- Communication Infrastructure & Services

- U.S. Factoring Services Market

U.S. Factoring Services Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Factoring Services Market by Category (Domestic, International), Service Type (Recourse, Non-Recourse), Financial Institutions (Banks, Non-Banking), Enterprise Size (Small & Medium Enterprises, Large Enterprises), Industry (Transport & Logistics, Manufacturing, Healthcare, Information Technology, Construction, Others), and Regional Analysis for 2026 - 2033

U.S. Factoring Services Market Size and Trend Analysis

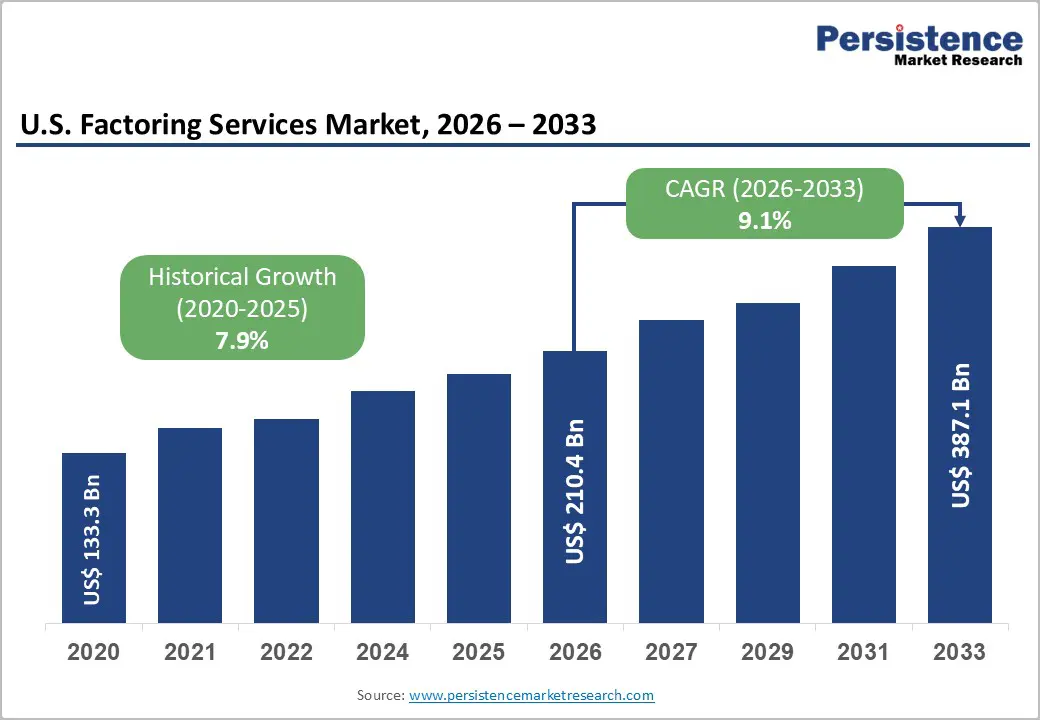

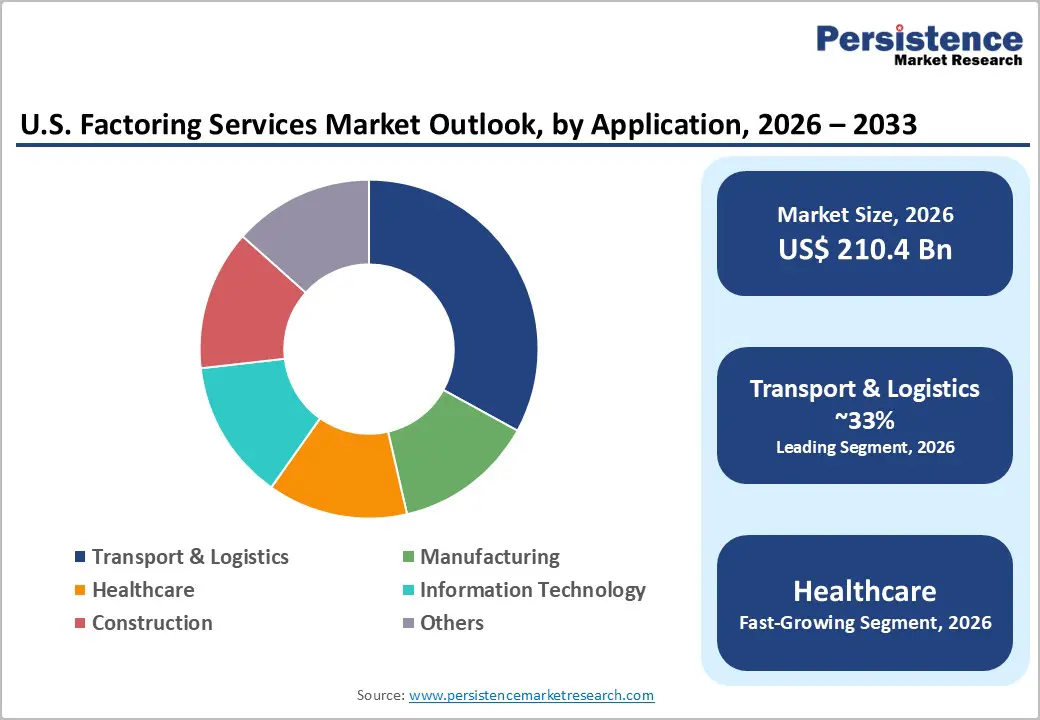

The U.S. factoring services market size is valued at US$ 210.4 Bn in 2026 and is projected to reach US$ 387.1 Bn by 2033, growing at a CAGR of 9.1% between 2026 and 2033.

The market is experiencing robust growth driven by mounting demand for alternative working-capital solutions among Small and Medium Enterprises (SMEs) that face persistent credit barriers from traditional banks. Rising adoption of Artificial Intelligence (AI), Machine Learning (ML), and blockchain-enabled Distributed Ledger Technology (DLT) is compressing approval cycles, broadening receivables eligibility, and strengthening fraud controls. Concurrently, the expansion of domestic e-invoicing infrastructure and the deepening of cross-border open-account trade are widening the addressable customer base for factoring providers across the United States.

Key Market Highlights

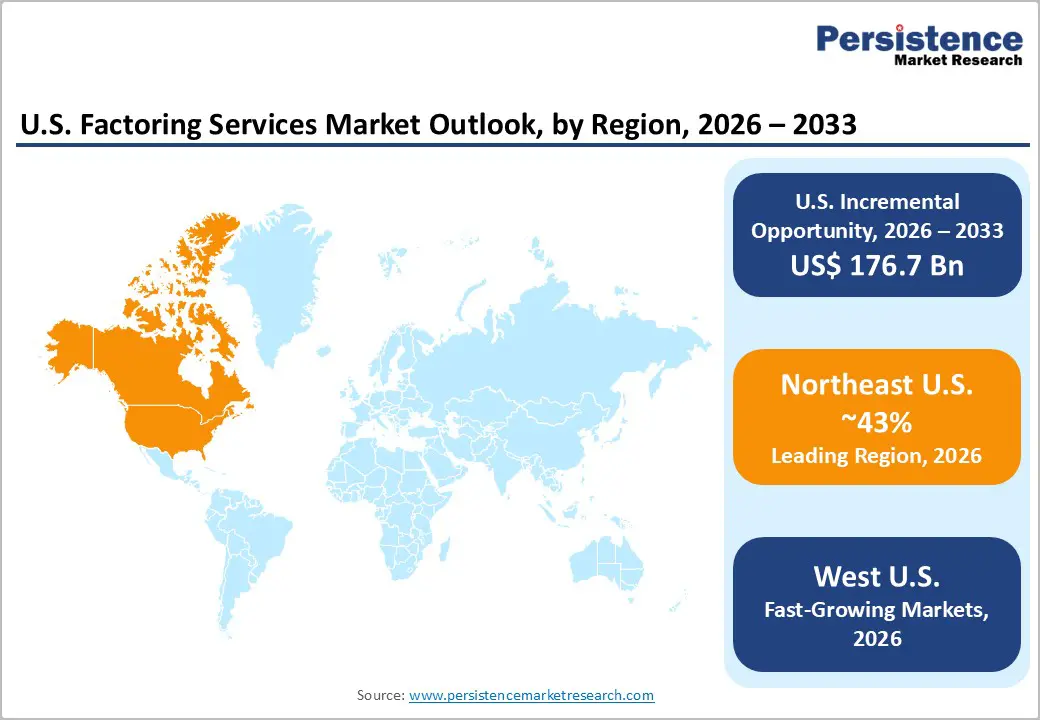

- Regional Leader: The Northeast U.S., anchored by New York City's concentration of bank-owned factors, including Wells Fargo, JPMorgan Chase, and BNP Paribas, maintains its position as the highest-service factoring region, supported by a mature legal framework and deep capital access.

- Fastest Growing Region: The Western U.S. is expanding at a projected CAGR of 9.4%, driven by California's 4.2 million SMEs, booming e-commerce volumes, and fintech innovation hubs in San Francisco and Seattle pioneering AI-first factoring platforms.

- Leading Segment: Transportation and logistics holds the largest end-use share of approximately 33%, as chronic 30- to 90-day freight-broker payment lags make same-day factoring advances structurally essential for over 3.5 million U.S. trucking operators.

- Fastest Growing Segment: Non-recourse factoring is expanding at the highest CAGR of approximately 9.9%, driven by healthcare providers seeking full credit-risk transfer against complex Medicare and Medicaid reimbursement cycles.

- Key Market Opportunity: Cross-border open-account trade exceeding US$ 7.0 trillion annually creates a compelling opportunity for fintech-driven international factoring platforms, supported by FCI's Two-Factor System, which connects factors across 90+ countries.

| Key Insights | Details |

|---|---|

|

U.S. Factoring Services Market Size (2026E) |

US$ 210.4 Bn |

|

Market Value Forecast (2033F) |

US$ 387.1 Bn |

|

Projected Growth CAGR (2026–2033) |

9.1% |

|

Historical Market Growth (2020–2025) |

7.9% |

Market Dynamics

Drivers - Persistent Credit Gap for SMEs Driving Factoring Adoption

The structural financing gap confronting Small and Medium Enterprises (SMEs) remains the principal force driving growth in the U.S. factoring services market. A Dallas Federal Reserve survey of 71 banking institutions conducted in March 2023 indicates that the Federal Reserve’s aggressive rate-hike cycle, raising the prime rate from 3.5% to 8.5% between April 2022 and July 2023, tightened credit standards and increased collateral and credit-score requirements.

Consequently, many SMEs have shifted toward receivables-based financing. Unlike traditional bank lending, factoring evaluates the quality of invoices rather than the borrower’s balance sheet, making it particularly suitable for firms with limited credit histories or variable cash flows. The U.S. Small Business Administration reports that over 33 million SMEs operate nationally, most with receivables cycles of 30 to 90 days, generating a consistent supply of factorable assets.

Digital Transformation and AI-Driven Platforms Streamlining Factoring Workflows

Technological advancement is fundamentally reshaping the U.S. factoring landscape. The integration of Artificial Intelligence (AI), Natural Language Processing (NLP), and blockchain-based Distributed Ledger Technology (DLT) into factoring platforms is reducing invoice approval times from days to hours, enhancing fraud detection, and enabling automated credit scoring at scale. Walmart Inc., one of the country's largest retailers, has already deployed blockchain DLT to track and verify product and payment information across its supply chain, underscoring the enterprise-level credibility of these tools.

According to Factors Chain International (FCI), the global representative body for the factoring industry, cumulative global factoring service reached approximately €3,894 billion in 2024, with digital-first markets recording the sharpest growth rates. Within the United States, the proliferation of SaaS-embedded factoring APIs is enabling SMEs to unlock same-day liquidity directly through their accounting platforms, materially widening market penetration.

Restraints - High Service Costs Limiting Adoption Among Micro-Enterprises

A key restraint on the broader adoption of factoring services in the United States is the product's comparatively high cost structure. A typical factoring fee ranges between 1.5% and 5% of invoice value per month, significantly higher than interest on a conventional bank line of credit. For micro-enterprises with thin margins, this cost differential can erode profitability.

The Federal Reserve's 2023 Small Business Credit Survey found that nearly 43% of small firms cited financing costs as the primary deterrent to seeking external working capital. This cost sensitivity constrains the addressable market for factoring providers, particularly in low-margin sectors such as retail and food service.

Regulatory Complexity and Absence of a Unified Federal Framework

Unlike banking activities, which are governed by a consolidated federal supervisory framework, invoice factoring in the United States operates under a patchwork of state-level Uniform Commercial Code (UCC) regulations, creating compliance complexity for factors operating across multiple states. The absence of a single federal regulatory body specifically governing factoring transactions adds legal overhead, particularly for international factoring engagements requiring coordination with foreign jurisdictions.

According to FCI's Annual Review, the U.S. accounts for only approximately 3-4% of global FCI-member factoring services, a remarkably low share for the world's largest economy, partly attributable to regulatory fragmentation that deters cross-border standardization.

Opportunities - Non-Recourse Factoring Expansion in Healthcare Receivables

The healthcare sector represents one of the most compelling growth opportunities in the U.S. factoring market. Healthcare providers, hospitals, physician groups, and home-care agencies routinely face payment cycles of 60 to 120 days due to the complexity of insurance reimbursement and Medicare and Medicaid billing processes. Non-recourse factoring, which transfers full credit risk to the factor, is emerging as the preferred structure for healthcare clients seeking protection against insurer denials and delayed settlements.

The Centers for Medicare & Medicaid Services (CMS) reported that U.S. national health expenditure reached US$ 4.9 trillion in 2023, with a growing share flowing through complex multi-payer billing architectures. Factors deploying AI-driven revenue cycle analytics, including automated denial management and payer behavior modeling, are uniquely positioned to capture this high-value vertical, which is projected to register the highest end-use CAGR in the market through 2033.

Fintech-Led International Factoring as Cross-Border Trade Accelerates

The rapid growth of cross-border open-account trade presents a structural opportunity for fintech-driven international factoring platforms in the United States. According to the U.S. Census Bureau, U.S. goods and services trade totaled over US$ 7.0 trillion in 2023, with a significant and growing share settled on open-account terms, the primary condition necessitating factoring. As Chinese manufacturers increasingly relocate production to countries in Latin America and Southeast Asia to navigate ongoing trade tensions, U.S.-based importers are seeking more agile receivables management tools.

FCI's Two-Factor System, which connects export and import factors across 90+ countries, provides a ready network infrastructure for U.S. factors to scale internationally. Non-banking financial institutions and fintech players, unburdened by legacy systems, are best positioned to capitalize on this opportunity through digital onboarding and real-time cross-currency settlement capabilities.

Category-wise Insights

By Category Type

The domestic segment is the leading category in the U.S. factoring services market, accounting for approximately 77% of total market share. This dominance is rooted in the well-established Uniform Commercial Code (UCC) public registry infrastructure, which enables factors to track and verify invoice ownership with a level of transparency that most countries lack. The widespread adoption of electronic invoicing (e-invoicing) across U.S. industries, actively promoted by the U.S. Treasury's Bureau of the Fiscal Service, further accelerates receivables monetization by reducing processing delays.

SME-heavy sectors such as staffing, transportation, and manufacturing generate high volumes of short-tenure domestic receivables, providing a recurring pipeline of factorable assets. As digital onboarding reduces the cost per account, domestic-focused independent factors and bank-owned arms alike are deepening SME penetration, reinforcing the segment's majority share through the forecast period to 2033.

By Service Type

The recourse factoring segment holds the dominant position in the U.S. market, accounting for approximately 77% of total revenues. In recourse structures, the client retains liability in the event of debtor default, enabling factors to charge lower fees, typically 0.5 to 1.5 percentage points below non-recourse equivalents, while maintaining tighter risk controls. This cost advantage drives adoption among established SMEs with reliable debtor bases, particularly in transportation and manufacturing.

The Commercial Finance Association (CFA), now known as the Secured Finance Network (SFNet), reports that recourse structures account for the majority of invoice financing transactions in North America. However, the non-recourse segment is expanding at the highest CAGR of approximately 9.9%, driven by economic uncertainty and growing demand, particularly in healthcare, for full credit-risk transfer.

By Financial Institutions

Bank-owned factors dominate the financial institutions segment, accounting for approximately 63% of market revenue, underpinned by their access to low-cost capital, established client relationships, and regulatory credibility. Leading banks such as Wells Fargo Capital Finance, JPMorgan Chase, and PNC Financial Services leverage their extensive branch networks and treasury management platforms to bundle factoring within broader working-capital solutions.

The adoption of blockchain DLT by several major U.S. banks is further enhancing the transparency and audit integrity of receivables portfolios. Non-banking financial institutions (NBFIs), however, are expected to record the highest segment CAGR of approximately 11.9%, driven by fintech-native players offering faster approvals, no minimum volume requirements, and industry-specialized risk models that traditional banks are structurally slower to develop.

By Enterprise Size

Small and Medium Enterprises (SMEs) represent the dominant enterprise-size segment, capturing approximately 68% of the U.S. factoring market service in 2025. According to the U.S. Small Business Administration (SBA), SMEs account for approximately 44% of U.S. economic activity and generate enormous amounts of trade receivables. The structural inability of many SMEs, particularly minority-owned and early-stage businesses, to satisfy collateral requirements for traditional bank credit makes factoring not merely an alternative but often a primary source of operational liquidity.

Mobile-based digital Know Your Customer (KYC) and AI-powered invoice verification are reducing onboarding friction, enabling factors to profitably serve ticket sizes as small as US$ 5,000. As embedded factoring modules are increasingly integrated into popular SME accounting platforms, penetration within this segment is expected to deepen further through the forecast period.

By Industry

The transport and logistics vertical leads Industry demand, accounting for approximately 33% of total factoring revenue. Freight carriers and trucking operators routinely face broker payment cycles of 30 to 90 days against immediate fuel, driver payroll, and maintenance obligations, a mismatch that makes same-day invoice advances structurally indispensable. According to the American Trucking Associations (ATA), the U.S. trucking industry moves approximately 72.6% of all domestic freight, generating a vast amount of factorable receivables.

Industry-specialist factors such as Triumph Financial, Inc. and RTS Financial Services, Inc. have built proprietary freight-bill collection and fuel-advance ecosystems that deepen wallet share and lower churn. Healthcare is projected to register the highest end-use CAGR, given the complexity and amount of insurer reimbursement cycles under Medicare and Medicaid billing frameworks.

Regional Insights

The U.S. factoring services market exhibits a moderately consolidated structure at the top tier, dominated by large bank-owned factors and a cohort of well-capitalized independent specialists, alongside an increasingly disruptive fintech fringe. Leading institutions such as Wells Fargo Capital Finance, JPMorgan Chase, and CIT Group Inc. compete primarily on cost of capital, client relationship depth, and technology investment. Independent factors differentiate through industry specialization, notably in transportation, healthcare, and staffing, while fintech entrants leverage AI-driven onboarding and API-first platforms to capture underserved SME segments. Strategic M&A, white-label partnerships, and embedded finance integrations are the dominant growth vectors, compressing the field and raising the minimum viable scale for profitable factoring operations.

Key Developments:

- July 2025: Wells Fargo expanded its Commercial Services Group to deepen receivables financing capabilities across manufacturing and healthcare verticals, integrating blockchain-based DLT for invoice verification to enhance audit traceability. The bank remains the leading U.S. bank-owned factor by portfolio volume, providing trade finance and asset-based lending at scale.

- February 2025: JPMorgan Chase launched Wire 365, an always-on wire transfer and settlement service that operates every calendar day of the year, removing traditional banking cut-off barriers and enabling continuous receivables settlement for factoring clients, particularly benefiting e-commerce marketplace sellers with embedded working-capital solutions.

- December 2024: CIT Group's commercial lending division, operating under First Citizens Bank following the 2022 acquisition, announced a strategic partnership with blockchain fintech providers to enhance transparency, security, and audit traceability across its domestic and international factoring receivables portfolios, aligning with industry-wide DLT adoption trends.

Top Companies in U.S. Factoring Services

Wells Fargo Capital Finance (San Francisco, U.S.) is the largest bank-owned factor in the United States, operating through its Commercial Services Group to deliver trade finance, accounts receivable management, and asset-based lending across manufacturing, retail, healthcare, and transportation. With a balance sheet exceeding US$ 1.7 trillion, Wells Fargo leverages unrivaled capital access and a national branch network to provide cost-competitive factoring solutions, recently appointing specialized leadership to accelerate growth in specialty asset-based lending and factoring.

JPMorgan Chase Bank (New York, U.S.) operates one of the most extensive trade finance and supply chain financing platforms globally, with dedicated factoring capabilities embedded within its Commercial Banking and Global Corporate Banking divisions. The bank's proprietary Liink (formerly Interbank Information Network) blockchain platform and its J.P. Morgan Payments infrastructure provide seamless integration between invoice processing, receivables financing, and cross-border settlement, differentiating its factoring offer for large corporates and fast-scaling mid-market companies.

Triumph Financial, Inc. (Dallas, U.S.) is the leading independent factor specializing exclusively in the transportation and freight sector. Its TriumphPay platform processes billions of dollars in annual freight payments, connecting brokers, carriers, and shippers in a closed-loop factoring and payments network with embedded fuel-card benefits. As a Nasdaq-listed company trading under TBK, Triumph's deep sector expertise, proprietary data assets, and broker relationship network give it a structural moat that generalist bank-owned factors find difficult to replicate in freight-specific receivables financing.

Companies Covered in U.S. Factoring Services Market

- Wells Fargo Capital Finance

- JPMorgan Chase Bank

- CIT Group Inc.

- PNC Financial Services

- HSBC Group

- BNP Paribas

- Bank of America Merrill Lynch

- Sterling National Bank

- Triumph Financial, Inc.

- RTS Financial Services, Inc.

- Riviera Finance of Texas, Inc.

- TCI Business Capital

- Hitachi Capital America Corp.

- Bibby Financial Services, Inc.

Frequently Asked Questions

The U.S. factoring services market is valued at US$ 210.4 Bn in 2026 and is projected to reach US$ 387.1 Bn by 2033, growing at a CAGR of 9.1%. Historically, the market grew at a CAGR of 7.9% between 2020 and 2025, driven by rising alternative finance demand from SMEs and digital platform adoption.

The most significant growth driver is the persistent financing gap for Small and Medium Enterprises (SMEs), compounded by the Federal Reserve's aggressive rate-hike cycle between 2022 and 2023, which curtailed traditional bank credit availability and redirected over 33 million U.S. SMEs toward receivables-based financing solutions. Digital platform innovation and AI-driven credit analytics are further amplifying this structural shift.

The Northeast U.S. leads the regional market, anchored by New York City's unparalleled concentration of bank-owned factors, including Wells Fargo Capital Finance, JPMorgan Chase, BNP Paribas, and HSBC Group. The region's mature New York State Department of Financial Services (NYDFS) regulatory framework, deep capital markets, and high density of B2B invoice-generating industries collectively reinforce its market leadership.

The expansion of fintech-driven international factoring represents the most compelling market opportunity, as U.S. goods and services trade exceeded US$ 7.0 trillion in 2023 with a growing share settled on open-account terms. Combined with the healthcare sector's need for non-recourse receivables finance against complex CMS reimbursement cycles, where national health expenditure reached US$ 4.9 trillion in 2023, these two verticals offer exceptional growth potential for specialized factoring providers.

Key market players include Wells Fargo Capital Finance, JPMorgan Chase Bank, CIT Group Inc., PNC Financial Services, HSBC Group, BNP Paribas, Triumph Financial, Inc., RTS Financial Services, Inc., Riviera Finance of Texas, Inc., TCI Business Capital, Bibby Financial Services, Inc., and Hitachi Capital America Corp., among others.