- Pharmaceuticals

- Urinary Incontinence Therapeutics Market

Urinary Incontinence Therapeutics Market Size, Share and Growth Forecast, 2026-2033

Urinary Incontinence Therapeutics Market by Therapy Type (Urge Incontinence, Overflow Incontinence, Others), Drug Class (Anticholinergics, Beta-3 Adrenoceptor Agonists, Others), End-user (Hospitals, Retail Pharmacy, & Online Pharmacy), and Regional Analysis for 2026 - 2033

Urinary Incontinence Therapeutics Market Share and Trends Analysis

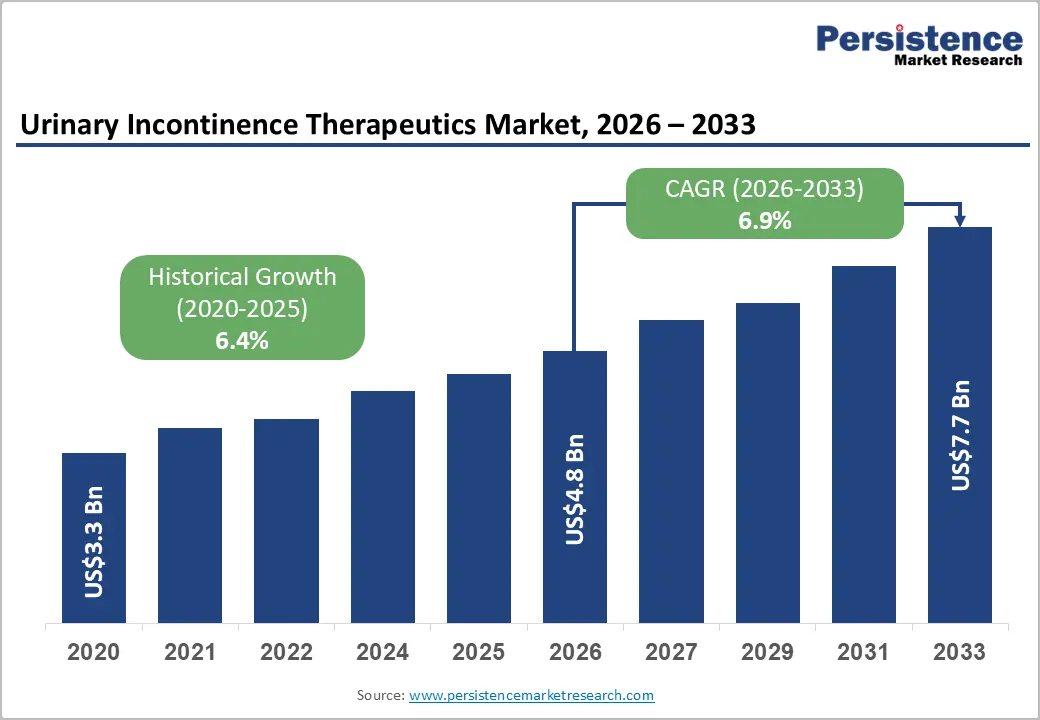

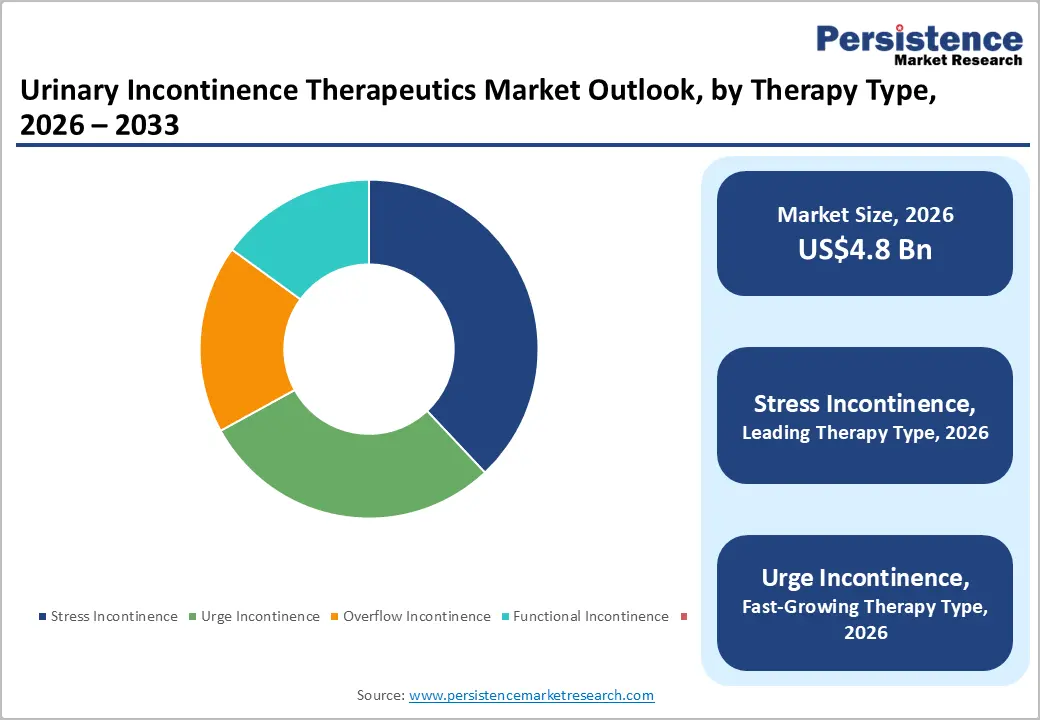

The global urinary incontinence therapeutics market size is likely to be valued at US$4.8 billion in 2026 and is projected to reach US$7.7 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by the rising prevalence of overactive bladder disorders, expanding geriatric populations, and increasing diagnosis rates among women. Continued innovation in urology therapeutics, particularly beta-3 adrenoceptor agonists and combination therapies, is improving treatment outcomes. Greater awareness, enhanced bladder health management programs, and broader access to specialty urology care are further supporting market growth.

Key Industry Highlights:

- Dominant Therapy Type: Stress incontinence is expected to lead with approximately 38% market share in 2026, while urge incontinence is projected to be the fastest-growing segment through 2033, driven by rising overactive bladder prevalence and growing treatment adoption.

- Leading Drug Class: Anticholinergics are anticipated to dominate with nearly a 34% share in 2026, while beta-3 adrenoceptor agonists are likely to witness the fastest growth during 2026–2033, supported by favorable efficacy and safety profiles.

- Dominant End-user: Hospitals are expected to account for around 46% of revenue in 2026, while online pharmacies are projected to be the fastest-growing channel through 2033, reflecting increasing digital healthcare adoption.

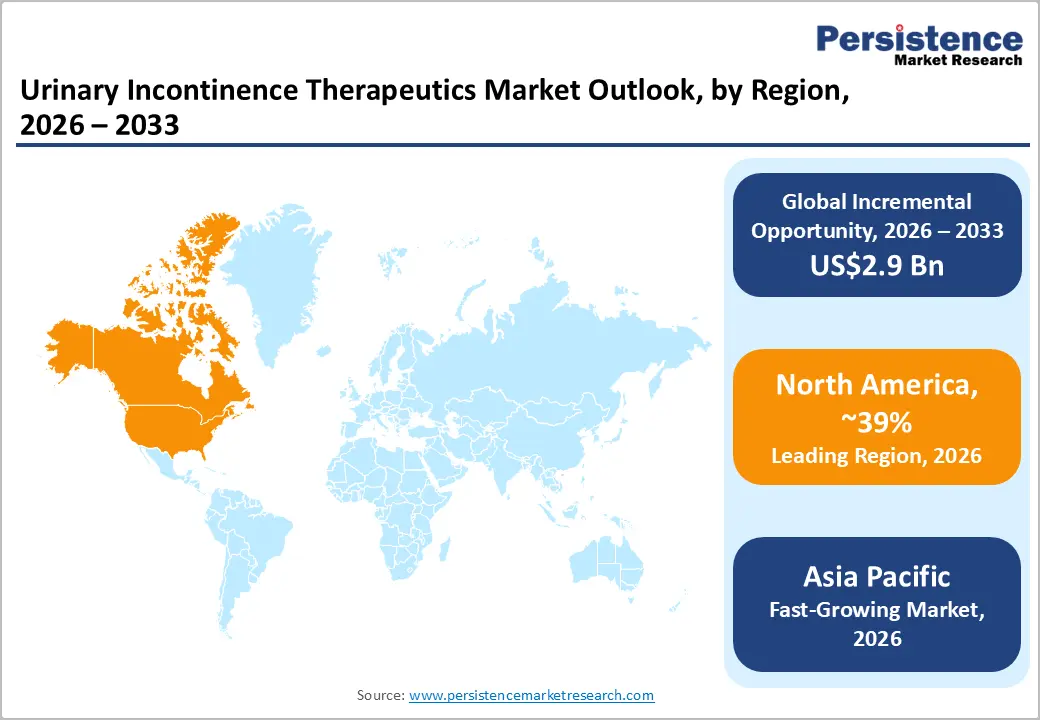

- Regional Leadership: North America is poised to lead with approximately 39% market share in 2026, supported by high healthcare spending, strong reimbursement coverage, and continued therapeutic innovation.

- Competitive Environment: Competitive activity is centered on novel overactive bladder therapies, geographic expansion, and combination drug development, with advancements in vibegron commercialization and clinical research.

DRO Analysis

Driver - Growing Aging Population and Rising Prevalence of Overactive Bladder Disorders

The most significant driver for the urinary incontinence therapeutics market is the rapid increase in elderly populations globally. According to the United Nations Department of Economic and Social Affairs (UN DESA), individuals aged 65 years and above are expected to exceed 1.6 billion by 2050. Clinical evidence published by the International Continence Society (ICS) indicates that urinary incontinence affects nearly 30%–40% of women and approximately 11%–34% of men over the age of 60.

Age-related weakening of pelvic floor muscles, neurological disorders, diabetes, and benign prostatic hyperplasia substantially increase disease incidence. As healthcare systems improve screening and diagnosis, treatment adoption continues to rise. Pharmaceutical manufacturers are benefiting from expanding patient pools requiring long-term pharmacological management, creating sustained demand for overactive bladder drugs, urge incontinence therapies, and innovative urology treatments.

Restraint - Limited Treatment Adherence and Adverse Effects Associated with Conventional Drug Therapies

Despite increasing diagnosis rates, long-term treatment adherence remains a major challenge across the urinary incontinence drugs market. Anticholinergic medications, which account for a substantial portion of prescriptions, are associated with dry mouth, constipation, blurred vision, dizziness, and cognitive side effects in elderly patients. Research published by the American Urological Association shows significant discontinuation rates within the first year of therapy among overactive bladder patients.

Additionally, concerns regarding potential cognitive decline linked to prolonged anticholinergic exposure have encouraged physicians to adopt more conservative prescribing practices. Reimbursement limitations in developing economies and the relatively high cost of newer beta-3 adrenoceptor agonists further restrict accessibility. These structural barriers continue to limit treatment penetration, particularly among cost-sensitive patient populations.

Opportunity - Expansion of Advanced Pharmacological Therapies across Emerging Markets

A major opportunity exists in emerging healthcare markets where diagnosis and treatment rates remain substantially below developed-country levels. Countries including China, India, Indonesia, Brazil, and Mexico are witnessing improvements in healthcare infrastructure, insurance coverage, and urology specialization. The World Health Organization highlights that aging demographics in Asia Pacific are accelerating demand for chronic disease management, including bladder dysfunction treatment.

Pharmaceutical companies are increasingly targeting these regions through local partnerships, distribution agreements, and regulatory expansion initiatives. The growing availability of beta-3 agonists, combination therapies, and telehealth-based prescription services is expected to improve treatment accessibility. These developments create significant revenue opportunities for manufacturers seeking geographic diversification and long-term market penetration.

Category-wise Analysis

Therapy Type Insights

Stress incontinence is expected to remain the leading segment, accounting for approximately 38% of global market revenue in 2026. The segment's dominance is driven by the high prevalence of bladder leakage associated with pregnancy, childbirth, menopause, obesity, and pelvic floor muscle weakness, particularly among women. Increasing awareness of women's health issues and improving diagnosis rates are encouraging more patients to seek treatment. In addition, pharmacological therapies combined with pelvic floor rehabilitation programs continue to support strong treatment adoption.

Urge incontinence is projected to be the fastest-growing segment, advancing at an estimated 7.5% CAGR through 2033. Growth is fueled by the increasing incidence of overactive bladder syndrome, diabetes-related bladder dysfunction, and neurological disorders. The growing availability of advanced therapies such as vibegron and mirabegron is improving treatment outcomes and patient compliance. Expanding elderly populations worldwide are expected to further accelerate demand for long-term urge incontinence management.

Drug Class Insights

Anticholinergics are anticipated to lead the market with nearly 34% revenue share in 2026, supported by their long-established role in urinary incontinence treatment. Medications such as oxybutynin, tolterodine, and solifenacin remain widely prescribed due to strong clinical familiarity and broad reimbursement coverage. The availability of cost-effective generic formulations has strengthened their adoption across both developed and emerging markets. Their affordability continues to sustain significant prescription volumes despite growing competition from newer therapies.

Beta-3 adrenoceptor agonists are expected to be the fastest-growing drug class, registering an estimated 8.1% CAGR during 2026–2033. The segment is benefiting from improved tolerability and a lower risk of cognitive side effects compared with traditional anticholinergic drugs. Increasing physician preference for products such as GEMTESA (vibegron) and mirabegron is driving adoption across major healthcare markets. Ongoing clinical research and market expansion initiatives are expected to further support segment growth.

End-user Insights

Hospitals are projected to account for approximately 46% of total market revenue in 2026, making them the dominant end-user segment. Their leadership is supported by access to specialist urologists, advanced diagnostic technologies, and comprehensive treatment pathways for complex urinary disorders. Growing investments in dedicated urology and pelvic health centers are further strengthening patient care capabilities. These advantages continue to position hospitals as the preferred treatment setting for urinary incontinence management.

Online Pharmacies are expected to emerge as the fastest-growing distribution channel, expanding at an estimated 8.4% CAGR through 2033. Rising adoption of telemedicine and digital prescription services is transforming access to urinary incontinence medications. The expansion of regulated e-pharmacy platforms across Europe and Asia Pacific is improving treatment accessibility for chronic disease patients. Competitive pricing, convenience, and home delivery services are further driving growth in this segment.

Regional Insights

North America Urinary Incontinence Therapeutics Market Trends

North America is expected to account for approximately 39% of the global urinary incontinence therapeutics market share in 2026, maintaining its position as the largest regional market. The region's leadership is likely to be supported by a large diagnosed patient population, favorable reimbursement policies, and early adoption of innovative therapies. Strong healthcare expenditure and a well-established urology care ecosystem are also expected to facilitate faster uptake of newly approved treatments.

U.S. Urinary Incontinence Therapeutics Market Trends

The U.S. is estimated to account for approximately 82% of the North America market share, supported by a rapidly aging population and high healthcare spending levels. The country is likely to maintain its dominance due to extensive clinical research activity and the presence of major pharmaceutical companies focused on overactive bladder therapies. Continued expansion of beta-3 agonist usage and a robust urology drug pipeline are expected to support market growth.

Canada Urinary Incontinence Therapeutics Market Trends

Canada is projected to contribute nearly 18% of the regional revenue share, benefiting from universal healthcare coverage and increasing awareness of age-related urinary disorders. Expanding access to pelvic floor physiotherapy and continence care pathways across provincial healthcare systems is expected to improve diagnosis and treatment rates. These developments are likely to strengthen patient access to urinary incontinence therapies over the forecast period.

Europe Urinary Incontinence Therapeutics Market Trends

Europe is expected to hold approximately 29% of the global market share in 2026, supported by a rapidly aging population and comprehensive public healthcare systems. Strong reimbursement frameworks and standardized treatment guidelines are likely to encourage consistent adoption of urinary incontinence therapies across major European markets. Growing emphasis on healthy aging and chronic disease management is expected to further support demand.

Germany Urinary Incontinence Therapeutics Market Trends

Germany is projected to account for nearly 33% of the Europe market share, making it the region's largest contributor. Its leadership is expected to be driven by high healthcare expenditure, advanced reimbursement mechanisms, and strong prescription drug utilization. Early adoption of innovative overactive bladder therapies, supported by an extensive network of specialist urology clinics, is likely to sustain market growth.

U.K. Urinary Incontinence Therapeutics Market Trends

The U.K is estimated to represent approximately 20% of regional revenue, supported by expanding continence care initiatives and broader women's health programs. Ongoing efforts by the NHS to improve bladder health management and early diagnosis are expected to enhance treatment uptake. Increasing use of telehealth platforms is also likely to improve access to specialist continence services across the country.

Asia Pacific Urinary Incontinence Therapeutics Market

Asia Pacific is projected to capture approximately 24% of the global market share in 2026 and is expected to register the fastest growth through 2033. Rising healthcare expenditure, expanding elderly populations, and improving healthcare infrastructure across emerging economies are likely to drive market expansion. Greater awareness of bladder health conditions and improved access to pharmaceutical therapies are expected to further accelerate adoption.

China Urinary Incontinence Therapeutics Market Trends

China is estimated to account for nearly 32% of the Asia Pacific market share, supported by a large patient population and ongoing healthcare modernization efforts. Government-led initiatives under the Healthy China 2030 strategy are expected to strengthen chronic disease management and expand access to specialist care services. Growth in domestic pharmaceutical manufacturing and broader reimbursement coverage for innovative therapies are also likely to improve treatment accessibility.

Japan Urinary Incontinence Therapeutics Market Trends

Japan is projected to represent approximately 26% of the regional revenue share in 2026, maintaining its position as one of the region's most established urinary incontinence treatment markets. The country's large elderly population is expected to continue generating substantial demand for bladder health therapies. Early adoption of beta-3 adrenoceptor agonists, combined with universal healthcare coverage and strong physician awareness, is likely to support steady market growth.

Competitive Landscape

The global urinary incontinence therapeutics market is moderately consolidated, with leading companies including Astellas Pharma, Sumitomo Pharma, Pfizer, Viatris, and Teva Pharmaceutical Industries accounting for a significant share of global revenue. These players leverage strong urology portfolios, extensive distribution networks, and continuous investment in clinical research to strengthen their positions. Strategic focus remains centered on expanding overactive bladder treatment offerings through next-generation therapies with improved efficacy and tolerability.

The generic manufacturers and regional pharmaceutical companies are increasing competition through cost-effective alternatives and broader market penetration. Regulatory requirements and reimbursement challenges continue to create barriers for new entrants. However, growing demand for innovative therapies and combination treatments is expected to support strategic partnerships, licensing agreements, and selective acquisitions, contributing to gradual market consolidation over the forecast period.

Key Industry Developments:

- In July 2025, Eisai launched Beova® (vibegron) in Thailand, marking the first commercial rollout within its licensed ASEAN territory and expanding access to advanced overactive bladder treatment.

Companies Covered in Urinary Incontinence Therapeutics Market

- Pfizer Inc.

- Astellas Pharma Inc.

- Sumitomo Pharma Co., Ltd.

- Viatris Inc.

- Teva Pharmaceutical Industries Ltd.

- AbbVie Inc.

- Johnson & Johnson

- Sanofi S.A.

- Bayer AG

- GlaxoSmithKline plc

- Eli Lilly and Company

- Boehringer Ingelheim GmbH

- Zydus Lifesciences Ltd.

- Dr. Reddy's Laboratories Ltd.

- Sun Pharmaceutical Industries Ltd.

Frequently Asked Questions

The global urinary incontinence therapeutics market is projected to reach US$4.8 billion in 2026.

Rising prevalence of overactive bladder disorders, growing elderly populations, and increasing treatment awareness drive market growth.

The market is expected to grow at a CAGR of 6.9% from 2026 to 2033.

Opportunities lie in emerging markets, the expansion of advanced therapies, and improving access to urology care.

Astellas Pharma, Sumitomo Pharma, Pfizer, Viatris, and Teva Pharmaceutical Industries are among the leading market participants.