Industry: Energy & Utilities

Published Date: March-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 250

Report ID: PMRREP35146

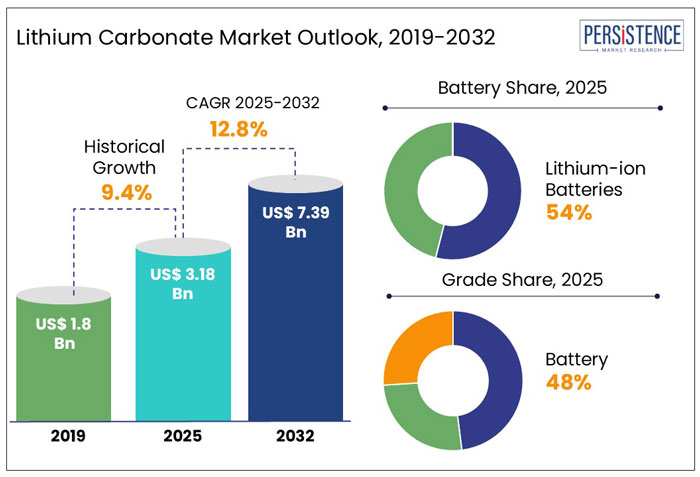

The global lithium carbonate market size is anticipated to rise from US$ 3.18 Bn in 2025 to US$ 7.39 Bn by 2032. It is projected to witness a CAGR of 12.8% from 2025 to 2032.

Not long ago, lithium carbonate was the undisputed king of the battery world. It was the fuel behind the electric vehicle (EV) revolution, the backbone of the energy storage movement.

The lithium carbonate market has experienced significant fluctuations recently, reflecting the dynamic nature of global industries and consumer behaviors.

As per the reports by Persistence Market Research 2024, global lithium production increased by 23% to approximately 180,000 tons, while consumption rose by 27% to 180,000 tons.

This imbalance led to a significant price drop, with spot lithium carbonate prices in China decreasing from about US$76,000 per ton in January to around US$23,000 per ton in November 2024.

Key Highlights of the Lithium Carbonate Market

|

Global Market Attributes |

Key Insights |

|

Lithium Carbonate Market Size (2025E) |

US$ 3.18 Bn |

|

Market Value Forecast (2032F) |

US$ 7.39 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.4% |

Electric Vehicle Revolution Skyrocketed the Demand for Lithium Carbonate

For years, lithium carbonate was the golden ticket of the energy revolution. Before 2024, demand for lithium carbonate was skyrocketing, fueled by the electric vehicle (EV) boom, the expansion of energy storage, and governments worldwide pushing for a clean energy transition.

Prices soared past US$76,000 per ton in early 2024, making lithium mining one of the most lucrative businesses on the planet.

By late 2024, an oversupply crisis emerged. China had ramped up production too aggressively, while EV sales, though growing, failed to match the hype. Prices crashed nearly 70%, forcing companies to shut down plants and rethink their strategies. Miners, once riding high, suddenly faced an existential crisis.

Innovations in Battery Technology to Bolster Market Prospects

While the market struggles in 2025, the long-term story is far from over. By 2032, demand is expected to double, driven by innovations in battery technology and energy storage. The winners will be companies that survive the downturn, invest in sustainable mining, and secure new markets.

Growth Driver

The EV Revolution is Powering the Future on Lithium

Imagine a world where gas stations are relics of the past, replaced by sleek EV chargers on every street corner. That world is coming fast, and lithium carbonate is at the heart of it.

Before 2024, skyrocketing EV demand fueled lithium’s price surge, but a slowdown in sales led to a market crash in 2024-2025. However, the bigger picture remains unchanged, where EV adoption only increases.

With governments worldwide setting aggressive carbon reduction goals, automakers are racing to produce cheaper, longer-range EVs. Companies like Tesla, BYD, and Volkswagen are investing billions in battery technology, ensuring that demand for lithium carbonate remains strong.

By 2030, global EV sales are projected to double, meaning today’s oversupply will become tomorrow’s supply crunch. Those who can weather the storm and secure long-term contracts will drive the future of transportation.

The Cost Volatility Trap and Uncertainty are Major Market Restraints

Imagine investing in a market where prices can triple in one year and crash by 70% the next, which is a fact for the lithium carbonate market.

As per the reports, before 2024, prices soared past US$76,000 per ton, making lithium mining one of the most profitable businesses on Earth. But by late 2024, oversupply flooded the market, sending prices plummeting.

Automotive and battery manufacturers need stability, but lithium’s price swings make planning difficult. When prices are high, companies rush to mine more, but demand cools down when production scales up, triggering another crash.

For lithium carbonate to reach its true potential, the industry must find balance through better supply chain coordination or government policies that stabilize prices. Until then, this volatility will keep investors and buyers on edge, slowing down expansion plans.

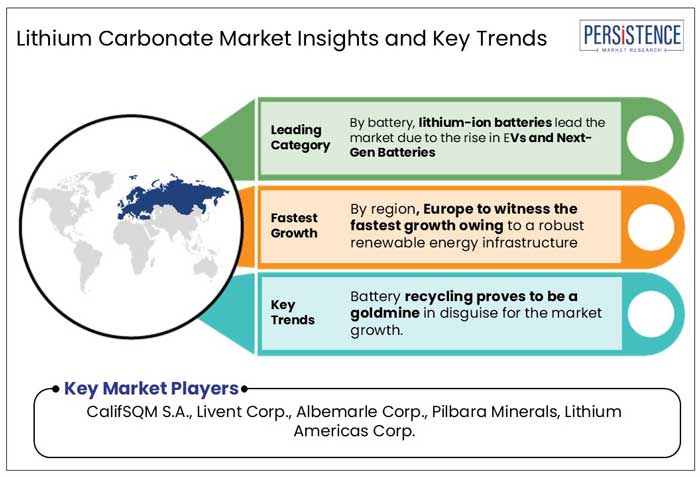

Battery Recycling Proves to be a Goldmine in Disguise for Market Growth

Every year, millions of EV batteries inch closer to the end of their lifespan, creating both a challenge and an opportunity. Instead of mining fresh lithium, the booming world of lithium-ion battery recycling has emerged, which presents key opportunities for the market players.

Industry leaders like Redwood Materials and Li-Cycle are proving that recycling can be both sustainable and profitable. New technologies now allow over 95% of lithium to be recovered from used batteries, creating a secondary market for lithium carbonate.

Recycling reduces reliance on environmentally damaging mining and provides a stable supply of lithium at lower costs. As governments push for circular economies and companies like Tesla and GM invest in closed-loop battery production, lithium recycling could soon become a multi-billion-dollar industry.

Battery Insights

EVs and Next-Gen Batteries Are Fueling the Future of Lithium-ion Batteries

Lithium-ion batteries led the market, accounting for a massive 54% of global revenue. Their widespread use in EVs, renewable energy storage systems, and consumer electronics has fueled an insatiable demand for lithium carbonate.

As governments and automotive manufacturers push for clean energy adoption, the need for high-performance batteries is only growing stronger. A new battery technology, lithium-metal batteries (LMBs), is on the rise, offering higher energy density, longer battery life, and lighter weight.

Experts predict that the lithium-metal battery market will grow at an impressive CAGR of 15.1% in the coming years, potentially reshaping the entire energy storage industry. As the race for clean energy and battery innovation accelerates, companies that secure a steady lithium carbonate supply will be the true winners of the future.

Grade Insights

Battery Grade Segment to Dominate with 48% of the Market Share

The expansion of renewable energy sources, especially solar and wind, drives the demand for battery-grade lithium carbonate.

As alternative energy sources gain prominence, there is an increasing demand for energy storage systems to stabilize the grid and provide a dependable electricity supply. Lithium carbonate of battery-grade quality is essential for high-performance batteries utilized in extensive energy storage systems, where efficiency and dependability are crucial.

The rising investments in grid-scale energy storage and off-grid applications, particularly in nations prioritizing renewable energy integration, propel the need for battery-grade lithium carbonate.

Asia Pacific Region Dominates with 34% of the Market Share with its Dominance in Electric Vehicle Manufacturing

The Asia Pacific lithium carbonate market is witnessing substantial expansion, propelled by the region's dominance in electric vehicle (EV) adoption and manufacturing.

Countries such as China, Japan, and South Korea are leaders in electric vehicle manufacturing. The rising demand for electric vehicles is escalating the requirement for lithium-ion batteries, which are predominantly dependent on lithium carbonate.

Regional governments facilitate the rise of electric vehicles through policies, subsidies, and the creation of manufacturing hubs, expediting market expansion. The demand for the product is increasing in response to the escalating manufacturing of EV batteries.

Favourable Policies and Subsidies Aid North American Lithium Carbonate Market

The North American lithium carbonate market is primarily driven by the region's expanding electric vehicle (EV) industry. Governments around the U.S. and Canada are implementing tax incentives, subsidies, and favourable rules to promote electric vehicle adoption, hence augmenting demand for EV battery production.

Prominent automotive manufacturers are increasing expenditures in North America's electric vehicle production facilities, enhancing the demand for domestically derived lithium carbonate. The growing utilization of renewable energy sources is a primary catalyst for the U.S. lithium carbonate market.

Lithium-ion batteries, crucial for energy storage devices, are extensively utilized to store solar and wind energy. This trend corresponds with the U.S. government's aggressive renewable energy objectives, enhancing industry demand.

Furthermore, expanding grid storage solutions, essential for stabilizing energy distribution networks, has increased the demand for high-quality battery materials, such as lithium carbonate.

Europe to Witness the Fastest Growth Owing to a Robust Renewable Energy Infrastructure

Europe is anticipated to see swift expansion, mostly propelled by the nation's commitment to establishing a resilient renewable energy infrastructure.

The demand for energy storage devices, crucial for balancing intermittent renewable energy sources such as wind and solar power, is rising throughout the region.

Lithium-ion batteries, utilizing lithium carbonate, are crucial for these storage solutions, rendering the market indispensable to the region's green energy transition.

The EU's Green Deal and related programs aimed at decarbonizing energy sectors enhance the demand for lithium carbonate in energy storage applications.

In the highly competitive market of lithium carbonate, industry giants are racing to secure lithium reserves, build processing plants, and dominate global supply chains.

With EV demand surging, the companies that can innovate, scale, and secure resources will be the true winners in this race for the future. China's position as the world's largest producer of lithium-ion batteries contributes to nearly 75% of global production.

As demand for lithium carbonate surges, companies that diversify supply chains, develop sustainable mining methods and invest in recycling will gain a competitive edge. With new lithium discoveries and technological breakthroughs on the horizon, the race for lithium supremacy is far from over. It's only getting started.

Key Industry Developments

|

Report Attributes |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Battery

By Grade

By Application

By Region

To know more about delivery timeline for this report Contact Sales

The market is set to reach US$ 3.18 Bn in 2025.

SQM S.A., Livent Corp., Albemarle Corp., are a few leading players.

The industry is estimated to rise at a CAGR of 12.8% through 2032.

China is the largest buyer of Lithium globally.

The market for is anticipated to reach a valuation of US$ 7.39 billion by 2032.