- Pharmaceuticals

- Human Insulin Market

Human Insulin Market Size, Share, and Growth Forecast 2026 - 2033

Human Insulin Market by Product Type (Short-Acting, Intermediate-Acting, Long-Acting, Premixed), Delivery Device (Pens, Syringes, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis, 2026–2033

Human Insulin Market Trends and Analysis

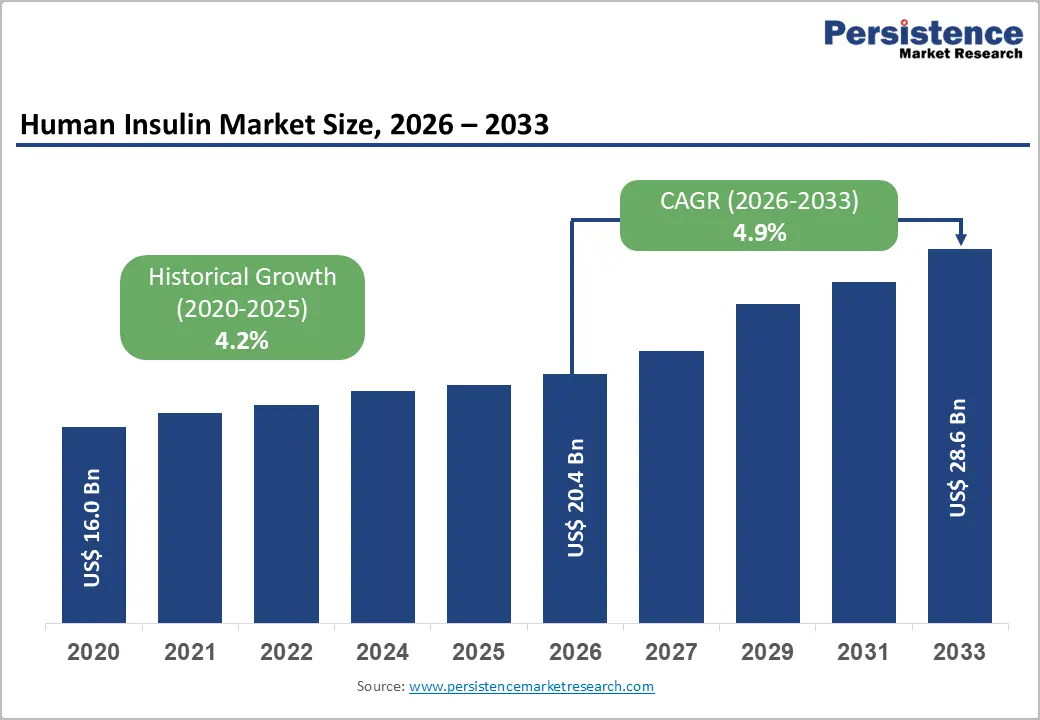

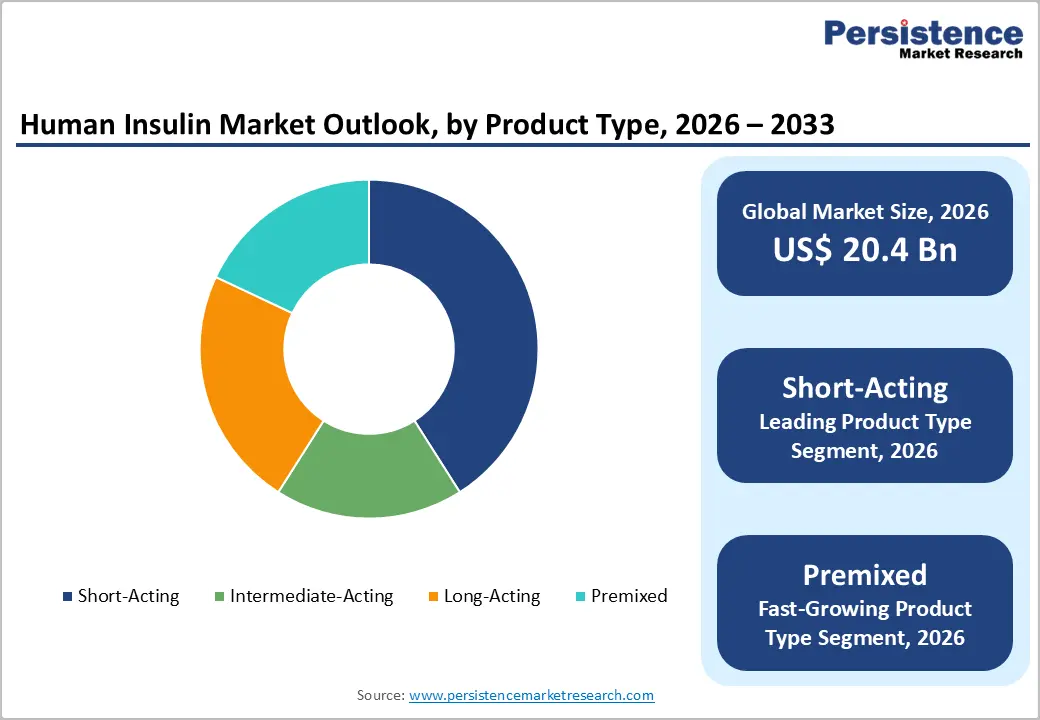

The global human insulin market size is expected to be valued at US$ 20.4 billion in 2026 and projected to reach US$ 28.6 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033. The global rise of diabetes with the International Diabetes Federation (IDF) estimating 537 million adults living with diabetes in 2021, projected to reach 783 million by 2045.

Human insulin remains the most widely prescribed and accessible insulin formulation globally, particularly in price-sensitive emerging economies where biosimilar and generic human insulin products dominate formulary selections. Expanding universal health coverage programs, rising diabetes screening rates, and the rollout of affordable insulin access initiatives by organizations, including the WHO, are further reinforcing consistent demand growth across all geographic segments.

Key Industry Highlights

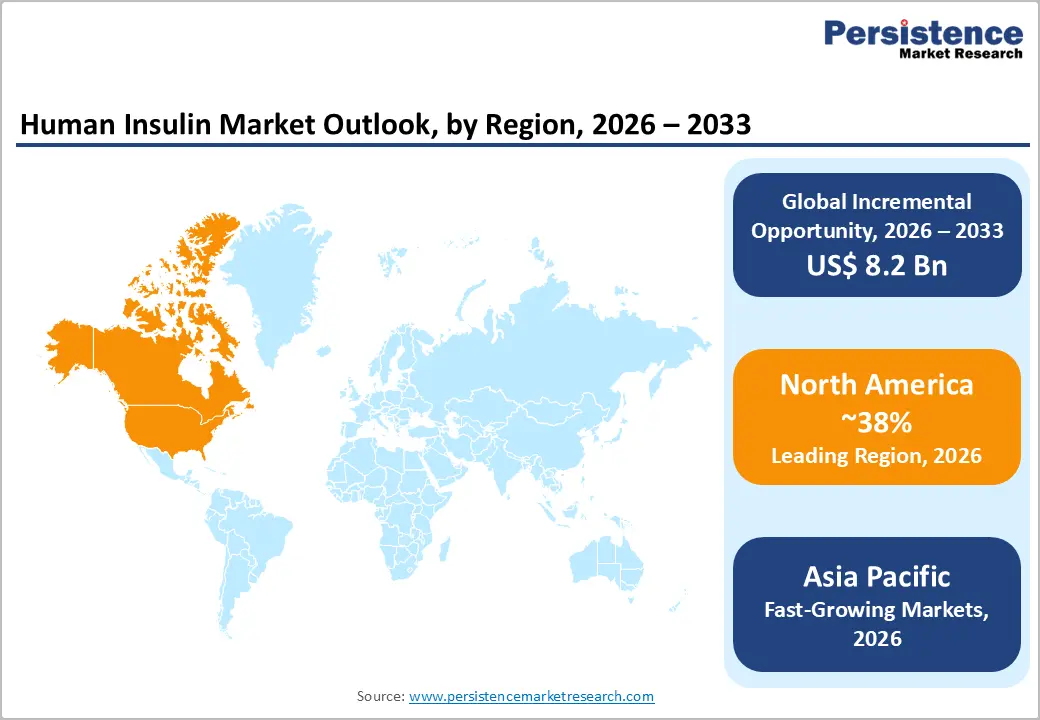

- Regional Leadership: North America leads the global human insulin market with approximately 38% share in 2025, driven by over 37 million U.S. diabetes patients per CDC data, robust Medicare/Medicaid insulin reimbursement, and pricing reform under the Inflation Reduction Act.

- Fast-growing Market: Asia Pacific is the fastest-growing regional market, home to over 140 million Chinese diabetics per IDF data and 101 million in India, with domestic manufacturers Tonghua Dongbao and Biocon Limited expanding affordable human insulin access.

- Leading Product: Short-acting human insulin dominates the product type segment with approximately 41% share in 2025, reinforced by the WHO Essential Medicines List inclusion, mandatory national formulary presence across 150+ countries, and significant cost advantage versus insulin analogue alternatives.

- Fast-growing Product Type: Premixed human insulin is the fastest-growing product type, driven by dosing simplicity for type 2 diabetes management in primary care settings across Asia-Pacific and Africa, supported by WHO Essential Medicines List inclusion and national diabetes program procurement priorities.

- The key market opportunity lies in biosimilar human insulin expansion in price-sensitive emerging markets with only 20% of people with diabetes in low-income countries accessing adequate insulin per Access to Medicine Foundation combined with connected pen delivery device integration to improve adherence.

Market Dynamics

Market Growth Drivers

Escalating Global Diabetes Burden Driving Insulin Demand

The exponential growth of the global diabetes population is the single most powerful structural driver of the human insulin market. According to the International Diabetes Federation (IDF) Diabetes Atlas, 10th Edition, approximately 537 million adults were living with diabetes in 2021, with type 2 diabetes accounting for over 90% of cases. The WHO projects that diabetes will be the seventh leading cause of death globally by 2030. Low- and middle-income countries account for approximately 80% of global diabetes cases, where human insulin given its significantly lower price point compared to insulin analogues remains the primary pharmacological treatment option. Rising diabetes screening rates under national health programs and the progressive expansion of insulin access initiatives under the WHO's Essential Medicines List are directly translating into sustained prescription volume growth for human insulin formulations.

Expanding Biosimilar Human Insulin Access in Emerging Markets

The proliferation of biosimilar and follow-on human insulin products from manufacturers in India, China, and Eastern Europe is substantially expanding treatment access in price-sensitive emerging markets, driving volume-led market growth. Biocon Limited and Wockhardt Ltd. in India, along with Tonghua Dongbao Pharmaceutical Co., Ltd. and Gan & Lee Pharmaceuticals in China, have established significant manufacturing scale at competitive price points enabling broader formulary access. The U.S. FDA's biosimilar approval pathway under the Biologics Price Competition and Innovation Act (BPCIA) has facilitated entry of biosimilar insulin products even in high-income markets. According to the Access to Medicine Foundation, pricing competition from biosimilar manufacturers is improving affordability metrics across Sub-Saharan Africa and Southeast Asia.

Market Restraints

Competition from Premium Insulin Analogues Eroding Human Insulin Market Share

The progressive clinical migration toward insulin analogues including long-acting basal insulins (insulin glargine, insulin detemir, insulin degludec) and rapid-acting analogues is exerting downward pressure on human insulin prescription share in developed markets. According to the American Diabetes Association (ADA) Standards of Medical Care in Diabetes guidelines, insulin analogues are generally preferred over human insulin for their reduced hypoglycemia risk and more predictable pharmacokinetic profiles. In the U.S. and Western Europe, insulin analogue prescriptions significantly outnumber human insulin prescriptions, constraining the latter's revenue growth trajectory in high-value markets.

Insulin Affordability Crisis and Policy-Driven Price Constraints

Paradoxically, the global push for insulin affordability while expanding access simultaneously constrains market revenue growth through aggressive price regulation and reference pricing mechanisms. The U.S. Inflation Reduction Act (IRA) of 2022 capped insulin co-payments at US$ 35 per month for Medicare beneficiaries, directly compressing manufacturer revenues. In developing markets, government tender pricing processes and price control regulations in countries including India and Brazil set official ceiling prices that limit commercial pricing flexibility, moderating overall market value expansion despite robust volume growth.

Market Opportunities

Premixed Human Insulin Growth in Type 2 Diabetes Management in Emerging Markets

Premixed human insulin formulations represent the fastest-growing product type segment, driven by their clinical convenience of combining short- and intermediate-acting insulin in a fixed ratio simplifying dosing regimens for type 2 diabetes patients in resource-constrained healthcare settings. The IDF projects that Asia-Pacific will account for the majority of new diabetes cases through 2045, with large populations in India, China, and Southeast Asia managing type 2 diabetes through primary care channels where simplified dosing protocols are critical for adherence. Premixed formulations from manufacturers including Novo Nordisk A/S (Novolin 70/30) and Sanofi are gaining adoption through national essential medicines programs. The WHO Essential Medicines List inclusion of intermediate-acting and premixed human insulin reinforces their procurement priority across public health systems globally.

Digital Health Integration and Smart Delivery Device Expansion

The integration of connected insulin delivery devices including smart insulin pens with dose capture and Bluetooth data transmission to diabetes management apps represents a growing commercial opportunity for human insulin manufacturers to differentiate commodity formulations through device-centric value propositions. Novo Nordisk A/S and Eli Lilly and Company have both invested in connected pen ecosystems designed for integration with digital health platforms. The American Diabetes Association (ADA) has increasingly endorsed digital diabetes management tools in its clinical standards. With global smartphone penetration exceeding 6.8 billion users in 2023 per Statista, mobile-connected insulin delivery devices offer a practical pathway to improve adherence and clinical outcomes, creating premium positioning opportunities for device-bundled human insulin offerings.

Category-wise Insights

Product Type Analysis

Short-acting human insulin leads the product type segment with approximately 41% of total market share in 2025. Regular human insulin (short-acting) remains the most widely prescribed and accessible insulin formulation globally, underpinned by its inclusion on the WHO Essential Medicines List and its mandatory presence in national formularies across over 150 countries. Its cost advantage versus rapid-acting insulin analogues typically priced 30–50% lower makes short-acting human insulin the default prescription choice across public health systems in Africa, South Asia, and Latin America. The IDF highlights that short-acting regular insulin is the primary prandial insulin available in most low-income country primary care settings. Despite analogue competition in high-income markets, short-acting human insulin retains dominant prescription volumes through the public healthcare procurement systems that serve the majority of the world's insulin-dependent population.

Delivery Device Analysis

Insulin pens constitute the leading delivery device segment in the human insulin market, accounting for approximately 55% of total delivery device share in 2025. The pen segment's leadership reflects its clinically validated advantages in dosing accuracy, patient convenience, portability, and improved adherence versus traditional vial-and-syringe administration. Clinical studies published in Diabetes Technology & Therapeutics confirm that pen users demonstrate significantly better dose accuracy and injection compliance compared to syringe users, particularly among elderly and vision-impaired patients. Novo Nordisk A/S and Sanofi have built comprehensive pen device ecosystems bundled with their human insulin formulations. While syringes retain relevance in hospital settings and cost-sensitive markets, the broad global transition toward pen-based delivery in both developed and emerging markets is sustaining the segment's dominant position.

Distribution Channel Analysis

Retail pharmacies represent the leading distribution channel for human insulin, capturing approximately 48% of total channel share in 2025. As a chronic disease requiring continuous long-duration pharmacotherapy, insulin dispensing aligns naturally with the community retail pharmacy model, which offers geographic accessibility, patient counseling support, and prescription refill convenience. Major pharmacy chains including CVS Health, Walgreens Boots Alliance, and Apollo Pharmacy (India) provide critical last-mile insulin access. In many developing markets, community pharmacies and drug stores serve as the primary insulin access point outside hospital settings. Hospital pharmacies hold a significant share for newly diagnosed patients initiating insulin therapy, while online pharmacy channels are growing rapidly, particularly in North America and Asia-Pacific, driven by direct-to-patient delivery convenience and competitive pricing.

Regional Insights

North America Human Insulin Market Trends and Insights

North America leads the global human insulin market with approximately 38% of total market share in 2025, driven by the United States' large diabetic patient population, established reimbursement coverage under Medicare and Medicaid, and active legislative interventions to improve insulin affordability under the Inflation Reduction Act (IRA). The region's premium drug pricing environment sustains high revenue per unit despite increasing biosimilar competition.

U.S. Human Insulin Market Size

The United States accounts for approximately 86% of the North American human insulin market in 2025. The CDC estimates over 37 million Americans have diabetes, with insulin dependency spanning both type 1 and advanced type 2 populations. The IRA's US$ 35 monthly insulin cap and biosimilar entry from Civica Rx are reshaping the pricing landscape while sustaining volume growth.

Europe Human Insulin Market Trends and Insights

Europe represents a mature and well-regulated human insulin market, governed by the European Medicines Agency (EMA) and characterized by robust national health technology assessment (HTA) processes controlling formulary access. Biosimilar human insulin products have achieved strong penetration across cost-conscious national health systems, particularly in Germany and the U.K., where reference pricing frameworks systematically favor generic and biosimilar formulations.

Germany Human Insulin Market Size

Germany leads the European human insulin market, representing approximately 20% of regional share in 2025. Germany's statutory health insurance (GKV) framework and mandatory AMNOG benefit assessment processes drive formulary adoption of cost-competitive biosimilar human insulins, with Biocon Limited's biosimilar insulin portfolio gaining significant traction through the Viatris partnership.

U.K. Human Insulin Market Size

The United Kingdom accounts for approximately 16% of the European market in 2025. The NHS procurement frameworks strongly favor cost-effective human insulin formulations, with NICE guidance supporting human insulin use in type 2 diabetes patients when analogue clinical benefits are not established. The Diabetes UK advocacy ecosystem further supports access improvement initiatives.

France Human Insulin Market Size

France accounts for approximately 14% of the European human insulin market in 2025. The Haute Autorité de Santé (HAS) governs insulin reimbursement decisions, with human insulin formulations maintaining strong formulary positions in type 2 diabetes management. France's Assurance Maladie provides broad insulin coverage, sustaining consistent prescription volumes across primary and specialist care channels.

Asia Pacific Human Insulin Market Trends and Insights

Asia-Pacific is the fastest-growing regional market for human insulin, home to the world's largest and fastest-expanding diabetic population. China alone has over 140 million people with diabetes per IDF estimates, with domestic manufacturers Tonghua Dongbao and Gan & Lee Pharmaceuticals capturing growing market share through competitive pricing and government tender procurement programs aligned with China's Healthy China 2030 initiative.

India Human Insulin Market Size

India represents approximately 20% of Asia-Pacific market share in 2025, anchored by its massive diabetic population of over 101 million per IDF 2021 data and the domestic manufacturing advantage of companies including Biocon Limited and Wockhardt Ltd. India's price-controlled pharmaceutical environment and government health schemes drive large-volume human insulin procurement.

Competitive Landscape

The global human insulin market is moderately consolidated, dominated by three innovator companies — Novo Nordisk A/S, Sanofi, and Eli Lilly and Company which collectively hold over 60% of the global insulin market. A competitive biosimilar tier, led by Biocon Limited, Gan & Lee Pharmaceuticals, and Tonghua Dongbao, challenges on price in emerging markets. Key differentiators include device ecosystems, regulatory approvals across major markets, cold-chain distribution networks, and government tender relationships. Emerging business models focus on DTC digital diabetes management platforms bundling insulin with connected pen devices and telehealth coaching services.

Key Developments

- In May 2026, Aspen Pharmacare received final approval from the South African Health Products Regulatory Authority (SAHPRA) to begin commercial sales of its first locally manufactured human insulin from its Gqeberha sterile facility under its partnership with Novo Nordisk.

- In January 2026, MannKind received U.S. FDA approval for an updated prescribing label for Afrezza (insulin human) Inhalation Powder, revising the starting mealtime dose guidance for adult patients switching from multiple daily injections (MDI) or insulin pump mealtime therapy to inhaled insulin.

Companies Covered in Human Insulin Market

- Novo Nordisk A/S

- Eli Lilly and Company

- Sanofi

- Biocon Limited

- Wockhardt Ltd.

- Julphar

- Tonghua Dongbao Pharmaceutical Co., Ltd.

- Gan & Lee Pharmaceuticals

- BIOTON S.A.

- Boehringer Ingelheim

- Merck & Co., Inc.

- Pfizer Inc.

Frequently Asked Questions

The global human insulin market is estimated to be valued at US$ 20.4 billion in 2026.

The primary demand drivers are the global diabetes epidemic with the IDF reporting 537 million adults living with diabetes in 2021 the WHO Essential Medicines List inclusion of human insulin mandating public system procurement across 150+ countries, expanding biosimilar manufacturer competition from India and China, and universal health coverage expansion improving insulin access in low- and middle-income countries.

North America leads the global human insulin market with approximately 38% of total market share in 2025. The United States' estimated 37 million diabetes patients per CDC data, comprehensive Medicare/Medicaid reimbursement, the Inflation Reduction Act's US$ 35 monthly insulin cap, and the headquarters presence of Novo Nordisk, Sanofi, and Eli Lilly collectively underpin regional market leadership.

The most significant opportunity lies in expanding affordable human insulin access in emerging markets where the Access to Medicine Foundation confirms only 20% of low-income country diabetes patients access adequate insulin through biosimilar manufacturing scale-up in India and China, combined with connected smart pen delivery device integration enabling improved adherence and digital diabetes management in growing Asia-Pacific markets.

The key market players include Novo Nordisk A/S, Sanofi, Eli Lilly and Company, Biocon Limited, Wockhardt Ltd., Tonghua Dongbao Pharmaceutical Co., Ltd., Gan & Lee Pharmaceuticals, Julphar, BIOTON S.A., Boehringer Ingelheim, Merck & Co., Inc., and Pfizer Inc., among others competing across innovator brand, biosimilar, and generic human insulin formulation segments globally.