Cloud-based Cold Chain Management Market

Industry: IT and Telecommunication

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 192

Report ID: PMRREP35027

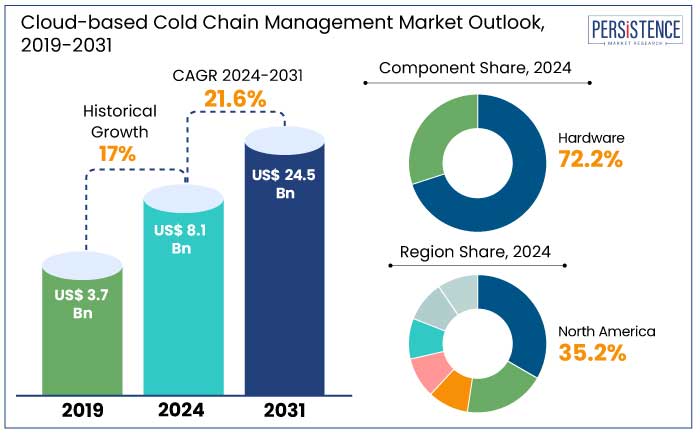

The global cloud-based cold chain management market is expected to be valued at US$ 8.1 Bn by 2024. It is anticipated to experience a healthy CAGR of 21.6% during the forecast period to reach a value of US$ 24.5 Bn by 2031. By the end of the forecast period, 85% of cold chain logistic providers are estimated to use IoT devices.

Advancements in IoT-enabled sensors are estimated to make them advanced, thereby offering precise temperature, humidity, and location monitoring. Companies are estimated to leverage AI-powered systems to optimize routes, forecast risks like equipment failure and improve decision-making. Predictive analytics is anticipated to decrease spoilage by 20% to 30%, thereby saving billions.

Stringent global food safety standards, like FSMA and Hazard Analysis and Critical Control Points (HACCP), are estimated to drive the adoption of cloud-based solutions. By 2031, compliance with these standards is predicted to account for 25% of investments in cloud-based chain systems.

Key Highlights of the Industry

|

Market Attributes |

Key Insights |

|

Cloud-based Cold Chain Management Market Size (2024E) |

US$ 8.1 Bn |

|

Projected Market Value (2031F) |

US$ 24.5 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

21.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

17% |

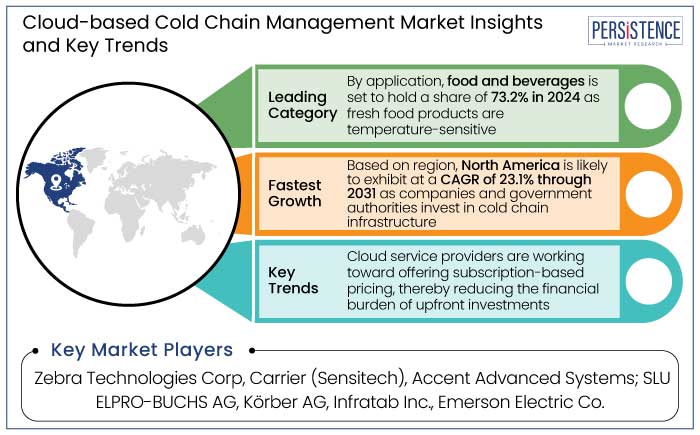

North America is predicted to hold a share of 35.2% in 2024. The region has a well-established technological infrastructure, with widespread adoption of IoT sensors, cloud computing, and real-time monitoring solutions. These technologies are the prominent drivers of cloud-based cold chain management systems.

The U.S. Food and Drug Administration’s (FDA) FSMA, has driven substantial adoption of cloud-based cold chain systems. The U.S. has the largest pharmaceutical industry which is heavily regulate and therefore requires robust cold chain management solutions for biologics, vaccines, and temperature-sensitive drugs. North America is a hub for e-commerce giants like Amazon, Walmart, and Instacart, which require efficient cold chain management for online grocery deliveries and food products.

Companies and government authorities in the region are heavily investing in cold chain infrastructure to meet the rising demand for perishable goods. DHL and Maersk are implementing energy-efficient refrigerated trucks and cold storage solutions across the region, aligning with the broader sustainability goals of decreasing carbon footprints. By 2030, North America is estimated to achieve a 50% adoption rate for carbon-neutral logistics in the cold chain sector, owing to demand for energy-efficient solutions and regulatory pressure.

Hardware is predicted to emerge as the leading component with a share of 72.2% in 2024. Global adoption of IoT devices in cold chain logistics is estimated to reach 80% by 2025, which largely driven by sensors, GPS devices, and data loggers that monitor temperature, location, and environmental conditions.

Hardware devices including refrigerated containers, trucks, and cold storage units equipped with IoT-enabled sensors ensure that goods are kept at the required temperatures throughout their journey. The adoption of temperature-controlled units integrated with sensors assists businesses to avoid temperature fluctuations that could lead to spoilage.

The growing demand for automated cold storage facilities is another factor driving hardware adoption. Automated warehouses equipped with temperature-controlled systems and IoT sensors facilitate labor cost reduction while enhancing the efficiency of managing perishable goods.

Compliance with several regulations requires the installation of hardware devices such as sensors and monitoring systems to meet legal requirements for food and pharmaceutical transportation.

Food and beverages is estimated to emerge as the leading application in the industry with a share of 73.2% in 2024. Global demand for fresh and perishable food products is witnessing rapid growth owing to population growth, urbanization, and changing consumer preference for healthy, fresh, and organic food.

Fresh vegetables, fruits, seafood, and meat are highly temperature-sensitive and require a robust cold chain infrastructure to ensure their quality and shelf life. The Food Safety Modernization Act (FSMA) in the U.S. mandates that food companies implement real-time tracking, monitoring, and documentation of temperature-sensitive food during transit. Consequently, increasing the adoption of cloud-based cold chain management systems.

A study conducted by the U.S. Food and Drug Administration (FDA) revealed that 40% of foodborne illnesses are caused by improper handling and storage of food, highlighting the crucial role of temperature monitoring in food safety. Cloud-based systems enable end-to-end traceability in the food supply chain, ensuring compliance with HACCP (Hazard Analysis and Critical Control Points) standards for food safety.

The cloud-based cold chain management market is predicted to be driven by the emergence of AI-driven systems that assist in predicting risks, optimizing routes, and improving energy efficiency. Expansion of blockchain technology for secure and immutable records of supply chain events is likely to emerge as a key growth driver.

Manufacturers in the industry are focusing on sustainability by adopting energy-efficient refrigeration and renewable energy-powered cold storage to meet environmental goals. They are also progressively investing in eco-friendly refrigerants and carbon neutral logistics solutions. Integration of autonomous vehicles including refrigerated trucks and drones are likely to become integral for last-mile delivery, improving cold chain efficiency.

The cloud-based cold chain management market growth was robust at a CAGR of 17% during the historical period. Key growth driver during the period were advancements in technology that facilitates the adoption of IoT-enabled sensors, GPS, and real-time tracking solutions powered by cloud platforms.

The COVID-19 pandemic period gave rise to biologics, vaccines, and personalized medicines that required robust cold chain systems. Vaccine distribution efforts in 2021 to 2022 for the COVID-19 drove massive investments in ultra-cold storage and monitoring solutions. Governments and private sectors invested significantly in cloud-based systems to ensure vaccine safety and compliance.

Platforms like Amazon Fresh, Instacart, and Alibaba’s Freshippo contributed to increased demand for cold chain solutions. Governments enforced stringent compliance requirements, such as FSMA in the U.S. and GDP guidelines in Europe, pushing companies to adopt advanced cold chain solutions.

Continuous emphasis on sustainability, regulatory compliance, and traceability are likely to drive adoption in the coming years. Technological innovations including the adoption of edge devices to process data locally, decrease latency, and dependence on stable internet connections is estimated to be a prominent growth driver.

Rising Demand for Perishable Goods

Growing demand for perishable goods like pharmaceuticals and food and beverages is a prominent growth driver for the cloud-based cold chain management market. COVID-19 vaccines highlighted the need for robust cold chain systems, as certain vaccines require ultra-low temperatures.

Cold chain logistics in pharmaceuticals accounts for 25% of total logistics costs, thereby underscoring the sectors’ reliance on precise temperature control. Around 20% of pharmaceutical products are temperature-sensitive, posing a need for reliable cold chain solutions to maintain efficacy and safety.

Consumers prefer frozen and chilled ready-to-eat meals, dairy products, and seafood owing to convenience and long shelf life. Approximately 1.3 billion tons of food is wasted annually. Cloud-based cold chain management systems assist in decreasing spoilage through real-time monitoring. Biologics usually requires precise temperature ranges for transport and storage, thereby making cloud-based monitoring critical.

Growth of E-commerce and Online Grocery

Online grocery sales in the U.S accounted for 13% of the total grocery sales in 2023. A survey revealed that 60% of consumers are willing to continue buying groceries online post-pandemic. Rising adoption of subscription services further drives the demand for cold chain logistics.

Customer demand same-day or next-day delivery for fresh produce, dairy, and frozen goods, requires efficient cold chain systems. Companies are progressively offering specialized delivery options like temperature control lockers and curb side pickup.

Last-mile delivery accounts for 53% of overall shipping costs, creating opportunities for cloud-based cold chain platforms to optimize routes and monitor conditions in real-time. Approximately 30% to 40% of fresh produce is wasted during transportation across the globe.

Cloud-based cold chain management decreases this waste by providing real-time data on temperature excursions and ensuring timely corrective actions. Meal kit delivery services mainly depend on cold chain logistics to ensure freshness and compliance with food safety standards.

Uncertainty in ROI Remains a Primary Barrier

A study conducted in 2023 revealed that 47% of companies cited uncertain ROI as the primary barrier to adopt cloud-based cold-chain management systems. Companies need to allocate significant capital for IoT-enabled sensors, cloud platforms, and integration with existing systems. Savings from decreased spoilage, enhanced efficiency, and regulatory compliance vary widely across industries and regions.

Benefits of adopting cloud-based solutions may be limited in regions with inadequate cold chain infrastructure due to underlying systemic inefficiencies. Intangible benefits like improved compliance, enhanced customer satisfaction, and decreased risk of recalls are difficult to quantify, making it difficult to justify the investment. A study revealed that nearly 30% of logistic companies have a clear understating of potential cost savings and revenue gains from cloud-based solutions.

Investment in Cold Chain Infrastructure

Increasing global trade of perishable goods such as seafood, fruits, vegetables, and biopharmaceuticals requires expanded cold storage and transport facilities. The pharmaceutical industry is investing heavily in cold chain solutions due to the rise in biologics, vaccines, and personalized medicine. As consumers pose a demand for fresh, organic, and minimally processes food, the demand for efficient cold storage and transportation systems increases.

The industry is witnessing an expansion of warehouses with advanced refrigeration technologies to store goods at controlled temperatures. The global cold storage capacity reached 719 million cubic meters in 2023, with significant growth in emerging markets like India and China. Companies are investing in refrigerated trucks, containers, and cargo planes for efficient transportation of goods.

Regulatory and Compliance Requirements

Governments across the globe have implemented stringent standards to ensure the safety, efficacy, and quality of temperature-sensitive products. This necessitates advanced cold chain solutions that are capable of real-time monitoring, traceability, and compliance reporting.

The FSMA (Food Safety Modernization Act) of the U.S., requires companies to monitor and document temperature control for perishable food throughout the supply chain. The European Union EC Regulation No. 852/2004 and No. 853/2004 mandate cold storage and transportation for frozen and chilled food to prevent spoilage.

Codex Alimentarius developed by FAO and WHO provides international food safety guidelines that include cold chain management for global trade. GDP guidelines from the World Health Organization (WHO) and European Union require strict temperature control and traceability during pharmaceutical distribution. Regulations on energy consumption and refrigerant use, such as the Kigali Amendment to the Montreal Protocol, encourage the adoption of eco-friendly cold chain solutions.

Companies in the cloud-based cold chain management market are incorporating IoT-enables sensors for real-time tracking of temperature, humidity, and location. They are using AI to predict potential issues like temperature excursions and optimize routes for efficiency.

Businesses are implementing blockchain technology for secure, traceable, and tamper-proof supply chain data. They are utilizing automation in data collection, monitoring, and reporting to improve accuracy and decrease manual errors.

Organizations are offering customized solutions for specific industries like pharmaceuticals, food, and chemicals. They are adding advanced features like predictive maintenance, anomaly detection, and compliance monitoring. They are also expanding their product lines to include hardware and software.

Recent Industry Developments

|

Attributes |

Detail |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Component

By Application

By Region

To know more about delivery timeline for this report Contact Sales

The market is anticipated to reach a value of US$ 24.5 Bn by 2031.

Cloud supply chain management uses cloud-based software to automate and oversee key processes.

North America to lead the market with a share of 35.2% in 2024.

Prominent players in the market are Zebra Technologies Corp, Carrier (Sensitech), and Accent Advanced Systems.

The market is predicted to witness a CAGR of 21.6% through 2031.