- Media & Entertainment

- Virtual Reality Market

Virtual Reality Market Size, Share, and Growth Forecast 2026 - 2033

Virtual Reality Market by Device Type (Head-Mounted Displays, Gesture Tracking Devices, Projected & Display Walls), Technology (Non-immersive, Semi and Full Immersive), Application (Gaming, Surgery & Training, E-learning, Vehicle Simulation, Other), End-use Industry (Media & Entertainment, Healthcare, Aerospace & Defense, Education, Other), and Regional Analysis for 2026 - 2033

Virtual Reality Market Size and Trend Analysis

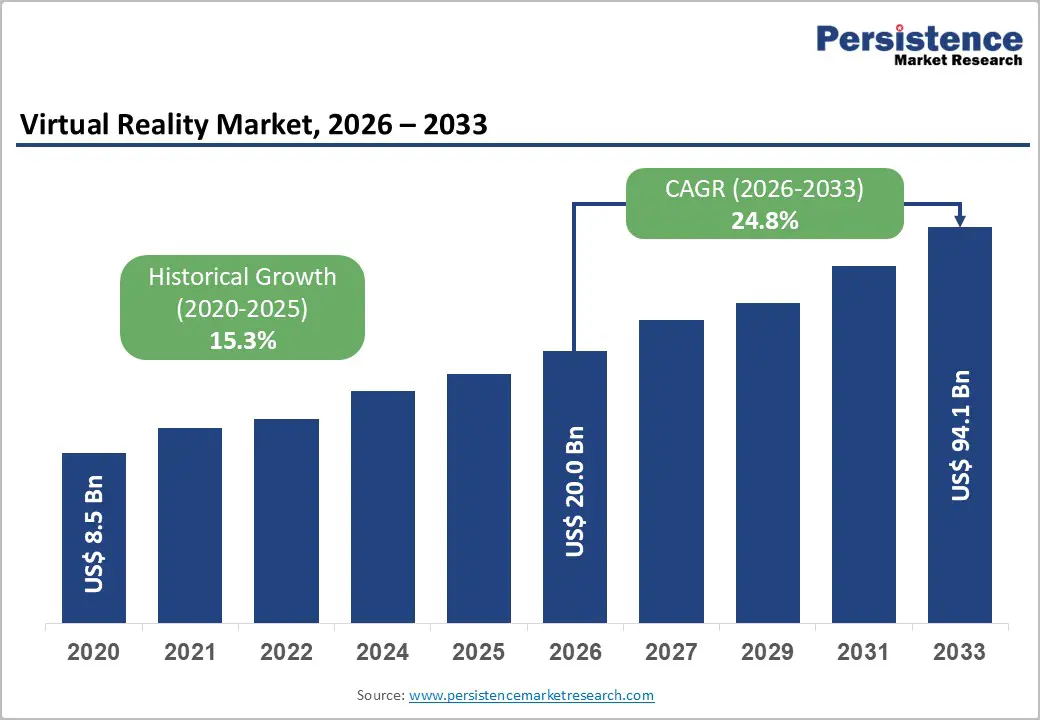

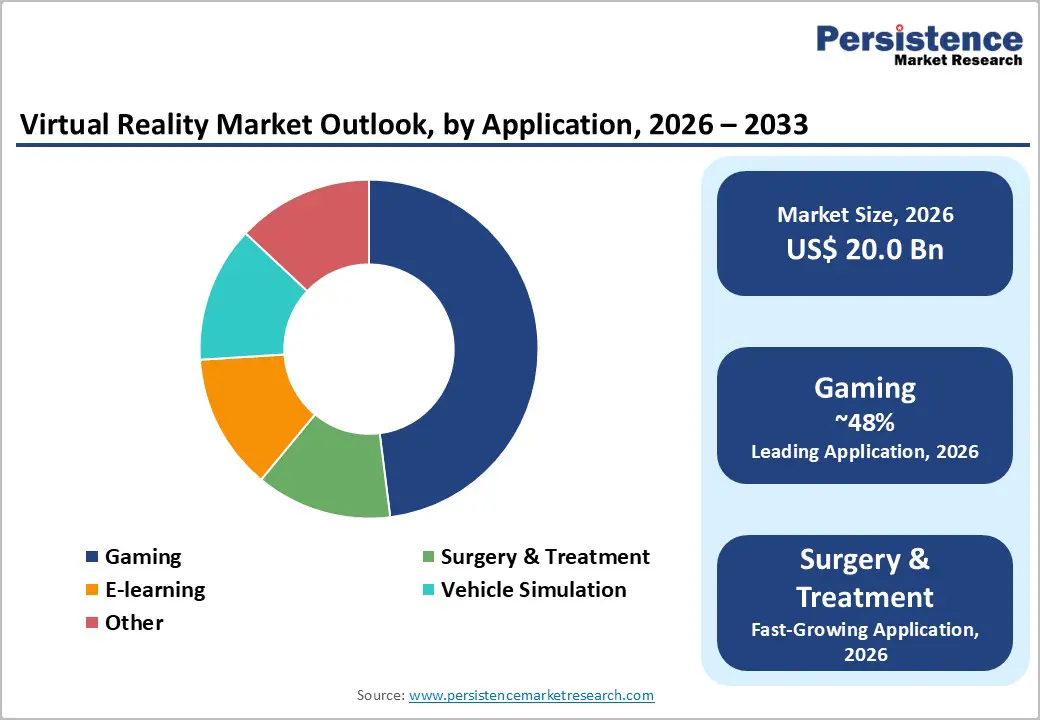

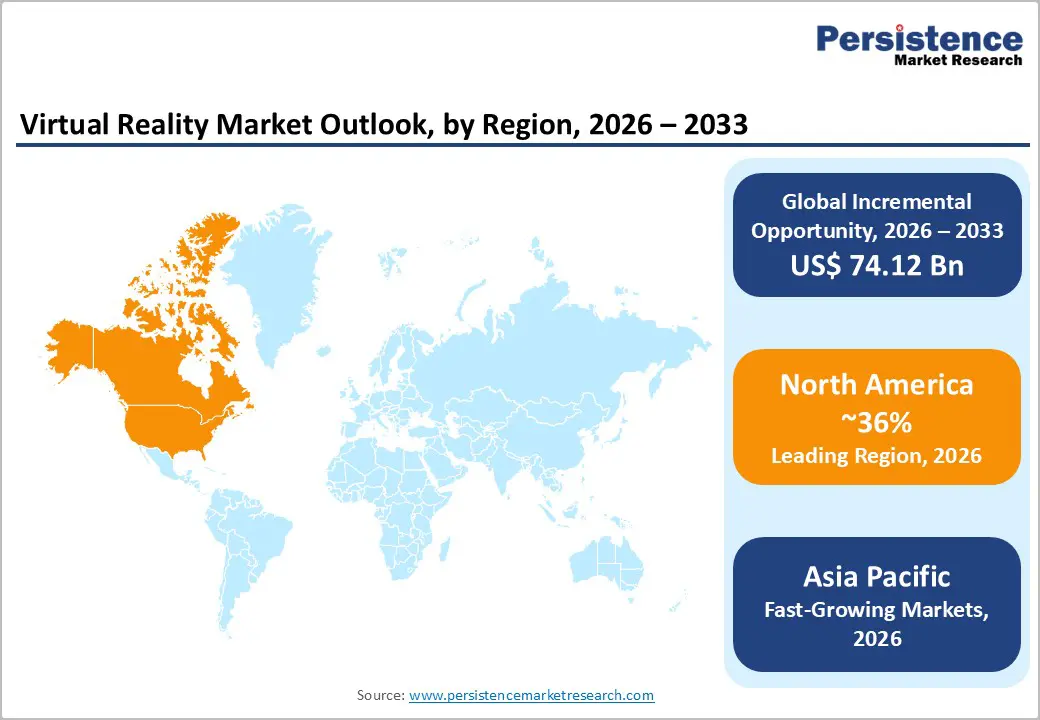

The global Virtual Reality market size is supposed to be valued at US$ 20.0 Bn in 2026 and is projected to reach US$ 94.1 Bn by 2033, growing at a CAGR of 24.8% between 2026 and 2033.

The virtual reality market is experiencing accelerated growth driven by three fundamental factors: rapidly declining hardware costs making VR headsets accessible to mainstream consumers, exponential expansion of immersive content ecosystems across gaming and enterprise applications, and increasing regulatory acceptance, evidenced by FDA approvals for medical devices. These factors collectively reinforce market expansion as price barriers diminish while value propositions strengthen across commercial and consumer segments.

Key Market Highlights

- Regional Leader: North America maintains regional dominance, accounting for approximately 36% of the global virtual reality market value in 2024-2025, driven by concentration of technology innovation, substantial enterprise investment in training applications, and consumer sophistication with advanced computing technologies.

- Fastest Growing Region: Asia-Pacific emerges as the fastest-growing regional market, with projections indicating 40%+ CAGR through 2033, driven by massive consumer populations in China and India, substantial government digital transformation investments, and favorable manufacturing economics enabling competitive hardware pricing.

- Leading Segment: Head-Mounted Displays command dominant segment positioning, capturing approximately 67% market share, reflecting superior immersive experience delivery, technological maturity, and ecosystem development. HMD form factor advantages, including high-resolution displays, sophisticated eye-tracking, and haptic feedback systems, establish this device type as an industry standard.

- Fastest Growing Segment: Gaming Applications represent the fastest-growing segment, with 30.4% CAGR, driven by exceptional consumer entertainment demand, mature content ecosystems, and demonstrated commercial success of titles.

- Key Market Opportunity: Healthcare Expansion represents the largest opportunity, driven by FDA regulatory validation of surgical planning and therapeutic applications, demonstrated clinical efficacy, expanding reimbursement frameworks, and government healthcare modernization initiatives.

| Key Insights | Details |

|---|---|

|

Virtual Reality Market Size (2026E) |

US$ 20.0 Bn |

|

Market Value Forecast (2033F) |

US$ 94.1 Bn |

|

Projected Growth CAGR (2026-2033) |

24.8% |

|

Historical Market Growth (2020-2025) |

15.3% |

Market Dynamics

Market Growth Drivers

Declining Hardware Costs and Improved Accessibility

The virtual reality market is undergoing significant expansion, primarily driven by substantial reductions in hardware costs that have enhanced accessibility for both consumer and enterprise segments. The Meta Quest 3S, priced at approximately US$269.99 for the 128GB model, reflects nearly a 50% decrease from previous flagship devices, signaling a democratization of pricing. This trend aligns with advancements in component manufacturing, notably in Qualcomm Snapdragon XR2 processors and optical systems.

Although cost remains the leading adoption barrier for 27% of organizations, competitive pricing strategies and standalone devices are mitigating this challenge by reducing total ownership costs. Industry forecasts indicate that by 2028, over 5.5 million additional VR headsets will enter circulation, supported by major manufacturers optimizing production efficiency through economies of scale to sustain affordability and market growth.

Enterprise Adoption and Training Standardization

Virtual reality training has evolved from experimental use to a standardized corporate practice, with 39% of enterprises now employing VR/AR technologies for workforce development across diverse skill sets. Organizations report measurable returns on investment through reduced training time, improved knowledge retention, and enhanced operational safety.

Studies indicate VR-trained employees exhibit 275% greater confidence in applying skills compared to traditional methods, while training completion is four times faster. Key examples include Walmart achieving a 70% improvement in test scores and a 30% rise in employee satisfaction, and Boeing reducing training time by 75% through simulation-based programs. Healthcare institutions increasingly adopt FDA-cleared VR surgical simulations, enabling patient-specific procedure rehearsals. This widespread adoption drives sustained demand for hardware, software, and content, positioning VR as a cost-effective, scalable training solution.

Market Restraints

Content Fragmentation and Limited Available Applications

Despite increasing hardware availability, fragmentation within the content ecosystem remains a major barrier to virtual reality adoption, with 27% of organizations citing limited application availability as the primary challenge. The VR landscape is divided across platforms such as Meta Quest, PlayStation VR2, Apple Vision Pro, and Steam VR, each operating proprietary ecosystems with incompatible content libraries. Developers face significant complexity in creating cross-platform applications while ensuring consistent performance and user experience.

The absence of universal development standards necessitates specialized expertise in engines like Unreal and Unity, excluding many smaller enterprises. Additionally, user experience issues persist, with 19% of organizations identifying them as the second-largest obstacle. Motion sickness and latency-related discomfort affect 25–40% of users, while premium solutions like Apple Vision Pro exceed US$3,500, limiting mass-market adoption and perpetuating ecosystem fragmentation.

Infrastructure Requirements and Skills Gaps

Implementation of robust virtual reality ecosystems demands sophisticated infrastructure and specialized technical expertise that many organizations, particularly in emerging markets, currently lack. Standalone headsets partially address infrastructure limitations, yet cutting-edge applications still require powerful computing resources, high-speed networking (5G and 6G), and substantial development capital. Educational institutions face notable adoption hurdles, with over 60% of educators in the Asia-Pacific lacking the skills to create and implement VR content.

Budgetary constraints further limit adoption among small-to-medium enterprises and schools, as quality VR devices typically cost between US$500 and US$1,000. Furthermore, regulatory complexity surrounding VR in healthcare creates implementation friction, as medical institutions must navigate FDA approval processes, data privacy requirements under HIPAA, and integration with existing electronic health record systems. This combination of capital requirements, skills deficiencies, and regulatory complexity creates disproportionate burdens on smaller organizations, limiting market penetration in segments with lower technical sophistication.

Market Opportunities

Healthcare and Surgical Training Revolution

The healthcare sector is emerging as one of the most dynamic growth areas for virtual reality, driven by regulatory validation and proven clinical benefits. FDA clearance for VR surgical planning solutions, such as AVATAR MEDICAL Vision and Realize Medical Elucis, has established a regulatory framework legitimizing immersive technologies for clinical use. Surgical simulations enable patient-specific procedure planning using CT/MRI-based anatomical models, reducing operative time, complications, and costs.

FDA-approved VR therapies, including EaseVRx for chronic pain, have created reimbursement pathways, reinforcing economic viability. Medical training applications demonstrate exceptional value propositions, with VR-trained physicians making 6 times fewer errors during surgical procedures compared to traditionally trained counterparts. Hospitals increasingly adopt VR training, which reduces errors and improves patient outcomes, positioning immersive technology as a transformative force in healthcare.

Education and Immersive Learning Platform Development

Educational technology has emerged as the fastest-growing application area for virtual reality, fueled by its proven ability to enhance learning outcomes and deliver cost efficiency at scale. The VR education market is expected to grow sixfold, underscoring its strong growth trajectory. Studies reveal that VR-based training improves learning effectiveness by 76% compared to traditional methods, with 75–80% of learners retaining knowledge for over a year, far surpassing conventional classroom retention rates. In 2024, the UK witnessed a 35% surge in VR adoption within education, driven by the availability of affordable headsets for schools.

Content creation has become increasingly accessible through platforms like Unity and Unreal Engine, enabling educators to design interactive learning experiences. The combination of enhanced pedagogy, affordability, and improved student engagement presents significant market opportunities. Particularly promising are hybrid learning models that integrate immersive VR training with traditional teaching, delivering richer educational experiences while optimizing resources.

Category-wise Insights

Device Type Analysis

Head-Mounted Displays (HMDs) dominate the Device Type category, accounting for an estimated 67% market share in 2026. This leadership is driven by their superior ability to deliver immersive experiences and by ongoing technological advancements. Leading products such as Meta Quest 3S, PlayStation VR2, Apple Vision Pro, and Sony’s offerings represent the most advanced form factors, featuring ultra-high-resolution displays (exceeding 2000 × 2040 pixels), sophisticated eye-tracking, and haptic feedback systems. Continuous R&D investments from major tech players fuel improvements in resolution, field of view, refresh rates, and overall user comfort.

Gesture Tracking Devices are emerging as a complementary subcategory, increasingly integrated into HMDs to enable intuitive hand-based interactions without controllers, appealing to both enterprise and casual users. In contrast, Projected & Display Walls remain niche solutions, primarily used for professional visualization in architecture, engineering, and design, where collaborative spatial experiences justify the infrastructure cost.

Technology Type Analysis

Semi-immersive and fully-immersive technologies accounted for nearly 83% of market value in 2026 and are expected to maintain dominance throughout the forecast period. Fully-immersive solutions, offering complete visual and auditory isolation, deliver the highest level of presence and emotional engagement, making them the preferred choice for gaming, entertainment, and advanced training applications. Semi-immersive systems, which partially replace the real environment, cater to practical enterprise needs such as design visualization, remote collaboration, and specialized training without requiring full sensory isolation.

Advancements such as 5G connectivity, haptic feedback, and eye-tracking further elevate fully-immersive experiences, reinforcing investment in next-generation platforms. Leading products like Meta Quest, PlayStation VR2, and Apple Vision Pro exemplify this evolution, emphasizing immersion as a key competitive differentiator.

Application Analysis

Gaming is the leading application segment in the virtual reality market, with 48% of the market share, driven by strong consumer demand for immersive entertainment and robust content ecosystems. Valued at US$12.32 billion in 2026, the VR Gaming Accessories Market is projected to reach US$33.58 billion by 2032, reflecting a 15.4% CAGR. This growth is supported by widespread adoption through platforms such as Steam, Meta Quest Store, and PlayStation Network, alongside consumer willingness to invest in advanced hardware and premium content.

Popular titles like Beat Saber, Horizon: Call of the Mountain, and Tetris Effect VR exemplify commercial success. Beyond gaming, emerging applications include e-learning, surgical training, and vehicle simulation, while location-based entertainment venues in urban areas provide additional revenue streams and enhance consumer engagement.

End-use Industry Analysis

The Media & Entertainment sector currently leads the virtual reality market, with 45% market share, driven by strong consumer demand for immersive experiences and widespread hardware adoption. Gaming, film production, and live entertainment companies generate significant revenue through content creation, distribution, and integration with family and indoor entertainment centers.

Healthcare is the fastest-growing vertical, supported by FDA regulatory approvals, proven clinical benefits in surgical training and therapeutic applications, and expanding reimbursement frameworks. Aerospace and Defense applications include pilot training, combat simulation, equipment maintenance, and mission planning, with substantial government procurement fueling growth. Education adoption is accelerating through public school initiatives, university collaborations, and corporate training programs.

Regional Insights

North America Virtual Reality Trends

North America remains the largest regional market for virtual reality, representing nearly 36% of the global market value. This leadership is driven by a strong concentration of technology innovation, significant enterprise investment in immersive applications, and high consumer adoption supported by advanced computing infrastructure. The U.S. dominates the region through major technology companies such as Meta Platforms Inc., Apple Inc., Microsoft Corporation, and Google Inc., which allocate substantial resources to VR research and development.

Government procurement further accelerates adoption, particularly in defense and aerospace, with VR utilized for military simulations, pilot training, and equipment maintenance. Healthcare leads global adoption in North America, supported by FDA regulatory frameworks and reimbursement pathways. Additionally, widespread enterprise training initiatives and 5G-enabled cloud streaming expand market reach, complemented by robust entertainment infrastructure and location-based VR experiences.

Europe Virtual Reality Trends

Europe ranks as the second-largest regional market for virtual reality, with notable strength in Germany, the U.K., France, and Spain. The region’s leadership in industrial applications reflects advanced manufacturing capabilities and significant automation investments, with automotive leaders such as Volkswagen Group and BMW leveraging VR for design visualization, production training, and quality assurance.

Regulatory frameworks, including GDPR and Medical Device Regulation, establish compliance standards that enhance trust in sensitive applications. Healthcare modernization initiatives support VR-based surgical training, while education adoption surpasses global averages, driven by government-backed digital transformation programs. Additionally, European startups like Varjo Technologies and XREAL foster innovation, complementing efforts by major technology companies.

Asia-Pacific Virtual Reality Trends

Asia-Pacific is positioned as the fastest-growing regional market for virtual reality, projected to capture over 40% of the global market value by 2033. China leads the region with its vast consumer base, significant government investments in digital transformation, and strong technology competitiveness. Metaverse policies and smart city initiatives further accelerate VR adoption across consumer and enterprise segments.

Japan’s technological leadership and cultural affinity for gaming foster vibrant VR entertainment markets, particularly through arcade-based location-based experiences. South Korea demonstrates high adoption driven by gaming culture, advanced internet infrastructure, and hardware innovation from companies such as Samsung Electronics. India offers exceptional growth potential, supported by a young population, expanding digital infrastructure, and educational modernization.

Competitive Landscape

Market Structure Analysis

The virtual reality market demonstrates moderate consolidation, with dominant positions held by major platform providers alongside significant fragmentation among specialized developers and content creators. Leading companies, Meta Platforms Inc., Sony Corporation, Apple Inc., Microsoft Corporation, and Google Inc., exert strong influence through platform control, extensive content ecosystems, and large installed user bases. These firms leverage advantages such as developer access, authentication systems, and integrated payment solutions, creating competitive moats. Consolidation trends include vertical integration and proprietary ecosystems, while emerging players differentiate through niche technologies.

Key Market Developments

December 2025: Meta Platforms Inc. announced suspension of Horizon OS third-party hardware partnerships, halting planned Asus gaming headset and Lenovo productivity device releases, refocusing on first-party development. This strategic reversal represents a significant market shift with implications for ecosystem fragmentation and Android XR competitive positioning.

September 2025: U.S. Army procurement of Anduril Industries' helmet-mounted mixed reality system under the Soldier Borne Mission Command program demonstrates government embrace of immersive defense technologies, expanding Aerospace & Defense market opportunities, and validating VR hardware for military applications.

November 2025: Sony dropped PlayStation VR2 pricing to US$ 299 during Black Friday promotions, demonstrating price-elasticity sensitivity and competitive pressure from Meta Quest 3S at US$ 249, driving volumes and market penetration into mainstream consumer segments.

Top Companies in the Virtual Reality Market

Meta Platforms Inc. (Menlo Park, California, U.S.) commands global market leadership through the Meta Quest product line spanning 3S, 3, and professional variants, representing the most accessible consumer VR platform with extensive content ecosystem. Meta leverages advertising and platform integration advantages while investing substantially in Reality Labs research, though the division reportedly generates annual losses exceeding US$ 4 billion. Meta's focus on mixed reality and spatial computing positions it competitively across gaming, social, and enterprise applications.

Sony Corporation (Tokyo, Japan) maintains premium positioning through the PlayStation VR2 headset optimized for console gaming, leveraging exclusive game development partnerships creating proprietary competitive advantages. Sony's OLED display technology and haptic controller innovations establish technical differentiation while PlayStation ecosystem strength ensures sustained content development. Sony's focus on high-end gaming experiences targets an affluent demographic willing to invest US$ 599.99-749.99 for exceptional immersive entertainment.

Apple Inc. (Cupertino, California, U.S.) entered the VR/MR market through Vision Pro, a premium US$ 3,500 device targeting professional and affluent consumers, emphasizing spatial computing for productivity, creativity, and entertainment. Apple's vertical integration of M2 and R1 processors, operating system, and application ecosystem creates ecosystem lock-in, while Apple's retail presence and brand prestige support premium positioning despite limited market penetration relative to competitors.

Companies Covered in Virtual Reality Market

- Meta Platforms Inc.

- Sony Corporation

- Apple Inc.

- Microsoft Corporation

- Google Inc.

- Samsung Electronics

- HTC Corporation

- Unity Technologies Inc.

- Barco

- Penumbra Inc.

- Lumus Ltd

- Valve Corporation

- Lenovo Group Ltd

- Qualcomm Inc.

Frequently Asked Questions

The global Virtual Reality market is projected to reach US$ 94.1 billion by 2033, growing from US$ 20.0 billion in 2026 at a CAGR of 24.8%, driven by expanding hardware accessibility, enterprise adoption of training applications, and healthcare regulatory validation supporting clinical applications.

Virtual Reality market expansion is propelled by three principal factors: hardware cost reduction with entry-level HMDs now available at US$ 269.99-399.99, increasing mainstream accessibility, enterprise standardization of VR training with 39% of enterprises adopting immersive solutions, and healthcare regulatory validation through FDA approvals, creating reimbursement pathways supporting clinical adoption.

Gaming represents the largest application segment with 30.4% CAGR, capturing substantial market share through consumer entertainment demand and established content ecosystems, including exclusive titles like Horizon: Call of the Mountain and Beat Saber.

North America maintains regional market leadership, commanding approximately 36% of global market value, driven by technology innovation concentration, enterprise training investment, and substantial defense sector procurement supporting aerospace and military applications through companies like Meta Platforms Inc., Apple Inc., and Microsoft Corporation.

Healthcare expansion constitutes the largest emerging opportunity, driven by FDA regulatory validation of VR surgical planning solutions, demonstrated clinical efficacy reducing surgical complications, and expanding reimbursement frameworks.

Leading companies include Meta Platforms Inc., commanding market share through the Meta Quest ecosystem, Sony Corporation, maintaining premium positioning via PlayStation VR2, Apple Inc. targeting affluent segments through Vision Pro, Microsoft Corporation pursuing enterprise applications, and Google Inc. developing the Android XR platform supporting multiple hardware partners, including Samsung Electronics and XREAL.