- Food Packaging

- Beverage Crates Market

Beverage Crates Market Size, Share, and Growth Forecast, 2026 - 2033

Beverage crates market by Material Type (HDPE, PP, PE, PVC, Others), Product Type (Nestable or Stackable, Collapsible), Application (Alcoholic Drinks, Non-alcoholic Drinks), and Regional Analysis for 2026 - 2033

Beverage Crates Market Size and Trends Analysis

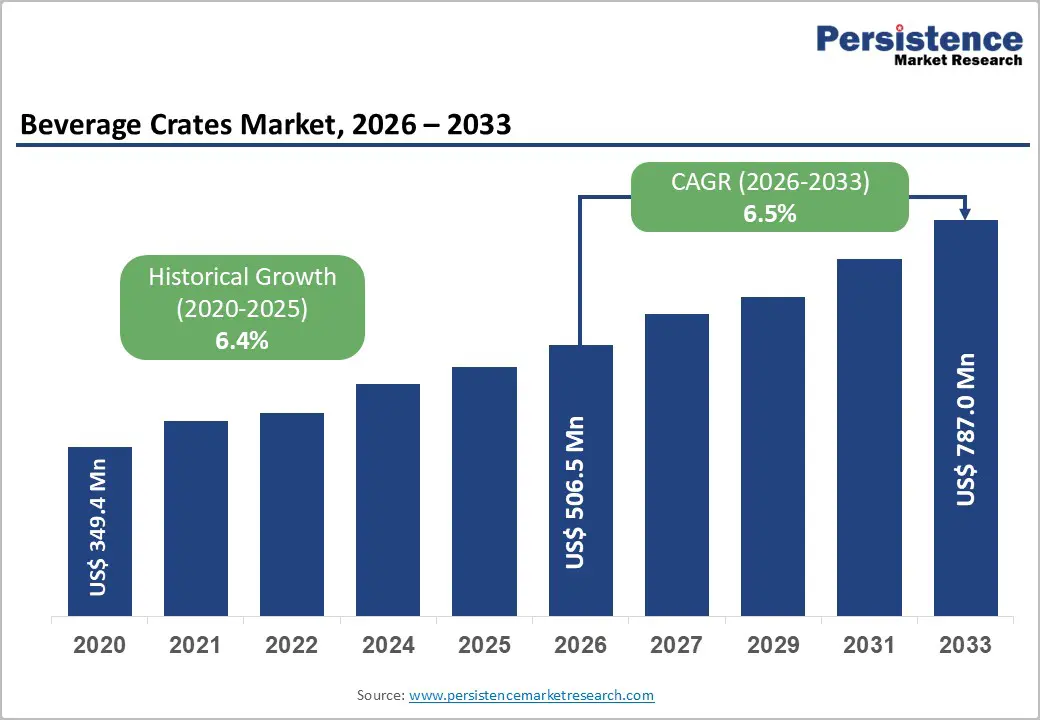

The global beverage crates market size is likely to be valued at US$506.5 million in 2026, and is expected to reach US$787.0 million by 2033, growing at a CAGR of 6.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of organized beverage distribution, rising demand for reusable and durable crates in the alcoholic and non-alcoholic drinks sector, and growing focus on supply-chain efficiency and sustainability in bottling and logistics.

The growing demand for HDPE nestable/stackable beverage crates, especially for non-alcoholic drinks in commercial logistics, is accelerating adoption among bottlers and distributors. Advances in UV-stabilized, food-grade polymers and collapsible designs are further boosting uptake by offering better hygiene, space savings, and longer service life. The increasing recognition of beverage crates as critical for product protection, cost reduction in returnable logistics, and compliance with the circular economy in emerging beverage markets remains a major driver of market growth.

Key Industry Highlights:

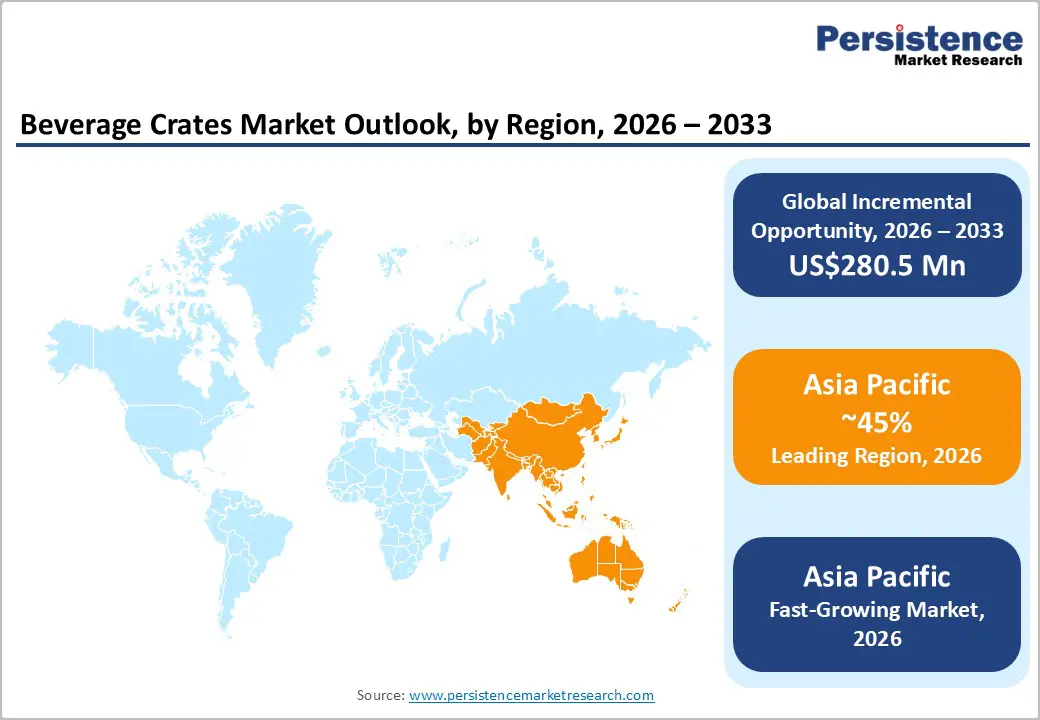

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by massive beverage production, rapid organized retail growth, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by expanding soft-drink and beer volumes, increasing reusable crate adoption, and rising logistics investments.

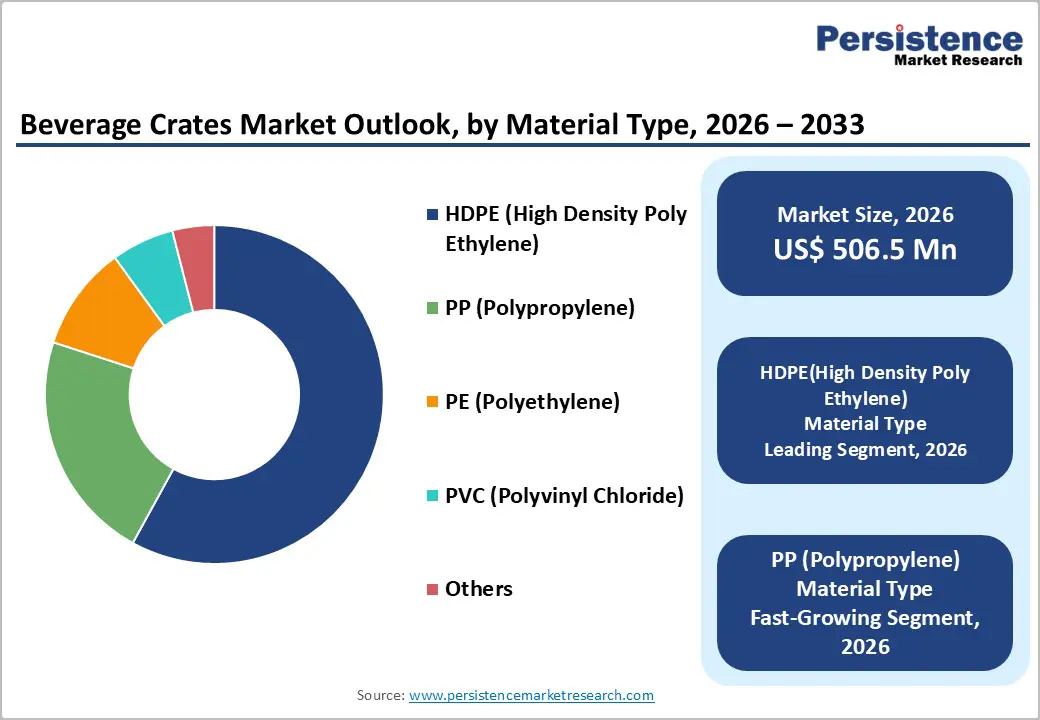

- Dominant Type: HDPE (High Density Poly Ethylene), to hold approximately 58% of the market share, as it remains the most preferred material for durability and cost.

- Leading Application: Non-alcoholic Drinks, accounting for over 55% of the market revenue, due to the highest consumption volume.

| Key Insights | Details |

|---|---|

|

Beverage Crates Market Size (2026E) |

US$506.5 Mn |

|

Market Value Forecast (2033F) |

US$787.0 Mn |

|

Projected Growth CAGR (2026-2033) |

6.5% |

|

Historical Market Growth (2020-2025) |

6.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Beverage Production and Returnable Logistics Adoption

Integration of beverage production with returnable logistics systems significantly propels the beverage crates market by reinforcing closed-loop asset circulation and aligning with government-mandated recovery targets. Governments worldwide are enacting deposit-return systems (DRS) and container-deposit legislation that financially incentivize the return of beverage containers for reuse or recycling and ensure high collection efficiency. Official data shows that jurisdictions implementing structured return schemes can achieve container return rates of more than 90% for targeted beverage packaging categories, underscoring the effectiveness of such systems in capturing packaging assets and driving reuse cycles.

Enhanced return logistics reduce losses and support predictable crate asset flows for beverage producers and logistics providers, thereby lowering dependency on single-use packaging and reducing operating costs over multiple cycles while helping companies meet tightening regulatory requirements for waste reduction and material recovery. As beverage production volumes continue to grow globally, with billions of bottles and cans sold annually, the ability to retrieve, sanitize, and reuse crates prevents material depletion and supports resilient supply chains. Market demand for durable returnable crates rises in tandem with these regulatory and operational shifts, making adoption of returnable logistics a strategic driver of the beverage crates market.

Focus on Sustainability and Circular Packaging

Sustainability and circular packaging are material drivers for the beverage crates market because they align supply chain cost-efficiency with regulatory mandates on waste reduction and resource reuse, improving operational and environmental outcomes. Governments and regulators are increasingly embedding circular economy principles into law to keep materials in circulation and reduce environmental externalities, requiring packaging producers to design for reuse and recyclability. For example, the European Union aims to make all packaging in its market recyclable in an economically viable way by 2030 and has set ambitious targets to double its overall circularity rate by 2030, demonstrating clear policy support for systems that keep packaging in use longer and divert waste from landfill.

Reusable packaging formats such as crates can dramatically cut lifecycle emissions and material demand compared with single-use alternatives. Industry-linked research shows that reusable crates emit substantially less greenhouse gas over their service life, reinforcing their strategic value for supply chain sustainability. Beverage industry players are adopting returnable crate systems to reduce dependency on disposable packaging, support compliance with extended producer responsibility schemes, and improve resource yield through multiple reuse cycles. Policies such as the EU’s packaging waste rules and similar frameworks in other jurisdictions enhance the economic advantages of circular systems by internalizing environmental costs and boosting material recovery.

Barrier Analysis - High Initial Investment in Returnable Systems

Returnable packaging systems require a substantial upfront capital outlay for durable containers, tracking technologies, cleaning facilities, and reverse logistics infrastructure, which can act as a significant barrier to broader adoption in the beverage crates market. Procuring a sufficient inventory of reusable crates and implementing technologies such as RFID tracking and automated sorting systems can run into hundreds of thousands of dollars before any operational benefits are realized. According to MDPI, comprehensive reusable packaging systems often require an initial investment ranging from US$500,000 to US$5 million, depending on scale and complexity, with extended payback periods that can strain working capital for many companies, especially those with limited financial resources.

The financial challenge extends beyond container procurement to the infrastructure needed for effective reuse cycles, including collection, cleaning, inspection, and redistribution networks. Establishing these capabilities adds both fixed and variable costs and demands strategic planning around inventory levels, transportation routes, and system integration. High upfront investment can divert funds from other operational priorities and increase perceived business risk when immediate returns are not guaranteed.

Reverse Logistics and Loss/Damage Challenges

Inefficiencies in reverse logistics and high rates of loss or damage in returnable systems restrain the beverage crates market by increasing operational costs and eroding projected lifecycle savings. Establishing and managing reverse logistics networks to collect, sort, clean, and redistribute crates requires significant coordination, specialized infrastructure, and asset-tracking capabilities, expenditures that can deter investment and limit adoption, particularly for smaller manufacturers and distributors.

Asset loss and damage during transport and handling further weaken the economics of reuse, forcing firms to maintain larger buffer inventories and incur replacement costs that reduce the cost-neutral advantage of multiple reuse cycles. Loss and theft rates averaging 8–15% annually across industry applications have been documented, indicating the scale of inefficiencies that reverse flows can impose on reusable packaging systems.

Opportunity Analysis - Adoption of Collapsible and Smart Beverage Crates

Emerging collapsible and smart crate technologies present a tangible opportunity for the beverage crates market by improving distribution efficiency, reducing logistics costs, and supporting compliance with tightening reuse mandates. Regulatory frameworks such as the European Packaging and Packaging Waste Regulation (PPWR) require that at least 10% of beverages (alcoholic and non-alcoholic) be sold in reusable packaging by 2030, creating a measurable market pull toward innovative returnable systems capable of meeting this reuse quota. Collapsible crates significantly cut backhaul and storage space costs by folding flat when empty, increasing asset utilization and lowering supply chain overheads in high-volume beverage distribution networks, a capability aligned with broader industry cost-reduction and sustainability goals.

Smart beverage crates further enhance these benefits by integrating technologies such as RFID and embedded sensors to provide real-time visibility, improve inventory accuracy, and support predictive logistics planning. Real-time tracking reduces losses and enables data-driven decisions that can decrease handling inefficiencies and asset downtimes throughout the return loop. Investment in smart systems positions beverage manufacturers and distributors to comply more effectively with regulatory reuse targets while unlocking operational value through improved traceability, custodial control of assets, and optimized routing, thereby strengthening competitive positioning in increasingly sustainability-focused supply chains.

Expansion of Retail and E-Commerce Distribution Networks

The rapid growth of retail and e-commerce channels is creating a strong demand for efficient, durable, and reusable packaging solutions, making beverage crates a critical component of modern supply chains. Retailers and online grocery platforms require standardized and robust crates that can withstand repeated handling, stacking, and transportation across complex distribution networks. Governments report that e-commerce sales in the U.S. food and beverage sector grew by over 18% annually between 2020 and 2023, underscoring the scale of the logistics challenge and the need for optimized packaging systems. Beverage companies that leverage reusable crates can improve operational efficiency by minimizing product damage during multi-stage delivery processes while meeting sustainability goals through multiple reuse cycles.

As distribution networks expand, integrating returnable beverage crates supports cost reduction and environmental compliance across the supply chain. The logistics advantages include simplified returns, reduced dependence on single-use packaging, and lower material costs. U.S. Department of Energy data indicates that optimized logistics and the use of reusable containers can reduce transportation energy consumption by up to 20% in high-frequency distribution scenarios. These efficiencies enhance profitability, strengthen supply chain resilience, and position beverage companies to meet both consumer expectations and regulatory sustainability targets, establishing a competitive advantage in an evolving retail landscape.

Category-wise Analysis

Material Type Insights

The HDPE (high-density polyethylene) segment is anticipated to dominate the market, accounting for approximately 58% of the market share in 2026. Its dominance is driven by its superior durability, chemical resistance, and lightweight properties. Its robustness allows crates to withstand repeated handling, stacking, and long-distance transportation without deformation, making it ideal for both retail and e-commerce distribution. HDPE’s recyclability and alignment with circular packaging initiatives further enhance its appeal, enabling manufacturers to meet sustainability targets and reduce environmental impact. Coca-Cola Europacific Partners is rolling out returnable beverage crates made from 97% recycled HDPE in the Netherlands. These reusable crates, produced in partnership with Schoeller Allibert and recycler Healix, have an average lifespan of around 15 years and are used to transport returnable glass bottles of Coca-Cola’s brands, including Coca-Cola, Fanta, and Sprite.

The PP (polypropylene) segment is the fastest-growing, driven by its strong impact resistance, chemical stability, and lightweight nature, which improve logistics efficiency and durability during repeated transport cycles. PP crates maintain structural integrity across a wide range of temperatures and handling conditions, making them suitable for complex beverage supply chains that include cold-chain distribution and multi-modal transport. Schoeller Allibert’s reusable plastic crates serve major beverage producers through customizable PP-based solutions designed for durability and supply chain resilience. These crates are widely used across Europe and North America for secure returnable transport, demonstrating PP’s practical value in high-volume beverage logistics.

Application Insights

Non-alcoholic drinks are expected to dominate the market, accounting for nearly 55% of revenue in 2026, driven by high consumption volumes and frequent circulation across retail and distribution networks. Products such as soft drinks, bottled water, juices, and ready-to-drink teas require robust, reusable crate systems that can endure repeated handling, stacking, and long-distance transport. The high turnover of these beverages drives demand for standardized, durable crates that improve operational efficiency and reduce losses during transit. Bundaberg Brewed Drinks, an Australian producer of non-alcoholic ginger beer and other soft drinks, distributes its products in returnable crates to retailers and supermarkets across domestic and international markets.

Alcoholic drinks represent the fastest-growing application, fueled by increasing global consumption of beer, wine, and spirits. Manufacturers and distributors are shifting toward reusable and durable crates to safely transport bottles, ensuring product integrity and reducing breakage. Seasonal demand peaks, festivals, and the expansion of bar and restaurant networks further drive the need for efficient packaging solutions. Lightweight, stackable, and sturdy crates help streamline logistics, lower transportation costs, and support sustainable practices. AB-InBev, the world’s largest brewing group, worked with Schoeller Allibert to develop a sustainable reusable beer crate made from over 90% recycled plastic, including maritime waste, for its Corona brand. These crates are designed to securely transport beer bottles while reducing environmental impact and supporting a circular packaging model, showing how breweries are investing in durable, reusable crates for alcoholic beverage logistics.

Regional Insights

North America Beverage Crates Market Trends

Market growth in North America is driven by the region’s large beverage production, strong logistics networks, and high public awareness of reusable packaging benefits. Distribution systems in the U.S. and Canada provide extensive support for beverage crate programs, ensuring wide accessibility across HDPE, nestable/stackable, and non-alcoholic drink categories. Increasing demand for durable, convenient, and easy-to-pool forms is further accelerating adoption, as these formats improve hygiene and reduce barriers associated with single-use packaging.

Innovation in beverage crate technology, including stable collapsible crates, improved food-grade delivery, and targeted alcoholic enhancement, is attracting significant investment from both public and private sectors. Government initiatives and EPA campaigns continue to promote the use of waste risks, sustainability concerns, and emerging circular threats, creating sustained market demand. The growing focus on collapsible grades and specialty uses, particularly for non-alcoholic drinks and others, is expanding the target applications for beverage crates.

Europe Beverage Crates Market Trends

Market growth in Europe is driven by increasing awareness of the benefits of circular packaging, strong regulatory frameworks, and government-led reusable packaging programs. Countries such as Germany, France, the U.K., and the Netherlands have well-established beverage logistics frameworks that support routine use of beverage crates and encourage adoption of innovative collapsible delivery methods. These high-compliance formulations are particularly appealing to non-alcoholic drink consumers, regulation-conscious bottlers, and retail users, thereby improving hygiene and coverage rates.

Technological advancements in beverage crates development, such as enhanced food-grade polymers, application-targeted delivery, and improved collapsible grades, are further boosting market potential. European authorities are increasingly supporting research and trials for crates against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, reusable options is aligned with the region’s focus on preventive waste reduction and extended producer responsibility. Public awareness campaigns and promotion drives are expanding reach in both food service and retail segments, while suppliers are investing in sustainable materials and novel variants to increase efficacy.

Asia Pacific Beverage Crates Market Trends

Asia Pacific is projected to dominate and be the fastest-growing market, capturing with 45% of the market revenue in 2026, driven by rising beverage consumption awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Indonesia, and Thailand are actively promoting crate campaigns to address organized beverage growth and emerging sustainability needs. Beverage crates are particularly attractive in these regions due to their cost-effective administration, ease of adoption, and suitability for large-scale non-alcoholic drinks and modern trade drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-pool beverage crates that can withstand challenging logistics conditions and minimize reliance on external suppliers. These innovations are critical for reaching domestic bottlers and improving overall supply-chain coverage. The growing demand for HDPE, nestable/stackable, and non-alcoholic drinks applications is driving market expansion. Public-private partnerships, increased beverage expenditure, and rising investment in crate research and production capacity are further accelerating growth. The convenience of crate delivery, combined with improved hygiene and reduced risk of breakage, positions it as a preferred choice.

Competitive Landscape

The global beverage crates market is shaped by intense competition between well-established pooling specialists and emerging regional manufacturers. In North America and Europe, industry leaders such as Brambles Ltd and Schoeller Allibert dominate through extensive rental networks, strong R&D capabilities, and close relationships with major bottlers. These companies focus on innovation, offering HDPE (high-density polyethylene) and collapsible crate programs that improve durability, reduce transport costs, and streamline storage. In the Asia Pacific region, local manufacturers are gaining traction with cost-effective solutions, making beverage crates more accessible for small and medium-scale bottlers and distributors.

Advanced HDPE nestable crates enhance pooling efficiency by lowering product loss risks and enabling large-scale integrations across bottling operations. Strategic partnerships, collaborations, and acquisitions are further shaping the market, merging technological expertise, expanding pool networks, and accelerating commercialization. Collapsible designs address urban logistics challenges by saving space during storage and transport, improving overall operational efficiency while supporting sustainable, reusable packaging practices in densely populated areas.

Key Industry Developments:

- In March 2025, Tetra Pak and Schoeller Allibert launched a new transport crate made from polyAl recovered from used beverage cartons at the Plastics Recycling Show in Amsterdam on 1–2 April 2025. The crates used up to 50% recycled polyAl combined with other recycled materials, with no virgin plastics. Schoeller Allibert designed the crates to meet high industry standards for durability and performance. The solution offers a sustainable, cost-competitive alternative to conventional packaging. This collaboration highlights circular economy practices and promotes reusable logistics solutions in the beverage industry.

- In June 2024, Schoeller Allibert teamed up with Coca-Cola Europacific Partners and recycler Healix to advance circular packaging. The partnership produced iconic red hospitality crates using 97% recycled plastic. Schoeller Allibert’s Material Innovation team developed a new material blend to enable this shift. The crates met durability and performance standards for hospitality use. Production cuts CO2 emissions by an estimated 66% compared with virgin plastic crates. The rollout reduced reliance on virgin polymers across the crate pool.

- In December 2023, German drugstore chain DM and Procter & Gamble adopted reusable GS1 Smart-Box transport crates, cutting disposable packaging by 50 metric tons. The initiative delivered initial savings for P&G’s Gillette line and planned to expand the use of crates across other product categories to boost environmental sustainability and operational efficiency. This move represented a significant step toward reducing waste and improving supply chain practices.

Companies Covered in Beverage Crates Market

- Brambles Ltd

- Schoeller Allibert

- DS Smith

- Rehrig Pacific Company

- TranPak Inc.

- Sino Mould

- Gamma-Wopla nv

- Mondi

- RPP Containers

- Ravensbourn Limited

- Supreme.co.in

- Didak Injection

- DynaWest Engineering Ltd.

- ENKO CHEM, INC.

- Xiamen Haosen Plastic Products Co., Ltd

- Guangzhou TSUNAMI Industrial Equipment Co., Ltd

- Zhejiang Zhengji Plastic Industry Co., Ltd

- Shenzhen Xingfeng Plastic Co., Ltd.

Frequently Asked Questions

The global beverage crates market is projected to reach US$506.5 million in 2026.

High damage and pilferage rates in corrugated packaging during multi-leg beverage distribution are pushing distributors to shift toward rigid crates that protect bottles and reduce write-offs.

The beverage crates market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Rapid growth of city-based micro-warehouses and quick-commerce beverage delivery creates demand for collapsible, nestable crates that reduce return-trip volume and improve last-mile efficiency.

Brambles Ltd, Schoeller Allibert, Rehrig Pacific Company, DS Smith, and TranPak Inc. are the key players.