- Renewable Energy

- Canada Solar Photovoltaic System Market

Canada Solar Photovoltaic System Market Size, Share, and Growth Forecast 2026 - 2033

Canada Solar Photovoltaic System Market by Product Type (Off-Grid Systems, Grid-Connected Systems), Technology (Monocrystalline, Polycrystalline, Thin-Film), Installation (Building-Applied Photovoltaics (BAPV), Building-Integrated Photovoltaics (BIPV)), End-user (Residential, Commercial, Utility, Industrial, Agricultural, Misc.), and Regional Analysis for 2026 - 2033

Canada Solar Photovoltaic System Market Size and Trend Analysis

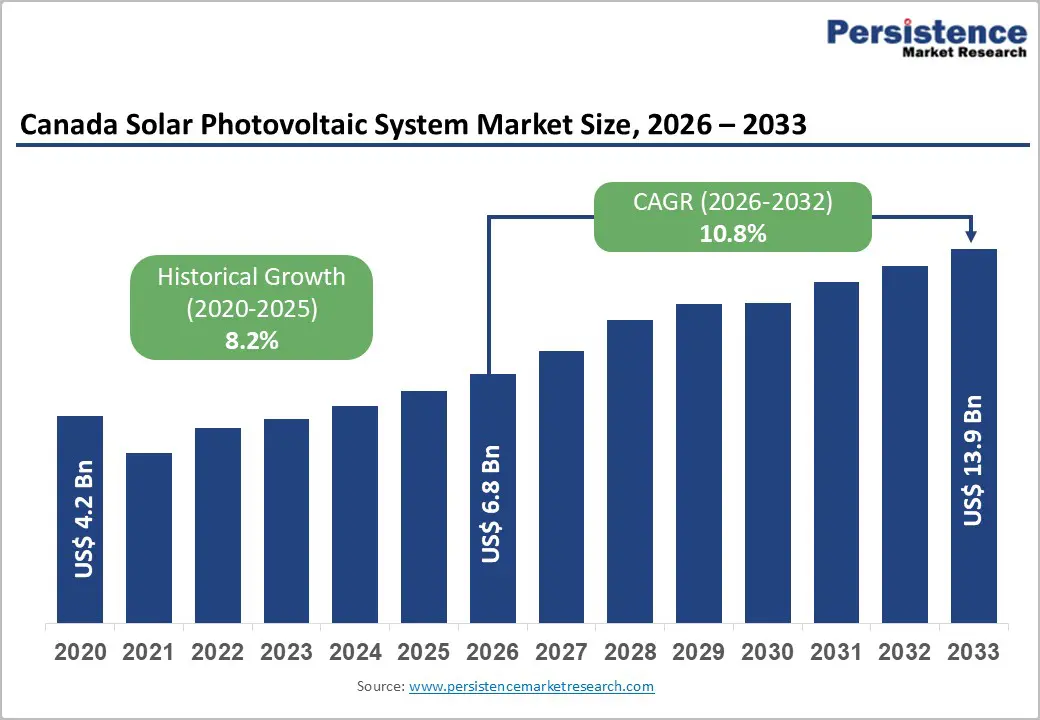

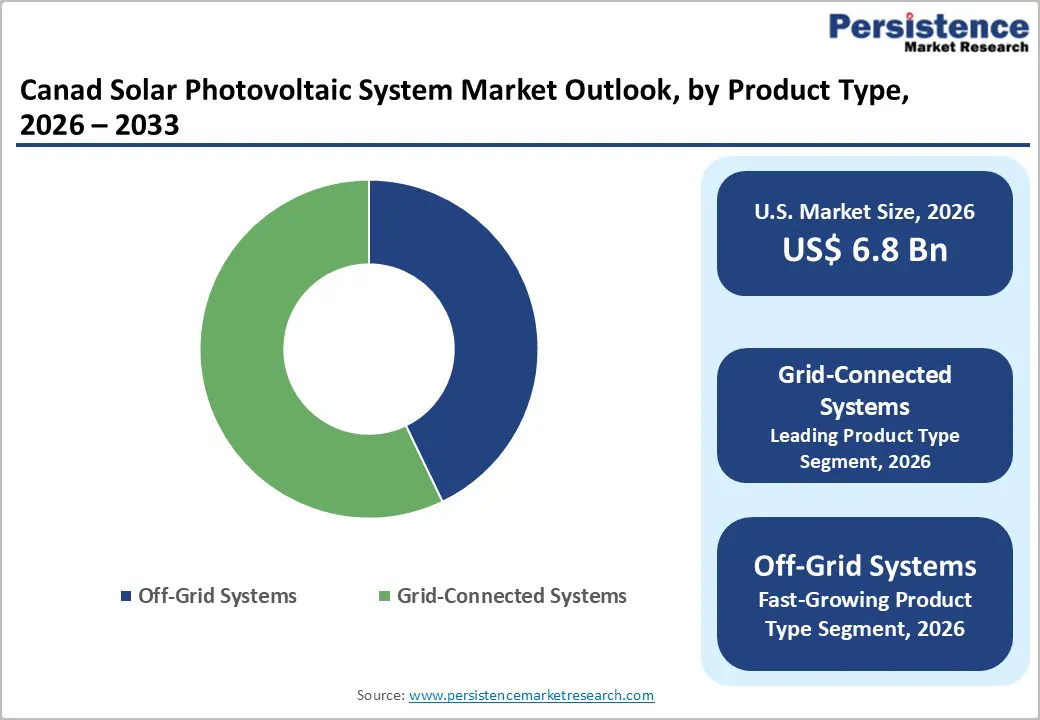

The Canada Solar Photovoltaic System market size is estimated to be valued at US$ 6.8 billion in 2026 and is projected to reach US$ 13.9 billion by 2033, growing at a CAGR of 10.8% between 2026 and 2033.

The market's sustained growth is fundamentally driven by Canada's binding national commitment to achieve a net-zero electricity grid by 2050, supported by the Government of Canada's Clean Electricity Regulations (CER) finalized in December 2024, which mandate progressive carbon intensity reduction limits on electricity generation. This policy clarity is compelling large-scale utility developers and distributed energy investors to accelerate solar PV deployment across provinces such as Alberta, Ontario, and Saskatchewan, where solar irradiance potential is highest.

Key Market Highlights

- Dominated Product Type: Grid-Connected Systems dominate the Product Type segment with approximately 72% market share, underpinned by net metering programs across all major Canadian provinces and utility procurement mandates driving large-scale ground-mount project development.

- Fastest Growing Installation: BIPV (Building-Integrated Photovoltaics) is the fastest-growing Installation segment, propelled by net-zero building codes, Toronto's Green Standard solar mandate, and growing architect and developer preference for energy-generating building envelope solutions.

- Growth Indicator: Canada's Clean Electricity Regulations (CER) finalized in December 2024 under the Canadian Environmental Protection Act, 1999 (CEPA) are the market's most powerful demand catalyst, mandating near-zero emissions electricity generation by 2035 and unlocking large-scale utility solar investment commitments nationwide.

- Restraint: Grid integration complexity and high soft costs remain the market's most significant restraint, with balance-of-system and permitting expenses representing up to 30–40% of total installation costs per the Canada Energy Regulator, slowing distributed solar adoption particularly among small commercial and residential project developers.

- Opportunity: Agrivoltaics represents the key emerging market opportunity, with Canada's 64 billion hectares of farmland offering enormous dual-use potential for solar energy generation alongside crop production under provincial zoning pilot programs in Alberta and Saskatchewan.

| Key Insights | Details |

|---|---|

|

Canada Solar Photovoltaic System Market Size (2026E) |

US$ 6.8 Billion |

|

Market Value Forecast (2033F) |

US$ 13.9 Billion |

|

Projected Growth CAGR (2026–2033) |

10.8% |

|

Historical Market Growth (2020–2025) |

8.2% |

Market Dynamics

Drivers - Canada's Clean Electricity Regulations Catalyzing Accelerated Solar PV Deployment

The finalization of Canada's Clean Electricity Regulations (CER) in December 2024, published in the Canada Gazette, Part II, represents one of the most consequential policy milestones for the domestic solar PV industry. The CER establishes annual carbon dioxide emission intensity limits for electricity generation units across the country, effectively creating a structural mandate for utilities to transition away from fossil-fuel-based generation toward clean sources, with solar PV emerging as a cost-competitive and rapidly deployable alternative. Under the Canadian Environmental Protection Act, 1999 (CEPA), the regulations require electricity producers to achieve near-zero emissions by 2035, with compliance pathways including offset credits and staggered timelines to provide operational flexibility.

The Government of Canada's accompanying Powering Canada's Future strategy reinforces this directive, channeling federal investment into grid modernization, transmission infrastructure, and provincial renewable capacity expansion. These combined regulatory and financial signals are directly accelerating utility-scale and commercial solar PV project commissioning nationwide, creating a highly favorable demand environment for the Canada Solar Power Growth Outlook through the forecast period.

Declining Module Costs and Rising Energy Demand Amplifying Investment Attractiveness

The dramatic and sustained decline in solar photovoltaic module prices over the past decade has fundamentally transformed the economic calculus of solar energy investments in Canada. IRENA has documented a roughly 90% reduction in the global cost of solar PV since 2010, and this cost deflation has translated directly into sharply improved project economics for Canadian developers and commercial buyers. Concurrently, Electricity Canada projects that national electricity demand will grow by 50% to 75% by 2050 driven by electrification of transportation, industrial processes, and heating systems, a demand expansion that will require substantial additions of new generation capacity, for which solar PV is ideally positioned.

Provincial renewable energy auctions, including Alberta's Renewable Electricity Program (REP) and Ontario's Competitive Process administered by the Independent Electricity System Operator (IESO), are generating predictable, long-term revenue visibility for solar project developers, lowering financing costs and accelerating project execution timelines across the country.

Restraints - Grid Integration Challenges and Intermittency of Solar Generation

Solar photovoltaic generation's inherent intermittency poses a substantial integration challenge for Canada's existing transmission and distribution infrastructure. Because solar output is contingent on daylight hours and weather conditions, particularly limiting in Northern provinces during winter months, grid operators must invest heavily in flexible backup generation, energy storage, and demand-response systems to maintain reliability. Natural Resources Canada has acknowledged in its Canada's Energy Future 2023 report that grid modernization requirements present both technical and financial complexities for system operators.

High curtailment rates observed during peak generation periods in Ontario and British Columbia further diminish the economic returns for some solar developers, discouraging investment in specific provincial markets where grid absorption capacity has not kept pace with renewable capacity additions.

High Upfront Capital Costs and Permitting Complexity

Despite substantial declines in module prices, the total installed cost of solar PV systems in Canada remains elevated when accounting for balance-of-system components, labor, permitting, and grid interconnection costs. According to the Canada Energy Regulator (CER), soft costs, including municipal building permits, engineering assessments, and utility interconnection studies, can represent up to 30–40% of total residential and commercial system installation costs.

The absence of a harmonized national permitting framework means that solar developers must navigate varying and sometimes cumbersome municipal and provincial regulatory requirements, extending project timelines and increasing transaction costs. These barriers disproportionately affect smaller commercial and residential project developers who lack the scale to amortize administrative overhead efficiently, thereby constraining the pace of distributed solar PV adoption in mid-sized cities.

Opportunities - Building-Integrated Photovoltaics (BIPV) as a High-Value Growth Frontier

The Building-Integrated Photovoltaics (BIPV) segment presents one of the most promising and high-margin growth opportunities for solar PV companies operating in Canada's construction and real estate sectors. Unlike conventional rooftop solar systems, BIPV solutions are architecturally embedded into building envelopes, including facades, skylights, curtain walls, and roofing membranes, delivering simultaneous energy generation and structural function. The City of Toronto's Green Standard initiative mandates new commercial and residential buildings to incorporate solar panels, creating a direct and growing demand pipeline for integrated photovoltaic solutions aligned with sustainable construction trends.

The global Building & Construction Sealants Market is itself evolving to accommodate solar-integrated building materials, with high-performance sealants and weatherproofing compounds now required to ensure long-term waterproofing integrity in BIPV installations. Canada's National Building Code (NBC) is progressively incorporating net-zero energy building requirements, compelling architects and developers to specify BIPV solutions for compliance. Companies that can deliver certified, aesthetically coherent, and structurally compliant BIPV product lines, combined with digital design simulation tools, are positioned to capture premium margin opportunities across Canada's rapidly growing green commercial construction pipeline.

Agricultural Solar (Agrivoltaics) Unlocking Underutilized Land for Dual-Use Energy Generation

Agrivoltaics, the co-location of solar PV systems on agricultural land to enable simultaneous crop production and renewable energy generation, is emerging as a high-potential and underexplored growth frontier for the Canadian solar PV market. Agriculture and Agri-Food Canada manages approximately 64 billion hectares of farmland across the country, a vast land resource that remains largely untapped for energy generation under conventional agricultural land-use restrictions. Emerging provincial policy experiments in Alberta and Saskatchewan are beginning to explore agrivoltaic zoning frameworks, encouraged by evidence from European and Japanese pilot programs demonstrating that shade-tolerant crops such as berries, root vegetables, and leafy greens can achieve comparable yields under bifacial solar arrays while providing simultaneous shading benefits that reduce water requirements.

The Canadian Agri-Food Policy Institute has identified dual-use land models as a critical tool for achieving both food security and clean energy targets simultaneously. Solar PV manufacturers capable of delivering low-profile, high-efficiency bifacial panel systems optimized for agrivoltaic configurations are strategically positioned to capture first-mover advantages in this nascent but rapidly maturing segment.

Category-wise Analysis

Product Type Insights

Grid-Connected Systems dominate the Canada Solar Photovoltaic System market by product type, accounting for approximately 72% of total market share in 2026. This leadership position is anchored in the superior economic viability and regulatory support infrastructure that grid-connected solar PV installations enjoy in Canada relative to off-grid alternatives. Net metering programs, now operational in all major provinces including Ontario, Alberta, British Columbia, and Quebec, enable residential and commercial system owners to export surplus solar electricity to the grid at regulated tariff rates, creating a financial incentive that substantially improves investment payback periods and accelerates system adoption.

Grid-connected utility-scale solar farms in Alberta and Saskatchewan have attracted billions in private capital investment, supported by Alberta Electric System Operator (AESO) renewable procurement rounds. The IESO in Ontario has further reinforced the grid-connected pipeline through its Competitive Process for Procurement of Renewable and Storage Resources, directly stimulating demand for grid-tied solar PV infrastructure across Canada's most densely populated provinces.

Technology Insights

Monocrystalline solar panels represent the leading technology segment in the Canada Solar Photovoltaic System market, commanding approximately 68% of total technology segment share in 2026. Monocrystalline panels' dominance is attributable to their superior energy conversion efficiency, typically ranging from 20% to 24%, their proven long-term reliability with manufacturer warranties frequently covering 25 to 30 years, and their superior performance in low-light and cold-weather conditions, which are critical performance requirements in Canadian climates characterized by significant seasonal variation.

IRENA's technology assessment reports confirm monocrystalline as the industry's preferred module type for both utility-scale ground-mount and commercial rooftop installations due to its highest power output per unit area. Advances in PERC (Passivated Emitter and Rear Cell) and TOPCon (Tunnel Oxide Passivated Contact) monocrystalline cell architectures have further widened the efficiency gap over polycrystalline alternatives, reinforcing monocrystalline's dominant position as the specification of choice among engineering consultants and large-scale solar project developers across Canada.

Installation Insights

Building-Applied Photovoltaics (BAPV), conventional rooftop and surface-mounted solar panel systems, represents the leading installation segment, accounting for approximately 78% of total installation segment revenue in 2026. BAPV systems benefit from a well-established installation ecosystem, a broad base of certified rooftop solar installers, compatibility with existing building structures, and significantly lower per-watt installation costs compared to BIPV alternatives. SkyFire Energy and Grasshopper Solar Corporation are among the Canadian installers driving large-scale commercial BAPV deployment across Alberta and Ontario respectively.

The proliferation of municipal green building requirements, including Toronto's Green Standard, which mandates solar readiness provisions for new buildings, has institutionalized BAPV as the default solar specification for commercial developers. BIPV is the fastest-growing installation sub-segment, driven by increasing net-zero building mandates and architecture-forward design preferences among premium commercial developers, positioning it as the high-growth frontier for the forecast period.

End-user Insights

The Utility segment leads the Canada Solar Photovoltaic System market by end use, capturing approximately 45% of total end-use segment share in 2026. Utility-scale solar projects, defined as ground-mounted installations typically exceeding 1 MW in generation capacity, have attracted the largest share of total solar investment in Canada due to their scale economics, predictable long-term revenue under power purchase agreements, and alignment with provincial clean energy procurement mandates.

Alberta's Renewable Electricity Program (REP) has contracted several utility-scale solar projects exceeding 400 MW in aggregate capacity, while SaskPower's renewable energy target of 50% renewable generation by 2030 has directly accelerated utility-scale solar development in Saskatchewan. Major project developers including Northland Power Inc. and Amp Solar Group Inc. have assembled substantial utility solar pipelines, supported by Infrastructure Canada's Strategic Innovation Fund and Export Development Canada's clean energy financing programs, collectively reinforcing the utility segment's dominant and growing position.

Competitive Landscape

The Canada Solar Photovoltaic System market exhibits a moderately fragmented competitive structure, with a blend of large multinational developers, such as Canadian Solar Inc., First Solar, Inc., and Northland Power Inc., and a robust tier of mid-scale regional project developers and equipment specialists. Market leaders differentiate through vertically integrated capabilities spanning module manufacturing, project development, engineering procurement and construction (EPC), and long-term operations. First Solar leverages its proprietary CadTel thin-film technology as a sustainability-differentiated offering with lower lifecycle carbon intensity.

Emerging business model trends include power-as-a-service (PaaS) and community solar subscription models. UGE International Ltd. and Amp Solar Group Inc. are expanding through commercial and industrial rooftop programs, targeting mid-market clients with turnkey solar solutions and long-term energy cost guarantees.

Key Developments:

- In April 2025, Canadian Solar Inc. announced a partnership with Flow Power in Australia to deliver the first solar project featuring its proprietary anti-hail module technology, marking a significant milestone in the company's international technology commercialization strategy.

- In March 2025, Canadian Solar Inc. signed Battery Supply Agreements and Long-Term Service Agreements (LTSAs) for two major energy storage projects, reflecting accelerated integration of solar-plus-storage solutions within its global project development pipeline.

- In December 2024, The Government of Canada finalized the Clean Electricity Regulations (CER) under the Canadian Environmental Protection Act, 1999 (CEPA), establishing a clear net-zero electricity mandate for 2035 and catalyzing accelerated solar PV investment commitments across provincial utility sectors.

Companies Covered in Canada Solar Photovoltaic System Market

- Northland Power Inc.

- Canadian Solar Inc.

- Solvest

- Silfab Solar Inc.

- SkyFire Energy

- Polar Racking

- Heliene Inc.

- Morgan Solar, Inc.

- Renewable Power Partners

- UGE International Ltd.

- Amp Solar Group Inc.

- Grasshopper Solar Corporation

- First Solar, Inc.

- SunPower Corporation

- Vivint Solar, Inc.

Frequently Asked Questions

The Canada Solar Photovoltaic System market is estimated to be valued at US$ 6.8 billion in 2026 and is projected to reach US$ 13.9 billion by 2033, registering a CAGR of 10.8% over the forecast period. The market recorded a historical growth rate of 8.2% CAGR between 2020 and 2025.

The market's primary growth drivers are the Government of Canada's Clean Electricity Regulations (CER), finalized in December 2024, which mandate near-zero emissions electricity generation by 2035, and the continued decline in solar PV module costs, down approximately 90% over the past decade per IRENA, which significantly improves the return on investment for residential, commercial, and utility solar projects.

The Monocrystalline technology segment leads the market with approximately 68% revenue share in 2026. Monocrystalline panels offer superior energy conversion efficiency of 20% to 24%, long-term reliability backed by 25–30 year manufacturer warranties, and excellent performance in cold-climate and low-light conditions, making them the specification of choice for Canadian utility and commercial solar projects.

The most significant growth opportunity lies in Building-Integrated Photovoltaics (BIPV) and agrivoltaics. Municipal mandates such as Toronto's Green Standard, the EU's Energy Performance of Buildings Directive (EPBD) requiring solar on new buildings by 2026–2030, and Canada's vast agricultural land base of 64 billion hectares offer transformative dual-use solar deployment opportunities for innovative PV manufacturers and project developers.

The leading companies include Canadian Solar Inc., First Solar, Inc., Northland Power Inc., Silfab Solar Inc., Heliene Inc., SkyFire Energy, UGE International Ltd., Amp Solar Group Inc., SunPower Corporation, Vivint Solar, Inc., and Boralex Inc., among other prominent solar PV developers, manufacturers, and installers operating across Canada's utility, commercial, and residential solar segments.