- Beauty & Personal Care

- Cosmetic Face Mask Market

Cosmetic Face Mask Market Size, Share, and Growth Forecast 2026 - 2033

Cosmetic face mask market by Product Type (Clay Face Mask, Peel-off Face Mask, Thermal Face Mask, Cream Face Mask, Warm-Oil Face Mask, Sheet Face Mask, Gel Face Mask, Others), Nature (Organic Face Mask, Synthetic Face Mask), Packaging Format (Tubes, Jars and Bottles, Sachets, Others), Sales Channel (Hypermarkets/Supermarkets, Specialty Stores, Departmental Stores, Multi-brand Stores, Others), and Regional Analysis, 2026 - 2033

Cosmetic Face Mask Market Size and Trend Analysis

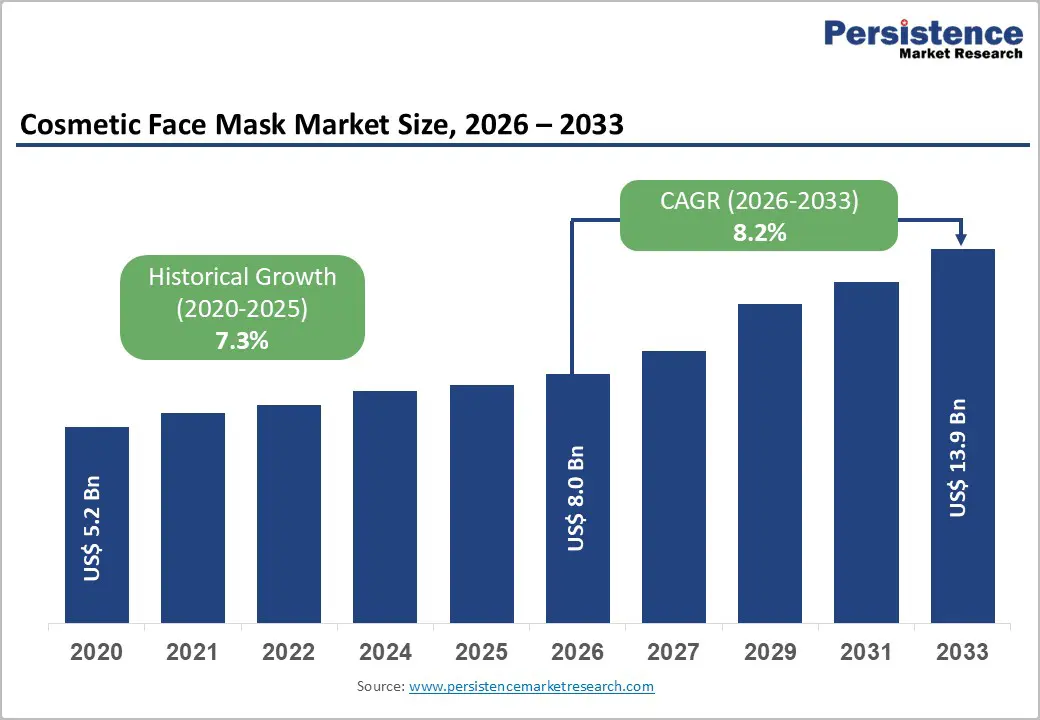

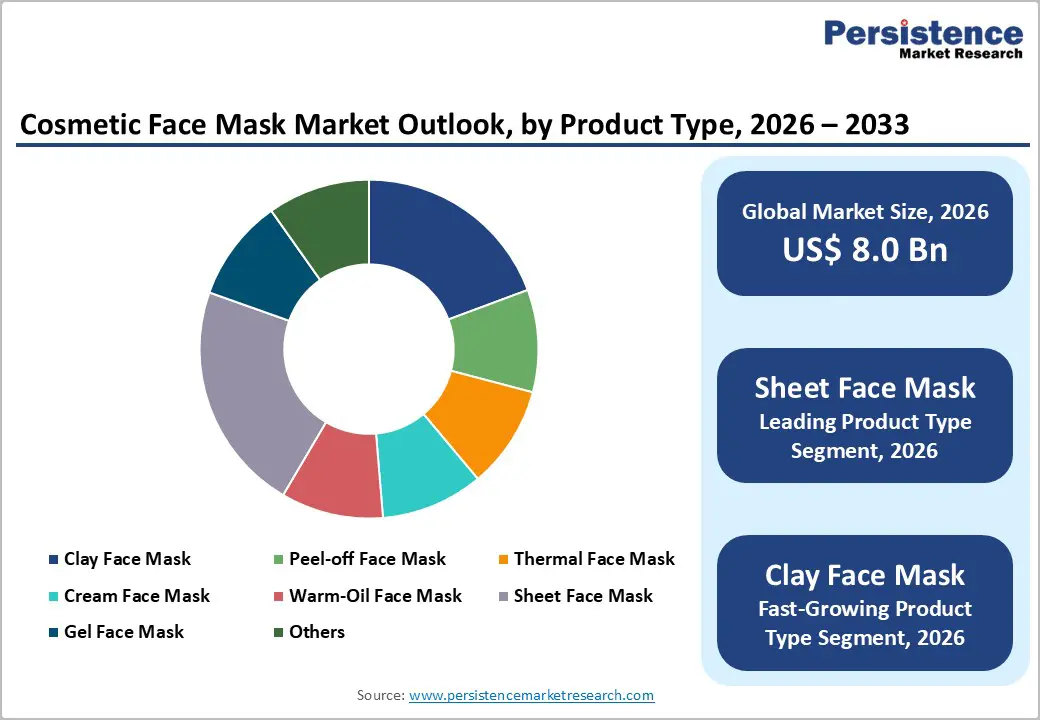

The global cosmetic face mask market size is likely to be valued at US$ 8 billion in 2026, and projected to reach US$ 13.89 billion, registering a CAGR of 8.2% by 2033 and expanding at a robust pace, propelled by premiumization trends, heightened self-care awareness, and accelerating digital retail penetration across mature and emerging economies.

Rising disposable incomes in high-growth markets, the global proliferation of K-beauty-influenced skincare routines, and escalating consumer demand for targeted efficacy collectively underpin this trajectory. Multi-functional face mask formats delivering hydration, detoxification, and anti-ageing benefits continue to outpace the broader skincare category, reinforcing the market's structural momentum.

Key Industry Highlights:

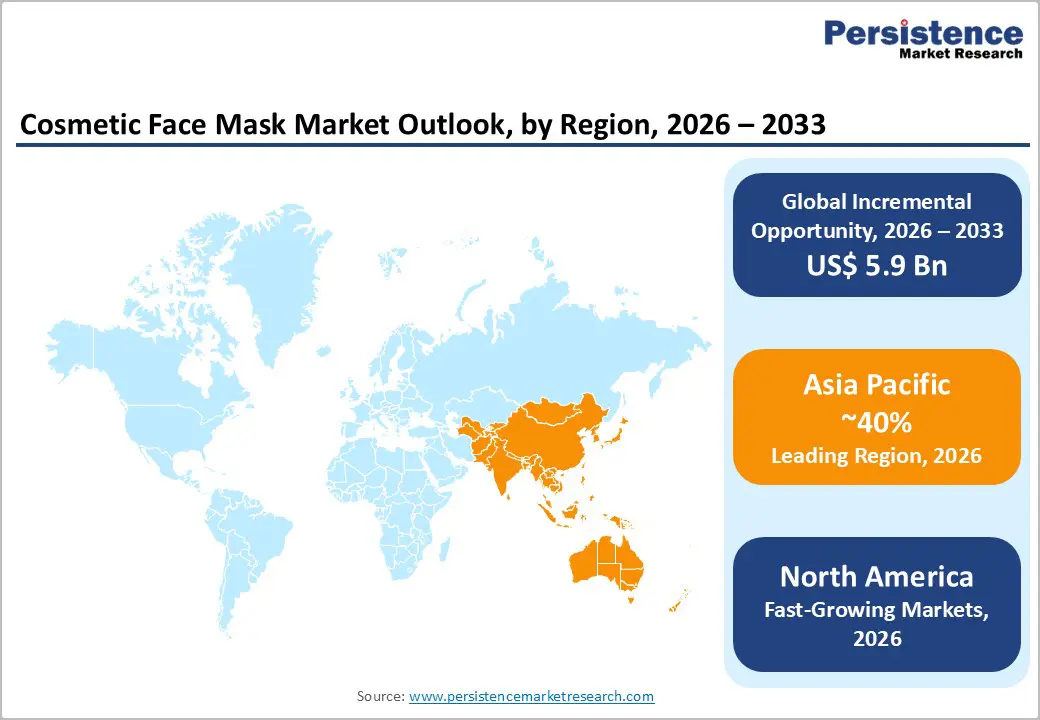

- Leading Region: Asia Pacific leads the cosmetic face mask market with a 41% revenue share, anchored by deeply embedded multi-step skincare routines, the global influence of K-beauty culture, and large-scale consumer demand across China, Japan, India, and Southeast Asia.

- Fastest Growing Region: The Middle East & Africa are fast-growing markets at a projected CAGR of 9.5%, driven by a presence of beauty-conscious population, urbanisation, and rapid modern retail expansion across underserved markets.

- Leading Category: Sheet face mask dominates by product type with a 31% segment share, earned through unmatched format convenience, single-use hygiene appeal, and near-universal compatibility with the active ingredient libraries used for targeted skincare delivery.

- Fastest Growing Category: Clay face mask is the fast-growing product type in the Cosmetic face mask market, accelerating on the back of surging consumer interest in pore-cleansing, oil-control, and detoxifying routines, particularly among Gen Z first-time skincare adopters.

- Key Market Opportunity: The most actionable opportunity in the Cosmetic face mask market lies in organic and clean-label premiumisation, where 15-30% price premiums in North America and Western Europe, combined with category penetration below 10% in several high-income markets, create a first-mover advantage window.

Market Dynamics

Drivers - Rising Consumer Investment in Preventive and Ritual-Based Skincare

Consumers across the Cosmetic face mask market are increasingly treating facial masking not as an occasional indulgence but as a non-negotiable element of a structured skincare regimen. Weekly or bi-weekly mask usage among adult consumers aged 18-44 has grown by more than 20% over the past three years, reflecting a fundamental shift in skincare philosophy that prioritises long-term skin health over reactive, problem-driven product use.

This behavioural pattern is particularly pronounced in Asia Pacific and North America, where social media platforms amplify product discovery and usage rituals. The result is a sustained volume uplift that drives repeat-purchase cycles, elevates average household spend on facial care, and accelerates category penetration among previously low-engagement demographics, including younger Gen Z consumers and an expanding cohort of male skincare buyers.

Expansion of E-Commerce and Direct-to-Consumer Channels

What drives growth in the Cosmetic face mask market beyond product innovation is the structural transformation of how consumers discover, evaluate, and purchase face care products. Online retail channels now account for a rapidly rising share of total market revenue, with digital-native brands leveraging influencer partnerships, subscription models, and algorithm-driven personalisation to compress the purchase funnel and convert passive browsers into committed, repeat buyers.

Platforms such as TikTok Shop, Amazon Beauty, and regional equivalents across Southeast Asia have lowered the barrier to trial for new entrants while simultaneously enabling established players to capture incremental spend. This channel shift creates durable demand by reaching consumers in geographies where physical retail infrastructure remains underdeveloped, unlocking previously inaccessible volume pools and reshaping competitive dynamics across both premium and mass-market price tiers.

Restraints - Ingredient Safety Scrutiny and Regulatory Complexity

The cosmetic face mask market faces mounting pressure from regulatory bodies, including the European Chemicals Agency (ECHA) and the U.S. Food and Drug Administration (FDA), which are tightening permissible ingredient lists for leave-on and rinse-off facial formulations. Manufacturers relying on synthetic preservatives, fragrances, and certain chemical exfoliants must now invest in reformulation pipelines that can span 12 to 24 months per SKU, adding material cost and meaningful time-to-market risk.

Smaller brands operating across multiple jurisdictions face a disproportionate compliance burden relative to their larger peers, as harmonising labelling, claims substantiation, and safety dossiers across regions strains limited regulatory affairs resources. This complexity compresses margins and can delay product launches in high-value markets, particularly within the European Union and the United Kingdom, where post-Brexit divergence has effectively doubled the documentation workload for brands seeking pan-European distribution.

Consumer Price Sensitivity in Value-Tier Segments

While premiumisation drives growth at the top of the market, a significant portion of the Cosmetic Face industry's volume base remains concentrated in price-sensitive consumer cohorts across Latin America, South Asia, and parts of Africa. Raw material cost inflation, particularly for naturally derived actives such as kaolin clay, hyaluronic acid, and botanical extracts, has forced brands to either absorb margin pressure or pass costs to consumers, materially risking trade-down behaviour.

Private-label competition from major grocery retailers and discount chains further erodes the pricing power of mid-market brands, narrowing the differentiation gap between branded SKUs and store-owned alternatives. Without robust brand equity or a compelling efficacy narrative supported by visible results, manufacturers in this segment face structural margin compression that limits reinvestment capacity in marketing, R&D, and channel expansion, perpetuating a cycle of weakening competitiveness.

Opportunities - Premiumization of Organic and Clean-Label Formulations

The organic segment of the Cosmetic face mask market presents one of the most compelling near-term growth opportunities for brands willing to invest in certified ingredient sourcing and transparent communication strategies. Consumer willingness to pay a premium of 15-30% for certified organic or clean-label face masks is highest among millennials and Gen Z consumers in North America and Western Europe, two of the market's highest-revenue geographies and most influential trend-setting regions globally.

Brands that secure third-party certifications such as COSMOS Organic, ECOCERT, or USDA Organic and communicate ingredient provenance clearly through packaging and digital channels can command superior shelf positioning. Integrating supply chain traceability tools is increasingly critical, as transparency now functions as a competitive differentiator rather than a compliance requirement. First movers in markets where organic face care penetration remains below 10% of category value stand to capture durable share before consolidation occurs.

Innovation in Personalized and Technology-Enabled Face Mask Formats

The intersection of biotechnology, artificial intelligence, and dermatology is creating a new frontier within the global Cosmetic Face space, one where bespoke formulations, diagnostic-linked recommendations, and smart-delivery systems are redefining what a face mask can deliver. Companies that invest in AI-powered skin diagnostics, either through proprietary mobile apps or in-store retail kiosks, can convert single-purchase consumers into loyal subscribers aligned to structured quarterly skin-health programmes with measurable outcomes.

The personalised beauty segment is growing at nearly twice the rate of the standard cosmetic category, signalling strong consumer appetite for tailored solutions. Strategic partnerships with dermatology platforms and telehealth providers are increasingly valuable, as physician endorsement dramatically accelerates consumer trust and willingness to pay premium prices. Targeting the 35-55 age demographic, which prioritises efficacy over price, represents the highest-return strategy for technology-enabled product launches through the forecast period.

Category-wise Analysis

Product Type Insights

Sheet face mask occupy a leading position in the cosmetic face mask market by product type, registering 31% of total segment revenue in 2026, a dominance underpinned by the convenience of application, single-use hygiene appeal, and deep alignment with K-beauty routines that have achieved global mainstream adoption. The format's compatibility with diverse active ingredient payloads, ranging from niacinamide and ceramides to peptides and botanical essences, makes it the preferred vehicle for brand innovation across both mass and premium tiers.

Clay Face Mask emerges as the fast-growing segment within the product type category, driven by surging consumer interest in pore-cleansing and detoxifying routines, particularly among younger demographics discovering active skincare for the first time. The breadth of formats in scope, spanning Peel-off, Thermal, Cream, Warm-Oil, Gel, and other variants, ensures that the Cosmetic face mask market remains resilient to single-format saturation and sustains continued category-level innovation.

Nature Insights

Synthetic face mask holds the dominant position representing approximately 62% of total segment revenue in 2026, reflecting its advantages in formulation stability, longer shelf life, broader compatibility with active ingredients, and more accessible price positioning for the majority of global consumers. Synthetic formulations enable manufacturers to deliver consistent clinical results at scale, which supports retailer confidence, predictable replenishment cycles, and elevated repeat-purchase rates across mass-market channels.

Organic face mask is the fast-growing segment by nature, accelerating as consumers in high-income markets increasingly scrutinise ingredient labels and prioritise clean-label credentials in their purchase decisions. The organic segment's growth trajectory, while starting from a comparatively smaller base, is steadily compressing the synthetic segment's share lead and creating a structural bifurcation that brands must navigate through deliberate portfolio architecture and credible sustainability storytelling.

Packaging Format Insights

Sachets lead the cosmetic face mask market by packaging format, accounting for approximately 37% of total segment revenue in 2026, a position earned through cost efficiency, portability, precise single-dose dispensing, and strong alignment with both travel-retail and e-commerce formats. Sachets reduce product waste, a quality increasingly valued by sustainability-conscious consumers, and they lower the trial barrier for first-time users, making them an ideal acquisition vehicle in emerging markets and across promotional sampling campaigns.

Tubes represent the fastest-growing packaging format, gaining traction as brands reformulate cream and gel mask products for repeated, controlled-dose application that resonates with routine-oriented consumers. The packaging format segment, which also includes Jars and Bottles and other variants, reflects broader cosmetic industry shifts toward functional, sustainable, and experiential packaging design that supports both shelf differentiation and post-purchase consumer engagement throughout the product usage lifecycle.

Sales Channel Insights

Hypermarkets/Supermarkets retain the leading position by sales channel, capturing approximately 35% of total channel revenue in 2026, driven by unmatched physical reach, the ability to deliver browsing-to-purchase conversions through in-store displays and promotional mechanics, and established trust among broad consumer demographics across all regions. The channel's scale also provides manufacturers with valuable shelf data and promotional leverage that smaller, more fragmented retail formats cannot consistently match.

Online Retailers constitute the fastest-growing sales channel, accelerating on the back of expanding smartphone penetration, social commerce integration, and consumers' growing comfort with purchasing skincare digitally after reviewing influencer content and user-generated reviews. The full channel landscape, including Specialty Stores, Departmental Stores, Multi-brand Stores, Convenience Stores, and Pharmacy and Drug Stores, illustrates the Cosmetic face mask market's increasingly omnichannel commercial architecture and reinforces the value of integrated channel strategies.

Regional Insights

North America Cosmetic Face Mask Market Trends and Insights

North America represents a structurally mature yet dynamically evolving segment of the global Cosmetic face mask market, holding approximately 24% of global revenue in 2026. High disposable incomes, widespread dermatologist-endorsed skincare advocacy, and the rapid assimilation of K-beauty and clean-beauty philosophies into mainstream retail drive consumer demand in this region. The United States leads regional consumption, supported by a dense e-commerce infrastructure and strong influencer culture. Looking forward, continued premiumisation and the rise of men's facial care routines are expected to sustain mid-single-digit revenue growth across the region through 2033.

- United States Cosmetic Face Mask Market Size

The United States accounts for approximately 78% of total North America Cosmetic face mask market revenue, making it the single largest national market in the region. Demand is anchored by a highly engaged consumer base that prioritises skincare efficacy, ingredient transparency, and brand storytelling. The proliferation of dermatologist-led and clinically validated face mask products is accelerating trade-up from mass to premium tiers. Looking ahead, the men's grooming crossover and AI-powered skin personalisation are expected to open incremental revenue pockets in the U.S. market through the forecast period.

Europe Cosmetic Face Mask Market Trends and Insights

Europe maintains a significant and structurally differentiated position within the Cosmetic face mask market, accounting for approximately 22% of global revenue in 2026 and characterised by stringent regulatory oversight from the European Commission's Cosmetics Regulation (EC) No 1223/2009, which drives formulation discipline and ingredient innovation. Consumer demand skews toward clinical efficacy, sustainability certification, and minimal-ingredient formulations, particularly in Germany, France, and the United Kingdom.

The EU Green Deal and Farm to Fork Strategy are creating indirect tailwinds for organic face mask products. Forward-looking brands are aligning product innovation with circular packaging mandates to sustain competitiveness in this regulatory-sophisticated market.

- Germany Cosmetic face mask market Size

Germany commands approximately 21% of the European Cosmetic face mask market, reflecting its position as the continent's largest cosmetics consumer by volume. German consumers exhibit above-average preference for dermatologically tested, fragrance-free, and sustainability-certified face care products. The country's robust pharmacy and drug store channel anchored by dm-drogerie markt and Rossmann, provides face mask brands with high-velocity distribution. Looking ahead, rising male grooming adoption and premiumisation within the mid-market tier are expected to drive incremental growth in Germany through 2033.

- United Kingdom Cosmetic face mask market Size

The United Kingdom represents approximately 18% of European Cosmetic face mask market revenue in 2026, supported by a digitally sophisticated consumer base that actively discovers and purchases face care products through social commerce platforms, including Instagram and TikTok. Post-Brexit regulatory divergence from EU standards is creating a dual compliance burden for cross-border brands but simultaneously opening space for domestically produced and marketed clean-beauty formulations. Looking ahead, the UK's premium multi-brand retail environment, anchored by Boots and Space NK will continue to favour innovation-led face mask brands with compelling efficacy narratives.

- France Cosmetic face mask market Size

France holds approximately 16% of the Europe cosmetic face mask market revenue in 2026, underpinned by the country's globally recognised heritage in luxury cosmetics and dermatological skincare innovation, with industry clusters centred on Paris and the Île-de-France region. French consumers demonstrate strong loyalty to heritage brands while remaining receptive to premium international entrants that communicate scientific efficacy effectively. The country's pharmacy channel the pharmacie network, serves as a highly trusted distribution point for dermatologically aligned face mask products.

Looking ahead, the growing export influence of French cosmetic brands positions France as both a major consumer and a significant product innovation hub within the global Cosmetic face mask market.

Asia Pacific Cosmetic Face Mask Market Trends and Insights

Asia Pacific leads the global Cosmetic face mask market, commanding approximately 41% of total global revenue in 2026, the highest share of any region, driven by deeply embedded multi-step skincare routines, the global origination and export of K-beauty trends from South Korea, and the mass-market scale of consumer demand across China, Japan, India, and Southeast Asia. The region's youthful demographics, rising middle-class expenditure on personal care, and dense social commerce ecosystems create compounding demand drivers.

- Japan Cosmetic face mask market Size

Japan accounts for approximately 19% of Asia Pacific Cosmetic face mask market revenue in 2026, reflecting a consumer culture that treats facial masking as a sophisticated, science-informed ritual rather than a casual indulgence. Japanese consumers demonstrate exceptional willingness to pay for premium formulations featuring advanced actives such as fermented ingredients, collagen peptides, and sake extract. Domestic brands, including Shiseido and Kao Corporation, benefit from deep consumer trust and distribution excellence. Looking ahead, Japan's ageing population will drive sustained demand for anti-ageing and firming face mask formats through the forecast period.

- India Cosmetic face mask market Size

India represents approximately 12% of Asia Pacific Cosmetic face mask market revenue in 2026 and stands as one of the highest-potential high-growth sub-markets in the global Cosmetic Face industry. Rising urbanisation, a young median population age of approximately 28 years, and expanding smartphone-driven beauty discovery are collectively catalysing category awareness and trial. Ayurvedic-inspired and natural ingredient positioning resonates strongly with Indian consumers, giving both domestic brands and international entrants a clear product localisation pathway. Looking ahead, as e-commerce infrastructure deepens in Tier 2 and Tier 3 cities, India is expected to deliver above-regional-average growth ratess.

- Southeast Asia Cosmetic face mask market Size

Southeast Asia contributes approximately 15% of Asia Pacific Cosmetic face mask market revenue in 2026, with Indonesia, Thailand, Vietnam, and the Philippines serving as the primary demand engines within the sub-region. The confluence of tropical climate-driven skincare needs including excess sebum, enlarged pores, and hyperpigmentation, creates strong functional demand for clay, gel, and sheet face mask formats specifically.

Social commerce penetration through platforms including Shopee and Lazada is accelerating product discovery and purchase conversion at a remarkable speed. Looking ahead, Southeast Asia's rapidly growing beauty-conscious middle class and continued digital retail expansion position the sub-region as a high-priority.

Competitive Landscape

The cosmetic face mask market operates as a moderately fragmented competitive landscape where global beauty conglomerates, regional mid-market specialists, and digital-native challenger brands compete simultaneously across overlapping price tiers and consumer segments. Scale-driven players leverage global supply chains, portfolio breadth, and retail relationships to maintain category leadership, while differentiation-focused players compete on heritage, ingredient authenticity, and cultural capital.

The primary bases of competition are brand equity, formulation innovation, channel access, and packaging sustainability. A clear strategic bifurcation is emerging: incumbents are acquiring or partnering with clean-beauty and digital-native brands to capture younger consumer cohorts, while challenger brands invest in proprietary active ingredient platforms to build defensible long-term differentiation across global markets.

Key Developments:

- In March 2025, L'Oréal expanded its Garnier face mask portfolio across Southeast Asian e-commerce platforms, introducing 12 new SKUs targeting the budget-conscious yet ingredient-aware Gen Z segment, reinforcing the brand's omnichannel penetration strategy in high-growth emerging markets.

- In January 2025, Amorepacific launched a biodegradable sheet mask line under its IOPE brand, featuring a plant-derived cellulose substrate and certified COSMOS Organic actives, aligning product innovation with mounting sustainability expectations across European and North American premium retail channels.

- In October 2024, Shiseido announced a strategic investment in a South Korean biotech startup specialising in fermentation-derived peptide actives, signalling the company's intent to accelerate science-backed differentiation in the global premium Cosmetic face mask market segment ahead of the 2026 - 2033 growth cycle.

Cosmetic Face Mask Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.24 Billion |

| Current Market Value (2026) | US$ 8.00 Billion |

| Projected Market Value (2033) | US$ 13.89 Billion |

| CAGR (2026 - 2033) | 8.2% |

| Leading Region | Asia Pacific (41%) |

| Dominant Product Type | Sheet Face Mask (31%) |

| Top-ranking Nature | Synthetic Face Mask (62%) |

| Top-ranking Packaging Format | Sachets (37%) |

| Top-ranking Sales Channel | Hypermarkets/Supermarkets (35%) |

| Incremental Opportunity (2026 - 2033) | US$ 5.89 Billion |

Companies Covered in Cosmetic Face Mask Market

- L'Oréal

- Unilever

- Procter & Gamble

- Estée Lauder

- Shiseido

- Johnson & Johnson

- Amorepacific

- LG Household & Health Care

- Kao Corporation

- Beiersdorf

- Coty

- Avon

- Revlon

- Dr. Jart+

- Innisfree

- The Face Shop

- Origins Natural Resources

- Clinique Laboratories

- Sulwhasoo

- Freeman Beauty

- Peter Thomas Roth Labs

- Glamglow (a Unilever brand)

- Yes To Inc.

- Boscia LLC

- Tatcha LLC

Frequently Asked Questions

The Cosmetic face mask market is valued at US$ 8.00 Billion in 2026 and projected to reach US$ 13.89 Billion by 2033, growing at 8.2% CAGR.

Growth is driven by rising consumer adoption of routine-based preventive skincare and rapid expansion of digital, direct-to-consumer, and social commerce channels worldwide.

Sheet Face Mask leads with 31% share in 2026, driven by convenience, single-use hygiene appeal, and universal compatibility with diverse active ingredient formulations.

Asia Pacific dominates with 41% revenue share in 2026, supported by entrenched multi-step skincare rituals and a large, affluent, beauty-conscious consumer base.

Premiumisation of organic and clean-label formulations offers the strongest opportunity, with consumers paying 15-30% premiums and category penetration still below 10%.

The leading companies in the Cosmetic face mask market include L'Oréal, Unilever, Estée Lauder, Shiseido, Amorepacific, Kao Corporation, Johnson & Johnson, Beiersdorf, Dr. Jart+, and Innisfree.