Industry: Healthcare

Published Date: September-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 173

Report ID: PMRREP34783

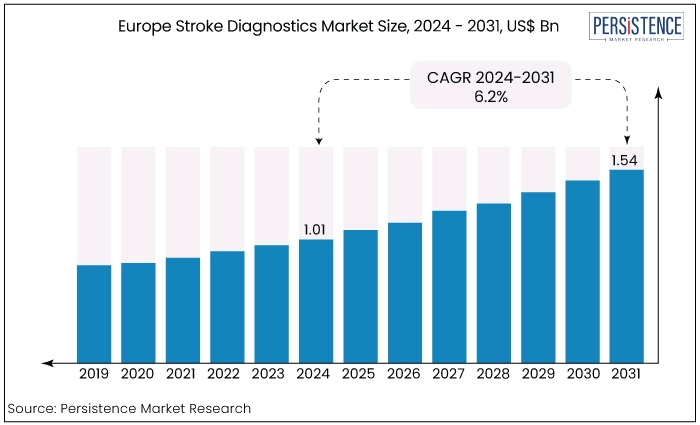

Europe stroke diagnostics market is estimated to increase from US$ 1.01 Bn in 2024 to US$ 1.54 Bn by 2031. The market is projected to record a CAGR of 6.2% during the forecast period from 2024 to 2031. Germany is poised to lead the European stroke diagnostics market, driven by significant advancements in healthcare research and development.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Europe Stroke Diagnostics Market Size (2024E) |

US$ 1.01 Bn |

|

Projected Market Value (2031F) |

US$ 1.54 Bn |

|

Europe Market Growth Rate (CAGR 2024 to 2031) |

6.2% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

5.0% |

|

Region |

Market Share in 2024 |

|

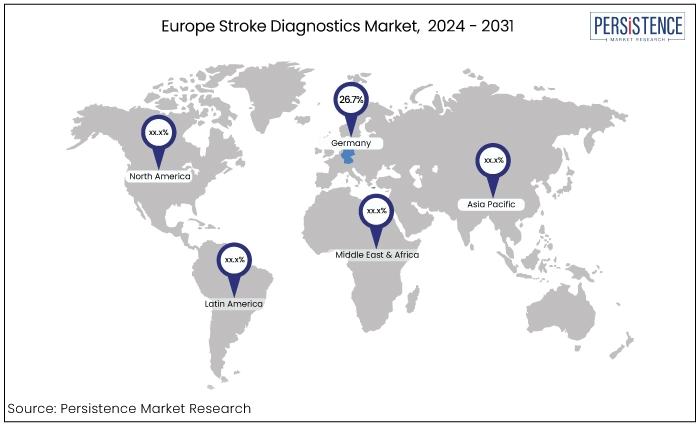

Germany |

26.7% |

Germany has consistently maintained a substantial share in Europe Stroke Diagnostics Market, estimated to account for around 26.7% in 2024. Germany’s well-established healthcare system significantly contributes toward the development and deployment of cutting-edge stroke diagnostic tools and services.

A strong network of academic and medical institutions also fosters an environment of innovation in stroke diagnostics sector. The country’s favorable regulatory environment facilitates adoption of new diagnostic solutions playing a critical role in maintaining this market share.

|

Category |

Market Share in 2024 |

|

By Stroke Type - Ischemic Stroke |

64.3% |

As per the Europe stroke diagnostics market analysis, based on stroke type, ischemic stroke type has maintained its position as the largest contributor capturing a substantial 64.3% share in 2024. This dominance is due to their increasing prevalence of stroke and growing need for developing targeted treatments to address various stroke conditions.

|

Category |

Market Share in 2022 |

|

By Diagnostic Test - CT scan |

44.2% |

The CT scan diagnostic tests have established a substantial lead, commanding an impressive 44.2% market share in terms of value. This segment's continued dominance can be attributed to their ability to provide precise visualization of any abnormality in tissues and organs. It captures detailed cross-sectional images, which is crucial for effective diagnosis and treatment planning.

Improvements in CT technology with respect to its image quality, reduced scan times, and minimized exposure to radiation have contributed significantly to enhance patient safety and comfort. CT scans are widely utilized for diagnosing a wide range of conditions such as cancer, cardiovascular diseases, trauma etc., further bolstering in their widespread adoption.

The stroke diagnostics market in Europe is driven by increasing awareness regarding stroke condition as well as its impact and advancements in imaging technologies. Stroke diagnostics incorporates the use of sophisticated diagnostic imaging tools and techniques such as CT scanners and advanced MRI systems, which enhances the precision of stroke detection and treatment planning.

There has been a significant shift in the adoption of digital and automated diagnostic solutions in Europe, with automated diagnostic systems and AI-driven analytics becoming increasingly prevalent. Thus, offering reliable, and quicker assessments while reducing the overall workload of healthcare professionals.

Growing emphasis on preventive diagnostics and risk assessment are being developed to identify individuals at high risk of stroke before symptoms manifest, facilitating early intervention. These enable early and accurate diagnosis, which is critical for improving patient outcomes and minimizing long-term disability.

Europe stroke diagnostics market is evolving significantly characterized by technological advancements, increased focus on early detection, and growing accessibility, all contributing to improved stroke management and outcomes.

The demand for stroke diagnostics in Europe has witnessed substantial growth fueled by increasing prevalence of stroke-related conditions.

Early detection technologies, including high-resolution imaging and advanced biomarkers, have significantly improved diagnostic accuracy and patient outcomes. Europe market for stroke diagnostics recorded a CAGR of 5.0% indicating steady growth during the historic period.

Rise in adoption of integrated telemedicine platforms, shift toward precision diagnostics and growing focus on personalized medicine is likely to drive further market development and improve overall stroke care in Europe.

The stroke diagnostics market overview has shown consistent growth over the years, and its upward trajectory is expected to continue in the future. The market is projected to capture a CAGR of 6.2% from 2024 to 2031.

Rise of Innovative Health Tech Startups

The stroke diagnostics industry in Europe is witnessing a surge in innovative health tech startups with introduction of cutting-edge solutions such as AI-powered imaging software, advanced biomarkers, and telemedicine platforms.

The rise of these startups is catalysing competition and fostering a dynamic environment, which accelerates technological progress and ultimately benefits patients with more precise and timely stroke diagnosis.

Government Initiatives Driving Stroke Diagnostic Innovation

Government of Europe is committed to cultivate an environment of innovation and development of new technologies through supportive policies and funding programs for research and development in stroke diagnostics.

The £400,000 and CHF 400,000 grant, administered by Innovate UK and Innosuisse, will fund their joint development of an AI-powered remote diagnosis and treatment platform for stroke. Starting in 2024, they will create an AI-assisted magnetic navigation system for robotic surgical tools, combining Brainomix's imaging technology with Nanoflex's navigation expertise for enhanced catheter guidance.

Several health campaigns and public awareness programs are encouraging early detection and timely treatment further driving demand for advanced diagnostic solutions.

Integration Challenges in Stroke Diagnostic Technologies

Integration of advanced technologies for diagnostic purposes with existing healthcare infrastructure often face challenges leading to operational inefficiencies. This increases the complexity and costly upgradation or custom solutions, increasing the overall cost for healthcare providers.

Legacy systems in many hospitals may not be compatible with these new technologies creating further problems with interoperability between different diagnostic platforms and electronic health record (EHR). Thus, leading to inconsistencies in patient data as well as diagnostic results, indirectly impacting the workflow of healthcare professionals, as they may need to adapt to new systems and processes.

Variability in Diagnostic Criteria and Protocols

There are different methods as well as diagnostic standards used for stroke diagnosis undertaken by various healthcare institutions and practitioners. The techniques are influenced by factors such as available technologies, clinical assessments and imaging results. While some protocols emphasize rapid imaging to rule out hemorrhagic strokes, others may prioritize extensive evaluations to assess ischemic causes.

This lack of uniformity affects the treatment modalities and timelines, as delays or misinterpretations due to varying criteria can hinder the initiation of appropriate interventions. Such inconsistencies in criteria often lead to challenges in comparing research findings and developing universally accepted treatment guidelines.

Harmonizing diagnostic criteria and protocols is crucial for improving diagnostic accuracy, ensuring equitable patient care, and enhancing overall stroke management.

Advancements in Non-Invasive Imaging and Diagnostic Tools

Researchers have been collaborating with manufacturers to identify and innovate new diagnostic technologies to identify stroke patients quickly and accurately. Traditional methods involving complex, time-consuming processes often delay treatment. Developing innovative diagnostic tools promises to streamline the diagnostic process, facilitating quicker decision-making.

The study involves key partners like the West Midlands Ambulance Service University NHS Foundation Trust, Midlands Air Ambulance Charity, University Hospitals Birmingham NHS Trust, and Marker Diagnostics.

Investing in and adopting these cutting-edge diagnostic solutions can position industry leaders at the forefront of advancing stroke care and optimizing treatment efficacy.

Expansion into Emerging Markets with High Stroke Incidence

Many developing regions experience high stroke rates due to factors like limited access to healthcare, rising prevalence of risk factors, and inadequate diagnostic infrastructure. By entering these markets, companies hold opportunities to address critical healthcare gaps, offering advanced diagnostic tools and technologies that are currently scarce.

This expansion not only meets an urgent need but also opens new revenue streams and establishes a foothold in rapidly growing healthcare markets. Additionally, it fosters global health equity by improving access to timely and effective stroke care ultimately contributing to better patient outcomes and long-term market success.

Europe stroke diagnostics market in Europe is marked by a diverse array of key players and innovative technologies. Multinational corporations, such as Siemens Healthineers, GE Healthcare, and Philips, are continually investing in R&D to integrate AI-driven diagnostic solutions, thus dominating the market with their advanced imaging systems.

Many small and specialized firms are also emerging with innovative diagnostic tools and software focusing on niche areas like advanced biomarkers and telemedicine platforms. Partnerships and collaborations between technology developers, healthcare providers, and research institutions are common aiming to accelerate the development and adoption of cutting-edge diagnostic technologies.

Competitive strategies like expanding product portfolios, enhancing technology capabilities, and pursuing strategic alliances are being undertaken to address the evolving needs of stroke diagnostics and improve patient outcomes across Europe.

Recent Developments in Europe Stroke Diagnostics Market

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Countries Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Stroke Type

By Diagnostic Test

By End User

By Country

To know more about delivery timeline for this report Contact Sales

The market is estimated to increase from US$ 1.01 Bn in 2024 to US$ 1.54 Bn by 2031.

Increased emphasis on early detection and personalized treatment is a key driver for market growth.

Siemens Healthineers, GE Healthcare, and Koninklijke Philips N.V are some of the leading industry players in Europe.

The market is projected to record a CAGR of 6.2% during the forecast period from 2024 to 2031.

A key opportunity in the stroke diagnostics industry lies in expanding telemedicine solutions for remote diagnosis and monitoring, improving access to stroke care in underserved and rural areas.