- Healthcare Services

- Cleanroom Disinfectant Market

Cleanroom Disinfectant Market Size, Share, and Growth Forecast 2026 – 2033

Cleanroom Disinfectant Market by Product Type (Oxidizing Disinfectants [Hydrogen Peroxide, Chlorine, Iodine, Others], Non-oxidizing Disinfectants [Alcohol, Phenols, Quaternary Ammonium Compounds, Others]), End-user (Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Hospitals, Food & Beverage Industry, Others), and Regional Analysis, 2026–2033

Cleanroom Disinfectant Market Share and Trends Analysis

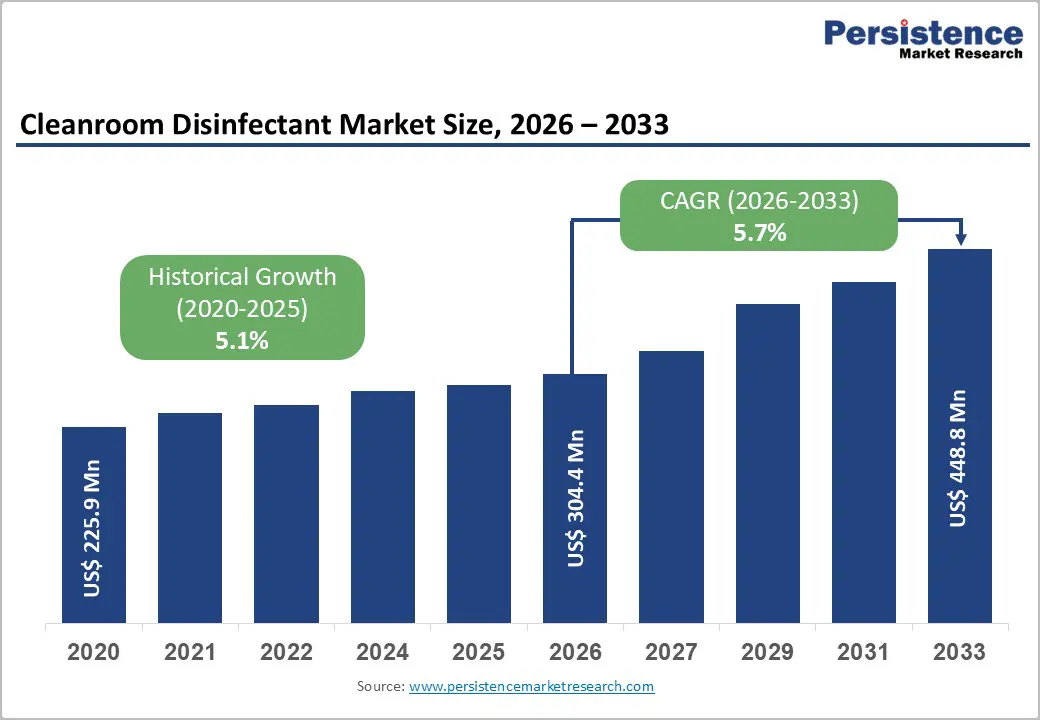

The global cleanroom disinfectant market size is expected to be valued at US$ 304.4 million in 2026 and projected to reach US$ 448.8 million by 2033, growing at a CAGR of 5.7% between 2026 and 2033, growing steadily due to rising demand for contamination control across pharmaceutical manufacturing, biotechnology, medical devices, hospitals, and food processing industries.

These disinfectants are essential for maintaining sterile environments, preventing microbial contamination, and ensuring compliance with strict regulatory standards such as FDA and EU GMP guidelines. Increasing production of biologics, vaccines, and cell therapies has further accelerated adoption in controlled environments. Market growth is also supported by the rising use of ready-to-use wipes, low-residue formulations, and eco-friendly disinfectant solutions.

Key Industry Highlights:

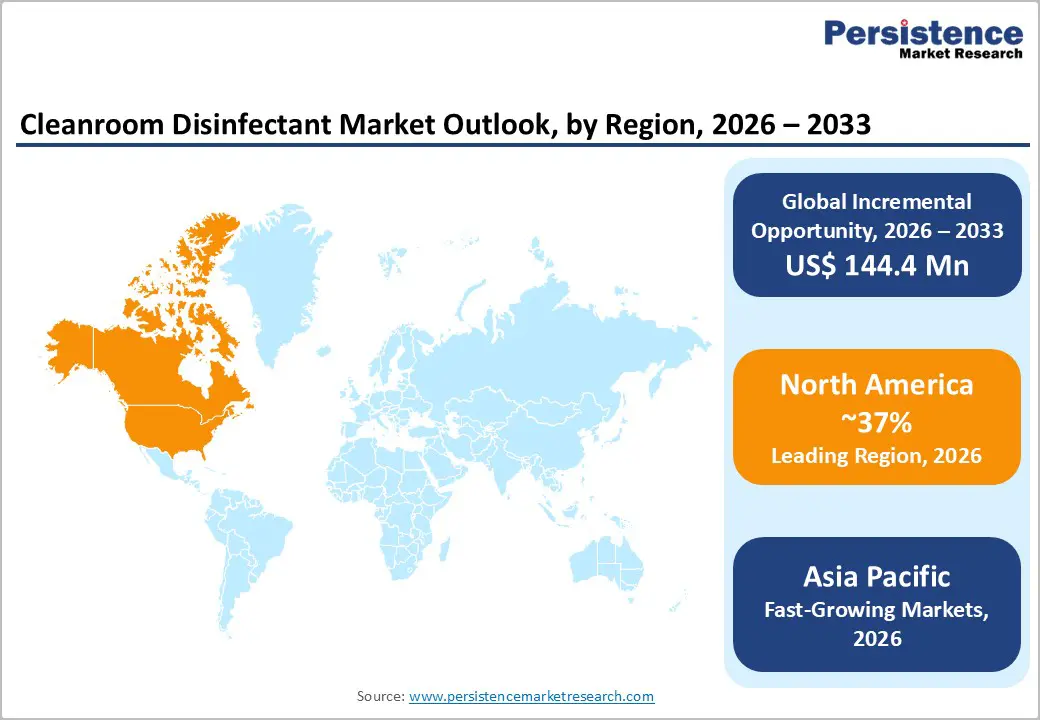

- Leading Region – North America dominates the global Cleanroom Disinfectant market with approximately 37% share in 2025, supported by the world's highest density of FDA-regulated GMP pharmaceutical facilities and updated USP <797> cleanroom disinfection compliance mandates.

- Fast-growing Market – Asia Pacific is the fastest-growing cleanroom disinfectant region through 2033, propelled by China's systematic GMP infrastructure upgrades, India's generics manufacturing scale under the PLI scheme, and Singapore's globally significant biopharmaceutical cluster.

- Dominant Product Segment – Oxidizing disinfectants lead the product type category with approximately 56% share in 2026, driven by mandatory sporicidal requirements under EU GMP Annex 1 (2023) and ISO 14644 standards for Grade A/B pharmaceutical cleanroom environments.

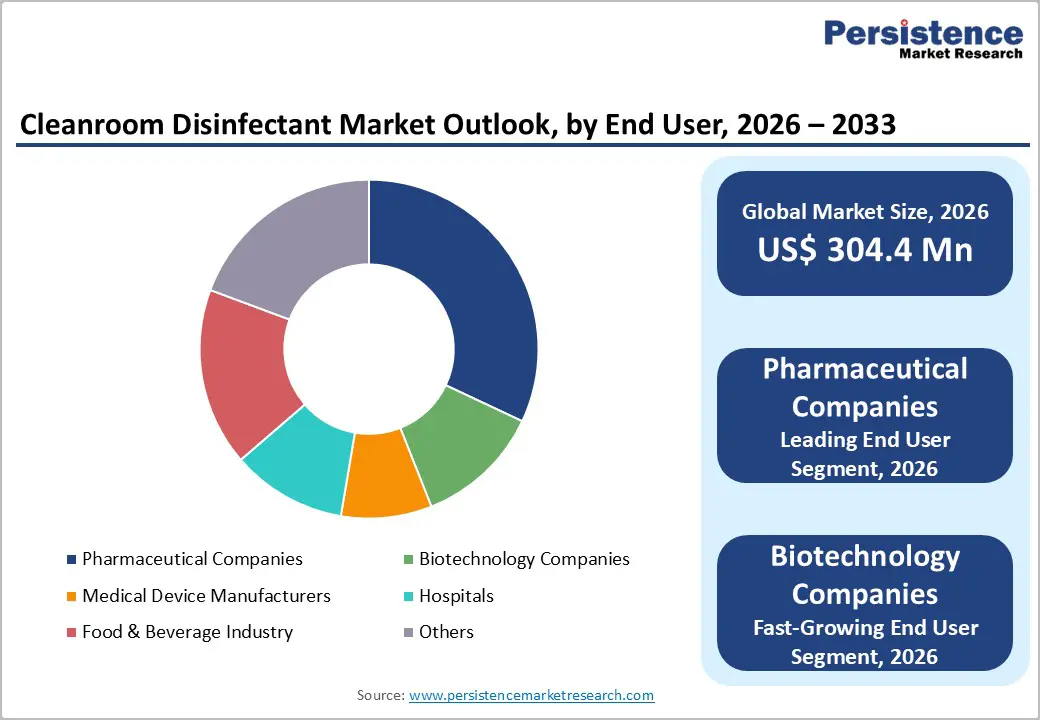

- Fast-Growing End-user Segment – Biotechnology companies are the fast-growing end-user segment, fueled by record biologic drug approvals by the FDA's CBER, mRNA vaccine manufacturing expansion, and cell and gene therapy facilities requiring specialized ISO Class 5–7 cleanroom disinfection programs.

- Key Opportunity: Vaporized Hydrogen Peroxide (VHP) decontamination technology represents a high-value growth frontier delivering validated 6-log sporicidal efficacy with zero residues, directly aligned with intensifying EU GMP Annex 1 aseptic processing validation requirements and RABS/isolator adoption trends.

Market Dynamics

Drivers – Rise in GMP Compliance Requirements in Pharmaceutical and Biopharmaceutical Manufacturing

Stringent Good Manufacturing Practice (GMP) regulations enforced by the FDA, EMA, and the World Health Organization (WHO) are the most powerful structural driver of the Cleanroom Disinfectant market. Cleanrooms classified as ISO Class 5 through ISO Class 8, as defined by ISO 14644-1, require validated, rotation-based disinfection protocols using multiple product classes to prevent microbial resistance buildup.

According to the FDA's Center for Drug Evaluation and Research (CDER), pharmaceutical manufacturing warning letters citing inadequate environmental monitoring and disinfection practices have increased by over 30% in the five years preceding 2024, directly incentivizing investment in validated disinfectant programs. The global biopharmaceutical contract manufacturing sector, projected by the Pharmaceutical Research and Manufacturers of America (PhRMA) to continue capacity expansion by 2030, further multiplies the addressable demand for cleanroom-grade disinfectants.

Post-Pandemic Intensification of Contamination Control Protocols Across Healthcare and Industry

The COVID-19 pandemic fundamentally elevated institutional awareness of contamination control, triggering lasting upgrades in decontamination protocols across hospitals, pharmaceutical facilities, medical device manufacturers, and food processing environments. The U.S. Centers for Disease Control and Prevention (CDC) and WHO issued updated environmental disinfection guidelines during the pandemic that have since been largely retained as permanent operational standards. Hospitals globally expanded their cleanroom-grade sterile compounding facilities post-pandemic.

The American Society of Health-System Pharmacists (ASHP) reports that USP Chapter <797> compliance requirements, which mandate validated disinfectants for sterile compounding cleanrooms, have driven significant procurement activity since the revised standards took effect in 2023. This permanent upward shift in baseline contamination control requirements creates a sustained, structurally embedded demand foundation for the cleanroom disinfectant market.

Restraints - Regulatory Complexity and Lengthy Validation Processes for New Disinfectant Products

Bringing new cleanroom disinfectant formulations to market requires extensive microbial efficacy testing, material compatibility validation, and regulatory submissions a process that typically spans 18 to 36 months and can cost several million dollars per product. In the European Union, biocidal disinfectants are regulated under Regulation (EU) No 528/2012 (Biocidal Products Regulation), and active substance approvals can take three to five years.

These regulatory timelines significantly inhibit product innovation cycles, constraining manufacturers' ability to rapidly respond to emerging microbial resistance threats or novel cleanroom contamination challenges, and creating a structural barrier to new market entrants that limits competitive dynamism.

Microbial Resistance Development Requiring Costly Rotation Programs

Repeated use of single-class disinfectants in cleanroom environments can promote microbial adaptation and reduced susceptibility, a phenomenon documented across clinical and manufacturing settings. The European Centre for Disease Prevention and Control (ECDC) has highlighted biofilm-forming microorganisms and intrinsically resistant environmental isolates as growing concerns in controlled manufacturing environments. Managing microbial resistance necessitates complex, multi-product rotation protocols, increasing procurement and training costs. For smaller pharmaceutical manufacturers and medical device companies operating on tighter margins, the financial and operational burden of maintaining validated rotation programs can constrain overall disinfectant spending growth, acting as a modest but meaningful market restraint.

Opportunities - Biotechnology Sector Expansion Creating High-Growth Demand for Specialized Disinfectants

The biotechnology industry represents the fast-growing end-user segment in the cleanroom disinfectant market, and constitutes a compelling commercial opportunity through 2033. Global biopharmaceutical R&D investment has accelerated dramatically. The PhRMA reports that U.S. biopharmaceutical companies alone invested over US$ 102 billion in R&D in 2022, driving parallel expansion in GMP-compliant manufacturing infrastructure.

Cell and gene therapy manufacturing, mRNA vaccine production, and monoclonal antibody synthesis require ISO Class 5 to Class 7 cleanroom environments with highly specialized, low-residue, materials-compatible disinfection programs. The FDA's Center for Biologics Evaluation and Research (CBER) has approved a record number of novel biologic therapies in the 2022–2024 period, each requiring dedicated cleanroom manufacturing space and ongoing contamination control programs, generating durable, high-value disinfectant procurement demand for specialized product suppliers.

Vaporized Hydrogen Peroxide (VHP) Technology Gaining Ground as Next-Generation Sporicidal Solution

Vaporized Hydrogen Peroxide (VHP) decontamination technology represents one of the most significant innovation-driven growth opportunities in the cleanroom disinfectant space. Unlike traditional liquid disinfectants, VHP systems deliver validated 6-log sporicidal efficacy as confirmed by EN 17272 and ISO 22441 international standards, penetrating complex equipment geometries and room surfaces while leaving no toxic residues, as hydrogen peroxide decomposes to water and oxygen.

The FDA has cleared multiple VHP systems for use in pharmaceutical isolators and RABS (Restricted Access Barrier System) decontamination, and adoption is accelerating in aseptic filling suites globally. Companies, including STERIS Corporation and Ecolab Inc., are actively expanding their VHP product and service portfolios. As regulatory expectations for aseptic processing validation intensify under revised Annex 1 of the EU GMP Guidelines (effective 2023), VHP solutions are positioned for accelerated adoption and premium pricing, delivering outsized revenue growth opportunities for technology-forward suppliers.

Category-wise Analysis

Product Type Insights

Oxidizing disinfectants lead the cleanroom disinfectant market by product type, accounting for approximately 56% of the total share in 2026. Within this category, hydrogen peroxide-based formulations are the dominant product, valued for their broad-spectrum efficacy against bacteria, spores, viruses, and fungi, combined with residue-free decomposition that is essential in pharmaceutical-grade cleanroom environments.

The revised EU GMP Annex 1 (2023) specifically recommends the use of sporicidal agents a requirement that strongly favors oxidizing disinfectants, particularly hydrogen peroxide and chlorine-based products, over non-oxidizing alternatives. According to ISO 13408 and ISO 14644 standards, sporicidal disinfection is mandated for Grade A/B cleanroom environments, ensuring the segment's sustained dominance as pharmaceutical and biopharmaceutical cleanroom infrastructure continues to expand globally.

End-user Insights

Pharmaceutical companies represent the dominant end-user segment in the cleanroom disinfectant market, commanding approximately 32% of global share in 2026. This leadership position is structurally anchored by the pharmaceutical industry's universal requirement for ISO-classified cleanrooms in drug manufacturing, packaging, and quality control operations, each requiring rigorous, validated disinfection programs under FDA 21 CFR Part 211, EU GMP Annex 1, and ICH Q10 guidelines.

The global pharmaceutical manufacturing sector invested over US$ 180 billion in capital expenditure between 2020 and 2024 per PhRMA data, including extensive cleanroom facility construction and upgrades. Large multinational pharmaceutical manufacturers operating multiple GMP-compliant facilities across geographies generate particularly high and recurring disinfectant procurement volumes, cementing the segment's position as the single largest revenue contributor to the cleanroom disinfectant market.

Regional Insights

North America Cleanroom Disinfectant Market Trends and Insights

North America leads the global cleanroom disinfectant market with approximately 37% of total market share in 2025, driven by the world's largest concentration of pharmaceutical and biopharmaceutical manufacturing facilities, rigorous FDA GMP enforcement, and the implementation of updated USP <797> and <800> standards mandating validated disinfectants in hospital sterile compounding cleanrooms. The region benefits from strong innovation activity and high adoption of advanced technologies such as VHP decontamination systems.

U.S. Cleanroom Disinfectant Market Size

The United States dominates North America’s share at approximately 88% of regional revenue in 2026, reflecting its unparalleled pharmaceutical manufacturing base, the world's highest density of FDA-regulated cleanroom facilities, and CDC- and ASHP-driven contamination control protocol upgrades across hospital sterile compounding operations. U.S. market demand is further amplified by the country's leadership in biopharmaceutical and cell and gene therapy manufacturing.

Europe Cleanroom Disinfectant Market Trends and Insights

Europe is the second-largest Cleanroom Disinfectant market, characterized by strict regulatory harmonization under the EMA's EU GMP guidelines, including the landmark revised Annex 1 (effective August 2023), which has triggered widespread cleanroom disinfection protocol reviews and product upgrades across the continent's extensive pharmaceutical and medical device manufacturing base. Germany, the U.K., France, and Switzerland are the region's largest national markets.

Germany Cleanroom Disinfectant Market Size

Germany holds approximately 24% of Europe cleanroom disinfectant market share, underpinned by its position as Europe's largest pharmaceutical manufacturing nation. The country hosts major global pharma manufacturers and a dense network of contract manufacturers, all operating under EU GMP Annex 1 requirements. Germany's pharmaceutical exports exceeded EUR 70 billion annually, according to Statista data, reflecting the scale of its GMP-compliant manufacturing activity.

U.K. Cleanroom Disinfectant Market Size

The United Kingdom contributes approximately 19% of European market revenue, supported by the Medicines and Healthcare products Regulatory Agency (MHRA)'s stringent GMP framework and a growing advanced therapy medicinal products (ATMPs) manufacturing sector. The U.K.'s significant biopharmaceutical cluster, particularly in the Golden Triangle of London, Oxford, and Cambridge, drives consistent specialist cleanroom disinfectant demand.

France Cleanroom Disinfectant Market Size

France is likely to account for approximately 16% share in 2026, driven by a well-established pharmaceutical sector led by companies including Sanofi and a robust network of sterile contract manufacturing organizations. ANSM (Agence nationale de sécurité du médicament) oversight ensures high GMP compliance standards, sustaining structured cleanroom disinfectant procurement across French pharmaceutical and biotechnology facilities.

Asia Pacific Cleanroom Disinfectant Market Trends and Insights

Asia Pacific is the fastest-growing regional market for cleanroom disinfectants, driven by massive pharmaceutical manufacturing capacity expansion across China, India, Japan, and South Korea. China is a particularly dominant force; the pharmaceutical industry has been undergoing systematic GMP infrastructure upgrades as manufacturers align with China National Medical Products Administration (NMPA) standards and seek international regulatory approval, generating exponential cleanroom disinfectant demand. The region's cost-competitive manufacturing environment is attracting global pharmaceutical outsourcing at record levels.

India Cleanroom Disinfectant Market Size

India holds approximately 20% of the Asia Pacific cleanroom disinfectant market share and is among the region's fast-growing markets. As the world's largest generics pharmaceutical producer with over 3,000 pharmaceutical companies, per the Pharmaceuticals Export Promotion Council of India (Pharmexcil) India's GMP-compliant manufacturing base generates substantial cleanroom disinfectant demand, further boosted by the government's Production Linked Incentive (PLI) scheme for pharmaceuticals.

Competitive Landscape

The global cleanroom disinfectant market is moderately consolidated, with global leaders Ecolab Inc., STERIS Corporation, Diversey Holdings Ltd., and 3M Company collectively commanding substantial market share through comprehensive validated disinfectant portfolios, global regulatory support capabilities, and established pharmaceutical and healthcare distribution networks.

Key competitive differentiators include regulatory validation documentation packages (compatibility testing, efficacy data, QA support), technical field service capabilities, and full-spectrum product rotation programs. Emerging competitive trends include digital inventory management integration, sustainability-focused low-VOC formulations, and VHP system bundling with service contracts. Specialized niche players, including Veltek Associates, Inc., Contec, Inc., and Decon Labs, Inc., maintain strong positions in high-purity pharmaceutical-grade product segments.

Key Developments:

- In April 2025, Ecolab expanded its Validex™ Disinfectant Efficacy Program by introducing a comprehensive data package for disinfectant wipes used in pharmaceutical cleanrooms.

- In June 2024, Ecolab introduces Disinfectant 1 Wipe, the first EPA-registered, 100% plastic-free, readily degradable disinfectant wipe that provides hospital-grade disinfection in just one minute.

Companies Covered in Cleanroom Disinfectant Market

- Ecolab Inc.

- STERIS Corporation

- 3M Company

- Diversey Holdings Ltd.

- Contec, Inc.

- Veltek Associates, Inc.

- Decon Labs, Inc.

- The Clorox Company

- Kimberly-Clark Corporation

- BASF SE

- GOJO Industries, Inc.

- Whiteley Corporation

- Reckitt Benckiser Group PLC

Frequently Asked Questions

The global cleanroom disinfectant market is expected to be valued at US$ 304.4 million in 2026.

The primary demand drivers are escalating FDA and EMA GMP enforcement requirements including the landmark revised EU GMP Annex 1 (2023) mandating sporicidal disinfection in aseptic environments, combined with the post-COVID-19 permanent elevation of contamination control standards across pharmaceutical manufacturing, hospital sterile compounding, and biotechnology facilities globally.

North America leads the global Cleanroom Disinfectant market with approximately 37% of total market share in 2025. The region's dominance is driven by the world's largest FDA-regulated pharmaceutical and biopharmaceutical manufacturing base, strict USP <797> compliance mandates for hospital cleanrooms, and active adoption of advanced VHP decontamination technologies.

The key opportunities in the cleanroom disinfectant market lie in the rapid expansion of biopharmaceutical manufacturing, especially for cell and gene therapies, vaccines, and biologics that require highly sterile environments.