- Sporting Goods & Equipment

- Europe Football Cleats Market

Europe Football Cleats Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Europe Football Cleats Market Analysis by Product Type (Firm Ground, Soft Ground, Artificial Ground, Hard Ground / Multi-Ground, Turf, Indoor Court), Stud Type (Metal, Rubber, Molded / Plastic, Flat Sole), Distribution Channel (Offline Retail, E-commerce Platforms, Direct-to-Consumer), for 2026 - 2033

Europe Football Cleats Market Share and Trends Analysis

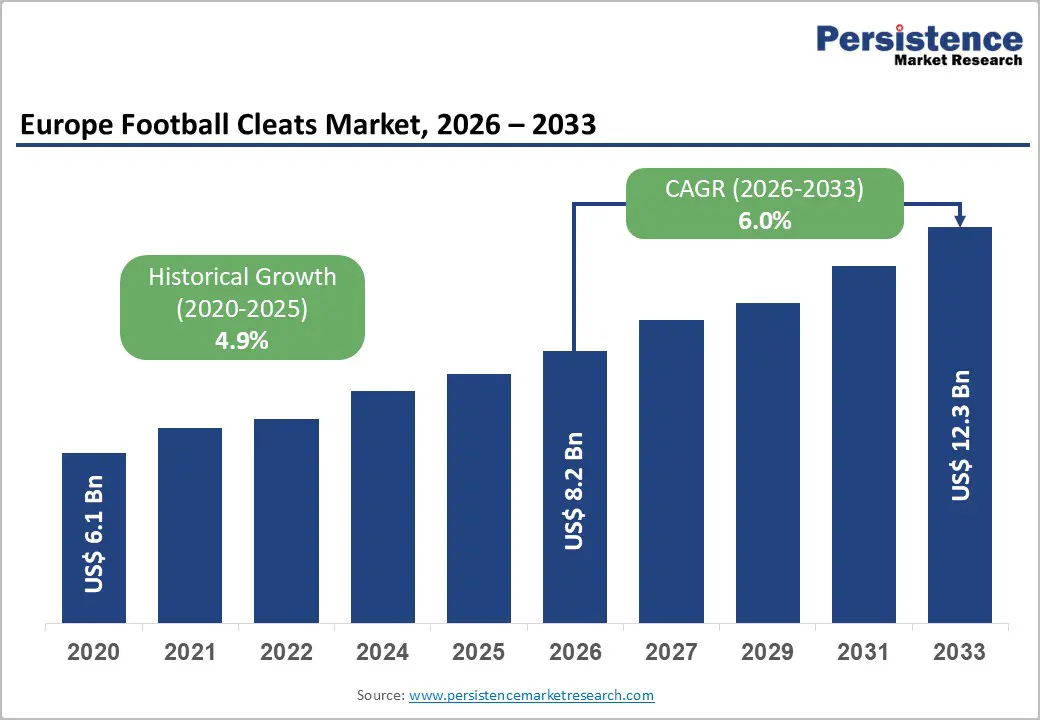

The Europe football cleats market size is projected at US$8.2 Bn in 2026 and is projected to reach US$12.3 Bn by 2033, growing at a CAGR of 6.0% between 2026 and 2033. Demand is supported by Europe’s strong professional and grassroots football ecosystem, with more than 209 million fans attending club matches in 2022-23.

Rising participation in organized leagues and academies increases replacement cycles and premiumization of cleats. Digital sales channels expand access, while innovation in lightweight materials and traction systems enhances performance across varied playing surfaces.

Key Industry Highlights:

- Europe Football Cleats Market is projected to grow from US$8.2 Bn in 2026 to US$12.3 Bn by 2033, reflecting 6.0% CAGR over the forecast period.

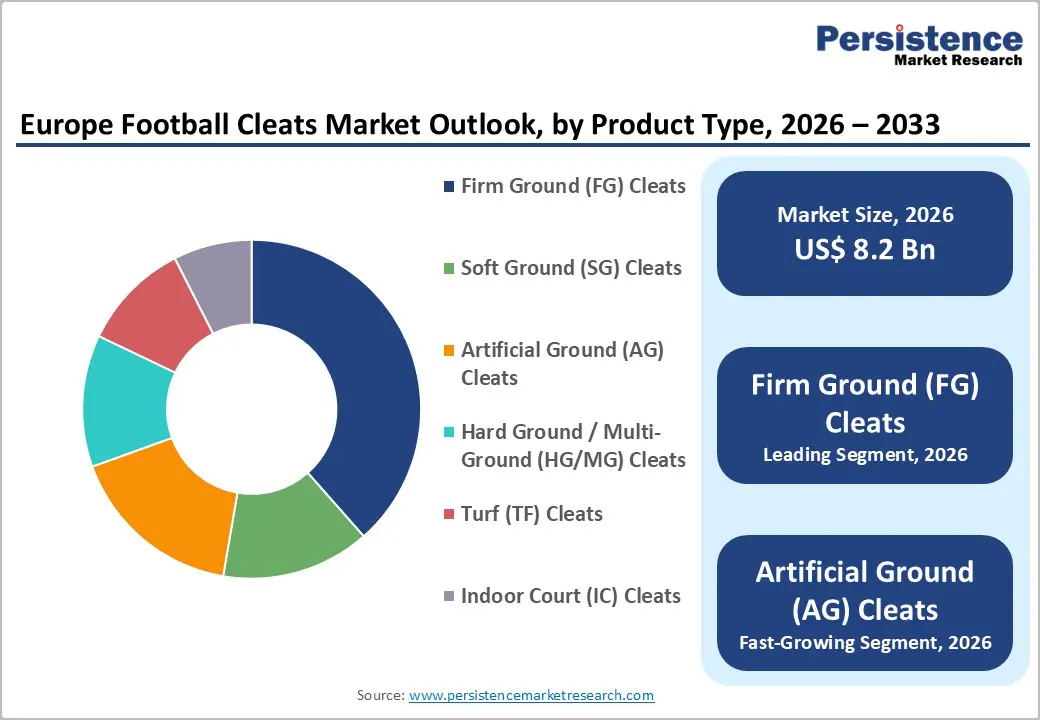

- Firm Ground cleats lead with ~38.5% share, while Artificial Ground cleats expand at approximately 7.1% CAGR supported by rising synthetic pitch installations.

- Molded / plastic studs dominate with ~34.8% share and are also the fastest-growing stud type at around 6.7% CAGR, aligned with multi-surface usage trends.

- Offline retail retains about 52.6% share, whereas e-commerce platforms grow fastest at an estimated 7.6% CAGR, reflecting rapid digitalization of sports footwear purchases.

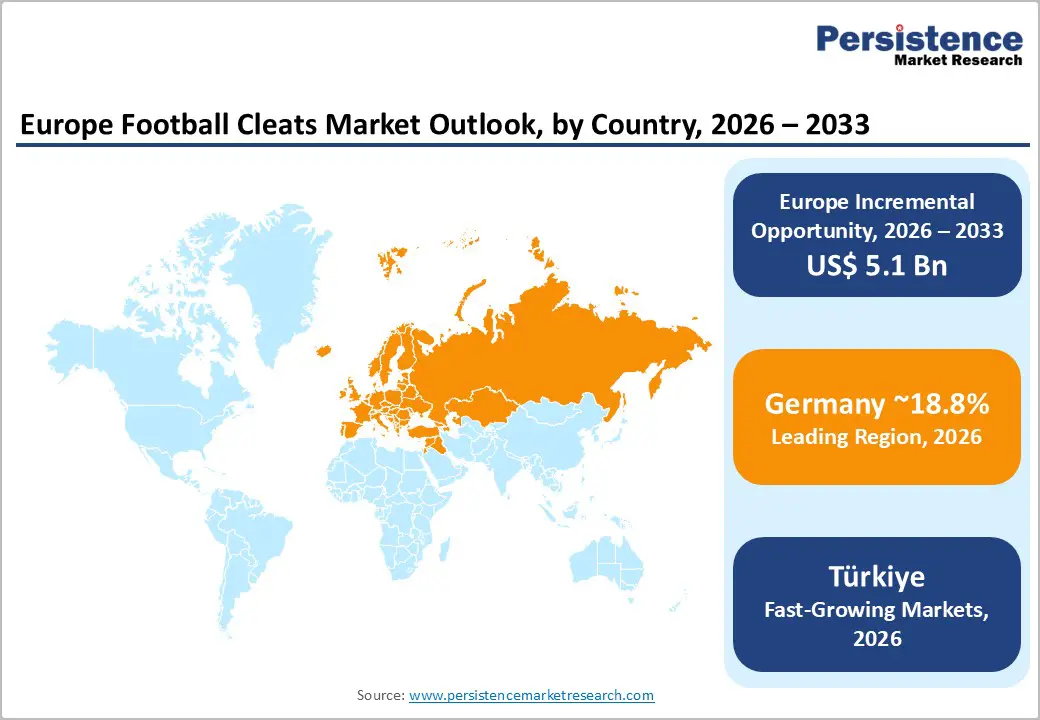

- Germany accounts for ~18.8% of regional revenue, the U.K. for 17.2% with ~5.9% CAGR, while Turkiye posts about 6.7% CAGR as an emerging growth market.

- Post-2023 developments include new performance boot launches, flagship store expansions, e-commerce partnerships, and sustainability collaborations shaping Europe’s football cleats innovation landscape.

| Key Insights | Details |

|---|---|

| Europe Football Cleats Market Size (2026E) | US$ 8.2 Bn |

| Market Value Forecast (2033F) | US$ 12.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.0% |

| Historical Market Growth (2020 - 2025) | 4.9% |

DRO Analysis

Drivers - Deep-rooted football culture and expanding participation base

Europe is the global epicenter of football, with UEFA reporting 209 million fans attending club fixtures in 2022-23 and record crowds across major leagues. Grassroots participation is supported by thousands of amateur clubs and academies, creating recurring demand for cleats at youth and adult levels. National federations and EU-backed sport-for-all programs further promote participation. As players progress through age categories, boot sizes and performance needs change, driving frequent replacements. This robust participation base underpins steady volume growth for firm ground and multi-ground cleats, particularly in football-dominant countries such as Germany, the U.K., Spain, Italy, and France.

Technological advances in materials, traction, and performance design

Leading brands invest heavily in R&D, integrating lightweight synthetic uppers, knitted constructions, and advanced plate geometries to enhance grip, acceleration, and agility. Modern cleats use engineered polymers, responsive foams, and anatomically tuned stud configurations, offering better energy return and injury risk reduction versus legacy leather models. Europe’s professional leagues act as innovation showcases, as elite players debut new models each season, influencing consumer demand. As an example, Europe’s football shoes market is projected to grow at about 5.1% CAGR to 2030, driven largely by product innovation and performance features. This technology race supports premium price points and faster upgrade cycles among aspirational players.

Restraints - Price sensitivity and competition from lower-cost alternatives

While premium cleats from global brands command strong demand, a significant portion of European consumers remains price sensitive, especially in Eastern and Southern Europe. Lower-priced private-label or unbranded boots compete directly with entry-level models, compressing margins. Economic uncertainty can prompt households to delay replacements or trade down, particularly among casual players. Strong competition among leading brands and emerging labels further intensifies discounting, pressuring average selling prices. These dynamics may dampen revenue growth, especially in regions where discretionary spending is under pressure.

Seasonality and exposure to weather and facility availability

Cleat sales are inherently seasonal, peaking around league start dates and declining in off-season periods, which complicates inventory management for retailers. Poor weather conditions, pitch closures, or disruptions to amateur leagues can reduce playing frequency and shorten replacement cycles. During the pandemic period, closures sharply restrained demand, demonstrating the segment’s sensitivity to facility availability and organized competition. While conditions have normalized, future disruptions or structural shifts toward indoor or multi-sport activities could moderate long-term growth, particularly for surface-specific models such as soft ground cleats.

Opportunities - Expansion of artificial and hybrid turf facilities is driving AG and MG demand

European clubs and municipalities continue investing in artificial and hybrid turf pitches to increase pitch utilization and reduce maintenance costs, particularly in Northern climates. As these surfaces proliferate, demand for artificial ground (AG) and multi-ground (MG) cleats rises, given their tailored stud patterns and outsole designs. Hard ground / multi-ground segments already represent the most lucrative product category in some projections, with strong growth expectations. If AG and MG cleats reach a combined 25-30% share of Europe’s football cleats revenue by 2033, they could contribute US$3-3.5 Bn annually, creating significant opportunities for brands offering surface-optimized designs.

Women’s football and youth development programs

UEFA and national federations are heavily promoting women’s football and youth academies, with rising participation rates and professionalization across Europe. Increased visibility of women’s leagues and tournaments boosts equipment demand among women and girls, a historically underserved segment. Purpose-designed women’s cleats that account for anatomical differences and fit preferences represent a growing product niche. Similarly, structured youth pathways require age-appropriate boots with safe traction and durability. Together, women’s and youth segments could account for an incremental US$1.0-1.5 Bn by 2033 in Europe, especially as participation at grassroots level continues to expand.

Category-wise Analysis

Product Type Insights

Firm Ground (FG) cleats are the leading product type in Europe, representing approximately 38.5% of the region’s football cleats revenue in 2026, aligned with data that firm ground models account for around 52% share across broader European football shoes markets. FG cleats are optimized for natural grass pitches in moderate conditions, which dominate competitive and recreational play across major leagues. Their versatility, wide style range, and extensive endorsement by professional players reinforce their dominance, especially in Germany, the U.K., Spain, Italy, and France.

Artificial Ground (AG) cleats are the fastest-growing product type, expanding at an estimated 7.1% CAGR between 2026 and 2033 as artificial and hybrid turf facilities proliferate across Europe. Clubs and municipalities invest in synthetic pitches to increase playable hours and reduce maintenance. Players increasingly seek AG-specific cleats to enhance grip and reduce injury risk on these surfaces, driving robust volume and value growth within this segment across both youth and adult categories.

Stud Type Insights

Molded / plastic studs constitute the leading stud type, capturing around 34.8% of Europe’s football cleats market in 2026, reflecting their wide usage across firm ground, multi-ground, and artificial turf surfaces. They offer a balance of traction, comfort, and durability, suitable for both professional and amateur players. Retailers and clubs favor molded stud configurations due to lower maintenance, broader surface compatibility, and reduced injury risk compared with replaceable metal studs, reinforcing their popularity across price points.

Molded / plastic studs are also the fastest-growing stud category, with an approximate 6.7% CAGR over 2026-2033. Growth is driven by the shift from traditional soft ground metal studs toward multi-surface and artificial ground configurations, particularly in regions investing heavily in synthetic pitches. Innovations in polymer compounds and stud geometry further improve performance, encouraging upgrades and premiumization among frequent players.

Distribution Channel Insights

Offline retail comprising sports specialty stores, multi-brand outlets, and branded stores is the leading distribution channel, accounting for about 52.6% of Europe’s football cleats sales in 2026, consistent with broader footwear data showing offline dominance around 60-63% in recent years. Players value the ability to try on boots, assess fit, and receive expert advice before purchase. High-traffic urban malls, club stores, and specialist football retailers anchor strong offline presence, particularly for premium models and new releases.

E-commerce platforms are the fastest-growing channel, with an estimated 7.6% CAGR between 2026 and 2033, outpacing offline growth by a significant margin. Online marketplaces and brand sites benefit from convenience, extensive assortments, user reviews, and targeted digital marketing. Younger consumers increasingly purchase cleats online, leveraging flexible returns and size guarantees, driving continuous share gains for this channel across Europe.

Country Insights

Germany Football Cleats Market Trends

Germany commands a dominant ~18.8% share of the Europe Football Cleats Market in 2026, reflecting its strong Bundesliga ecosystem, well-developed amateur leagues, and high sports participation. The country hosts major footwear manufacturing and design centers, particularly for brands like Adidas and Puma, reinforcing innovation and product availability. Robust club structures and academies foster continuous demand across age groups. Germany’s market is also a testbed for sustainability-led innovations in footwear, with consumers receptive to eco-friendly materials.

Germany’s football cleats market is projected to grow at around 5.5-6.0% CAGR through 2033, slightly above broader athletic footwear growth. Investment in artificial turf facilities, women’s football, and youth academies supports expansion of AG and MG cleats. The regulatory environment is generally supportive, with consumer protection and sustainability frameworks guiding material choices and marketing practices, but not significantly constraining innovation in cleat design.

U.K. Football Cleats Market Trends

The U.K. holds roughly 17.2% of Europe’s football cleats revenue in 2026 and is growing at about 5.9% CAGR over 2026-2033. The English Premier League’s global profile and packed stadiums drive strong cleat sales, supported by a vibrant grassroots and school football environment. Club and player endorsements significantly influence consumer preferences, often triggering demand spikes around high-profile transfers or new boot launches. Retailers range from nationwide sports chains to club-branded stores and specialist outlets.

U.K. growth is reinforced by high online retail penetration and early adoption of direct-to-consumer offerings. E-commerce channels capture an increasing share of cleat sales, particularly among younger fans and players following digital campaigns. Regulatory conditions related to product safety and marketing are mature, while alignment with broader European standards continues post-Brexit, ensuring consistent quality benchmarks and facilitating brand operations.

Türkiye Football Cleats Market Trends

Türkiye is one of the fastest-growing football cleats markets in Europe, with an estimated 6.7% CAGR from 2026 to 2033 off a smaller base. Strong football culture, national league popularity, and government-backed sports initiatives drive participation, especially among youth. Rising disposable incomes and expanding retail infrastructure support growth in both mid-priced and premium cleat categories. Türkiye is also emerging as a manufacturing base for footwear, including sports shoes, benefiting from competitive labor costs and proximity to EU markets.

Investments in stadiums, training facilities, and artificial turf pitches increase demand for AG and MG cleats. Local brands and regional distributors partner with global companies to expand selection and improve availability. Regulatory harmonization with European product standards enhances export potential and ensures quality compliance. Türkiye’s combination of domestic demand and manufacturing advantages positions it as a strategic node within the broader Europe Football Cleats Market.

Competitive Landscape

Market leaders pursue innovation-led and endorsement-driven strategies, leveraging advanced materials, data-informed traction designs, and high-profile athlete sponsorships to differentiate performance cleats. They balance premium positioning with mid-tier models to capture broader demographics, while investing heavily in e-commerce, direct-to-consumer channels, and customization services. Emerging business models include circular initiatives, subscription-based boot programs for youth, and data-driven marketing that links on-field performance analytics with footwear design and promotion.

Key Developments:

- In June 2024, Adidas AG reintroduced its iconic F50 football boot line under the “Advancement Pack,” featuring three new silhouettes engineered for game-changing speed, incorporating advanced technologies such as the Sprintframe 360 soleplate to enhance multidirectional acceleration and traction across firm and multi-ground surfaces, aligning with evolving pitch conditions across European leagues and training facilities.

- In December 2025, Puma SE strengthened its European direct-to-consumer strategy by opening its largest-ever flagship store on Oxford Street, London, offering an immersive retail experience featuring key football boot lines such as FUTURE, ULTRA, and KING, while enhancing brand visibility and consumer engagement in one of Europe’s most influential shopping destinations.

Companies Covered in Europe Football Cleats Market

- Nike

- Adidas

- Puma

- Under Armour

- Mizuno

- ASICS

- New Balance

- Umbro

- Fila

- Li-Ning

- Joma

- Lotto

- Kipsta

- Diadora

Frequently Asked Questions

The Europe Football Cleats Market is estimated at about US$8.17 Bn in 2026, projected to reach roughly US$12.28 Bn by 2033.

Market growth is driven by deep-rooted football culture, expanding participation, performance-oriented product innovation, and rapid growth of online retail channels.

The Europe Football Cleats Market is expected to grow at approximately 6.0% CAGR between 2026 and 2033.

Key opportunities include AG/MG cleats for synthetic pitches, women’s and youth-focused products, and sustainable, circular-economy footwear solutions.

Major players include Nike, Adidas, Puma, Under Armour, Mizuno, ASICS, New Balance, Umbro, Fila, Li-Ning, Joma, Lotto, Kipsta, and Diadora.