- Healthcare Services

- Cleanroom Doors Market

Cleanroom Doors Market Size, Share, and Growth Forecast, 2026 - 2033

Cleanroom Doors Market by Material (Glass, Stainless Steel, Aluminum, Others), Door Type (Sliding Doors, Swing Doors, Roll-Up Doors, Others), Application (Pharmaceutical, Biotechnology, Medical Device, Electronics and Semiconductor, Food and Beverage, Others), and Regional Analysis for 2026 - 2033

Cleanroom Doors Market Share and Trends Analysis

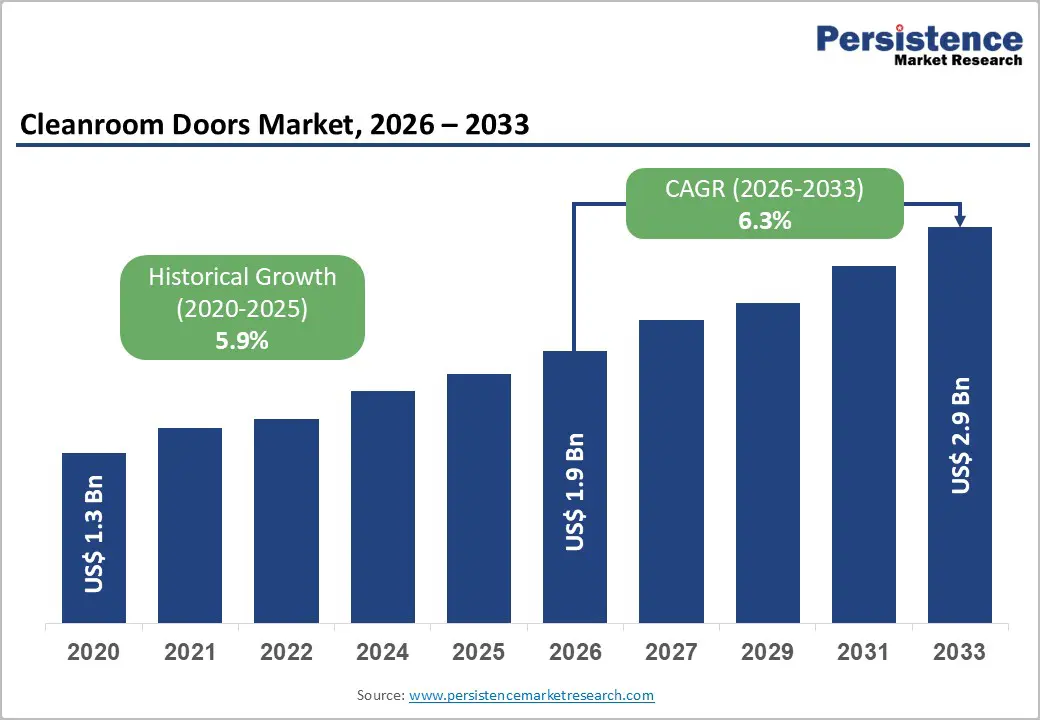

The global cleanroom doors market size is likely to be valued at US$ 1.9 billion in 2026 and is estimated to reach US$ 2.9 billion by 2033, growing at a CAGR of 6.3% during the forecast period 2026−2033, driven by increasing demand for contamination-controlled environments in pharmaceuticals, biotechnology, and semiconductor manufacturing.

Expanding biologics and sterile production, along with compliance standards set by the International Organization for Standardization and U.S. Food and Drug Administration, is boosting the adoption of advanced, airtight door systems with automation and energy-efficient features.

Key Industry Highlights:

- Leading Door Type: Sliding doors are set to command around 38% revenue share in 2026, driven by space efficiency and airflow control advantages.

- Fastest-growing Door Type: Roll-up doors are likely to expand at the fastest pace during 2026–2033 through flexibility and high-speed operation benefits.

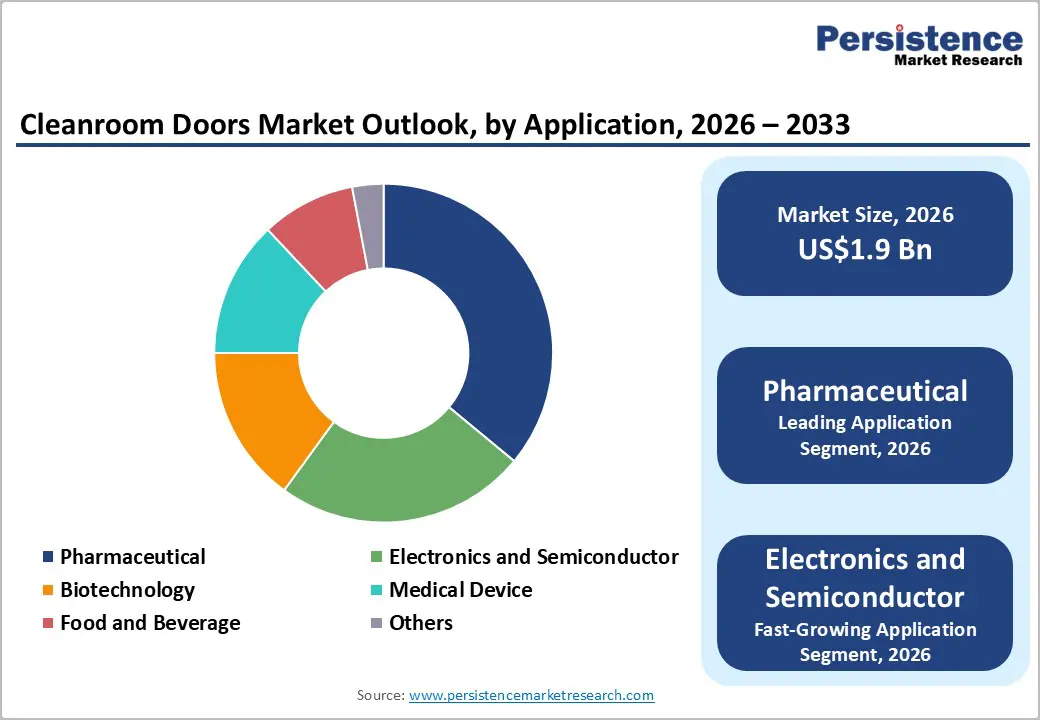

- Leading Application: Pharmaceuticals are expected to hold approximately 36% share in 2026, supported by stringent regulatory requirements and high reliance on sterile manufacturing environments.

- Fastest-growing Application: Electronics and semiconductors are projected to become the fastest-growing market due to the increasing demand for ultra-clean environments in advanced component manufacturing.

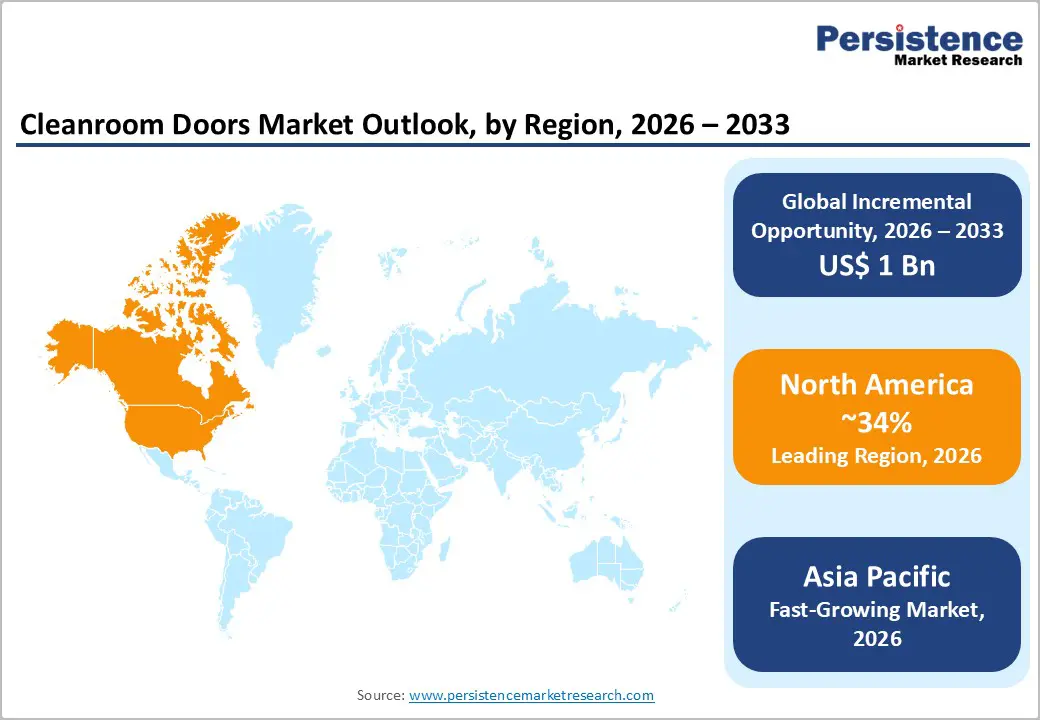

- Regional Leadership: North America is projected to lead with nearly 34% share in 2026, while Asia Pacific is projected to grow the fastest during 2026 – 2033 due to industrial expansion and infrastructure investment.

| Key Insights | Details |

|---|---|

|

Cleanroom Doors Market Size (2026E) |

US$1.9 Bn |

|

Market Value Forecast (2033F) |

US$2.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

DRO Analysis

Driver - Expansion of Pharmaceutical and Biopharmaceutical Manufacturing Infrastructure

Rising investment in pharmaceutical manufacturing is driving demand for controlled environments that meet strict regulatory standards. Cleanroom doors play a critical role in maintaining pressure differentials and minimizing particle ingress across classified zones, ensuring contamination control. Expansion in sterile injectables, biologics, and cell and gene therapies is increasing the need for modular, high-performance door systems aligned with Good Manufacturing Practice (GMP) frameworks. As facilities scale, procurement of advanced doors with airtight sealing, automation, and rapid cycling features is accelerating. The U.S. Food and Drug Administration reported 46 novel drug approvals in 2025, reflecting sustained pipeline growth and ongoing infrastructure expansion.

Large biologics manufacturing sites require strict environmental segregation to ensure process integrity and prevent cross-contamination. Cleanroom doors support efficient personnel and material movement in high-throughput settings. In emerging markets, manufacturing expansion is strengthening demand for advanced cleanroom systems. India’s pharmaceutical exports, reported at US$30.47 billion in FY 2024–25, highlight strong production momentum, further supporting the adoption of automated, compliant cleanroom solutions.

Semiconductor Industry Expansion and Advanced Electronics Miniaturization

Rapid expansion of semiconductor fabrication facilities is increasing the need for contamination-controlled environments, driving demand for advanced cleanroom door systems. Sub-5-nanometer nodes require extreme precision, where even microscopic particles can impact yield and raise costs. Cleanroom doors help maintain airflow stability, pressure differentials, and efficient material transfer within fabrication zones. According to the U.S. Census Bureau, semiconductor manufacturing shipments exceeded $200 billion in 2025, reflecting strong investment in fabrication infrastructure. Growing fab construction across Asia and North America supports sustained demand for high-performance, standardized access systems.

Ongoing miniaturization in electronics, medical devices, and automotive components further increases sensitivity to airborne contamination. Higher component density and tighter tolerances require stringent cleanroom standards, boosting demand for doors with superior sealing, durability, and automation compatibility. High-speed, sensor-integrated doors enable efficient, repeatable access while maintaining sterility, supporting throughput, and defect reduction across advanced manufacturing environments.

Restraint - Complex Validation and Regulatory Certification Processes

Stringent validation protocols and regulatory certification requirements create extended product approval cycles within the cleanroom doors market. Manufacturers face multiple stages of performance testing, documentation review, and compliance verification aligned with standards set by agencies such as the FDA and International Organization for Standardization (ISO). Each iteration demands engineering adjustments, increasing development costs, and delaying commercialization timelines. Capital allocation shifts toward compliance management rather than production scale expansion. Smaller firms encounter entry barriers due to limited technical resources and certification expertise. Procurement decisions slow across end users, as buyers prioritize fully validated systems, reducing immediate demand visibility and limiting rapid revenue realization across supply chains.

Regulatory divergence across regions introduces further complexity, requiring separate certification pathways for different geographic markets. Documentation standards, material traceability expectations, and audit procedures vary, increasing administrative burden and compliance risk exposure. Project timelines extend as firms coordinate with third-party inspectors and accreditation bodies, affecting installation schedules for pharmaceutical and semiconductor facilities. Delayed project completion constrains downstream equipment integration and facility commissioning. Pricing pressure emerges as compliance costs pass through to customers, influencing budget allocation decisions. End users may defer upgrades or expansion projects, moderating order volumes and reducing consistent demand flow for specialized door systems.

Opportunity - Rising Demand for Energy-efficient and Low-maintenance Systems

Growing preference for energy-efficient and low-maintenance infrastructure creates a strong opportunity for the cleanroom doors market. Industrial operators face rising utility costs and stricter environmental compliance targets, pushing the adoption of insulated, airtight door systems that reduce air leakage and pressure loss. Improved sealing performance lowers Heating, Ventilation, and Air Conditioning (HVAC) load and supports stable contamination control, which directly reduces operating expenditure. Data from the U.S. Department of Energy in 2025 indicates that buildings account for 40% of total energy consumption, reinforcing the urgency for efficiency upgrades. Manufacturers respond with advanced materials, automation, and smart monitoring features that optimize lifecycle performance and minimize manual intervention.

End-user industries such as pharmaceuticals, biotechnology, and electronics prioritize operational continuity and contamination control, driving demand for durable systems with minimal servicing requirements. Reduced maintenance frequency limits production downtime and labor costs, supporting higher throughput and predictable output quality. Integration of automated sliding and hermetic mechanisms enhances reliability under high-cycle conditions while lowering wear-related failures. Energy-efficient configurations align with sustainability mandates and carbon reduction goals set by regulatory bodies and corporate strategies. This alignment expands procurement budgets toward upgraded infrastructure, enabling suppliers to capture value through premium, performance-driven solutions across facility construction and retrofit projects.

Growing Adoption of Modular Cleanroom Facilities

Modular cleanroom facilities enable rapid deployment, flexible scaling, and reduced capital intensity, which directly elevates demand for specialized door systems engineered for controlled environments. Prefabricated panel structures rely on standardized interfaces, creating consistent specifications for airtight, contamination-resistant access points. This standardization accelerates procurement cycles and shortens installation timelines, increasing unit volumes across pharmaceutical, biotechnology, and electronics production sites. Rising investment in controlled manufacturing environments drives frequent project initiation, reinforcing sustained demand for precision-engineered door assemblies designed for seamless compatibility with modular construction frameworks and evolving production requirements across global industrial operations.

Design flexibility within modular environments encourages reconfiguration of layouts to support changing production batches and regulatory protocols, driving replacement and upgrade cycles for door components. Cleanroom doors integrated with automation, interlocking mechanisms, and sensor-based controls align with modular design principles, enabling seamless expansion or relocation without major structural disruption. Cost efficiency achieved through off-site fabrication reduces project risk and attracts small and mid-scale manufacturers into controlled production segments. This broader participation enlarges the customer base and diversifies application areas, strengthening long-term revenue streams for door suppliers focused on standardized, scalable, and compliance-ready access solutions across manufacturing ecosystems and supply networks.

Category-wise Analysis

Door Type Insights

Sliding doors are poised to dominate with a forecasted market share of over 38% in 2026, powered by efficient space utilization and seamless operation in controlled environments. These systems enable smooth, non-intrusive movement that preserves airflow integrity and contamination control. Strong adoption across pharmaceutical and healthcare facilities reinforces reliability perception. Industrial design trends favor automation and reduced manual contact. Standardized product availability supports global distribution. Examples include installation in sterile drug manufacturing units where consistent pressure maintenance remains essential for regulatory compliance.

Roll-up doors are estimated to be the fastest-growing segment, fueled by demand for flexible and high-speed access solutions in industrial cleanroom environments. These systems enable rapid cycles that limit exposure and sustain airflow control. Industrial users value efficiency and adaptability across varied applications. Manufacturing sectors favor solutions that enhance throughput and workflow continuity. Supply networks and direct procurement improve accessibility. Examples include use in pharmaceutical logistics zones where quick material transfer supports contamination control and operational speed.

Application Insights

Pharmaceuticals are likely to be the leading segment with a projected 36% of the cleanroom doors market share in 2026 due to strict regulatory requirements and high demand for sterile manufacturing environments. Production depends on contamination-free processes ensuring safety and efficacy. Industry referrals sustain infrastructure adoption, including specialized door systems. Digital manufacturing supports automated door integration for compliance and efficiency. Facility expansion across regions improves accessibility. Standardized cleanroom designs enable scalable deployment and cost efficiency. Examples include sterile injectable manufacturing plants where controlled access systems maintain pressure differentials and regulatory alignment.

Electronics and semiconductors are anticipated to be the fastest-growing segment, fueled by increasing demand for ultra-clean environments required for advanced component manufacturing. Precision-driven production links contamination control with yield performance. Industry networks support the adoption of high-performance cleanroom infrastructure. Smart manufacturing integrates door systems into automated workflows. Global semiconductor investments and localized supply chains expand accessibility. Process optimization improves cost efficiency at scale. Examples include wafer fabrication facilities where automated doors regulate particle levels and support consistent microchip production quality.

Regional Insights

North America Cleanroom Doors Market Trends

North America is expected to lead with an estimated 34% of the cleanroom doors market share in 2026, supported by a dense network of high-value pharmaceutical, biologics, and semiconductor manufacturing facilities across the United States, Canada, and Mexico. Regulatory enforcement from the FDA drives stringent contamination control standards, increasing reliance on advanced door systems with airtight sealing and automation capabilities. Capital intensity within manufacturing infrastructure enables faster adoption of premium technologies. High labor costs accelerate the transition toward automated and touchless access solutions. Strong presence of contract manufacturing organizations strengthens recurring demand. Established validation protocols and certification requirements create consistent replacement cycles across controlled production environments.

Sustained dominance is reinforced by early adoption of Industry 4.0 practices across the United States and Canada, where cleanroom door systems integrate with building management and environmental monitoring platforms. Investment in advanced therapies, including cell and gene production, drives demand for modular cleanroom expansion requiring high-performance access systems. Procurement strategies favor lifecycle efficiency, encouraging adoption of energy-optimized and low-maintenance door designs. Supply chain maturity supports rapid customization and deployment across Mexico's manufacturing clusters. Aerospace and defense manufacturing further contributes through precision-controlled environments, sustaining infrastructure upgrades, and continuous demand for technologically advanced cleanroom access solutions.

Europe Cleanroom Doors Market Trends

Europe demonstrates strong demand for cleanroom door systems driven by advanced pharmaceutical production, medical device engineering, and precision manufacturing activity across Germany, France, and Italy. European Union Good Manufacturing Practice (EU GMP) regulatory frameworks enforce strict contamination control, encouraging the adoption of airtight, automated door solutions. Energy efficiency mandates influence product design, increasing preference for insulated and low-leakage systems. Retrofit projects within established facilities generate steady replacement demand. Aerospace and automotive electronics sectors contribute through controlled assembly environments that require stable pressure conditions and minimal particle intrusion.

Europe maintains innovation-driven growth supported by biotechnology research and high-value manufacturing ecosystems across Switzerland, the Netherlands, and Sweden. Investment in life sciences infrastructure drives modular cleanroom expansion, increasing the need for flexible and high-performance door systems. Sustainability targets influence procurement decisions, promoting recyclable materials and energy-optimized designs. Automation adoption enables integration with digital monitoring platforms, enhancing operational control. Supply chain localization strategies strengthen domestic production capabilities, supporting continuous infrastructure upgrades and consistent demand for specialized cleanroom access technologies.

Asia Pacific Cleanroom Doors Market Trends

Asia Pacific is forecast to be the fastest-growing market for the cleanroom doors market between 2026 and 2033, stimulated by the rapid expansion of pharmaceutical production, semiconductor fabrication, and biotechnology research infrastructure. China and India drive large-scale capacity additions supported by industrial policy incentives and cost-efficient manufacturing ecosystems. Increasing export orientation for high-value drugs and electronics elevates demand for contamination-controlled environments. Investment in greenfield facilities accelerates the installation of modern cleanroom access systems. Rising adoption of modular construction techniques supports faster deployment. Skilled labor availability and competitive operating costs strengthen manufacturing attractiveness, encouraging global producers to expand controlled environment infrastructure.

Japan and South Korea contribute through advanced semiconductor and precision manufacturing ecosystems that demand ultra-clean operational conditions. High focus on yield optimization drives integration of automated and high-speed door systems within production workflows. Localization strategies across electronics and healthcare supply chains increase infrastructure investments. Expansion of contract manufacturing and research services supports recurring demand for cleanroom upgrades. Digital manufacturing adoption enables synchronization of door operations with environmental monitoring systems. Infrastructure development across emerging industrial hubs improves accessibility, strengthening procurement of specialized door solutions aligned with strict contamination control requirements.

Competitive Landscape

The cleanroom doors market reflects a moderately fragmented structure, with global engineering firms and specialized providers competing across pharmaceutical and semiconductor applications. ASSA ABLOY, Dormakaba Group, and NABCO Entrances maintain strong positioning through technological expertise, automation capabilities, and long-term industrial contracts. Competitive differentiation centers on product customization, airtight performance, and compliance with strict contamination control standards, supporting sustained demand in high-value manufacturing environments.

Gilgen Door Systems, Record Group, and Horton Automatics compete through specialized solutions tailored to healthcare and cleanroom infrastructure. Regional manufacturers emphasize cost efficiency and localized service responsiveness. Global participants invest in advanced materials, digital integration, and turnkey project execution. Market dynamics reflect continuous innovation, where performance reliability and system compatibility influence procurement decisions across expanding controlled environment applications.

Key Industry Developments:

- In February 2026, ASSA ABLOY Entrance Systems unveiled the next-generation RT1000 spiral high-speed door, enhancing cleanroom door performance through improved energy efficiency, rapid operation, and advanced sealing capabilities for controlled industrial environments.

- In September 2025, GCS launched an advanced automated cleanroom panel manufacturing line in the United States, significantly expanding integrated production capacity for cleanroom doors and accelerating high-performance modular infrastructure deployment across pharmaceutical and semiconductor facilities.

Companies Covered in Cleanroom Doors Market

- ASSA ABLOY

- Dormakaba Group

- NABCO Entrances

- Gilgen Door Systems

- Record Group

- Horton Automatics

- Stanley Access Technologies

- Manusa

- KADRA

- Metaflex Doors

- HPL Cleanroom Furniture

- Clean Air Products

- Terra Universal

Frequently Asked Questions

The cleanroom doors market is projected to reach US$ 1.9 billion in 2026.

Rising demand for contamination-controlled environments in pharmaceutical, biotechnology, and semiconductor manufacturing drives the adoption of advanced cleanroom door systems.

The cleanroom doors market is poised to witness a CAGR of 6.3% from 2026 to 2033.

Expansion of biologics manufacturing, semiconductor fabrication investments, and adoption of automated, energy-efficient cleanroom door systems create strong market opportunities.

Some of the key market players include ASSA ABLOY, Dormakaba Group, NABCO Entrances, Gilgen Door Systems, Record Group, and Horton Automatics.