- Agrochemicals

- Urea Market

Urea Market Size, Share, and Growth Forecast 2026 - 2033

Urea Market by Product Form (Granular, Prilled), Application (Fertilizer, Industrial/Chemical: Resins, Adhesives & Laminates, Others; Diesel Exhaust Fluid, Animal Feed, Others), End-user (Agriculture, Chemical, Automotive, Construction, Others), and Regional Analysis, 2026 - 2033

Urea Market Size and Trend Analysis

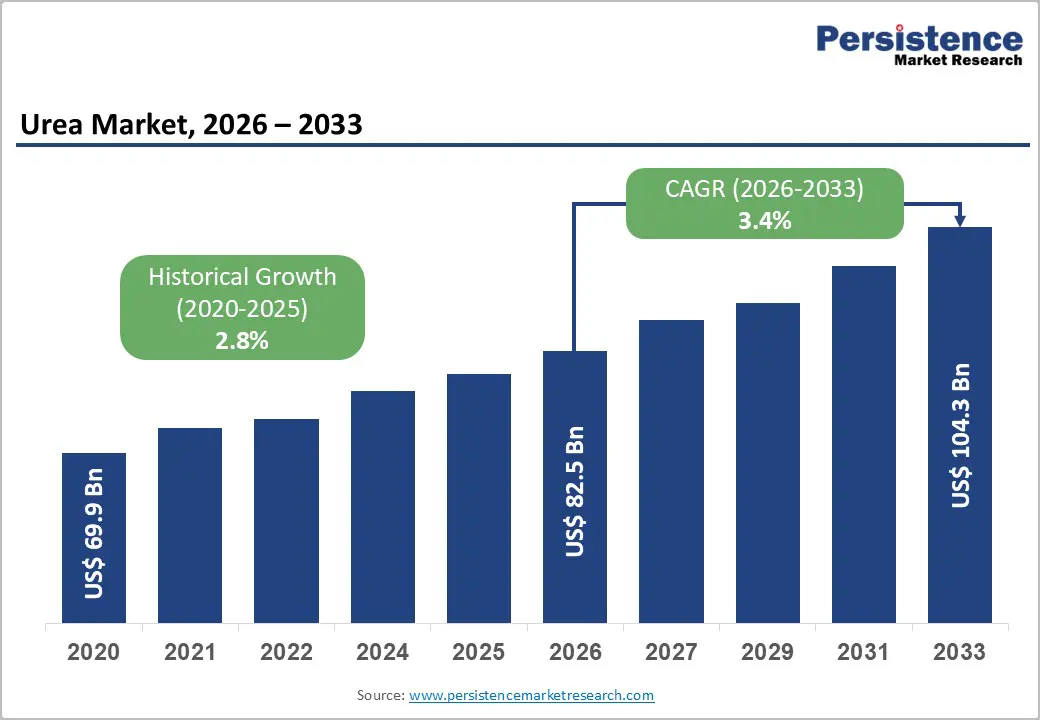

The global urea market size is expected to be valued at US$ 82.5 billion in 2026 and projected to reach US$ 104.3 billion by 2033, growing at a CAGR of 3.4% between 2026 and 2033.

This steady growth is primarily driven by expanding global agricultural activity requiring nitrogen fertilizer inputs to sustain crop yields for a growing world population, the mandatory rollout of Diesel Exhaust Fluid (DEF) programs under stringent vehicle emission regulations globally, and growing urea-formaldehyde resin demand from the construction and furniture manufacturing sectors.

Key Industry Highlights

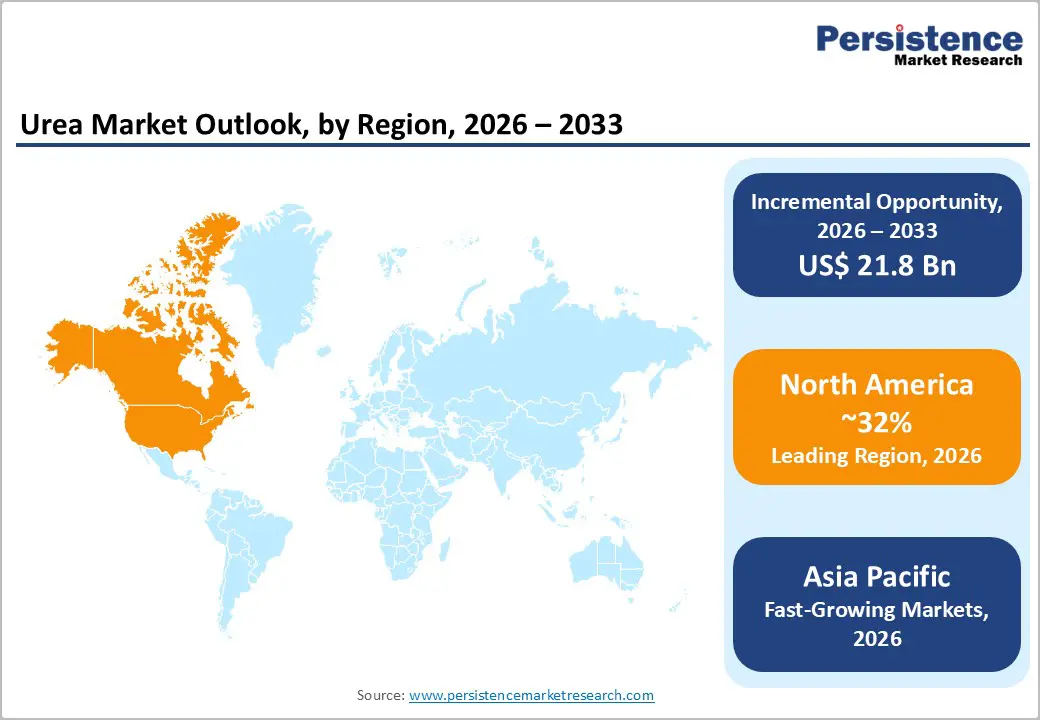

- Leading Region: North America commands 32% global urea market share in 2026, driven by large-scale corn and wheat production requiring consistent nitrogen fertilization, the world's highest DEF adoption rate under EPA emission mandates, and major domestic producers CF Industries and Nutrien serving both domestic and export markets.

- Fastest Growing Region: Asia Pacific is the fastest growing urea region through 2026–2033, with India at 4.8% CAGR as the world's largest urea importer under IFFCO/NBS subsidy programs, and Southeast Asia at 5.2% CAGR driven by Indonesia's PT Pupuk Kalimantan Timur-led agricultural urea demand.

- Dominant Product Segment: Granular urea holds 65% product form market share in 2026, dominating through superior handling characteristics for mechanized agriculture in North America, Europe, and Brazil, US$ 5–15/ton price premium over prilled equivalents, and IFA-documented specification preference by large-scale farming operations globally.

- Fastest Growing Product Segment: DEF is the fastest growing urea application segment, driven by Euro VI, EPA Tier 4, BS6, and China 6 emission mandates creating non-discretionary ISO 22241-specification 32.5% urea solution demand across expanding global commercial vehicle and construction machinery fleets.

- Key Opportunity: EU fertilizing Products Regulation-certified EEF urea products commanding 20–40% price premiums and Yara's green ammonia-derived low-carbon urea program target premium agricultural markets where regulatory and ESG sustainability mandates are structurally elevating urea product quality specifications through 2033.

DRO Analysis

Drivers - Global Food Security Imperative Driving Agricultural Urea Fertilizer Demand

The fundamental challenge of feeding a growing world population on finite agricultural land is the structural driver sustaining urea demand as the world's most widely applied nitrogen fertilizer. The Food and Agriculture Organization (FAO) of the United Nations projects global food production must increase by 50% by 2050 to meet demand from an estimated 9.7 billion people, making nitrogen fertilizer application, which directly governs crop yield potential, a non-negotiable agricultural input.

The International Fertilizer Association (IFA) documents urea as the world's most important nitrogen fertilizer by volume, accounting for approximately 55% of global nitrogen fertilizer consumption. In key agricultural markets including India, China, Brazil, and Sub-Saharan Africa, urea remains the preferred nitrogen fertilizer due to its highest nitrogen content per unit weight (46% N), convenient handling in granular and prilled form, and established agronomic application infrastructure.

Mandatory Diesel Exhaust Fluid Adoption Under Vehicle Emission Regulations

The global regulatory mandate for Selective Catalytic Reduction (SCR) technology on diesel vehicles, requiring Diesel Exhaust Fluid (DEF), also marketed as AdBlue) in Europe, as a consumable operational input, is creating structurally growing, non-discretionary urea demand from the automotive and transport sectors. The European Union's Euro VI standards, the U.S. EPA's Non-road Tier 4 and on-highway emission rules, and India's Bharat Stage VI (BS6) regulations mandate SCR systems on commercial vehicles, agricultural machinery, and construction equipment.

DEF is 32.5% high-purity urea solution consumed at approximately 3–5% of diesel fuel consumption per vehicle, creating a large and growing industrial urea demand channel that is entirely regulation-driven and therefore price-inelastic. The global commercial vehicle fleet expansion across Asia Pacific, Latin America, and Africa is continuously enlarging the DEF consumption base.

Restraints - Natural Gas Feedstock Price Volatility Compressing Urea Production Economics

Urea production is highly energy-intensive, requiring natural gas both as the hydrogen feedstock for ammonia synthesis and as process energy, making production economics acutely sensitive to natural gas price cycles. The IEA documents natural gas price fluctuations of 200–400% in European and Asian markets during the 2021–2023 energy crisis, forcing multiple European urea plants to curtail or halt production as production costs exceeded market prices.

This feedstock cost volatility creates significant margin uncertainty for urea producers without access to low-cost gas supplies, limiting investment in new capacity in gas-price-exposed regions.

Environmental Concerns and Regulatory Pressure on Nitrogen Fertilizer Use

Growing scientific and regulatory attention to the environmental impacts of excessive nitrogen fertilizer application, including nitrous oxide greenhouse gas emissions, nitrogen runoff causing waterway eutrophication, and soil acidification, is creating regulatory headwinds for urea demand in environmentally sensitive agricultural markets.

The EU's Farm to Fork Strategy targets a 20% reduction in fertilizer use by 2030, directly constraining urea demand growth in European agriculture. Environmental nutrient management regulations across the U.S. Corn Belt, the Netherlands, and China are similarly imposing application rate restrictions and enhanced efficiency requirements that limit per-hectare urea consumption growth.

Opportunities - Diesel Exhaust Fluid: Fastest Growing Non-Agricultural Urea Application

Diesel exhaust fluid represents the fastest growing individual application segment for urea, expanding well above the overall urea market CAGR as vehicle emission standards tighten progressively across emerging market vehicle fleets that are mandating SCR technology for the first time. India's BS6 standard implementation, affecting hundreds of thousands of new commercial vehicles annually, China's China 6 emission norms), and Brazil's PROCONVE P8 emission phase have each triggered step-change DEF demand creation in large vehicle markets.

The AUS32 standard governing DEF quality (ISO 22241) mandates 99.5%+ purity urea in solution, creating a premium high-specification urea demand channel. Yara International, OCI Global), and CF Industries are expanding dedicated DEF production capacity to capture this growing non-agricultural urea revenue stream, which offers more stable margins than commodity agricultural urea markets.

Enhanced Efficiency Fertilizers and Controlled-Release Urea: Premium Product Innovation

Growing regulatory pressure to reduce nitrogen fertilizer environmental impact while maintaining crop yields is creating a premium market opportunity for enhanced efficiency urea products, including polymer-coated controlled-release urea (CRU)) and urease and nitrification inhibitor-treated urea (NBPT-treated, DCD-coated). These enhanced-efficiency formulations reduce nitrogen loss through volatilization and leaching while improving nitrogen use efficiency (NUE), addressing the sustainability concerns of regulators and precision farmers.

The European Enhanced-Efficiency Fertilizers Association (EEFA) documents growing regulatory preference for EEF products under the EU Fertilizing Products Regulation (2019/1009), which provides a regulatory framework for EEF product certification and market access. These products command 20–40% price premiums over standard granular urea, enabling above-average revenue growth for producers investing in EEF formulation technology.

Category-wise Analysis

Product Form Insights

Granular urea is the dominant product form segment, accounting for approximately 65% market share in 2026. Granular urea's dominance reflects its superior handling characteristics for mechanized agricultural application, its larger, harder particles reduce dust generation, improve flow characteristics through spreader equipment, and offer greater resistance to caking during storage and transportation compared to prilled urea.

The IFA documents granular urea as the preferred specification for mechanized agriculture in North America, Europe, Brazil, and Australia, where large-scale farming operations rely on precision equipment for efficient fertilizer application.

Leading producers including Yara International, CF Industries, Nutrien, and EuroChem Group have invested in granulation technology upgrades at their major production facilities, reflecting commercial prioritization of this premium product form. Granular urea commands a US$ 5–15 per ton price premium over prilled equivalents in international trade markets.

Application Insights

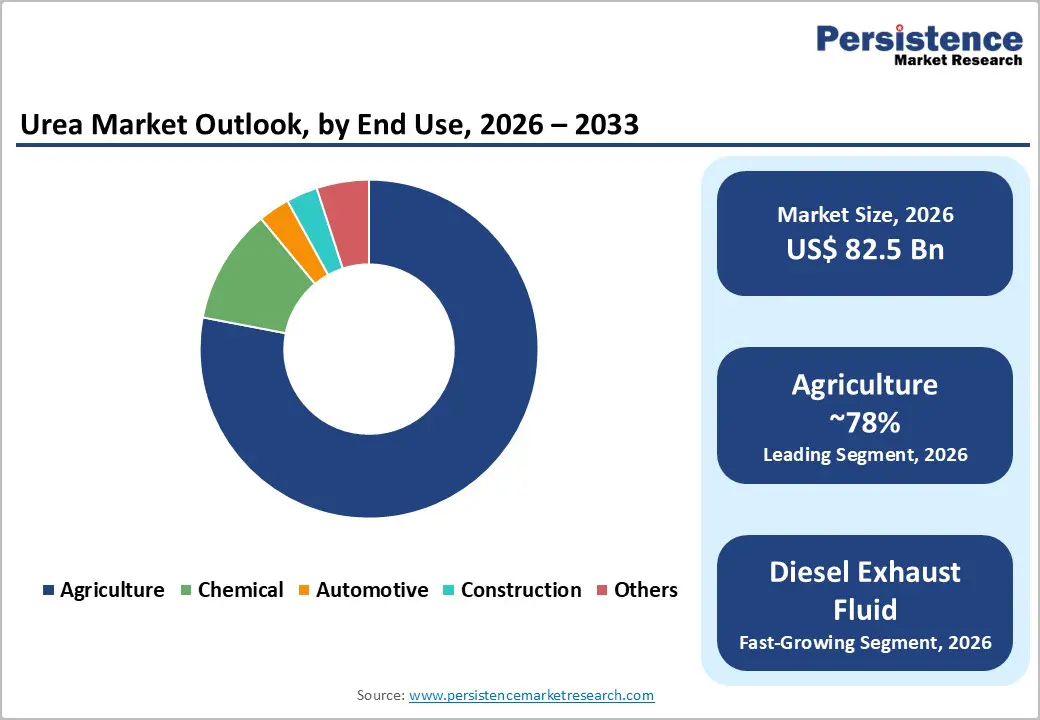

Fertilizer application is the dominant segment, accounting for approximately 75% of global urea consumption in 2026. Agricultural nitrogen fertilization is the fundamental, non-substitutable demand driver for urea globally, as the world's highest-nitrogen-content solid fertilizer at 46% N, urea is the most cost-effective nitrogen delivery mechanism per unit of applied nutrient for cereal crop production across rice, wheat, and corn cultivation globally.

The FAO documents that nitrogen fertilizer application is directly responsible for approximately 50% of global food production, a statistic that underscores urea's indispensable role in global food security. In Asia Pacific, which accounts for the majority of global urea fertilizer consumption, rice and wheat cultivation programs under national food security initiatives directly mandate consistent fertilizer application that sustains urea demand.

End-user Insights

Agriculture is the dominant End-user segment, accounting for approximately 78% of total urea demand by end-use in 2026. Global crop production's dependence on nitrogen fertilization, with the FAO attributing half of global food production to synthetic nitrogen fertilizer application, positions agriculture as the irreplaceable foundation of urea demand.

Key agricultural consuming countries including China (the world's largest urea consumer), India (the world's largest urea importer), and Brazil (the world's largest soybean producer and a major urea fertilizer importer) collectively sustain the agricultural end-use segment's commanding market position. The automotive end-use segment is the fastest growing, driven by DEF adoption under Euro VI, EPA, BS6, and China 6 emission standards expanding the DEF-consuming commercial vehicle base across all major markets.

Regional Insights

North America Urea Market Trends and Insights

North America leads the global urea market through its large-scale corn, wheat, and soybean production base requiring consistent nitrogen fertilization, among the world's highest DEF adoption rates for its extensive commercial vehicle and agricultural machinery fleet, and active domestic urea production capacity from CF Industries and Nutrien Inc. serving both domestic demand and market supply programs. Growing interest in enhanced-efficiency urea products is a key regional trend.

U.S. Urea Market Size

The United States accounts for approximately 76% of North American urea market revenue in 2026. The U.S. is one of the world's largest urea importers for agricultural use, particularly for the Corn Belt covering Iowa, Illinois, and Indiana, and a significant DEF consumer under EPA emission mandates. CF Industries Holdings and Nutrien operate major U.S. production facilities. U.S. CAGR is projected at approximately 3.1% through 2033.

Europe Urea Market Trends and Insights

Europe's urea market is shaped by the EU Farm to Fork Strategy targeting 20% fertilizer reduction by 2030), which constrains agricultural urea volume growth, while Euro VI DEF demand from Europe's extensive commercial vehicle fleet sustains non-agricultural consumption. The 2021–2022 energy crisis severely disrupted European urea production, leading to increased import dependence from Middle Eastern and Russian producers. Enhanced-efficiency urea is gaining specification share under EU fertilizing Products Regulation.

Germany Urea Market Size

Germany holds approximately 18% of the European urea market revenue in 2026. Germany's large agricultural sector and extensive commercial vehicle fleet sustain both fertilizer and DEF urea demand. BASF SE's chemical operations and Germany's active construction adhesive and resin industry generate significant industrial urea consumption. Germany's Euro VI vehicle fleet DEF compliance sustains non-agricultural demand. Germany is projected at approximately 3.0% CAGR through 2033.

U.K. Urea Market Size

The United Kingdom represents approximately 9% of European urea market revenue in 2026. UK agricultural consumption, particularly for winter wheat and spring barley nitrogen applications, is the primary demand driver, alongside Euro VI commercial vehicle DEF consumption. The UK's post-Brexit fertilizer import policy framework and growing regulatory interest in enhanced-efficiency fertilizers under the Clean Air Strategy are shaping procurement patterns. UK CAGR is projected at approximately 2.9% through 2033.

France Urea Market Size

France accounts for approximately 12% of European urea market revenue in 2026. France's active arable farming sector, with extensive wheat, barley, and rapeseed cultivation, is the primary urea consumer. France's Plan Ecophyto and CAP-aligned nitrogen management programs are directing French farmers toward enhanced-efficiency urea and precision application, sustaining consumption value while moderating volume growth. France is projected at approximately 3.1% CAGR through 2033.

Asia Pacific Urea Market Trends and Insights

Asia Pacific is the world's largest urea producing and consuming region, with China accounting for approximately 30% of global urea production capacity per IFA data, while India is the world's largest urea importer, importing over 8–10 million tons annually under its government-subsidized fertilizer program per Fertilizers Association of India (FAI) data. The region's rice, wheat, and vegetable cultivation programs are the primary urea consumption drivers, with Southeast Asia's rapidly expanding agri-food sector adding incremental demand.

India Urea Market Size

India represents approximately 22% of Asia Pacific urea market revenue in 2026 as the world's single largest urea import market. India's nutrient-based subsidy (NBS) and direct urea subsidy program, managed by the Ministry of Chemicals and Fertilizers, sustains affordable urea access for millions of smallholder farmers. Indian Farmers Fertilizers Cooperative (IFFCO) and National Fertilizers Limited are major domestic producers. India is projected at approximately 4.8% CAGR through 2033.

Japan Urea Market Size

Japan contributes approximately 5% of Asia Pacific urea market revenue in 2026. Japan's urea demand is primarily industrial and DEF-driven rather than large-scale agricultural, reflecting the country's limited arable land base. Japan's advanced commercial vehicle and construction machinery fleet under strict JNLA emission standards sustains consistent DEF urea demand. Takasugi Pharmaceutical is a specialized Japanese urea producer serving pharmaceutical and industrial sectors. Japan is projected at approximately 3.2% CAGR through 2033.

Southeast Asia Urea Market Size

Southeast Asia collectively accounts for approximately 14% of Asia Pacific urea market revenue in 2026. Indonesia, Vietnam, Thailand, and the Philippines sustain growing agricultural urea demand for rice, corn, and palm oil cultivation. PT Pupuk Kalimantan Timur, Indonesia's largest urea producer, serves both domestic agricultural demand and regional export markets. Southeast Asia is projected at approximately 5.2% CAGR through 2033, among the fastest in the global market.

Competitive Landscape

The global urea market exhibits a moderately consolidated competitive structure, with state-owned and large integrated fertilizer companies controlling substantial global production capacity. Yara International ASA, Nutrien Inc., CF Industries, EuroChem Group, and OCI Global represent major Western urea producers, while CNPC), IFFCO), and Middle Eastern sovereign producers including Qatar Fertilizer Company (QAFCO) and SAFCO dominate regional supply chains.

Key competitive differentiators include natural gas feedstock cost access, proximity to agricultural import demand markets, product form (granular premium), and enhanced-efficiency fertilizer formulation capabilities. Emerging trends include green/blue ammonia integration for low-carbon urea production and strategic long-term supply contracts with government agricultural agencies.

Key Developments

- In March 2025, Yara International ASA announced the commissioning of its green ammonia pilot facility in Norway, targeting production of low-carbon urea for European premium agricultural markets seeking certified sustainable nitrogen fertilizer with reduced scope 1 and 2 carbon footprint credentials.

- In September 2024, CF Industries Holdings, Inc. expanded its DEF (Diesel Exhaust Fluid) production capacity at its Donaldsonville, Louisiana complex, targeting growing North American commercial vehicle and off-road equipment DEF demand under EPA Tier 4 and Tier 4 Final emission compliance mandates.

- In May 2023, Nutrien Inc. launched an expanded enhanced-efficiency urea product range incorporating NBPT urease inhibitor treatment across its granular urea production, targeting North American precision agriculture markets where nitrogen use efficiency and emissions reduction are increasingly mandated by state-level environmental regulations.

Global Urea Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 69.9 Billion |

|

Current Market Value (2026) |

US$ 82.5 Billion |

|

Projected Market Value (2033) |

US$ 104.3 Billion |

|

CAGR (2026–2033) |

3.4% |

|

Leading Region |

North America, ~32% market share (2026) |

|

Dominant Category – Product Form |

Granular, ~65% share (2026) |

|

Top-Ranking Category – Application |

Fertilizer, ~75% share (2026) |

|

Incremental Opportunity (2026–2033) |

US$ 21.8 Billion |

Companies Covered in Urea Market

- Yara International ASA

- PT Pupuk Kalimantan Timur

- Qatar Fertilizer Company

- National Fertilizers Limited

- EuroChem Group AG

- Saudi Arabian Fertilizer Company

- CF Industries Holdings, Inc.

- Nutrien Inc.

- Fazaz Global Concepts LLC

- Takasugi Pharmaceutical Co., Ltd.

- IBI Scientific

- OCI Global

- BASF SE

- CNPC

- Indian Farmers Fertilisers Cooperative Limited

Frequently Asked Questions

The global urea market is projected to be valued at US$ 82.5 billion in 2026, growing from US$ 69.9 billion in 2020. The market is forecast to reach US$ 104.3 billion by 2033 at a CAGR of 3.4%, representing an absolute dollar opportunity of US$ 21.8 billion.

Primary drivers include the FAO-documented need to increase global food production by 50% by 2050 requiring nitrogen fertilizer for 50% of global food production, with urea's 46% nitrogen content making it the most cost-effective nitrogen source per applied unit.

North America leads with approximately 32% market share in 2026, driven by the U.S. Corn Belt's large-scale nitrogen fertilizer demand, the world's highest DEF per-vehicle adoption rates under EPA emission mandates, and major domestic producers CF Industries and Nutrien serving both domestic procurement and export supply programs.

Enhanced-efficiency urea products, NBPT urease inhibitor-treated and polymer-coated controlled-release formulations, represent the highest-value opportunity, commanding 20–40% price premiums over standard granular urea under EU Fertilising Products Regulation (2019/1009) certification frameworks.

Leading companies include Yara International ASA), Nutrien Inc.), CF Industries Holdings), EuroChem Group AG), OCI Global), Qatar Fertilizer Company (QAFCO)), SAFCO), PT Pupuk Kalimantan Timur), IFFCO), National Fertilizers Limited), CNPC), BASF SE), and Koch Fertilizer LLC).