- Healthcare Services

- Human Platelet Lysate Market

Human Platelet Lysate Market Size, Share, and Growth Forecast 2026 - 2033

Human Platelet Lysate Market by Product Type (Heparin-Based Human Platelet Lysate, Heparin-Free Human Platelet Lysate), by Application (Cell Therapy, Stem Cell Expansion, Regenerative Medicine, Tissue Engineering, Drug Discovery, Research Applications, Others), End-user (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Hospitals & Diagnostic Laboratories, Cell Banks, Others), and Regional Analysis, 2026 - 2033

Human Platelet Lysate Market Share and Trends Analysis

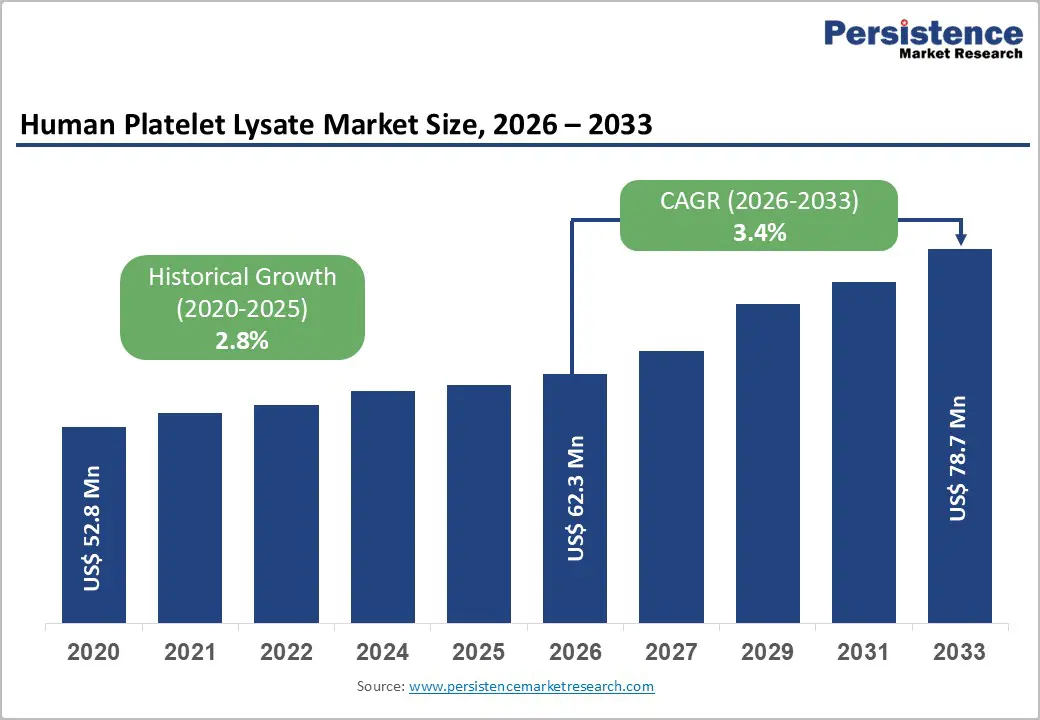

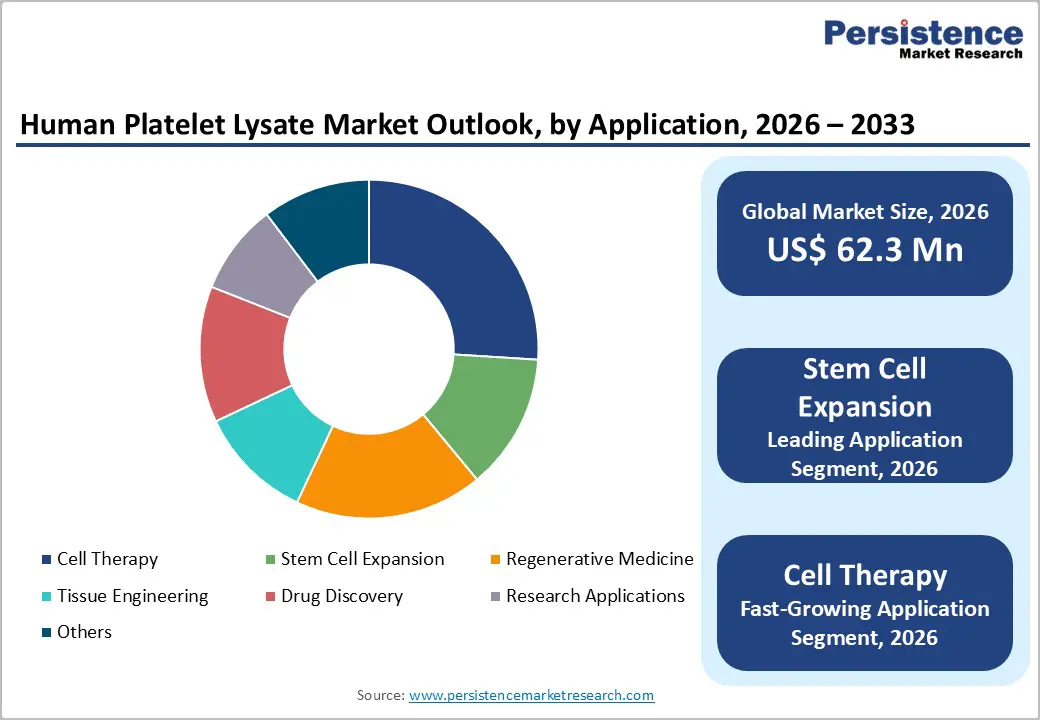

The global human platelet lysate market size is expected to be valued at US$ 62.3 million in 2026 and projected to reach US$ 78.7 million by 2033, growing at a CAGR of 3.4% between 2026 and 2033. This steady growth is primarily driven by the accelerating adoption of human platelet lysate (hPL) as a clinically safer, xeno-free alternative to fetal bovine serum (FBS) in cell culture and expansion workflows for advanced therapy medicinal products (ATMPs).

Regulatory pressure from the European Medicines Agency (EMA) and the U.S. FDA to minimize animal-derived components in cell therapy manufacturing, combined with the rapidly expanding global pipeline of CAR-T cell therapies and mesenchymal stem cell (MSC)-based regenerative medicine products, is creating structural demand for qualified hPL supplements across pharmaceutical, biotech, and academic research end-users.

Key Industry Highlights

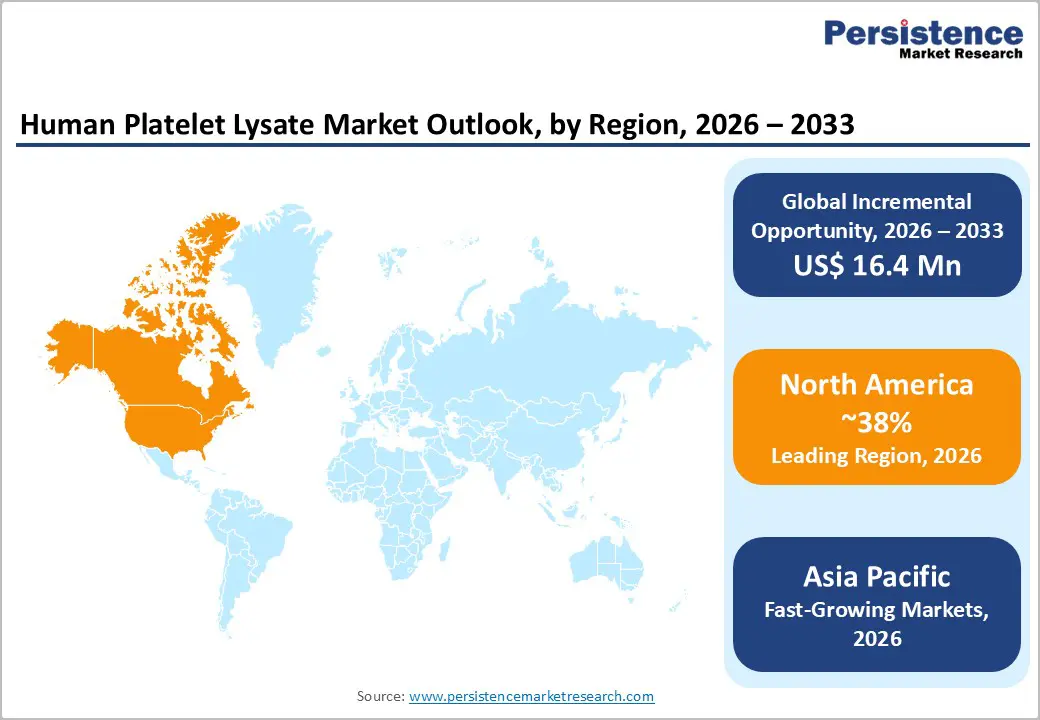

- Leading Region - North America holds approximately 38% of global market share in 2025, driven by FDA-approved CAR-T therapy commercial manufacturing demands, NIH NCATS-funded cell therapy infrastructure, and the U.S. leadership in regenerative medicine clinical trial activity per ARM's 2023 Annual Report

- Fast-Growing Market- Asia Pacific is the fastest-growing region, propelled by China's NMPA ATMP guideline alignment with EMA standards, Japan's AMED-funded regenerative medicine programs, South Korea's cell therapy pipeline, and Singapore's A*STAR-anchored biomedical manufacturing hub.

- Dominant Product Segment - Heparin-Free formulations lead with approximately 55% share in 2026, driven by FDA and EMA ATMP guidance minimizing adventitious agents, the 2008 heparin contamination precedent, and validated equivalent MSC expansion performance published in Cytotherapy and Transfusion journals.

- Fast-Growing Application - Cell therapy is the fast-growing application, driven by ARM-documented 2,000+ regenerative medicine clinical trials, commercial CAR-T scale-up by Novartis, Gilead/Kite, and BMS, and EMA ATMP mandates requiring xeno-free GMP manufacturing conditions.

Market Dynamics

Drivers - Regulatory Shift Toward Xeno-Free Cell Culture Media Accelerating hPL Adoption

Growing regulatory and ethical pressure to eliminate animal-derived components from cell therapy manufacturing is the primary structural driver for human platelet lysate adoption. Both the EMA's Advanced Therapy Medicinal Products (ATMP) guidelines and the FDA's Guidance for Human Somatic Cell Therapy emphasize minimizing the use of animal-origin raw materials, including FBS, to reduce risks of xenogeneic immune reactions and pathogen transmission in clinical cell therapy products.

Published comparative studies in the Cytotherapy journal have demonstrated that hPL supports equivalent or superior mesenchymal stromal cell (MSC) proliferation compared to FBS while yielding clinical-grade cell products more acceptable to regulatory authorities. The European Blood Alliance (EBA) and International Society for Cell & Gene Therapy (ISCT) have both issued position statements supporting hPL as a preferred FBS alternative, reinforcing regulatory and scientific consensus around the transition.

Restraints - Lot-to-Lot Variability and Standardization Challenges Limiting Clinical Confidence

A fundamental technical challenge constraining broader hPL adoption is the inherent biological variability between production lots derived from different donor pools. Unlike chemically defined synthetic media supplements, hPL's composition including growth factor concentrations, platelet count, and residual plasma proteins, varies between batches, creating concerns about process reproducibility for GMP cell manufacturing. The U.S. Pharmacopeia (USP) and European Pharmacopoeia (Ph. Eur.) do not yet have fully harmonized hPL monographs, and the absence of standardized characterization requirements across regulatory jurisdictions adds complexity to qualification and regulatory submission processes for cell therapy developers.

Limited Plasma Donation Infrastructure and Supply Scalability Constraints

Human platelet lysate production depends on a consistent supply of human platelet concentrates primarily from blood donation centers, creating an inherent supply constraint tied to blood donation rates and plasma collection infrastructure. The WHO reports that global voluntary blood donation rates vary enormously between high-income and low-income countries, with a significant supply-demand gap in developing markets. As cell therapy manufacturing scales toward commercial volumes requiring increasingly large quantities of GMP-grade hPL, supply chain security and geographic production distribution become critical commercial constraints that favor established players with dedicated blood bank partnerships over new entrants.

Opportunities - Cell Therapy Manufacturing Scale-Up: The Fastest-Growing Application Segment

Cell therapy manufacturing represents the fastest-growing and highest-value application for human platelet lysate, driven by the commercial approval and clinical scale-up of CAR-T cell therapies and the expanding MSC-based therapeutic pipeline. The ARM's 2023 Annual Report identified over 2,000 active regenerative medicine clinical trials globally, with cell therapies comprising the majority.

As approved CAR-T therapies scale up commercial manufacturing with single-patient manufacturing costs in the range of USD 50,000-100,000 per batch, the quality and consistency of expansion media supplements, including hPL, become critical GMP parameters. EMA ATMP guidelines explicitly recommend minimizing FBS use in clinical manufacturing, creating a direct regulatory mandate for hPL integration. Companies including Merck KGaA, Stemcell Technologies, and PL BioScience GmbH are expanding GMP-certified hPL production capacity specifically to serve the growing clinical cell therapy market, where premium pricing for certified xeno-free supplements is commercially viable.

Heparin-Free hPL Innovation: Addressing Key Safety Concerns for Broader Clinical Application

Heparin-free human platelet lysate formulations represent a high-growth product innovation opportunity, directly addressing safety concerns associated with heparin, an anticoagulant used in traditional hPL preparation that can cause heparin-induced thrombocytopenia (HIT) in sensitive patient populations and introduce immunological confounders in cell therapy products.

Published clinical and preclinical research demonstrates that heparin-free hPL maintains equivalent cell expansion performance to heparin-based formulations while eliminating heparin-related risk vectors. The FDA and EMA have both flagged heparin sourcing transparency as a regulatory concern, particularly following the 2008 heparin contamination crisis, elevating the appeal of heparin-free alternatives. Companies including PL BioScience GmbH and AventaCell BioMedical have commercialized heparin-free hPL products, and growing awareness among cell therapy developers of the clinical and regulatory advantages positions heparin-free formulations as a structurally superior and premium-priced product tier within the broader hPL market.

Category-wise Analysis

Product Type Insights

Heparin-Free human platelet lysate is the leading and increasingly dominant product type segment, estimated at approximately 55% of global share in 2026, having displaced Heparin-Based formulations as the clinical and GMP manufacturing preference. This transition reflects the combined impact of FDA and EMA regulatory guidance emphasizing the elimination of adventitious agents and immunological risks in cell therapy raw materials.

Published studies in Transfusion and Cytotherapy journals confirm that heparin-free hPL achieves equivalent or superior MSC expansion outcomes compared to heparin-based alternatives, while the 2008 global heparin contamination crisis elevated regulatory vigilance around heparin sourcing. PL BioScience GmbH's GMP-certified heparin-free hPL platform and Merck KGaA's clinical-grade xeno-free supplement portfolio have become benchmark products for GMP cell therapy manufacturing, reinforcing heparin-free formulations' structural market leadership.

Application Insights

Stem cell expansion leads the Application category with approximately 26% market share in 2026. Human platelet lysate's proven ability to support robust, reproducible expansion of mesenchymal stromal/stem cells (MSCs) at clinically relevant scales has established it as the preferred culture supplement for this foundational application. Multiple studies in Stem Cell Research & Therapy confirm superior MSC proliferation rates and preserved multipotency using hPL versus FBS, aligning with ISCT consensus statements recommending xeno-free culture conditions for clinical-grade MSC production. The global MSC clinical trial pipeline, with the ARM reporting MSCs among the most clinically investigated cell therapy modalities, ensures sustained volume demand. Cell Therapy is the fastest-growing application, reflecting the commercial scale-up of CAR-T and other clinical cell therapy programs requiring GMP-grade hPL for T-cell, NK cell, and tumor-infiltrating lymphocyte (TIL) expansion.

End-user Insights

Pharmaceutical & biotechnology companies represent the leading enduser segment with an estimated 42% global share in 2026. This dominance reflects the critical role of GMP-grade hPL in commercial cell therapy manufacturing, where product quality consistency directly impacts clinical outcomes and regulatory submissions. Companies manufacturing approved CAR-T products, allogeneic cell therapies, and MSC-based ATMPs represent the highest-value per-unit hPL customers, requiring large volumes of certified, fully characterized, and traceable hPL preparations.

Academic & Research Institutes represent the second-largest segment, driven by NIH, ERC, and AMED-funded stem cell and regenerative medicine research programs that collectively represent significant consumption of research-grade hPL. Cell Banks operating as critical intermediaries in the cell therapy supply chain represent a growing end-user segment as the industry infrastructure for clinical-grade cell storage and distribution expands globally.

Regional Insights

North America Human Platelet Lysate Market Trends and Insights

North America leads the global Human Platelet Lysate market with approximately 38% share in 2026, driven by the world's largest approved CAR-T cell therapy commercial manufacturing base, robust FDA ATMP regulatory frameworks promoting xeno-free manufacturing, and extensive NIH NCATS-funded cell therapy research infrastructure across leading academic medical centers.

U.S. Human Platelet Lysate Market Size

The United States dominates North America with an expected share of 90% of regional revenue in 2026, estimated at around US$ 21.3 million. FDA-approved CAR-T therapies from Novartis, Gilead/Kite, and Bristol-Myers Squibb collectively drive large-volume GMP hPL procurement, and the NIH-funded cell therapy infrastructure sustains significant research-grade hPL demand.

Europe Human Platelet Lysate Market Trends and Insights

Europe is the second-largest and most technically advanced regional market, characterized by the world's most mature ATMP regulatory framework under the EMA and the highest density of GMP-certified hPL manufacturers. The EU ATMP Regulation (EC 1394/2007) provides the regulatory foundation, while progressive European Blood Alliance guidelines on hPL manufacturing standards are driving product quality benchmarking across the region.

Germany Human Platelet Lysate Market Size

Germany is Europe's largest hPL market, estimated at approximately US$ 4.8 million in 2026, representing around 28% of European revenue. Germany's leadership in ATMP manufacturing, including companies such as PL BioScience GmbH and academic-industry cell therapy programs at major university hospitals, underpins strong institutional and commercial hPL demand.

U.K. Human Platelet Lysate Market Size

The United Kingdom holds approximately 18% of the European market share in 2026, valued at around US$ 3.1 million. NHS Blood and Transplant (NHSBT) operates a platelet collection infrastructure that can support hPL production, and MHRA-regulated cell therapy manufacturers driving hPL adoption for CAR-T and MSC programs are key demand drivers.

France Human Platelet Lysate Market Size

France accounts for approximately 14% of the regional market share in 2026, estimated at around US$ 2.4 million. Établissement Français du Sang (EFS) operates a national blood and platelet collection network, and France's active ANSM-regulated ATMP manufacturing sector including Macopharma SA's established hPL production capabilities drives consistent market demand.

Asia Pacific Human Platelet Lysate Market Trends and Insights

Asia Pacific is the fastest-growing regional market for human platelet lysate, driven by rapidly expanding cell therapy clinical trial activity, particularly in China, Japan, South Korea, and Australia and growing government investment in regenerative medicine manufacturing infrastructure. China's National Medical Products Administration (NMPA) has approved several cell therapy products and is progressively aligning manufacturing guidelines with EMA ATMP standards, stimulating domestic demand for xeno-free culture supplements, including hPL.

India Human Platelet Lysate Market Size

India is an emerging hPL market, estimated at approximately US$ 0.9 million in 2025, representing around 8% of Asia Pacific revenue. India's expanding stem cell research and cell therapy sector, supported by the Department of Biotechnology (DBT)'s funding of regenerative medicine research and a growing number of CDSCO-regulated ATMP clinical trials, is creating nascent but growing hPL demand.

Competitive Landscape

The global human platelet lysate market is highly competitive, driven by increasing demand for xeno-free cell culture supplements in stem cell research, regenerative medicine, and cell therapy applications. Market participants compete through product purity, GMP compliance, consistent batch quality, and strong regulatory standards for clinical use. Innovation focuses on heparin-free formulations, pathogen reduction technologies, and improved scalability for therapeutic manufacturing. Strategic collaborations with research institutes, biopharmaceutical companies, and cell therapy developers strengthen market presence.

Key Developments:

- In May 2025, PL BioScience and DewCell Biotherapeutics signed a Letter of Intent to jointly develop scalable, animal-free cell culture media using artificial human platelet lysate. Under the agreement, DewCell supplied artificial platelet raw material produced through stem cell differentiation into megakaryocytes, while PL BioScience applied its manufacturing expertise to create a synthetic, xeno-free culture medium.

- In May 2024, Captivate Bio, a leading scientific supplier to the life sciences industry, announced a significant step in its commitment to providing cutting-edge cell culture and labware solutions to its customers. Captivate Bio entered into a non-exclusive distribution agreement with NEST Scientific USA, a leading plasticware manufacturer.

- In June 2023, PL BioScience GmbH announced a Patent License and Assignment Agreement with the French company Macopharma S.A.S. As a result of the Agreement, PL BioScience will hereby accept a worldwide license under the patents filed by Macopharma, with a right to sublicense (through multiple tiers), for the duration of the license period.

Companies Covered in Human Platelet Lysate Market

- Merck KGaA

- Compass Biomedical Inc.

- Macopharma SA

- Mill Creek Life Sciences Llc.

- Stemcell Technologies Inc.

- Zen-Bio, Inc.

- Sclavo Diagnostics International Srl.

- Life Science Group Limited (Life Science Production)

- Trinova Biochem GmbH

- AventaCell BioMedical Corp

- PL BioScience GmbH

- Regenexx

Frequently Asked Questions

The global Human Platelet Lysate market is estimated at US$ 62.3 million in 2026.

The primary demand drivers in the Human Platelet Lysate market include the rising adoption of stem cell therapies, regenerative medicine, and cell-based research that require safe and xeno-free culture supplements.

North America leads with approximately 38% of global market share in 2026, estimated at around US$ 21.3 million for the U.S. The U.S. dominates through FDA-approved CAR-T commercial manufacturing (Kymriah, Yescarta, Breyanzi), NIH NCATS-funded cell therapy programs, and world-leading biopharma investment in regenerative medicine.

The key market opportunity in the human platelet lysate industry lies in the expanding use of xeno-free and GMP-compliant culture media for large-scale cell therapy and regenerative medicine production.

Leading players include Merck KGaA (MilliporeSigma), PL BioScience GmbH, Macopharma SA, Stemcell Technologies Inc., Mill Creek Life Sciences LLC, Compass Biomedical Inc., AventaCell BioMedical Corp., and Trinova Biochem GmbH.