PMRREP5225

9 Apr 2025 IT and Telecommunication

185 Pages

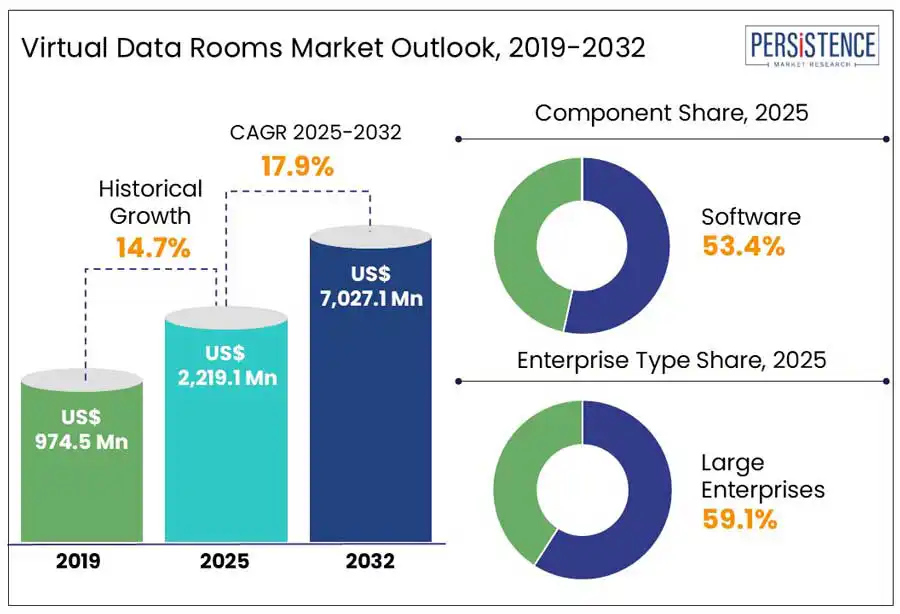

The global virtual data rooms market size is projected to rise from US$ 2,219.1 Mn in 2025 to US$ 7,027.1 Mn by 2032. It is anticipated to witness a CAGR of 17.9% during the forecast period from 2025 to 2032.

According to Persistence Market Research, the ability of a virtual data room (VDR) to offer a hierarchical file structure in a company for improving user experience and document management propels demand. Integration of Machine Learning (ML) and Artificial Intelligence (AI) to automate every process is further anticipated to strengthen the document management features of VDRs.

Key Industry Highlights

|

Global Market Attribute |

Key Insights |

|

Virtual Data Rooms Market Size (2025E) |

US$ 2,219.1 Mn |

|

Market Value Forecast (2032F) |

US$ 7,027.1 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

17.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

14.7% |

Rapid shift toward hybrid and remote work models is projected to propel demand for digital collaboration tools such as VDRs. Moving to such work models often come with a set of challenges, including data security, version control, and document accessibility. Remote teams mainly require cloud-based, secure platforms that not only provide encryption and permissions to prevent data breaches but also enable access from multiple locations.

According to studies, as of 2023, more than 82% of companies plan to maintain a hybrid work model going forward. Hence, VDRs are estimated to be important in such settings to access confidential files with features such as automatic document expiration, activity tracking, and role-based access control. These features are particularly essential in fields where sensitive projects require cooperation between staff members, consultants, and external advisors.

Demand for VDRs is anticipated to witness a decline in specific industries owing to increasing adoption of alternative collaboration tools providing a wide range of functions at lower costs. Platforms such as Dropbox Business, Google Workspace, and Microsoft SharePoint have evolved, offering compliance support, real-time collaboration, and novel access controls features. These features were once only limited to VDRs.

A few companies are likely to opt for these tools for regular corporate file sharing as these are integrated with existing productivity software solutions and have more user-friendly interfaces. Companies conducting board meetings or internal audits, for instance, are projected to choose Microsoft Teams paired with OneDrive. It is likely to enable easy access to required documents without licensing fees or the steep learning curve related to VDRs.

A key opportunity in the virtual data rooms market lies in developing new solutions for niche verticals apart from legal due diligence and mergers and acquisitions. Pharmaceutical companies, for instance, often run several clinical trials at once. They are projected to adopt VDRs to easily submit regulatory documents, share critical information with Contract Research Organizations (CROs), and manage trial protocols.

A few other pharmaceutical companies are also predicted to use VDRs for collaborations and vaccine development. These solutions offer a secure platform to conduct research across various countries, while maintaining privacy. VDRs are further projected to be used for media licensing agreements, real estate asset scrutinization, and energy sector deals as these involve the exchange of proprietary assets and high-value contracts.

As the threat landscape transforms, cybersecurity improvements are likely to become a key focus of VDR providers. As per a recent study, in 2023, the average cost of a data breach was US$ 4.45 Mn globally, with breaches in the healthcare sector reaching over US$ 10 Mn. VDRs mainly store sensitive information such as intellectual property, merger agreements, board communications, and financial statements. Hence, these are becoming easy targets for cybercriminals.

VRD providers are focusing on innovative, multi-layered cybersecurity frameworks to enhance security. They are implementing zero-trust architecture in VDR models to allow constant device compliance and verification before providing access. Firmex, for example, provides multi-factor authentication, time-limited document access, and dynamic watermarking to reduce the risk of breaches. Similar initiatives by key companies are projected to create new opportunities for long-term growth.

In terms of component, the global market is bifurcated into software and services. Among these, the software segment will likely lead by generating a virtual data rooms market share of around 53.4% in 2025, says Persistence Market Research. Growth is driven by increasing demand for efficient and secure data sharing solutions in high-stake work environments.

Software solutions also provide granular control over who can edit, download, or view documents. Features such as two-factor authentication, audit trails, and watermarking are projected to ensure that confidentiality is maintained at every stage.

Services are anticipated to witness steady growth in the foreseeable future. Rising demand for VDR services such as maintenance, consulting, support, training, and integration across various industries is predicted to contribute to growth. Varying maintenance requirements and lack of skilled staff in several industries are further projected to boost the segment.

Based on enterprise type, the global market is bifurcated into large enterprises and Small and Medium Enterprises (SMEs). Out of these, large enterprises are anticipated to dominate by accounting for a share of about 59.1% in 2025. It is attributed to increasing external interactions, large-scale operations, and the presence of various teams in different parts of the world.

The aforementioned factors are propelled by different processes such as collaborative projects, mergers, compliances, and financial transactions. High demand for remote monitoring and constant transformations in work culture are further estimated to push the segment.

SMEs, on the other hand, are likely to see decent growth through 2032 with easy availability of cost-effective virtual data room services and solutions. Adoption of several digital technologies by various SMEs and lack of in-house experts are also spurring demand.

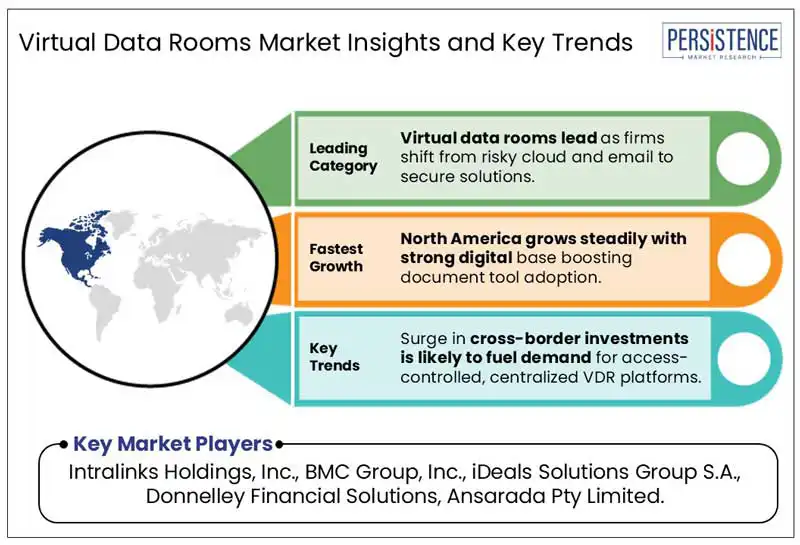

In 2025, North America is projected to hold a share of around 42.5%. Growth is attributed to rapid digitization of corporate workflows and increasing mergers and acquisitions in the region. The U.S. virtual data rooms market is predicted to remain at the forefront through 2032 as local platforms including DealRoom, Intralinks, and Datasite are investing in extending their product lines to launch innovative VDR solutions.

Laws such as the California Consumer Privacy Act (CCPA), HIPAA, and the Sarbanes-Oxley Act (SOX) in the U.S. are further estimated to propel companies to embrace safe digital environments to handle sensitive information. VDRs are projected to provide user-specific permissions and audit trails to help companies comply with the aforementioned norms.

India is projected to be a key VDR adopter in Asia Pacific due to its rising venture capital and private equity activities. Studies showed that the country stood 3rd worldwide in start-up funding in 2023, bagging over US$ 25 Bn. VDRs are likely to be increasingly used during due diligence for corporate restructuring, mergers, and funding rounds, thereby spurring demand.

Japan, on the other hand, is creating new growth avenues backed by an aging corporate ownership structure as well as rising cross-border mergers and acquisitions. Various mid-sized companies in the country are demanding international restructuring or buyers through buyouts, pushing the need for safe data-sharing platforms, including VDRs.

In Europe, the U.K. is projected to be one of the most significant users of VDR platforms. London, a key hub for legal advisory and private equity firms, houses several heavy users of VDR platforms. The requirement for region-specific compliance features has also surged due to post-Brexit regulatory divergence. U.K.-based law firms, for example, are required to use Ansarada and Intralinks for cross-border corporate restructuring and litigation.

France, on the other hand, is anticipated to witness a decent CAGR from 2025 to 2032. Growth of the country’s market is attributed to government-backed digitization programs. Also, booming biotech and technology start-up culture in the country is estimated to propel growth. As per a new study, more than €13.5 Bn was spent in 2023 on technology alone. Each funding round involved sensitive investor information, making VDRs a key tool.

The global market houses several big and small-scale companies. They are competing for high shares by adopting various strategies such as new product launches, partnerships, and acquisitions. A few start-up firms in emerging markets are focusing on joining hands with international players to co-develop innovative virtual file rooms. Some of the other well-established companies are striving to create robust data rooms to get a better understanding of their business models.

The market is projected to be valued at US$ 2,219.1 Mn in 2025.

The market is estimated to rise at a CAGR of 17.9% through 2032.

iDeals Solutions Group S.A., BMC Group, Inc., and Intralinks Holdings, Inc. are a few leading companies.

The key players mentioned in the virtual data rooms market include Intralinks Holdings, Inc., BMC Group, Inc., iDeals Solutions Group S.A., Donnelley Financial Solutions, and Ansarada Pty Limited.

Software is anticipated to be the dominant component in the market.

|

Report Attribute |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As Applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Component

By Enterprise Type

By Deployment

By End-user

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author