.

The industry is estimated to rise at a CAGR of 6.7% through 2032.

Asia Pacific is projected to hold the largest share of the industry in 2025.