- Medical Devices

- Urinary Catheters Market

Urinary Catheters Market Size, Share, and Growth Forecast 2026 - 2033

Urinary Catheters Market by Product (Intermittent Catheter, Indwelling (Foley) Catheter, External Catheter), by Catheter Type (Coated, Uncoated), Application, End-user, and Regional Analysis, 2026 - 2033

Urinary Catheters Market Size and Trend Analysis

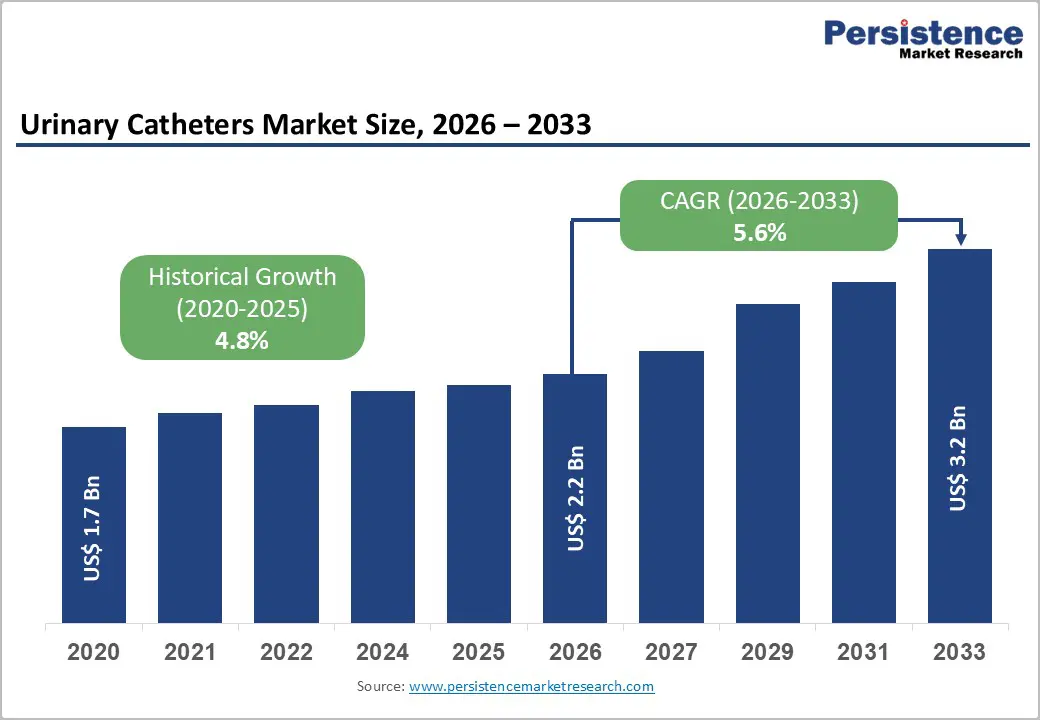

The global urinary catheters market size is expected to be valued at US$ 2.2 billion in 2026 and projected to reach US$ 3.2 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. It is on a steady and sustainable growth path, driven by the rise in global prevalence of urological disorders, an aging population requiring long-term catheterization management, and rising surgical procedure volumes across urology and general surgery.

The World Health Organization (WHO) identifies non-communicable diseases and age-related conditions, including benign prostatic hyperplasia (BPH), spinal cord injuries, and urinary incontinence, as the primary clinical indications for urinary catheterization, all of which are rising globally. Advancements in anti-infective coated catheter technologies that significantly reduce catheter-associated urinary tract infection (CAUTI) rates, combined with expanding home-based catheterization management in long-term care settings, are further broadening market demand and improving clinical outcomes.

Key Industry Highlights:

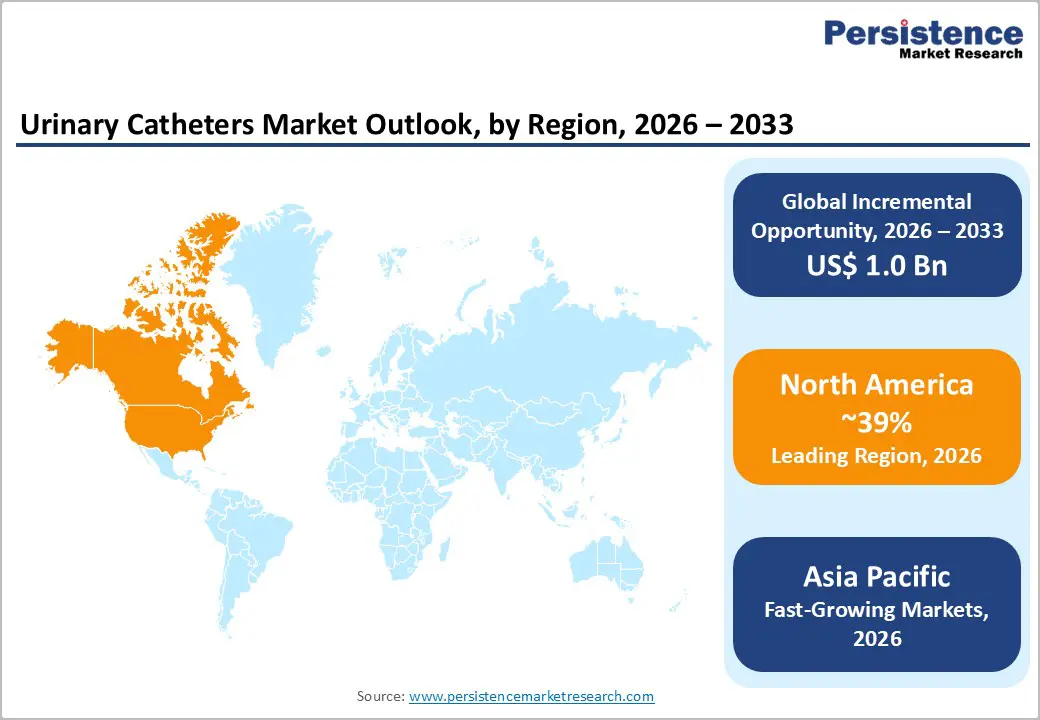

- Leading Region: North America leads with 39% share due to high urological disease prevalence, strong CMS CAUTI reduction mandates, and robust reimbursement support for catheterization management.

- Fastest Growing Region: Asia Pacific grows fastest due to rapidly aging populations, large unmet urological disease burden, and expanding healthcare infrastructure under government healthcare programs.

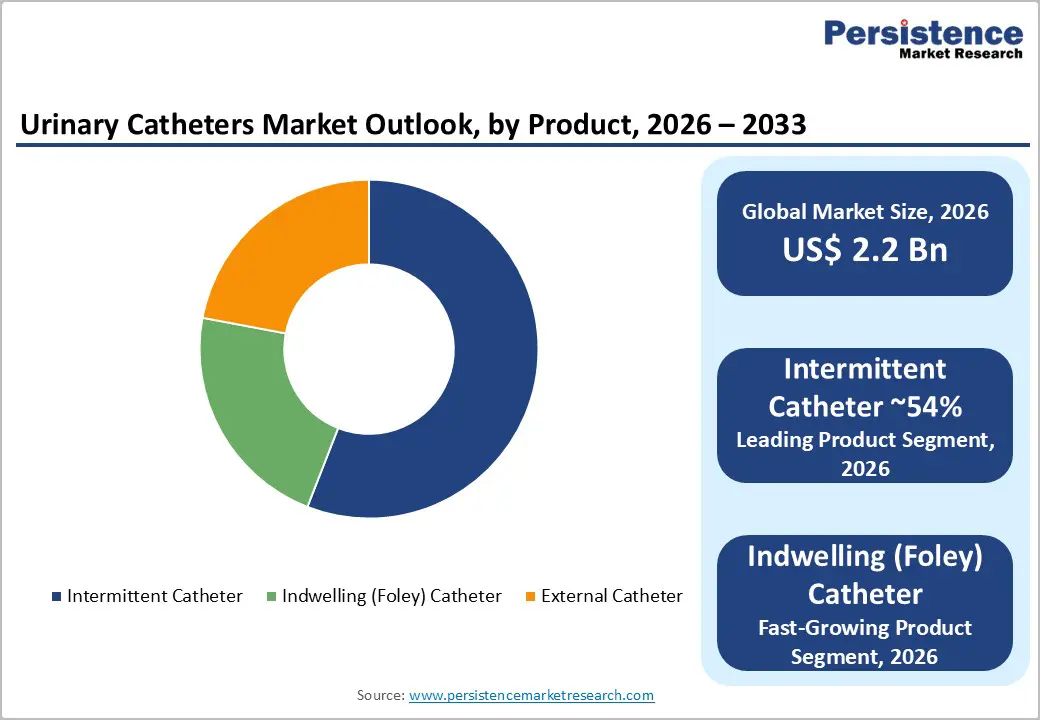

- Dominant Segment: Intermittent catheters dominate with 54% share driven by clinical guideline preference, long-term neurogenic bladder management, and rising spinal cord injury patient population.

- Fastest Growing Segment: Indwelling (Foley) catheters grow fastest due to increasing surgical procedure volumes, hospital usage, and rising adoption of antimicrobial-coated Foley catheters.

- Key Market Opportunity: Hydrophilic-coated catheters offer strong growth potential due to lower CAUTI rates, premium product adoption, and reimbursement-linked infection prevention mandates.

Market Dynamics

Drivers - Increased Focus on Homebased Care

Conditions like urinary incontinence, neurogenic bladder, and benign prostatic hyperplasia (BPH) often require long term management using urinary catheters. For example, According to the National Association for Continence (NAFC), around 70% of patients with urinary incontinence prefer self-catheterization over relying on healthcare providers for assistance.

Self-catheterization has become a popular option for patients requiring intermittent catheterization owing to convenience and cost-effectiveness. Innovations like hydrophilic coated catheters are easy to use and decrease discomfort, boosting their adoption in home settings. For instance, The Agency for Healthcare Research and Quality (AHRQ) reports that home healthcare is 30% to 50% more cost-effective than institutional care.

Favourable Reimbursement Policies

Several countries include intermittent, indwelling, and external urinary catheters in their healthcare reimbursement frameworks. This ensures that patients can access necessary products without incurring substantial out-of-pocket expenses. For example, In the U.S., Medicare Part B and private insurance plans cover intermittent catheterization supplies for individuals with permanent urological conditions.

Coverage includes 200 catheters per month for eligible patients. Catheters with sterile packaging or coatings are also reimbursable if deemed medically necessary. For example, In Canada, provincial health programs like the Assistive Devices Program (ADP) in Ontario provide coverage for urinary catheters, decreasing the financial burden on patients.

Hydrophilic-coated catheters, known for decreasing catheter-associated urinary tract infections (CAUTIs), saw a 12% higher adoption rate in regions with comprehensive reimbursement policies.

Restraints - High Risk of Catheter-Associated Urinary Tract Infections (CAUTIs)

Despite advancements in catheter coating technology, CAUTI remains a significant clinical and reputational restraint for urinary catheter adoption. The CDC estimates that CAUTIs contribute to approximately 13,000 deaths annually in the United States and add substantial hospital costs estimated at over US$ 1 billion annually by the Agency for Healthcare Research and Quality (AHRQ). Reimbursement penalties under the Centers for Medicare & Medicaid Services (CMS) Hospital-Acquired Condition Reduction Program for institutions with high CAUTI rates incentivize catheter minimization strategies, creating headwinds for overall catheter utilization volumes in hospital settings.

Opportunities - Expanding Home-Based and Long-Term Care Catheterization Management

The global shift toward home-based healthcare and long-term care facility management for chronically ill and elderly patients represents a high-growth opportunity for urinary catheter manufacturers. The U.S. Centers for Medicare & Medicaid Services (CMS) has been progressively expanding reimbursement frameworks for home health services, with the National Association for Home Care & Hospice (NAHC) reporting that over 12 million Americans receive home-based healthcare services annually.

For patients requiring long-term intermittent self-catheterization, including those with spinal cord injuries, multiple sclerosis, and post-prostatectomy urinary retention, the home care setting is increasingly preferred over hospital or clinic-based catheterization. This trend is creating strong demand for compact, user-friendly, pre-lubricated single-use intermittent catheter products designed for self-administration, a segment where Coloplast A/S, Hollister Incorporated, and Teleflex Incorporated have been actively investing in patient-friendly product innovation and remote patient support programs.

Category-wise Analysis

Product Insights

Intermittent Catheters dominate the urinary catheters market, commanding approximately 54% of global market share in 2026. This leadership position reflects the clinical preference for intermittent catheterization (IC) as the gold standard for long-term bladder management in patients with neurogenic bladder dysfunction, spinal cord injuries, and chronic urinary retention. The European Association of Urology (EAU) and American Urological Association (AUA) guidelines both endorse clean intermittent catheterization (CIC) as the preferred management technique over indwelling catheters for long-term use, owing to its lower infection risk, preservation of bladder function, and compatibility with active lifestyles.

The growing population of spinal cord injury patients, estimated at over 5.4 million individuals in the United States per the National Spinal Cord Injury Statistical Center (NSCISC) represents a permanent and growing user base for intermittent catheter products, securing segment leadership through the forecast period.

Catheter Type Insights

Coated Catheters hold the leading position within the catheter type segmentation, accounting for approximately 58% of the global urinary catheter market share in 2026. Coated catheters encompassing hydrophilic, antimicrobial, and gel-reservoir pre-lubricated formats have achieved market leadership through compelling clinical evidence demonstrating significantly reduced CAUTI rates, lower urethral trauma, and improved patient quality of life compared to uncoated alternatives.

The CDC's Healthcare Infection Control Practices Advisory Committee (HICPAC) guidelines actively recommend the use of coated catheters where clinically appropriate as a CAUTI prevention measure. Institutional procurement mandates from major hospital systems, NHS trusts, and long-term care networks, all under quality-based reimbursement pressure to reduce CAUTI rates, are consistently upgrading procurement specifications to favor coated over uncoated catheter formats, driving volume and value migration toward the coated segment.

End-user Insights

Hospitals are the dominant end-user segment for urinary catheters, representing approximately 55% of global market demand in 2025. Hospitals serve as the highest-volume procurement center for the full spectrum of catheter products from perioperative indwelling Foley catheters to intermittent catheters for inpatient urological management. The American Hospital Association (AHA) reports approximately 6,120 registered hospitals in the United States, all of which routinely utilize urinary catheters across urology, surgery, intensive care, and general medical wards. The CDC estimates that urinary catheters are used in approximately 15 to 25% of hospitalized patients at some point during their stay, reflecting the extraordinary breadth of hospital-based catheter utilization. Group purchasing organization (GPO) contracts and value analysis committee procurement processes make hospitals the most commercially critical channel for catheter manufacturers seeking large-volume contracts and institutional formulary placement.

Regional Insights

North America Urinary Catheters Market Trends and Insights

North America urinary catheters market is estimated to hold a share of 38.7% in 2025 and witness a CAGR of 4.1% through 2032. Urological conditions like urinary retention, incontinence, and bladder dysfunction are highly prevalent in the region. For example, according to the National Association for Continence (NAFC), nearly 25 million Americans experience urinary incontinence, a significant factor driving demand for urinary catheters.

The aging population of the region is particularly affected, with over 30% of men and women aged 65 and above predicted to have some form of urinary incontinence. This fuels the need for intermittent and indwelling catheters. According to the U.S. Census Bureau, the population aged 65 and older in the U.S. reached 56 million in 2020 and is predicted to grow to 73 million by 2030. Older adults are predicted to require long-term catheterization, supporting the growth of the urinary catheter market in the region. Availability of skilled healthcare professionals in the region ensures the widespread adoption of catheters in hospitals and clinics.

U.S. Urinary Catheters Market Size

The United States accounts for approximately 87% of North America's urinary catheter market. The CDC estimates approximately 449,334 CAUTIs occur in U.S. hospitals annually, creating strong institutional pressure to adopt premium coated catheter products. With over 33 million Americans affected by urinary incontinence per the NIDDK and a robust home health reimbursement framework under CMS, the U.S. represents the single largest national urinary catheter market globally.

Europe Urinary Catheters Market Trends and Insights

Europe is the second-largest regional market for urinary catheters, characterized by universal healthcare systems with strong institutional procurement frameworks, advanced clinical guideline adoption from the European Association of Urology (EAU), and progressive regulatory standards under EU MDR 2017/745. The region demonstrates high adoption of hydrophilic-coated intermittent catheters, driven by quality-based hospital procurement standards and NHS infection prevention programs across Western Europe. Aging demographics across Germany, France, Italy, and Spain are sustaining long-term market demand growth.

Germany Urinary Catheters Market Size

Germany accounts for approximately 22% of Europe's urinary catheter market, anchored by its comprehensive statutory health insurance system covering urological devices and a high density of urological specialist practitioners. Germany's aging population, followed by the growing BPH and urinary incontinence prevalence, and advanced hospital infection control standards drive consistent demand for coated intermittent catheters. B. Braun Melsungen AG, headquartered in Germany, is a leading global catheter manufacturer with strong domestic market penetration.

UK Urinary Catheters Market Size

The UK represents approximately 16% of Europe's urinary catheter market, with the National Health Service (NHS) serving as the dominant procurement authority. NHS England's CAUTI reduction programs and its proactive adoption of hydrophilic-coated catheter specifications across NHS trusts have significantly driven the shift toward premium coated products. The NHS handles over 1.2 million daily patient contacts, with urological catheterization representing a consistent high-volume clinical activity across inpatient and community care settings.

Asia Pacific Urinary Catheters Market Trends and Insights

Asia Pacific is the fastest-growing regional market for urinary catheters, fueled by rapidly expanding healthcare infrastructure, a large and aging population base, and growing awareness of urological health conditions across China, India, Japan, and ASEAN nations. China leads regional demand, with the National Health Commission of China's Healthy China 2030 plan driving hospital capacity expansion and improving urological diagnostic and treatment infrastructure. Rising surgical procedure volumes and increasing adoption of CAUTI prevention protocols are amplifying catheter demand regionally.

India Urinary Catheters Market Size

India represents approximately 9% of Asia Pacific's urinary catheter market, with demand growing rapidly alongside hospital infrastructure expansion under the Ayushman Bharat scheme and rising urological disease awareness. India has a large and underdiagnosed BPH and urinary incontinence patient population, with increasing specialist care access driving catheter utilization growth. Domestic manufacturers alongside global players including Becton, Dickinson and Company are expanding India distribution networks to capture growing market demand.

Japan Urinary Catheters Market Size

Japan accounts for approximately 18% of Asia Pacific's urinary catheter market, reflecting its highly aged demographic profile with 29% of the population aged 65 or above per the Statistics Bureau of Japan and mature healthcare system. Japan's Ministry of Health, Labour and Welfare (MHLW) infection control mandates and strong clinical guideline adoption from the Japanese Continence Society drive consistent demand for premium coated catheters in hospitals and long-term care facilities.

Competitive Landscape

The global urinary catheters market is moderately consolidated, with multinational medical device companies including Coloplast A/S, B. Braun Melsungen AG, Becton, Dickinson and Company, Teleflex Incorporated, Hollister Incorporated, and Boston Scientific Corporation collectively commanding significant market share. Competitive differentiation centers on advanced coating technologies (hydrophilic, antimicrobial, and gel-reservoir formats), patient-centric self-catheterization product design, clinical evidence generation for CAUTI reduction, and integrated patient support programs. Market leaders are actively pursuing geographic expansion in Asia Pacific and Latin America, and investment in digital health catheter management platforms is emerging as a new frontier. Specialty players such as Cathetrix and UroDev Medical are innovating with novel catheter materials and form factors targeting niche clinical applications.

Key Developments:

- In March 2025, Uni Pharma launched the TrueClr active negative-pressure urinary catheter, a non-invasive, reusable solution that improves bladder drainage, reduces CAUTI risk, enhances patient comfort, and supports home and hospital care.

- In September 2024: Teleflex Incorporated received FDA 510(k) clearance for its new antimicrobial-coated Foley catheter incorporating a novel silver alloy surface treatment demonstrated in clinical studies to reduce CAUTI incidence in short-term indwelling catheterization applications.

- In January 2024, the California Institute of Technology published a report on how their researchers utilized AI to develop a catheter design that reduced bacterial upstream movement by 100-fold in lab tests. This innovation prevents the use of antibiotics or chemicals, ensuring effective infection prevention.

- In September 2023, the Sage PrimaFit External Urine Management device reduced CAUTI rates by 72%. Clinical Nurse Specialists implemented a quality improvement program to decrease the prevalence and associated harm of catheter-associated urinary tract infections effectively.

Global Urinary Catheters Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 1.7 Billion |

|

Current Market Value (2026) |

US$ 2.2 Billion |

|

Projected Market Value (2033) |

US$ 3.2 Billion |

|

CAGR (2026–2033) |

5.6% |

|

Leading Region |

North America, 39% market share (2025) |

|

Dominant Product Category |

Intermittent Catheter, ~54% market share (2025) |

|

Top-Ranking Catheter Type |

Coated Catheters, ~58% market share (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 1.0 Billion |

Companies Covered in Urinary Catheters Market

- B. Braun Melsungen AG

- Coloplast A/S

- Becton, Dickinson and Company

- Teleflex Incorporated

- Boston Scientific Corporation

- Medtronic plc.

- Hollister Incorporate

- Cook Medical

- Cathetrix

- UroDev Medical

- Stryker Corporation

- Consure Medical

- J and M Urinary Catherters LLC

- Urocare Products Inc.

- Others

Frequently Asked Questions

The global urinary catheters market is estimated to be valued at US$ 2.2 billion in 2026.

Aging population, rising urinary disorders, increasing CAUTI prevention focus, and strong hospital demand for advanced coated catheter solutions drive market growth.

North America leads the global market with approximately 39% market share in 2025.

Major growth opportunity lies in hydrophilic-coated intermittent catheters for homecare, driven by reimbursement support, lower CAUTI risk, and self-catheterization demand.

Prominent players in the market include B. Braun Melsungen AG, Coloplast A/S, and Becton, Dickinson and Company.