- Food Packaging

- Cold Seal Packaging Market

Cold Seal Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Cold Seal Packaging Market by Material Type (Films, Polypaper / Paper-Based, Aluminum Foil & Foil Laminates), Industry (Food & Beverage, Pharmaceutical & Healthcare, Personal Care & Cosmetics, Home Care, Industrial Goods), Packaging Format (Wraps & Rollstock, Pouches, Sachets, Stick Packs, Bags), and Regional Analysis, 2026 - 2033

Cold Seal Packaging Market Size and Trend Analysis

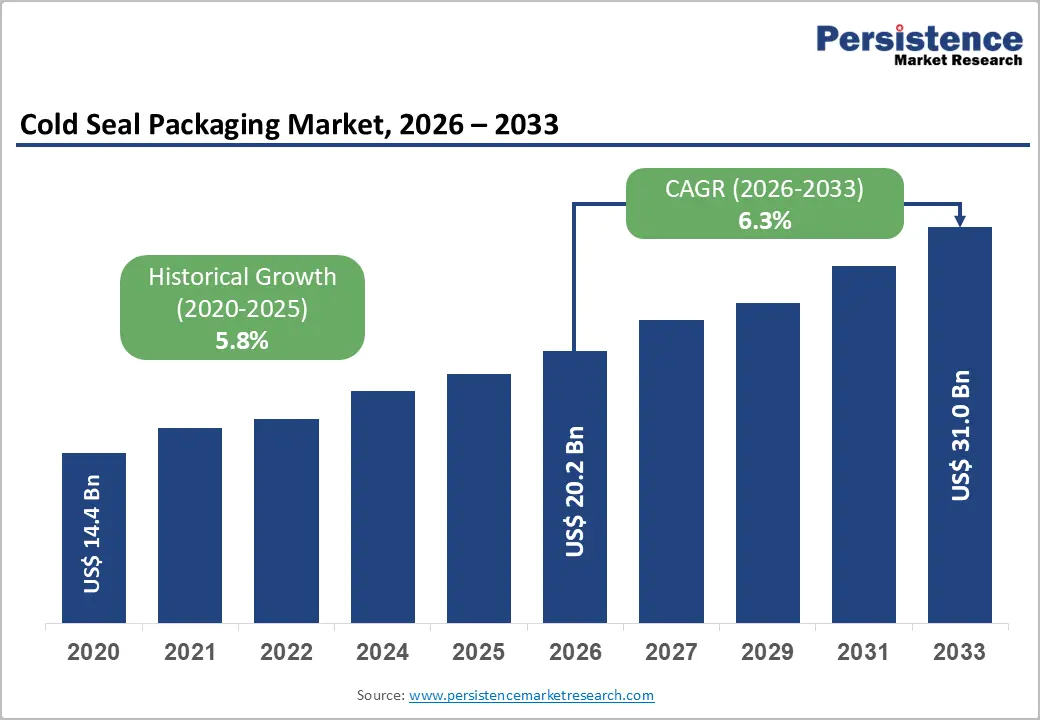

The global cold seal packaging market size is expected to be valued at US$20.2 billion in 2026 and projected to reach US$31 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The market expansion is anchored by heat-sensitive product categories that demand low-temperature sealing, particularly in confectionery, bakery, and medical device packaging, where heat-based sealing risks product degradation.

According to the U.S. Food and Drug Administration (FDA), chocolate and cocoa products lose structural integrity above 34°C, reinforcing demand for cold seal substrates. Concurrently, the shift toward recyclable mono-material films, momentum behind the EU Packaging and Packaging Waste Regulation (PPWR), and rapid throughput requirements on high-speed flow-wrap lines collectively reinforce adoption across food, pharmaceutical, and personal care converters.

Key Industry Highlights:

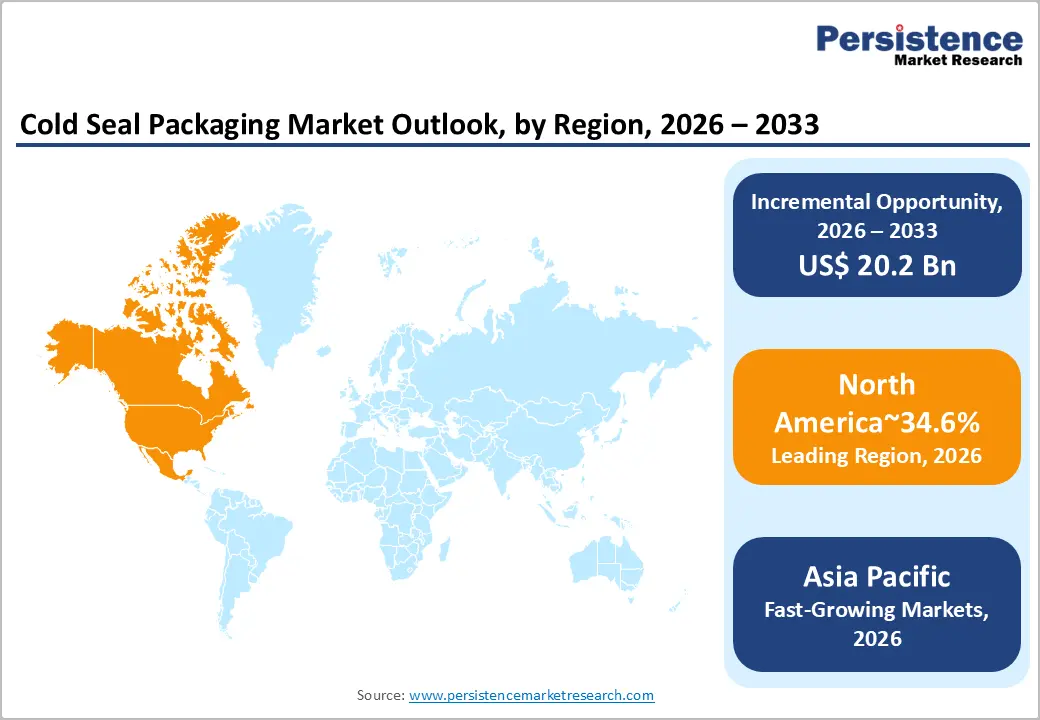

- Leading Region: North America commands a 34.6% share in 2025, anchored by the US$48 billion U.S. confectionery sector and an established medical device pouching base.

- Fast-Growing Market: Asia Pacific, holding 29.8% share in 2025, is expanding fastest, led by China's confectionery output and India's US$535 billion food processing sector projection.

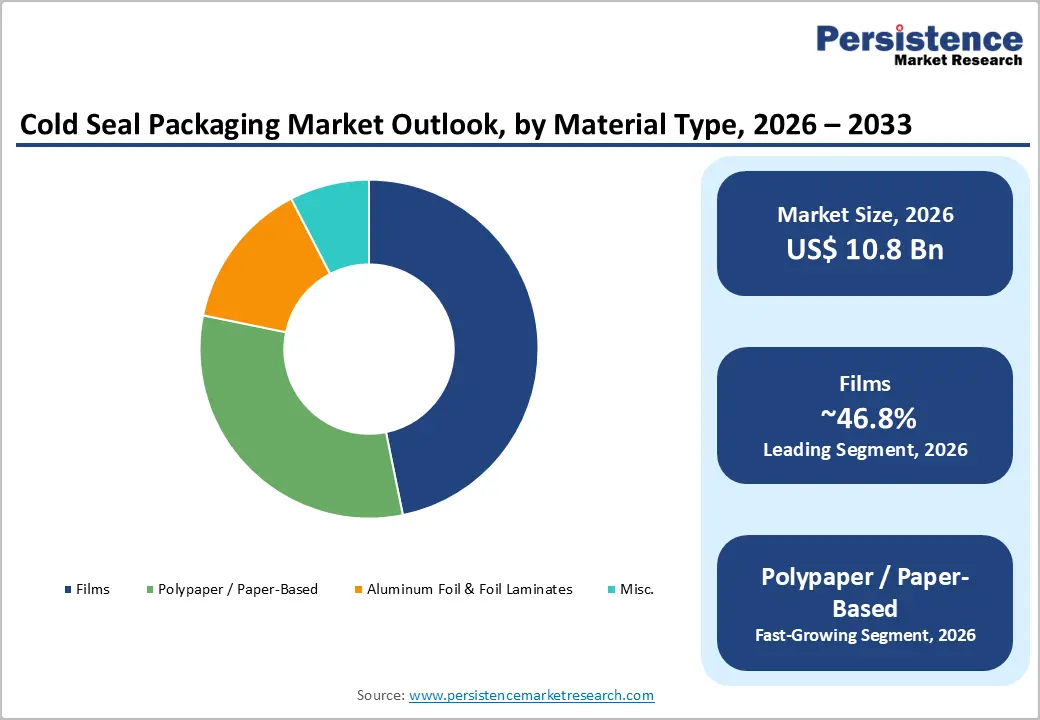

- Leading Material: Films lead the material category with 47% share in 2025, owing to BOPP and PET clarity, print receptivity, and machinability on high-speed flow-wrap lines.

- Fast-Growing Material Segment: Polypaper/Paper-Based substrates expand at 6% CAGR, propelled by the EU SUPD, PPWR, and brand owner shifts to plastic-free shelf positioning.

- Key Opportunity: Mono-material polypropylene structures aligned with the EU PPWR 2030 recyclability mandate and Ellen MacArthur Foundation Global Commitment offer converters a multi-year reformulation runway.

DRO Analysis

Drivers - Heat-sensitive Confectionery and Bakery Production Demand Low-temperature Sealing Technology

Cold seal packaging remains the technology of choice for chocolate bars, energy bars, ice cream novelties, and laminated bakery items where conventional heat sealing causes melting, blooming, or texture loss. According to the International Cocoa Organisation (ICCO), global cocoa grindings reached 4.93 million tonnes in the 2023/24 season, while the U.S. Department of Agriculture (USDA) reports that confectionery shipments contribute over US$48 billion to American manufacturing output annually.

Production lines running at 1,200-1,500 packs per minute further necessitate cohesive cold seal coatings that bond on contact without thermal dwell, reinforcing converter preference across high-throughput confectionery operations.

Sterile Barrier Requirements for Medical Devices Reinforce Pharmaceutical Packaging Conversion

Pharmaceutical and medical-device manufacturers depend on cold seal pouches for sterile barrier systems that must remain stable through ethylene oxide (EtO) or gamma sterilisation. The U.S. FDA recognizes ISO 11607 as the consensus standard for terminally sterilised device packaging, and MedTech Europe reports that the European medical technology sector generates over €160 Billion in annual sales with more than 36,000 companies relying on validated barrier packaging. Cold-sealable Tyvek and paper laminates deliver peel-open integrity without thermal stress on adhesives, supporting consistent uptake across surgical kits, catheters, and diagnostic device pouching converters.

Restraints - Latex Sensitivity Concerns Limit Natural Rubber Cohesive Adoption

Traditional cold seal coatings rely on natural rubber latex, which presents allergen risks for both consumers and packaging line workers. The U.S. Centers for Disease Control and Prevention (CDC) estimates that 8-12% of healthcare workers exhibit latex sensitisation, while the FDA mandates labeling for latex-containing medical packaging under 21 CFR Part 801.s

These regulatory headwinds, combined with consumer advocacy in the EU under REACH, have constrained the use of latex-based cohesives in food-contact applications, forcing converters to invest in synthetic alternatives that often carry a 15-20% cost premium over conventional formulations.

Recyclability Concerns for Multi-layer Laminated Structures

Cold seal flow wraps often combine polyethylene, polypropylene, and metallised layers, structures that the Association of Plastic Recyclers (APR) categorises as problematic for curbside recycling streams. Under the EU Packaging and Packaging Waste Regulation (PPWR), all packaging placed on the EU market must be recyclable by 2030, and member states such as Germany impose extended producer responsibility fees that can reach €1,500 per tonne for non-recyclable laminates. This regulatory environment pressures brand owners to redesign existing cold seal SKUs, slowing reorder cycles and capital deployment.

Opportunities - Mono-material Polypropylene Structures Aligned With Circular Economy Mandates

The shift toward mono-material polypropylene (PP) cold seal films presents a substantial opportunity for converters seeking PPWR compliance ahead of the 2030 EU deadline. According to Plastics Europe, polypropylene accounts for 19.7% of European plastic converter demand and is one of only four polymers with established mechanical recycling infrastructure.

Leading converters have launched all-PP cold seal laminates that retain machinability on legacy flow-wrap equipment running at 1,000+ packs per minute. This transition is reinforced by retailer commitments, with members of the Ellen MacArthur Foundation Global Commitment representing over 20% of global plastic packaging volume pledging recyclable, reusable, or compostable designs, creating a multi-year reformulation runway for cold seal substrate suppliers.

Paper-based Cold Seal Substrates Serving Plastic-free Shelf Positioning

Polypaper and barrier-coated paper substrates represent the fastest-growing material category at a 6% CAGR between 2026 and 2033, driven by retailer pledges and the Single-Use Plastics Directive (SUPD) in the European Union. Eurostat data indicate that paper and cardboard packaging waste reached 41.1 million tonnes across the EU in 2022, with a recycling rate of 82.5%

the highest of any packaging material, giving brands a compelling sustainability narrative. Confectionery majors, including Mars Wrigley and Nestlé, have piloted paper-wrap chocolate bars across European supermarkets, while Mondi and Smurfit Westrock have commercialised barrier paper grades compatible with existing cold seal coating lines, expanding the addressable opportunity for converters.

Category-wise Analysis

Material Type Insights

Films dominate the cold seal packaging market with an estimated 47% share in 2026, anchored by polypropylene (BOPP), polyethene, and PET substrates that combine clarity, machinability, and barrier performance. According to Plastics Europe, BOPP demand exceeded 8 million tonnes globally in 2023, with confectionery flow wraps representing one of the largest converter end-uses.

The films category benefits from compatibility with high-speed flow-wrap equipment operating above 1,200 packs per minute, excellent print receptivity for high-graphic SKUs, and proven cold-seal cohesive anchorage. Continuous structural innovations from suppliers such as Jindal Films and Taghleef Industries toward recycle-ready mono-material BOPP further entrench films as the leading substrate.

Industry Insights

Food & beverage commands the leading position with roughly 58% share of the cold seal packaging market in 2025, with confectionery, bakery & snacks, and frozen/ready-to-eat foods driving the bulk of converter volume.

The U.S. Department of Agriculture (USDA) reports that U.S. food and beverage manufacturing accounted for 16.8% of total manufacturing sales in 2021 and employed approximately 1.7 million workers, while in the European Union, the accommodation and food services sector generated €280.7 Billion in value added in 2022, according to Eurostat. Cold seal is indispensable for chocolate bars, granola products, and frozen novelties where heat sealing compromises product integrity, anchoring sustained demand from packaged-food converters across developed and emerging geographies.

Packaging Format Analysis

Wraps & Rollstock hold the leading packaging format share at approximately 44% in 2026, owing to their dominance in single-serve confectionery, energy bars, and individual cookie portions. According to the National Confectioners Association (NCA), U.S. confectionery sales exceeded US$48 billion in 2023, with an overwhelming majority of unit volume distributed via flow-wrapped formats.

Cold seal rollstock enables converters to operate horizontal flow-wrap machines at speeds exceeding 1,500 packs per minute without the dwell time required by heat-seal alternatives, translating directly into higher line OEE. Leading suppliers, including Sonoco Products Company and Amcor plc, continue to invest in lightweight, mono-material rollstock to support recyclability mandates while maintaining throughput economics.

Regional Insights

North America Cold Seal Packaging Market Trends and Insights

North America holds a 34.6% share of the global cold seal packaging market in 2026, supported by a mature confectionery industry, leading pharmaceutical converters, and the highest per-capita consumption of single-serve snack formats globally. Key trends include accelerated adoption of recycle-ready mono-PE structures, How2Recycle on-pack labelling penetration, and reshoring of medical device pouching capacity post-pandemic.

U.S. Cold Seal Packaging Market Trends

The U.S. cold seal packaging market is valued at US$5.9 billion in 2026, driven by strong demand from the confectionery, healthcare, frozen food, and nutraceutical packaging industries. The country accounts for the largest share within North America due to its advanced flexible packaging infrastructure, high penetration of automated flow-wrap packaging systems, and the presence of major consumer packaged goods manufacturers.

Growth is strongly supported by the US$48 billion confectionery sector tracked by the National Confectioners Association (NCA), alongside rising consumption of protein bars, ready-to-eat snacks, and portion-controlled packaged foods requiring high-speed cold seal wrapping solutions

Europe Cold Seal Packaging Market Trends and Insights

Europe accounts for 24.1% of the global cold seal packaging market in 2025, shaped by the most aggressive sustainability regulation worldwide. The EU Packaging and Packaging Waste Regulation (PPWR) mandating recyclability by 2030, combined with Germany's extended producer responsibility framework and the UK Plastic Packaging Tax of £217.85 per tonne, is accelerating the substitution of multi-layer laminates with mono-PP and paper-based cold seal substrates.

Germany Cold Seal Packaging Market Size

Germany commands the leading position in Europe with a market value of US$ 1,135.0 Million in 2026 driven by its position as Europe's largest confectionery exporter and a stringent VerpackG packaging law. The country hosts converters such as Constantia Flexibles and is home to chocolate giants Ritter Sport and Storck, reinforcing demand for high-performance cold seal substrates.

U.K. Cold Seal Packaging Market Size

The U.K. cold seal packaging market reached US$ 851.7 million in 2026, supported by the UK Plastic Packaging Tax, which levies £217.85 per tonne on packaging containing less than 30% recycled content. Major snack and confectionery converters, including Mondelez UK and Cadbury, have accelerated mono-material substrate rollouts, anchoring sustained demand across flow-wrapped SKUs.

France Cold Seal Packaging Market Size

France accounts for approximately US$ 612 million in 2026, equivalent to nearly 13% of the European regional total. The AGEC Law (Anti-Waste for a Circular Economy Act) prohibits non-recyclable plastic packaging and mandates reuse targets, while bakery exports valued at over €2.5 Billion annually per FranceAgriMer sustain cold seal demand from converters such as Barry Callebaut France.

Asia Pacific Cold Seal Packaging Market Trends and Insights

Asia Pacific holds a 29.8% share of the global cold seal packaging market in 2026 and is the fastest-growing region, powered by China's confectionery output, India's expanding packaged food sector, and Japan's premium medical device exports. China alone contributes nearly 38% of regional cold seal demand, with regional converters scaling mono-PP substrate capacity to serve both domestic and export channels.

China Cold Seal Packaging Market Size

China leads the Asia Pacific region with a market value of US$2,174.2 million in 2026, propelled by the world's largest confectionery and snack manufacturing base. According to the China National Food Industry Association, domestic confectionery output exceeded 3.2 million tonnes annually, with converters such as Want Want and Hsu Fu Chi anchoring flow-wrap demand across single-serve formats.

India Cold Seal Packaging Market Size

India represents the fast-growing market in Asia Pacific, valued at US$ 1,285.2 million in 2026. The food processing sector contributed 8.8% of manufacturing GVA in 2024 per the Ministry of Food Processing Industries (MoFPI), supported by 41 Mega Food Parks and US$13.4 billion in cumulative FDI inflows, with converters such as UFlex and Huhtamaki India expanding cold seal capacity.

Competitive Landscape

The global cold seal packaging market is moderately consolidated, with the top five players accounting for an estimated 45% of global revenue. Leaders such as Amcor plc, Sonoco Products Company, Mondi Group, and Constantia Flexibles differentiate through proprietary cohesive chemistries, mono-material substrate platforms, and integrated print-and-convert capabilities.

Strategic initiatives center on capacity expansion in Asia, M&A targeting speciality coater assets, and joint R&D with brand owners on recycle-ready laminates. Emerging business models include closed-loop take-back programs and digital print-on-demand offerings, which are reshaping converter-brand relationships across confectionery and pharmaceutical end-uses.

Key Developments:

- In March 2025, SPG introduced its Cold Seal packaging solution to expand its flexible packaging portfolio, offering heat-free sealing technology designed for heat-sensitive and high-speed packaging applications such as chocolate, energy bars, and ice cream, enabling seamless integration into existing production lines without machine adjustments or additional operational costs.

- In October 2023, American Packaging Corporation, Bostik, and Charter Next Generation collaborated to develop an APR-approved recyclable polyethylene cold seal film structure that passed critical recycling guidance testing, enabling brand owners to maintain Store Drop-off recyclability certification while advancing sustainable and market-compliant cold-seal packaging solutions.

Companies Covered in Cold Seal Packaging Market

- PSG

- Uniflex

- Swisspac

- Watershed Packaging

- American Packaging Corporation

- Cortec Corporation

- Altea Packaging

- Pouch Makers Canada

- Hatzopoulos S.A.

- Guanzhou Heyusheng

- Enmalyn

- Rizon Group

- CP Flexible Packaging

Frequently Asked Questions

The global cold seal packaging market is valued at US$ 20.2 Billion in 2026 and is projected to reach US$ 31.0 Billion by 2033, registering a 6.3% CAGR over the forecast period.

Heat-sensitive confectionery, bakery, and frozen food production, combined with sterile barrier requirements under ISO 11607 for medical devices, is the principal demand driver for cold seal substrates.

North America leads the market with a 34.6% share in 2025, supported by the US$ 48 Billion U.S. confectionery industry and the world's largest medical device manufacturing base.

Mono-material polypropylene and paper-based, recycle-ready substrates aligned with the EU PPWR 2030 mandate and Ellen MacArthur Foundation Global Commitment represent the largest opportunity for converters and substrate suppliers.

Leading players include Amcor plc, Sonoco Products Company, Mondi Group, Constantia Flexibles, Sealed Air Corporation, Huhtamaki Oyj, ProAmpac LLC, and UFlex Limited.