- Medical Devices

- Urea Breath Test Systems Market

Urea Breath Test Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Urea Breath Test Systems Market by Product Type (Urea Breath Test Kits, Urea Breath Test Analyzer), Test (Point-of-Care Tests (POCT), Laboratory-Based Test), Instrument (Mass Spectrometer, Others), and Regional Analysis for 2026 - 2033

Urea Breath Test Systems Market Size and Trends Analysis

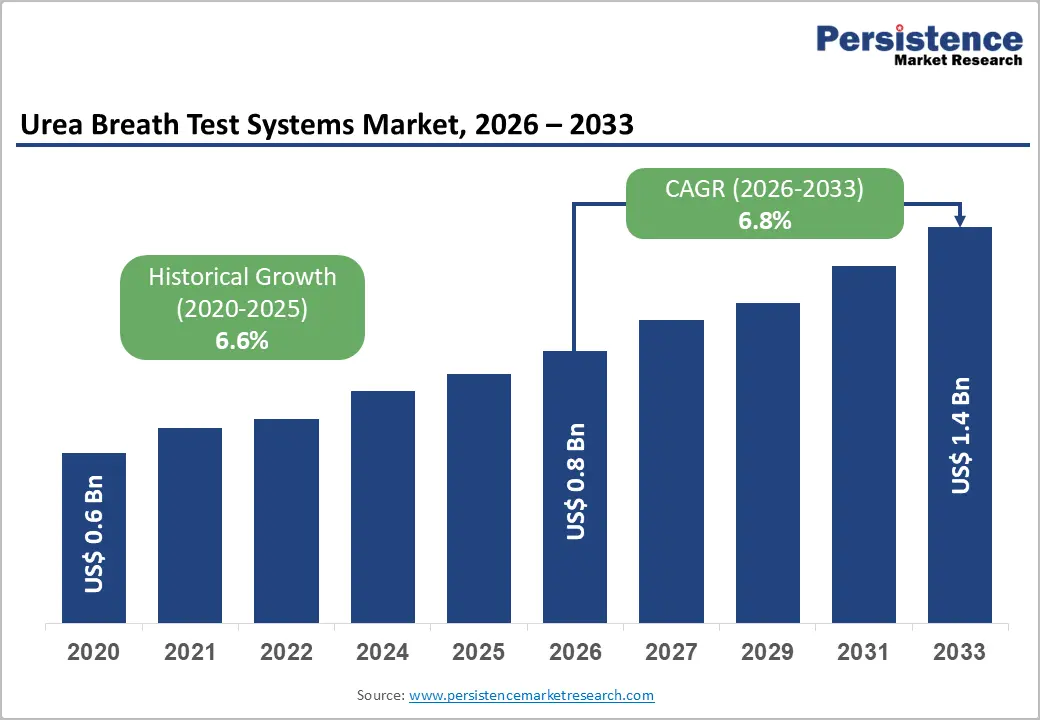

The global urea breath test systems market size is likely to be valued at US$0.8 billion in 2026 and is expected to reach US$1.4 billion by 2033, growing at a CAGR of 6.8% during the forecast period from 2026 to 2033, driven by rising awareness of gastrointestinal disorders, increasing prevalence of helicobacter pylori (H. pylori) in both developed and developing regions, and a growing preference for non-invasive, accurate, and patient-friendly diagnostic methods over traditional endoscopy or serological tests.

These systems are widely used for detecting active infections, confirming eradication post-treatment, and supporting risk assessment for peptic ulcer disease and gastric cancer. Technological advancements in analyzers, including portable and point-of-care devices, have enhanced speed, accuracy, and accessibility, enabling adoption in hospitals, specialized clinics, and diagnostic laboratories. Regulatory focus on early detection and treatment of H. pylori-related complications has bolstered market momentum. Despite strong demand, regional variations in healthcare infrastructure, clinical awareness, and reimbursement policies influence adoption rates.

Key Industry Highlights:

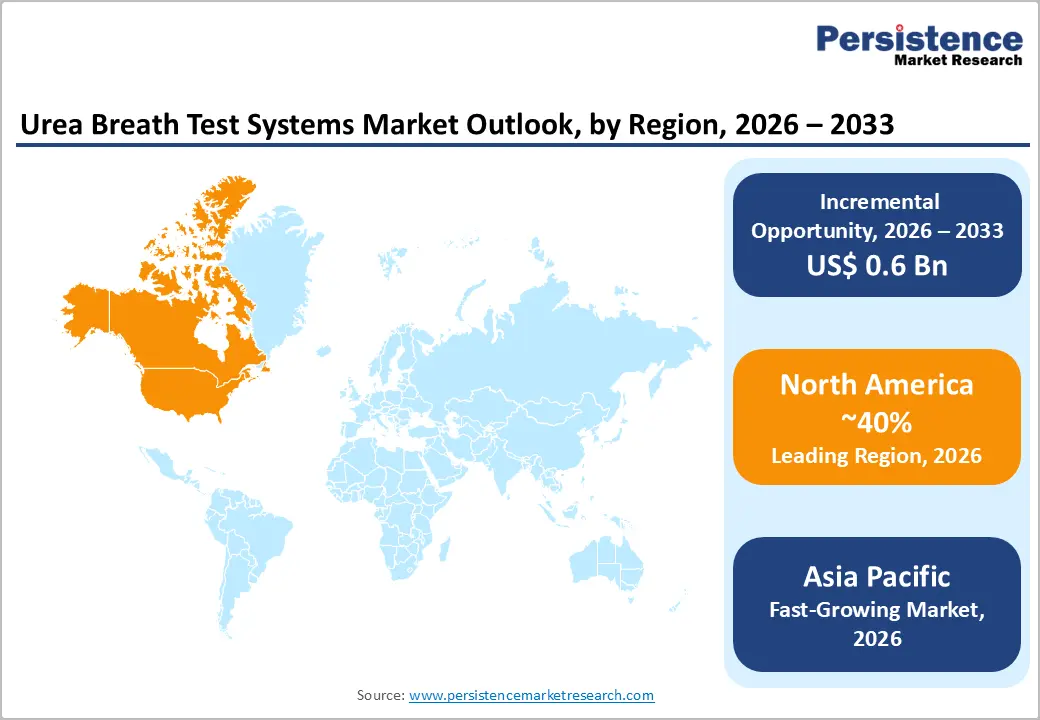

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by advanced healthcare infrastructure, high awareness, strong reimbursement frameworks, and widespread adoption of non-invasive diagnostics.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by high H. pylori prevalence, expanding healthcare infrastructure, and increasing adoption of non-invasive diagnostics.

- Leading Product Type: Urea breath test kits are projected to represent the leading product type in 2026, accounting for 60% of the revenue share, driven by recurring consumption in testing protocols and widespread use across labs and clinics.

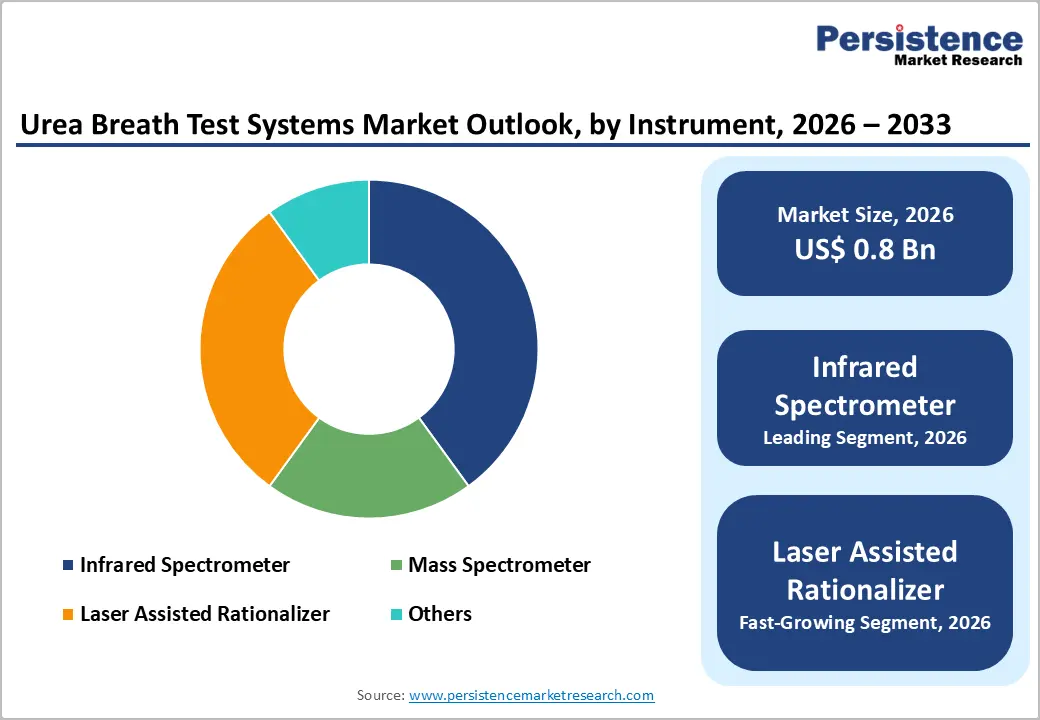

- Leading Instrument: The infrared spectrometer is anticipated to be the leading instrument, accounting for over 50% of the revenue share in 2026, supported by cost-effectiveness, sufficient accuracy, and suitability for mid-sized laboratories.

| Key Insights | Details |

|---|---|

| Urea Breath Test Systems Market Size (2026E) | US$0.8 Bn |

| Market Value Forecast (2033F) | US$1.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.6% |

DRO Analysis

Driver - Rising Prevalence of H. Pylori Infections and Associated Diseases

The rise in H. pylori infections, particularly in developing regions, has intensified demand for effective diagnostic tools. Increasing incidences of peptic ulcers, gastritis, and gastric cancer underscore the need for timely and accurate detection. Urea breath tests are widely recognized for their sensitivity and specificity, making them a preferred choice for clinicians managing gastrointestinal health. Growth in routine screening programs and follow-up monitoring drives steady consumption of kits and analyzers.

The sustained prevalence of H. pylori across populations has prompted healthcare providers to prioritize non-invasive diagnostics that can be deployed at scale. Public health initiatives targeting infection control and gastrointestinal disease prevention have reinforced market growth. Diagnostic laboratories and point-of-care centers are expanding their use of urea breath tests to meet rising clinical demand. The high reliability of these systems in confirming eradication post-treatment and guiding therapy decisions enhances their adoption in both outpatient and hospital settings.

Preference for Non-Invasive, Patient-Friendly Diagnostic Methods

Patients and healthcare providers increasingly favor non-invasive diagnostic methods over traditional endoscopy or serology due to reduced discomfort and procedural risk. Urea breath tests provide a simple, quick, and reliable alternative that can be performed without extensive preparation, sedation, or invasive sampling. This patient-centered approach supports higher compliance rates and allows repeat testing for follow-up monitoring, expanding clinical use. The convenience of point-of-care testing in clinics, combined with laboratory-based options, encourages adoption.

The preference for patient-friendly diagnostics is reinforced by clinical guidelines recommending non-invasive tests for both initial detection and post-eradication verification. Healthcare systems prioritize solutions that minimize hospital stay, reduce procedure-related anxiety, and lower overall treatment costs. Urea breath tests fulfill these requirements while delivering high sensitivity and specificity, making them suitable for routine screening in diverse populations.

Restraint - Availability of Alternative Diagnostic Methods

Competing diagnostic options, such as endoscopy with biopsy, stool antigen tests, and serology, create limitations for the urea breath test market. These alternatives are well-established in many regions and may be preferred due to clinician familiarity, infrastructure availability, or insurance coverage. In some clinical settings, particularly in hospitals with advanced gastroenterology departments, endoscopic procedures remain the standard for comprehensive assessment, reducing reliance on non-invasive methods.

The existence of multiple diagnostic options also intensifies price competition and impacts procurement decisions by healthcare providers. In emerging markets, where endoscopy facilities are limited, stool antigen tests or serology may still dominate due to cost advantages and accessibility. This competitive environment requires urea breath test manufacturers to demonstrate clear clinical benefits, cost-effectiveness, and ease of use to secure wider adoption.

Limited Awareness and Adoption in Emerging Markets

In many emerging regions, awareness of H. pylori-related complications and the benefits of non-invasive diagnostics remains low, constraining market growth. Limited knowledge among healthcare providers and patients results in underutilization of urea breath tests. Infrastructure challenges, including the availability of analyzers, trained personnel, and supply chains for consumables, restrict adoption. Budgetary constraints and prioritization of other pressing health concerns reduce investment in advanced diagnostics.

Healthcare providers in these markets may also be hesitant to shift from traditional methods due to perceived costs or unfamiliarity with test protocols. Public health initiatives and government programs focused on early detection are still evolving, creating a gap in awareness and integration of urea breath test systems. Overcoming these challenges requires collaboration between manufacturers, clinicians, and policymakers to enhance knowledge, improve accessibility, and promote reimbursement mechanisms.

Opportunity - Technological Convergence and Point-of-Care Innovation

Advances in technology offer opportunities to enhance the functionality, portability, and automation of urea breath test systems. Integration of mass spectrometry, infrared spectroscopy, and laser-assisted detection methods with software analytics improves accuracy, speed, and ease of use. Point-of-care devices allow clinicians to conduct tests in clinics, outpatient centers, and remote locations, expanding accessibility and reducing dependency on centralized labs. Innovations in miniaturization, cloud connectivity, and AI-enabled data interpretation provide efficient workflows and faster decision-making.

Emerging innovations also enable cost optimization, scalability, and multi-site deployment, supporting healthcare providers in both urban and rural settings. Automated analyzers and simplified kits reduce training requirements and procedural errors, fostering adoption in smaller hospitals and community clinics. Strategic partnerships between technology developers and diagnostic companies accelerate R&D, commercialization, and market penetration. Investment in research for enhanced sensitivity, rapid detection, and integrated patient management tools strengthens the market’s long-term prospects.

Policy Support for Early Gastrointestinal Disease Management

Government and regulatory bodies increasingly emphasize early detection and management of H. pylori infections to reduce complications such as ulcers and gastric cancer. Initiatives promoting routine screening and guideline-driven care provide favorable conditions for the adoption of urea breath tests. Policies supporting reimbursement, standardization of diagnostic procedures, and integration of non-invasive testing into national health programs encourage healthcare providers to implement these systems widely.

Regulatory support also facilitates faster approvals for new analyzers, kits, and point-of-care devices, reducing barriers to market entry and enhancing competitive advantage. Inclusion of urea breath tests in clinical guidelines strengthens adoption in hospitals, clinics, and laboratories. Governments and health organizations focus on increasing accessibility in underserved regions, addressing both diagnostic and treatment gaps. By promoting early intervention and efficient disease management, policy support amplifies market opportunities, drives sustained growth, and encourages stakeholders to develop innovative solutions that improve outcomes in gastrointestinal health worldwide.

Category-wise Analysis

Product Type Insights

Urea breath test kits are expected to lead the urea breath test systems market, accounting for approximately 60% of revenue in 2026, driven by their dominant position in diagnostic testing for H. pylori infections. These kits provide the essential ¹³C- or ¹&sup4;C-urea substrates and collection materials, enabling widespread use across hospitals, diagnostic laboratories, and clinics. Their consumable nature ensures recurring demand as kits are required for both initial diagnosis and follow-up testing post-eradication. For example, Meridian Bioscience’s urea breath test kits are widely utilized in clinical laboratories for their high sensitivity and ease of use.

The urea breath test analyzer is likely to represent the fastest-growing segment, supported by increasing demand for automated and high-throughput diagnostic systems. These analyzers deliver quantitative results with high precision, supporting efficiency gains in busy laboratories and clinical facilities. For example, Sercon Group’s automated ¹³C-urea breath test analyzers are rapidly adopted in hospital laboratories due to their reliability and integration with laboratory information management systems.

Instrument Insights

Infrared spectrometers are projected to lead the market, capturing around 50% of the revenue share in 2026, supported by their cost-effectiveness and suitability for routine clinical use. These systems balance accuracy and affordability, making them ideal for mid-sized laboratories and hospitals that perform frequent H. pylori testing. For example, Kizlon Inc. offers infrared spectrometer-based urea breath test analyzers that provide rapid and reliable detection while minimizing operational costs. The widespread adoption of infrared-based systems stems from their ability to deliver consistent results with relatively simple infrastructure, supporting high-volume workflows in both diagnostic and research settings.

Laser-assisted ratio analyzers are likely to be the fastest-growing instrument, driven by demand for speed, reduced complexity, and modern optical detection techniques. These analyzers enable rapid, non-dispersive measurement of ¹³C-urea in breath samples, allowing for efficient testing in high-throughput or point-of-care environments. For example, Beijing Richen-Force Science & Technology has developed laser-assisted analyzers that minimize operational complexity while maintaining high sensitivity, appealing to hospitals and diagnostic centers expanding their testing capacity.

Regional Insights

North America Urea Breath Test Systems Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by advanced healthcare infrastructure, high clinical awareness, and strong reimbursement policies. Hospitals and diagnostic laboratories increasingly adopt urea breath test systems for routine H. pylori detection and post-eradication monitoring due to their non-invasive nature and high sensitivity. For example, Meridian Bioscience Inc. has strengthened its market presence by providing comprehensive urea breath test kits and analyzers widely utilized across U.S. hospitals, clinics, and outpatient centers.

The region’s growth is supported by rising patient preference for minimally invasive procedures, increasing adoption of point-of-care testing, and investments in advanced laboratory equipment. Innovation in analyzer technologies, including infrared spectrometry and automated data processing, enhances precision and efficiency, enabling broader implementation across clinical settings. North American healthcare providers prioritize reliable, non-invasive diagnostics to manage gastrointestinal diseases effectively.

Europe Urea Breath Test Systems Market Trends

Europe is likely to be a significant market for urea breath test systems, due to high awareness of H. pylori infections and strong regulatory standards emphasizing diagnostic accuracy and patient safety. Hospitals, diagnostic laboratories, and specialized clinics are increasingly implementing urea breath test systems to align with evidence-based guidelines. For example, Bio-Rad Laboratories Inc. has contributed to the European market by offering advanced analyzers and consumable kits that streamline laboratory workflows, reduce processing time, and enhance test accuracy.

Growth is also fueled by rising demand for infrared spectrometers and mass spectrometer-based systems in hospital laboratories, while portable point-of-care devices gain popularity in outpatient settings. Investments in clinical infrastructure, laboratory modernization, and training for healthcare personnel enhance the capacity to perform accurate and efficient H. pylori testing. Increasing collaboration between diagnostic companies, healthcare providers, and public health programs promotes the adoption of innovative technologies.

Asia Pacific Urea Breath Test Systems Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by high H. pylori prevalence in countries, including China, Japan, and India, combined with the rapid expansion of healthcare infrastructure and increasing awareness of gastrointestinal health. Hospitals, diagnostic centers, and rural outreach programs are adopting both laboratory-based analyzers and point-of-care kits to improve access to accurate diagnostics. Local manufacturers, such as Beijing Richen-Force Science & Technology Co. Ltd., are developing cost-effective analyzers and consumable kits that cater to high-volume testing and emerging markets, driving adoption.

Investments in healthcare technology, modernization of laboratory facilities, and public-private partnerships expand availability across urban and rural areas. The growing emphasis on non-invasive diagnostics, high patient compliance, and portable point-of-care devices supports rapid market growth. Asia Pacific benefits from a combination of demographic factors, rising disease awareness, and the adoption of innovative technologies that improve throughput, accuracy, and efficiency.

Competitive Landscape

The global urea breath test systems market exhibits a moderately fragmented structure, driven by a combination of established diagnostics firms and specialized regional manufacturers offering a range of systems and consumables to detect Helicobacter pylori. Market participation spans large multinational companies to niche innovators, each contributing through tailored product lines and expanding geographic presence.

With key leaders, including Sercon, Kibion GmbH, Meridian Bioscience Inc., Kizlon Medical, Beijing Richen-Force Science & Technology Co., Ltd., Shenzhen Zhonghe Headway Bio-Sci & Tech Co., Ltd., and Exalenz Bioscience Ltd., the landscape reflects broad participation from regional players focusing on continuous innovation and market coverage. These players compete through product innovation, strategic partnerships, expansion of distribution networks, and enhanced customer support services to strengthen market share and clinical adoption.

Key Industry Developments:

- In January 2026, AIG Hospitals in Hyderabad introduced PYtest®, a non-invasive urea breath test for early detection of Helicobacter pylori infections - marking the first clinical availability of this validated breath test in India. The test, developed by Nobel Laureate Prof. Barry Marshall, provides rapid and accurate detection of active H. pylori infection without requiring invasive procedures such as endoscopy or biopsy, improving patient comfort and diagnostic efficiency.

- In July 2025, Meridian Bioscience Inc., a leading global diagnostics company, continued its expansion of Helicobacter pylori diagnostic solutions by securing U.S. FDA clearance for its Premier® HpSA® FLEX™ test, which enhances the detection of H. pylori antigens in both preserved and unpreserved stool samples. The Premier HpSA FLEX joins Meridian’s existing portfolio, including the BreathID® urea breath test system, offering clinicians additional non-invasive tools for gastrointestinal diagnosis.

Companies Covered in Urea Breath Test Systems Market

- Sercon Group

- Kibion GmbH

- AdvaCare Pharma

- Kizlon Medical

- Meridian Bioscience Inc.

- Thermo Fisher Scientific Inc.

- Bio-Rad Laboratories Inc.

- Paladin Pharma Inc.

- Eurofins Scientific

- Beijing Richen-Force Science & Technology Co., Ltd.

- Shenzhen Zhonghe Headway Bio-Sci & Tech Co., Ltd.

Frequently Asked Questions

The global urea breath test systems market is projected to reach US$0.8 billion in 2026.

The urea breath test systems market is driven by the rising prevalence of Helicobacter pylori infections and growing preference for accurate, non-invasive, patient-friendly diagnostics.

The urea breath test systems market is expected to grow at a CAGR of 6.8% from 2026 to 2033.

Key market opportunities in the urea breath test systems market include technological advancements in analyzers, point-of-care adoption, and expanding access to non-invasive gastrointestinal diagnostics in emerging regions.

Sercon Group, Kibion GmbH, AdvaCare Pharma, Kizlon Inc., Meridian Bioscience Inc., and Thermo Fisher Scientific Inc. are the leading players.