- Metals & Minerals

- Europe Green Steel Market

Europe Green Steel Market Size, Share, and Growth Forecast 2026 - 2033

Europe Green Steel Market by Product Type (Flat Steel Products, Long Steel Products, Others), Production Technology (Electric Arc Furnace (EAF), Molten Oxide Electrolysis (MOE), Others), End-user (Automotive, Building & Construction, Electronics, Metal Products, Mechanical Equipment), and Regional Analysis, 2026 - 2033

Europe Green Steel Market Size and Trend Analysis

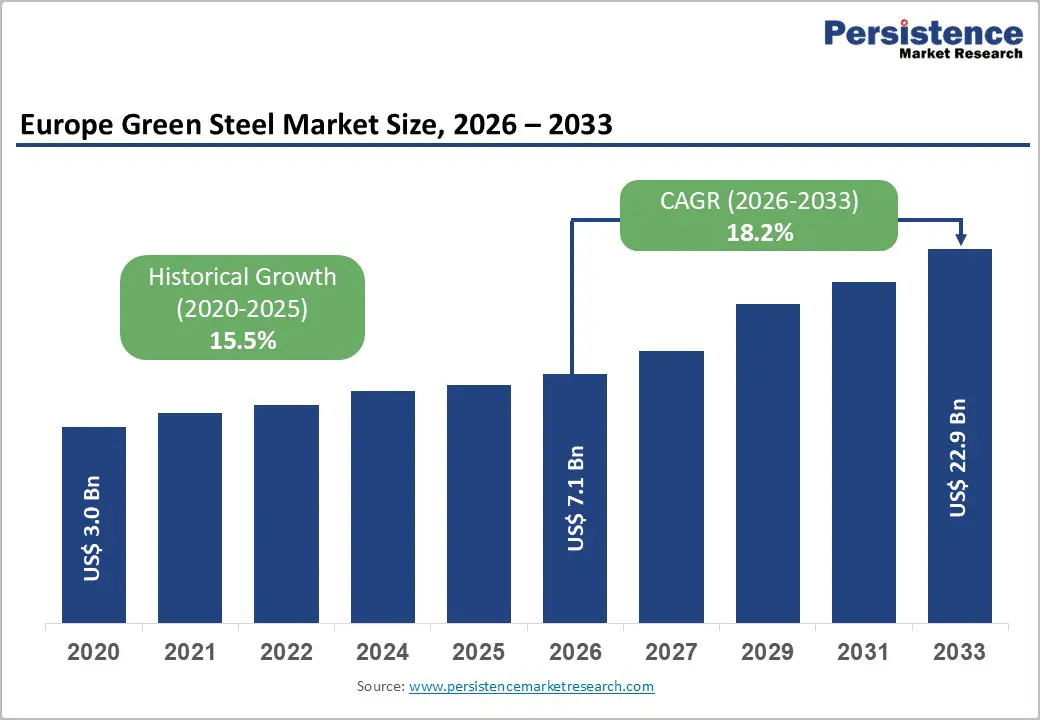

The Europe green steel market size is expected to be valued at US$ 7.1 billion in 2026 and projected to reach US$ 22.9 billion growing at a CAGR of 18.2% between 2026 and 2033. This exceptional growth trajectory is underpinned by the European Union's binding carbon neutrality targets under the European Green Deal and the Carbon Border Adjustment Mechanism (CBAM), which are compelling steelmakers and downstream industries to decarbonize supply chains at an accelerated pace.

The steel sector accounts for approximately 7-9% of global CO2 emissions, according to the World Steel Association (World Steel), making green steel adoption both an environmental imperative and a commercially strategic necessity for manufacturers seeking to retain market access and customer relationships in a rapidly tightening regulatory environment.

Key Industry Highlights

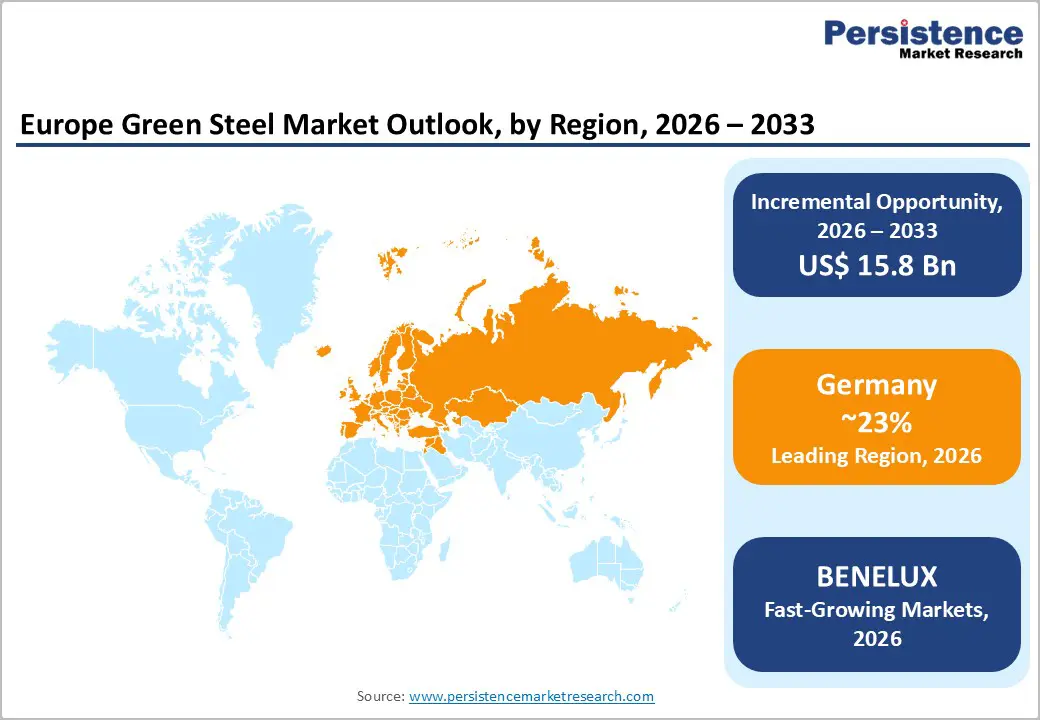

- Leading Region: Germany leads Europe Green Steel market with approximately 23% market share in 2026, supported by flagship hydrogen-DRI projects from ThyssenKrupp AG and Salzgitter AG, substantial state funding via Carbon Contracts for Difference, and strong downstream demand from Germany’s automotive manufacturing sector.

- Fastest Growing Region: BENELUX is the fastest-growing sub-region, propelled by Tata Steel Netherlands’ EUR 4-5 billion IJmuiden decarbonization plan, ArcelorMittal Ghent’s DRI-EAF transition, and strategic green hydrogen import infrastructure development at the Ports of Rotterdam and Antwerp.

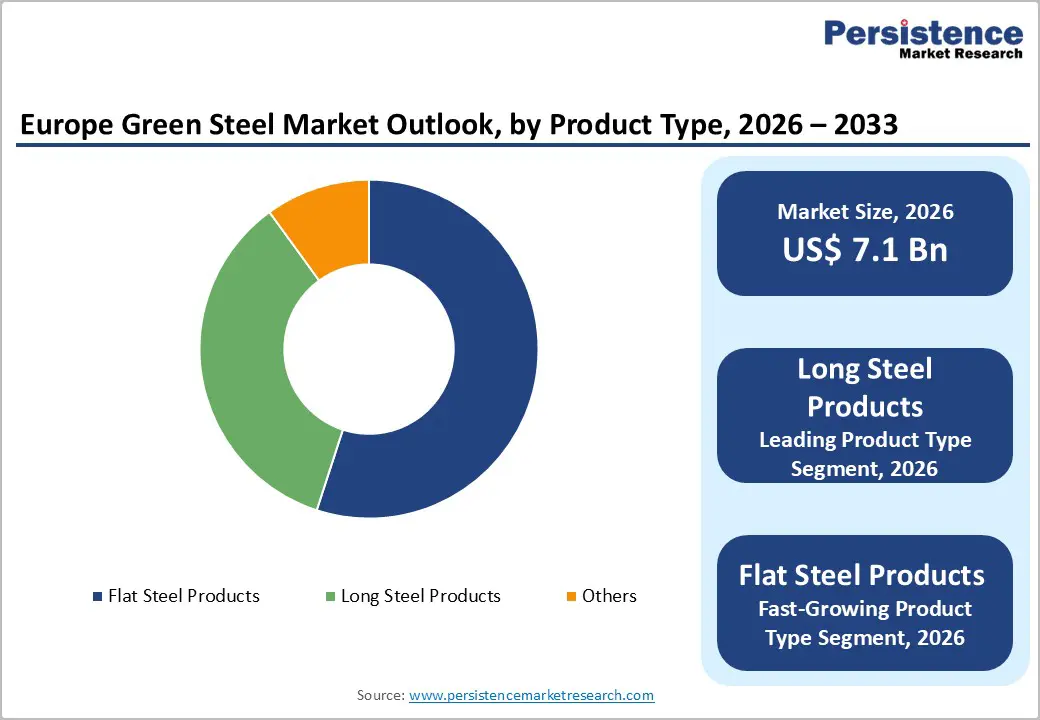

- Dominant Product Segment: Long steel products dominate Europe Green Steel market, underpinned by EAF technology compatibility, Europe’s mature scrap recycling infrastructure, and robust demand from the green building and infrastructure sectors funded through EU recovery programs.

- Fast-Growing Product Segment: Flat steel products are the fast-growing segment, driven by surging automotive and white goods OEM procurement mandates for low-carbon steel and the scaling of hydrogen-DRI production, enabling virgin flat steel with near-zero emissions.

- Key Opportunity: Green steel certification frameworks such as ResponsibleSteel and SteelZero are enabling EUR 50-200/tons price premiums, validated by H2 Green Steel’s USD 1.5 billion+ pre-commercial offtake pipeline from Scania, Porsche, and Marcegaglia.

DRO Analysis

Drivers- EU Carbon Border Adjustment Mechanism (CBAM) Accelerating Decarbonization Demand

The European Union’s Carbon Border Adjustment Mechanism, which entered its transitional phase in October 2023 and will be fully operational by 2026, places a carbon price on imported steel and iron products equivalent to what European producers pay under the EU Emissions Trading System (ETS). As EU ETS carbon prices have ranged between EUR 60 and EUR 100 per tons of CO2 in recent years, with projections suggesting sustained elevation through the decade, the cost disadvantage for carbon-intensive steel is structurally increasing.

According to the European Commission, steel is among the most carbon-exposed sectors under CBAM. This regulatory architecture directly incentivizes European steelmakers and their supply chain partners to accelerate green steel investments, as low-emission production becomes a prerequisite for competitiveness rather than a premium differentiation strategy.

Expanding Automotive and Construction Sector Commitments to Green Procurement

Volkswagen Group, Mercedes-Benz, BMW, and Volvo Cars have each publicly committed to sourcing low-carbon or green steel as part of their Scope 3 emissions reduction strategies under the Science Based Targets initiative (SBTi). The construction sector, which accounts for roughly 50% of total European steel consumption according to the European Steel Association (EUROFER), is similarly responding to tightening green building standards under the EU Taxonomy for Sustainable Activities.

This convergence of demand-side pulls from two of the largest steel-consuming industries is creating a durable structural demand signal that is significantly supporting green steel investment cycles and capacity expansion plans across Europe.

Restraints - Prohibitively High Capital Expenditure for Green Hydrogen-Based Production

Transitioning from conventional blast furnace operations to hydrogen-based direct reduced iron (H-DRI) and electric arc furnace (EAF) processes requires capital expenditure that industry sources estimate at EUR 1-2 billion per million tons of annual green steel capacity. ThyssenKrupp AG’s planned direct reduction plant at Duisburg, for instance, has a project value exceeding EUR 2 billion.

Smaller and mid-scale European steelmakers, lacking the balance sheet depth of majors such as ArcelorMittal or Voestalpine, face material financing constraints that delay or preclude technology transitions. The European Investment Bank (EIB) and national state aid frameworks partially address this gap, but subsidy availability remains uneven across member states, creating competitive distortions within the European market.

Green Hydrogen Supply Scarcity and Infrastructure Immaturity

Green steel production via the hydrogen-DRI route depends critically on the availability of affordable green hydrogen, produced through water electrolysis powered by renewable energy. However, Europe’s green hydrogen production capacity remains nascent. The European Hydrogen Backbone initiative projects that adequate hydrogen transmission infrastructure will not be fully operational until the early 2030s.

Current green hydrogen costs in Europe range from EUR 4 to EUR 8 per kilogram, compared to approximately EUR 1-2/kg for grey hydrogen derived from natural gas, according to the European Clean Hydrogen Alliance. This cost differential significantly impairs the economic viability of green steel at scale today, constraining near-term production ramp-up and limiting the pace at which producers can transition away from fossil fuel-based operations.

Opportunities - Molten Oxide Electrolysis (MOE) as a Transformative Low-Carbon Production Technology

Molten Oxide Electrolysis represents one of the most promising next-generation green steel technologies, capable of producing liquid steel directly from iron ore using only electricity, eliminating the need for carbon-based reductants or hydrogen. Boston Metal, the MIT spinout pioneering MOE at commercial scale, raised USD 262 million in Series C funding in 2023 and is advancing its European operations.

Unlike EAF or H-DRI routes, MOE produces oxygen as a byproduct rather than CO2, offering a pathway to near-zero emission steel production. As European energy grids become increasingly renewables-dominated and electricity costs decline along with solar and wind LCOE curves, MOE’s economics are expected to become commercially competitive by the late 2020s, positioning early movers to capture significant market advantage and premium pricing from sustainability-committed buyers.

Green Steel Certification and Premium Pricing Opportunity

The emergence of standardized green steel certification frameworks, including the ResponsibleSteel International Standard and the SteelZero initiative championed by the Climate Group, is creating a verifiable premium market segment with tangible price differentiation. Buyers in the automotive, white goods, and construction sectors are demonstrating willingness to pay a green premium reported at EUR 50-200 per tons above conventional steel prices.

H2 Green Steel, which is constructing Europe’s first large-scale green steel plant in Boden, Sweden (targeting 5 million tons/year by 2030), has already secured over USD 1.5 billion in offtake agreements from major European manufacturers including Scania, Porsche, and Marcegaglia. This pipeline validates the commercial reality of the premium pricing model and creates a replicable business case for other European green steel producers.

Category-wise Analysis

Product Type Insights

The long steel products segment is the leading product type in Europe Green Steel market, holding approximately 56% share in 2026. Long steel products, encompassing rebar, wire rod, structural sections, rails, and merchant bars, are inherently suited to green steel production via Electric Arc Furnace technology, which predominantly uses scrap steel as feedstock.

Europe’s mature scrap collection infrastructure and high recycling rates exceeding 85% in some Northern European economies, according to the European Ferrous Recovery and Recycling Federation (EFR), make EAF-based long steel production both technically straightforward and commercially viable at scale today. Demand from the green building and infrastructure sectors, including EU-funded green recovery investments under the European Green Deal, provides a sustained volume offtake, reinforcing the segment’s dominant market position.

Production Technology Insights

The Electric Arc Furnace (EAF) segment leads the Production Technology category, commanding approximately 68% of Europe Green Steel market share in 2026. EAF technology’s dominance is rooted in its established commercial maturity, lower capital intensity relative to greenfield hydrogen-DRI plants, and its ability to achieve significantly reduced carbon emissions, approximately 0.4-0.6 tons of CO2 per ton of steel compared to 1.8-2.0 tons for integrated blast furnace operations, when powered by renewable electricity.

The European Commission’s Steel Action Plan and state-level industrial decarbonization programs in Germany, France, and Sweden have directed substantial public funding toward EAF capacity expansion. Accelerating renewable electricity capacity additions are progressively lowering EAF operational emissions, reinforcing the segment’s leading position through the forecast period.

End-user Insights

The building & construction segment leads the end-use category in Europe green steel market, accounting for approximately 38% share in 2026. The European construction sector is the largest single consumer of steel on the continent, and intensifying regulatory pressure under the EU Taxonomy for Sustainable Activities and the Energy Performance of Buildings Directive (EPBD) is fundamentally reshaping procurement standards.

Green building certifications, including BREEAM, LEED, and the EU Green Building certification framework, increasingly award credits for the use of low-embodied-carbon materials. Public infrastructure programs funded through the EU Recovery and Resilience Facility (RRF), which allocated EUR 723 billion for post-COVID green and digital recovery, prioritizing sustainable construction materials, making it the most volume-significant and policy-supported end-use segment.

Country Insights

Germany Green Steel Market Trends and Insights

Germany is the dominant country in Europe Green Steel market, holding approximately 23% of the regional share in 2026, supported by its position as Europe’s largest steel producer and its industrial decarbonization policy architecture. The German government’s National Hydrogen Strategy, backed by EUR 9 billion in public investment, and the Klimaschutzvertrage (Carbon Contracts for Difference) program, which compensates steel producers for the cost difference between conventional and green production, are providing critical investment security for hydrogen-DRI transitions.

ThyssenKrupp AG’s tkH2Steel project at Duisburg and Salzgitter AG’s SALCOS (Salzgitter Low CO2 Steelmaking) program are flagship national initiatives receiving state and EU funding. Germany’s automotive manufacturing density and deep OEM-supplier integration further create a localized premium demand base for certified green steel.

Italy Green Steel Market Trends and Insights

Italy represents one of Europe’s more dynamic green steel markets, driven by its high proportion of EAF-based steel production, accounting for approximately 70% of national crude steel output according to Federacciai (the Italian Steel Federation), which provides a structurally advantaged starting position for green steel transition.

Italy’s steel sector is anchored by significant long steel producers in the Brescia district, collectively known as the “Bresciani” mini mills, which have historically operated EAF technology and are increasingly investing in renewable power procurement agreements (PPAs) to further reduce Scope 2 emissions. National decarbonization incentives under the PNRR (Piano Nazionale di Ripresa e Resilienza) and alignment with EU industrial decarbonization directives are supporting investment in low-carbon upgrades. Italy’s construction sector creates robust domestic demand for green rebar and structural steel products.

France Green Steel Market Trends and Insights

France’s green steel market is shaped by its unique industrial structure, dominated by ArcelorMittal’s integrated steelmaking operations at Fos-sur-Mer and Dunkirk, alongside a national climate strategy aligned with the EU’s 2050 carbon neutrality target. France Industrie Verte, the national industrial decarbonization roadmap, identifies steel as a priority sector for low-carbon transition.

ArcelorMittal’s XCarb initiative and its EUR 1.7 billion Smart Carbon and Direct Reduced Iron investment plan for French operations represent the most significant decarbonization commitment in the country. The French government’s reindustrialisation agenda and the Green Industry Law (2023) provide tax incentives and simplified permitting for low-carbon industrial investments. Downstream demand from Stellantis and Renault Group provides premium offtake demand for certified low-carbon steel.

U.K. Green Steel Market Trends and Insights

The United Kingdom’s green steel market is navigating a critical structural transition, with the planned closure of the last two remaining blast furnaces at the Port Talbot steelworks by Tata Steel UK, supported by a GBP 500 million government co-investment package, marking the most significant decarbonization inflection point in UK steel history. The transition to an EAF-based facility at Port Talbot, targeting 2026 commissioning, positions the UK to substantially reduce its steelmaking CO2 intensity.

The UK’s Independent Climate Change Committee (CCC) has identified green steel as a strategic priority in achieving the country’s Sixth Carbon Budget commitments. Post-Brexit, the UK Emissions Trading Scheme (UK ETS) is increasingly aligned with EU ETS pricing dynamics, sustaining carbon cost pressures. Demand from the UK offshore wind, construction, and automotive sectors, including Jaguar Land Rover’s sustainability commitments, provides growing green steel offtake.

BENELUX Green Steel Market Trends and Insights

BENELUX is identified as the fastest-growing sub-regional market for green steel in Europe, driven predominantly by the Netherlands and Belgium’s strategic positioning within major European steel and industrial value chains. Tata Steel Netherlands’ IJmuiden facility has announced a EUR 4-5 billion decarbonization investment plan to transition from blast furnaces to direct reduction using initially natural gas and subsequently green hydrogen, targeting 2030 completion.

Belgium’s ArcelorMittal Ghent operations are similarly undergoing a DRI-EAF transition. The Port of Rotterdam and Antwerp’s hydrogen import infrastructure ambitions, targeting green hydrogen imports from North Africa and the Middle East, are strategically significant for enabling cost-competitive green hydrogen supply. BENELUX’s dense industrial cluster, logistics infrastructure, and proximity to offshore wind resources in the North Sea make it the region with the most compelling green hydrogen-DRI economics in Europe.

Competitive Landscape

Europe green steel market exhibits a moderately consolidated competitive structure, with a small number of large integrated steelmakers, ArcelorMittal, ThyssenKrupp AG, Voestalpine, Salzgitter AG, and Tata Steel, commanding substantial production capacity and long-term OEM supply relationships. Key competitive differentiators include green hydrogen procurement security, access to renewable electricity via long-term PPAs, proprietary low-carbon technology IP, and the ability to secure binding offtake agreements from premium buyers.

Emerging challengers such as H2 Green Steel and Boston Metal are disrupting the competitive order with purpose-built green steel facilities and novel production technologies. Strategic partnerships with energy companies (e.g., Vattenfall, Ørsted) for renewable power supply are increasingly central to competitive positioning.

Key Developments:

- In March 2025, H2 Green Steel secured an additional EUR 300 million in debt financing for its Boden, Sweden facility, bringing total project financing to over EUR 3.5 billion, with commercial production on track for 2025 startup targeting leading European automotive buyers.

- In November 2024, ThyssenKrupp AG commenced construction of its first direct reduction plant at Duisburg, Germany, with a EUR 2+ billion investment backed by combined state and federal subsidies, targeting annual production of 2.5 million tons of green steel by 2027.

- In June 2024, ArcelorMittal and Ørsted announced a strategic partnership to supply offshore wind-generated electricity to ArcelorMittal’s Hamburg EAF operations, targeting carbon-neutral steel production at the facility by 2030 under the XCarb certified green steel program.

Europe Green Steel Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 3.0 Billion |

| Current Market Value (2026) | US$ 7.1 Billion |

| Projected Market Value (2033) | US$ 22.9 Billion |

| CAGR (2026 - 2033) | 18.2% |

| Leading Region | Germany, 23% market share (2026) |

| Dominant Category-1 (Product Type) | Long Steel Products, 56% market share (2026) |

| Top-ranking Category-2 (Technology) | Electric Arc Furnace (EAF), 68% market share (2026) |

| Incremental Opportunity | US$ 15.8 Billion |

Companies Covered in Europe Green Steel Market

- ArcelorMittal

- Voestalpine

- SSAB

- Salzgitter AG

- Ansteel Group

- Boston Metal

- China Baowu Group

- Cleveland-Cliffs

- H2 Green Steel

- Nippon Steel Corporation

- Nucor Corporation

- Steel Dynamics, Inc.

- ThyssenKrupp AG

- POSCO

- Salzgitter AG

Frequently Asked Questions

The Europe Green Steel market is expected to be valued at US$ 7.1 billion in 2026, and is further projected to reach US$ 22.9 billion by 2033, reflecting a forecast CAGR of 18.2% over the 2026 - 2033 period.

The primary demand driver is the European Union’s Carbon Border Adjustment Mechanism (CBAM) and binding EU ETS carbon pricing, which are structurally elevating the cost of carbon-intensive steel production.

Germany leads the Europe Green Steel market with approximately 23% market share in 2026. The country’s dominance is supported by Europe’s largest integrated steelmaking base, the National Hydrogen Strategy backed by EUR 9 billion in public investment, Carbon Contracts for Difference, and flagship programs by ThyssenKrupp AG (tkH2Steel) and Salzgitter AG (SALCOS).

The most compelling opportunity lies in the emerging green steel certification and premium pricing ecosystem, where standardized frameworks including ResponsibleSteel and SteelZero are enabling verifiable price premiums of EUR 50-200 per tons.

The leading companies in the Europe Green Steel market include ArcelorMittal, ThyssenKrupp AG, Voestalpine, Salzgitter AG, SSAB, H2 Green Steel, Tata Steel, Nucor Corporation, Steel Dynamics Inc., POSCO, Nippon Steel Corporation, Boston Metal, Cleveland-Cliffs, China Baowu Group, Ansteel Group, Riva Group, Tenaris, and Gerdau S.A.