- Technology

- Broadcast Scheduling Software Market

Broadcast Scheduling Software Market Size, Share, and Growth Forecast 2026 - 2033

Broadcast Scheduling Software Market by Offering (Software/Platform, Services), by Deployment (On-premises, Cloud-based, Hybrid), Application (Television & Entertainment Broadcasting, Radio Broadcasting, Cable & Satellite Networks, OTT & Streaming Platforms, Sports Broadcasting, Others), and Regional Analysis, 2026 - 2033

Broadcast Scheduling Software Market Size and Trend Analysis

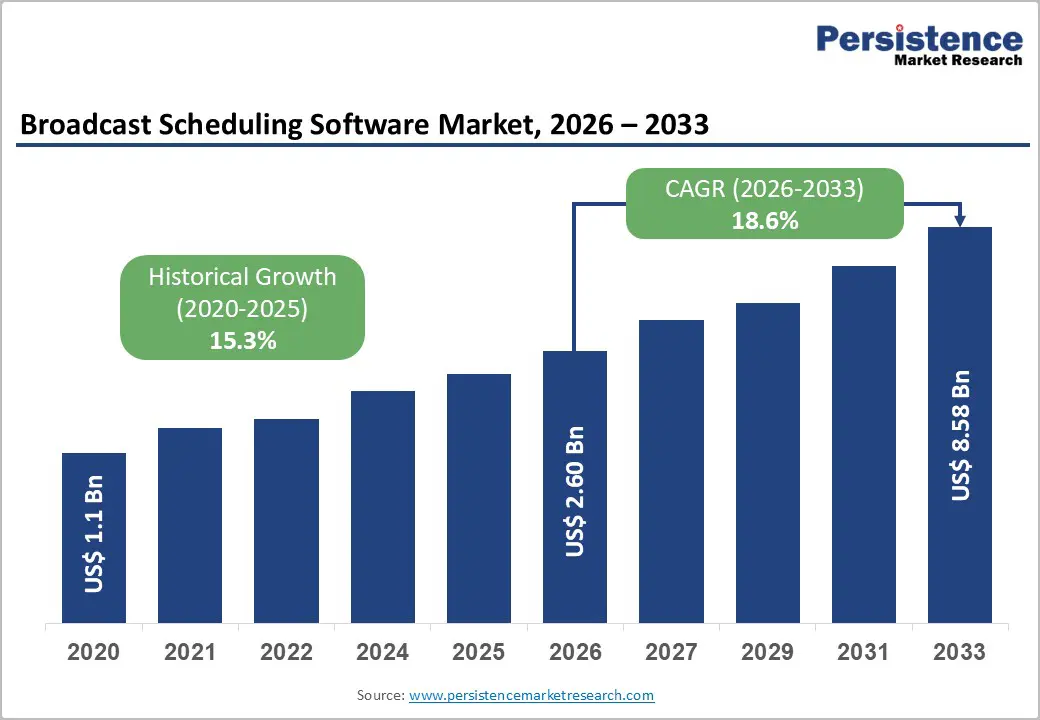

The global broadcast scheduling software market is expected to be valued at US$ 2.60 billion in 2026. It is projected to reach US$ 8.58 billion, growing at a CAGR of 18.6% between 2026 and 2033, as broadcasters are required to modernize legacy systems to support cloud-based, multi-platform content delivery.

Industry-wide standardization efforts, such as the European Broadcasting Union’s cloud-native Media Service Platform specification, are driving organizations to adopt interoperable, scalable scheduling solutions. The FCC’s ATSC 3.0 rollout is compelling broadcasters to manage hybrid linear and digital broadcast workflows efficiently. These shifts create operational pressure to handle more complex content distribution, dynamic scheduling, and IP-based transmission.

Key Industry Highlights:

- Leading Offering: Software/Platform is projected to dominate with over 65% share in 2026, valued at approximately US$ 1.69 billion, driven by demand for centralized scheduling engines, playout automation, and EPG management systems enabling unified control across linear and digital ecosystems.

- Leading Deployment: On-premises deployment is anticipated at over 37% share in 2026, driven by requirements for high reliability, secure environments, and deep integration with legacy broadcast infrastructure.

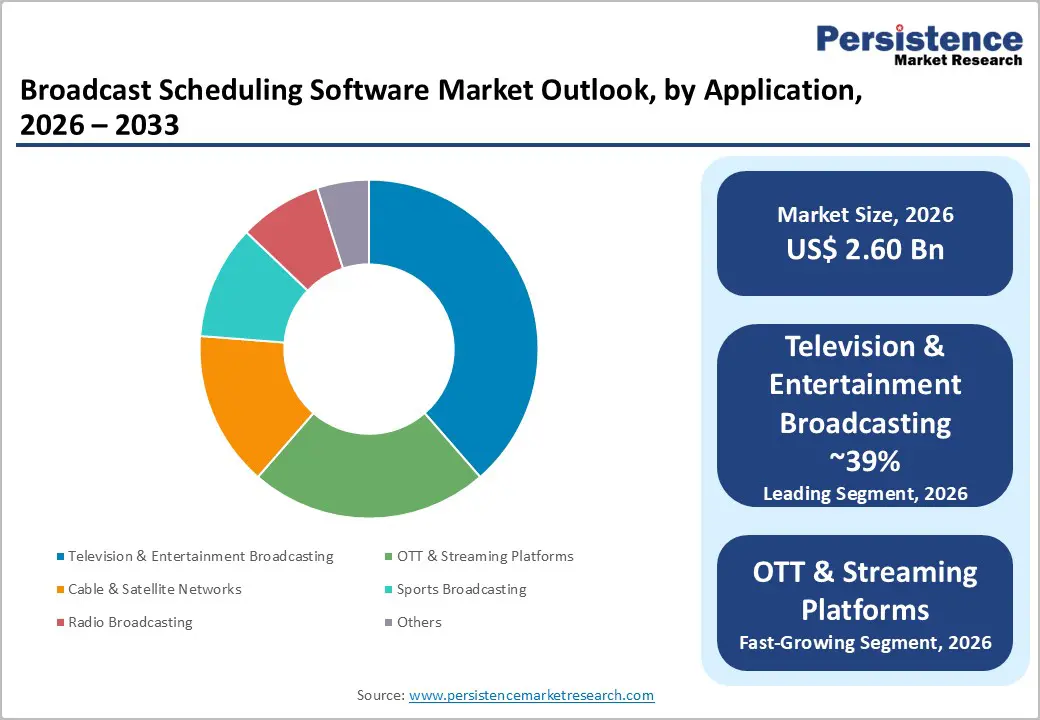

- Leading Application: Television & entertainment broadcasting leads with over 39% share in 2026, valued at more than US$ 1,014.74 Million, driven by complex programming structures, advertising coordination, and compliance-heavy scheduling requirements.

- Fast-Growing Application: OTT & streaming platforms are the fast-growing applications, fueled by FAST channels, continuous streaming models, and automated real-time scheduling systems.

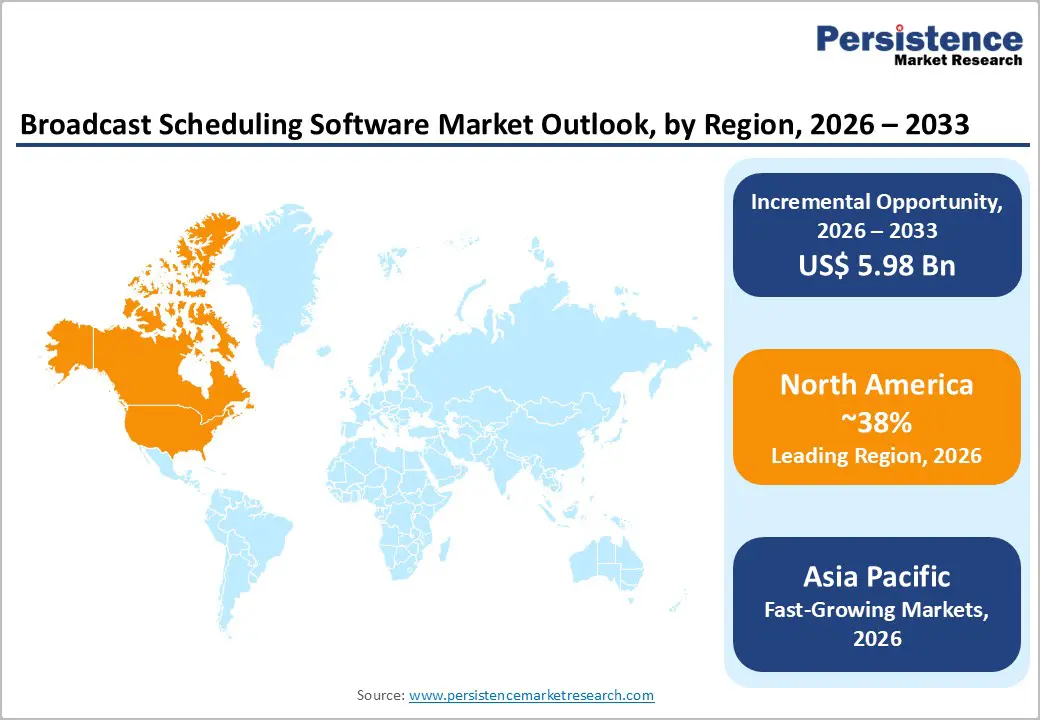

- Leading Region: North America is likely to lead with over 38% share in 2026, valued at approximately US$ 988.72 Million, supported by a mature broadcasting ecosystem, strong FAST channel penetration, and advanced scheduling automation adoption across major networks and sports broadcasters.

- Fast-growing Market: Asia Pacific is the fast-growing region with a CAGR of 24.5%, supported by rapid OTT expansion, large-scale digitization of terrestrial broadcasting infrastructure, and government-led digital migration initiatives across China, India, and Southeast Asia.

Market Dynamics

Drivers - Proliferation of OTT Channels and Linear-Digital Scheduling Convergence

The rapid expansion of OTT platforms alongside traditional linear broadcasting is driving demand for unified scheduling solutions that manage both environments within a single workflow. Global OTT video revenues surpassed US$ 300 billion in 2025, while streaming continues to account for an increasing share of total TV viewing time in major markets.

Broadcasters are now operating hybrid ecosystems that combine linear channels, FAST services, and on-demand libraries, intensifying the need for integrated scheduling systems. Legacy tools designed for linear-only operations struggle to manage cross-platform coordination, leading to inefficiencies and a manual workload. The expansion of global broadband infrastructure, with over 1.6 billion fixed broadband subscriptions worldwide, is further enabling large-scale multi-platform content distribution.

AI-Driven Automation Replacing Manual Schedule Optimisation

Increasing programming complexity and audience fragmentation are accelerating the shift from manual scheduling to AI-driven automation in broadcast operations. Large networks managing thousands of weekly programme slots are increasingly adopting algorithm-based tools to optimize scheduling decisions across content, advertising, and compliance requirements.

AI-enabled systems can reduce scheduling cycle times by 30-40% in vendor-reported deployments, particularly in high-volume multi-channel environments. These platforms also improve targeting accuracy by aligning content placement with audience affinity and real-time consumption data. Industry adoption is rising as broadcasters aim to improve efficiency, reduce operational costs, and enhance responsiveness in highly dynamic viewing environments.

Restraints - High Total Cost of Ownership for Legacy System Migration

Migration from on-premises broadcast management systems to modern scheduling platforms requires broadcasters to absorb simultaneous capital expenditure on new software licences, integration middleware, staff retraining, and often temporary parallel operations, a cost structure that compresses operating margins during transition and delays procurement decisions, particularly at regional and community broadcast operators.

The Society of Motion Picture and Television Engineers (SMPTE) has documented through its ST 2110 and ST 2022 standards compliance frameworks that full IP-transition projects for mid-size broadcasters routinely extend across 18 to 36 months and exceed initial budget projections, creating hesitancy among finance committees approving multi-year technology investments.

Data Sovereignty Regulations Constraining Cloud Adoption

National data localisation requirements directly suppress the addressable market for cloud-hosted scheduling platforms by forcing broadcasters in regulated jurisdictions to maintain on-premises or locally hosted infrastructure, fragmenting the economies of scale that make SaaS delivery commercially efficient for vendors. The General Data Protection Regulation (GDPR), enacted by the European Union in 2018, reinforced by the EU Data Act 2023, imposes strict constraints on cross-border data transfers that affect metadata, audience analytics, and EPG data flows integral to modern scheduling workflows, adding legal compliance overhead estimated at 10-20% of total project cost for broadcasters deploying pan-European scheduling platforms.

Market Opportunities

Emerging Market Public Broadcasters Digitising National Broadcast Infrastructure

Public broadcasters across Southeast Asia, Sub-Saharan Africa, and Latin America are increasingly modernising legacy broadcast operations through digital transformation initiatives. This shift is driven by spectrum efficiency, cost optimisation, and gradual migration from analogue to digital and cloud-based workflows. It is creating demand for modular broadcast scheduling software that can operate in bandwidth-constrained and infrastructure-limited environments.

Vendors offering phased deployment models, flexible pricing, and hybrid on-premise cloud architectures are better positioned to serve these markets. Localisation capabilities, including language support and regulatory compliance adaptation, are becoming key differentiators.

Sports Rights Fragmentation Driving Specialised Scheduling Platform Demand

The increasing fragmentation of sports media rights across linear broadcasters, OTT platforms, and hybrid streaming services is significantly raising scheduling complexity. Broadcasters now manage overlapping rights, concurrent live events, and multi-platform simulcast requirements, which traditional scheduling systems are often not designed to handle efficiently. This has created demand for specialised scheduling solutions with capabilities such as rights conflict detection, live-event rescheduling, and automated cross-platform coordination.

Integration with rights management systems and real-time production workflows is becoming critical for operational efficiency. Sports content owners and broadcasters are increasingly willing to invest in premium, purpose-built modules that reduce scheduling risk and improve monetisation of live content.

Category-wise Analysis

Offering Insights

Software/platform segment accounts for over 65.0% of the global broadcast scheduling software market in 2026, equivalent to US$ 1,691.23 Million, due to demand for centralized control over multi-channel programming, automated scheduling workflows, and real-time content coordination across linear and digital platforms.

Broadcasters rely on integrated scheduling engines, playout automation, and EPG management tools to reduce manual intervention and improve operational accuracy. Large networks require unified systems to manage complex programming grids across domestic and international feeds simultaneously. The emphasis is on scalability, workflow efficiency, and seamless coordination between content and advertising operations.

Services are expanding faster as broadcasters increasingly depend on external expertise for implementation, integration, and operational support of advanced scheduling platforms. Many operators lack in-house technical capability to configure complex workflows involving AI-based scheduling and multi-platform distribution. As platforms become more sophisticated, continuous vendor involvement is required for customization, system upgrades, and managed operations. This shift is particularly visible among OTT operators transitioning from manual EPG systems to automated scheduling pipelines.

Deployment Insights

On-premises deployment is likely to account for more than 37% share in 2026, reaching US$962.70 million, due to broadcasters with operational control, secure environments, and deep integration with legacy broadcast infrastructure.

High-reliability transmission environments continue to depend on localized systems to ensure uninterrupted scheduling and playout continuity. Many large operators maintain long lifecycle systems that are difficult to transition due to regulatory and technical constraints. The focus remains on stability, data control, and compliance within controlled broadcast facilities.

Cloud-based deployment is expanding rapidly as broadcasters shift toward flexible, scalable, and cost-aligned infrastructure models. It enables smaller and mid-sized operators to access advanced scheduling capabilities without heavy upfront infrastructure investment. Elastic capacity supports multi-channel scheduling, rapid content updates, and automated workflows across distributed networks. Increasing availability of media-optimized cloud infrastructure enhances performance and reduces latency concerns. The model is also favored for its ability to support remote operations and centralized content management.

Application Analysis

Television & entertainment broadcasting segment is likely to register over 39% of the global broadcast scheduling software market in 2026, driven by complex programming structures involving primetime planning, rights management, and regulatory content distribution requirements. Broadcasters require precise scheduling systems to balance audience engagement, advertising slots, and compliance obligations across large content volumes.

The segment depends heavily on structured workflows to manage thousands of annual programming hours efficiently. Automation supports optimization of content placement while maintaining consistency across multiple channels.

OTT & Streaming Platforms are emerging as a fast-expanding application due to the rise of FAST channels and continuously running digital content streams. Operators manage large volumes of linear-style channels that require uninterrupted scheduling automation without manual intervention. The scale of channel creation demands systems capable of handling real-time updates, advertising alignment, and content rotation. These platforms depend on scheduling intelligence to maximize engagement and advertising inventory utilization. Growth in ad-supported streaming models further increases reliance on automated scheduling frameworks.

Regional Insights

North America Broadcast Scheduling Software Market Trends and Insights

North America accounts for over 38% of the global broadcast scheduling software market in 2026, reaching approximately US$ 988.72 Million, supported by a highly mature and digitized broadcasting ecosystem. The region is anchored by a dense concentration of commercial television networks, FAST channel operators, and global sports rights holders, all of which are increasingly dependent on advanced scheduling automation.

Large-scale public investment in digital infrastructure, including the U.S. National Telecommunications and Information Administration (NTIA) broadband funding under the Infrastructure Investment and Jobs Act of 2021, exceeding US$ 65 billion, is expanding high-speed connectivity access and broadening the addressable viewer base. This expansion is reinforcing demand for scalable scheduling platforms among both enterprise and mid-tier broadcasters.

The United States broadcast scheduling software market is expected to reach approximately US$ 840.41 million by 2026, driven by the world’s largest commercial broadcasting and media distribution ecosystem. The country hosts more than 1,700 full-power commercial television stations licensed by the Federal Communications Commission, creating sustained demand for highly automated scheduling and playout management systems. The ongoing ATSC 3.0 transition is further reshaping operational requirements, as broadcasters increasingly need scheduling platforms capable of managing datacasting, targeted advertising overlays, and hybrid digital-terrestrial programming workflows.

Europe Broadcast Scheduling Software Market Trends and Insights

Europe broadcast scheduling software market is projected to surpassing the value of US$ 728.53 Million in 2026, driven by a highly regulated and mature broadcast ecosystem. The growth is shaped by the EU Audiovisual Media Services Directive (AVMSD), which mandates strict content quotas and prominence rules for European works across linear and on-demand platforms. The 2022 transposition across member states has accelerated compliance-led procurement of scheduling platforms with built-in quota tracking and automation capabilities.

Europe’s strong public broadcasting foundation, supported by organisations such as ARD, ZDF, France Télévisions, and BBC, ensures stable enterprise-grade software renewal cycles.

Germany holds over 20% in the regional market surpassing US$ 145.71 Million, supported by ARD and ZDF’s extensive multi-channel operations and strict regulatory requirements under the Interstate Broadcasting Treaty, which enforces algorithmic compliance for must-carry and content prominence rules.

The United Kingdom broadcast scheduling software market value exceeding US$ 167.56 Million, due to broadcasters such as BBC, ITV, Channel 4, and Sky UK, alongside Ofcom’s updated Media Act 2024, enhancing prominence compliance obligations.

France growth is supported by France Télévisions and TF1 Group, where ARCOM regulations enforce French-language content quotas and expanding oversight now includes streaming platforms, broadening scheduling software demand.

The Rest of Europe market surpassing the value of US$ 123.85 Million value by 2026, covering key markets such as Poland, BENELUX, and Nordics. Poland is undergoing multi-year digital transformation initiatives, increasing adoption of cloud-based and IP-integrated scheduling systems. Nordic broadcasters represent early adopters of advanced cloud-assisted scheduling workflows integrated with modern IP production environments. Growth across these markets is further supported by EU-level funding mechanisms such as the Creative Europe MEDIA programme, which co-finances broadcast modernization projects across smaller member states.

Asia Pacific Broadcast Scheduling Software Market Trends and Insights

Asia Pacific broadcast scheduling software market is exceeding the value over US$ 624.46 Million by 2026 and emerge as the fast-growing region at a CAGR of 24.5% due to large-scale digitisation of terrestrial broadcasting infrastructure and rapid OTT platform proliferation across emerging and developed markets.

Government-led digital migration mandates and regulatory modernisation are increasing compliance-driven demand for advanced scheduling systems. The shift toward IP-based broadcasting and automated playout orchestration is further strengthening enterprise software penetration across the region. Growing mobile-first content consumption is reinforcing the need for real-time, metadata-rich scheduling workflows.

China's broadcast scheduling software market is surpassing US$ 212.32 million in 2026, driven by centrally regulated broadcasting operations under the National Radio and Television Administration (NRTA). Large-scale networks such as CCTV and provincial satellite broadcasters require highly controlled scheduling systems to ensure domestic content quotas, transmission compliance, and multi-channel coordination.

The NRTA’s ultra-high-definition broadcasting roadmap extending through 2025 is accelerating upgrades toward 4K and 8K-capable scheduling platforms with enriched metadata workflows. Japan is reaching the market value of US$ 124.89 Million, supported by NHK and major commercial broadcasters managing hybrid terrestrial, satellite, and IP simulcast operations. Regulatory reforms enabling IP-delivered broadcasting are driving replacement cycles for legacy scheduling systems across licensed operators.

India is likely to achieve a robust growth supported by one of the world’s largest multi-channel broadcast ecosystems under TRAI oversight. With more than 900 licensed television channels, broadcasters such as Disney Star and Zee Entertainment Enterprises require enterprise-grade scheduling tools capable of managing multilingual content libraries, advertising compliance, and regional programming distribution. Expanding FAST channel adoption and connected TV penetration is further strengthening demand for automated scheduling platforms.

South Korea's growth is driven by advanced IP-integrated broadcast operations across KBS, MBC, and SBS. Strong global export of Korean content is increasing complexity in international rights window scheduling, pushing demand for AI-assisted compliance and monetisation-aware scheduling systems.

Competitive Landscape

The broadcast scheduling software market operates as a moderately concentrated landscape where top players collectively hold leading share positions through deep integration into broadcast automation, traffic management, and media asset workflows, making displacement costly and contractual switching infrequent at the enterprise tier. Competition pivots primarily on depth of cloud-native architecture, AI scheduling optimisation capability, and API ecosystem breadth rather than price, as the total cost of workflow disruption outweighs licence cost differences for Tier-1 buyers.

Key Developments:

- In March 2026, Imagine Communications enhanced its Landmark Rights & Scheduling platform with new AI-assisted scheduling capabilities to automate and streamline broadcast programming workflows. The upgrade aims to reduce manual effort by optimizing scheduling tasks such as off-peak and overnight content planning.

- In March 2026, Mediagenix launched a new content-aware scheduling engine designed to enhance channel performance by automatically optimizing broadcast playlists using contextual and audience-driven insights. The solution supports linear TV, FAST channels, and streaming platforms by integrating content metadata, rights, and engagement data into scheduling decisions.

Companies Covered in Broadcast Scheduling Software Market

- WideOrbit

- Imagine Communications

- MediaGenix

- Marketron

- BroadView Software

- Amagi

- Pebble

- Dalet

- Myers Information Systems

- Provys

- Aveco

- VSN

- AxelTech

- Others

Frequently Asked Questions

The global broadcast scheduling software market is valued at US$ 2.60 billion in 2026 and is projected to reach US$ 8.58 billion by 2033, expanding at a CAGR of 18.6%, due to structural convergence of linear broadcast and digital streaming workflows, compelling broadcasters globally to replace siloed scheduling systems with unified, AI-capable platforms.

The growth is driven by the rising need to automate high-volume content scheduling for expanding FAST channels, with platforms like Roku hosting 350+ linear FAST channels.

Software/Platform segment leads with 65% share in 2026 due to its critical role in managing scheduling engines and EPG workflows. Broadcasters depend on these systems as essential infrastructure to ensure uninterrupted transmission, compliance, and monetisation across both linear and digital channels.

North America leads with an over 38% share, supported by a dense network of over 1,700 TV stations regulated by the Federal Communications Commission. The region’s dominance is reinforced by FAST channel expansion and evolving broadcast standards such as ATSC 3.0, which increase demand for advanced scheduling systems.

The key opportunities lie in FAST ecosystem expansion and first-time digitization of public broadcasters in emerging markets. These users need cloud-native, modular scheduling tools with compliance support, especially as governments modernize broadcasting infrastructure and shift toward automated, scalable content delivery systems.

The leading companies include WideOrbit, Imagine Communications, MediaGenix, Marketron, BroadView Software, Amagi, Pebble, and Dalet, among others.