- Healthcare IT

- Therapeutic Drug Monitoring Market

Therapeutic Drug Monitoring Market Size, Share and Growth Forecast, 2026 - 2033

Therapeutic Drug Monitoring Market by Product (Kits & Consumables, Instruments), Technology Platform (Immunoassay-based, Chromatography-based, Others), Drug Class (Antiepileptic drugs, Immunosuppressant, Others), and Regional Analysis for 2026 - 2033

Therapeutic Drug Monitoring Market Size and Trends Analysis

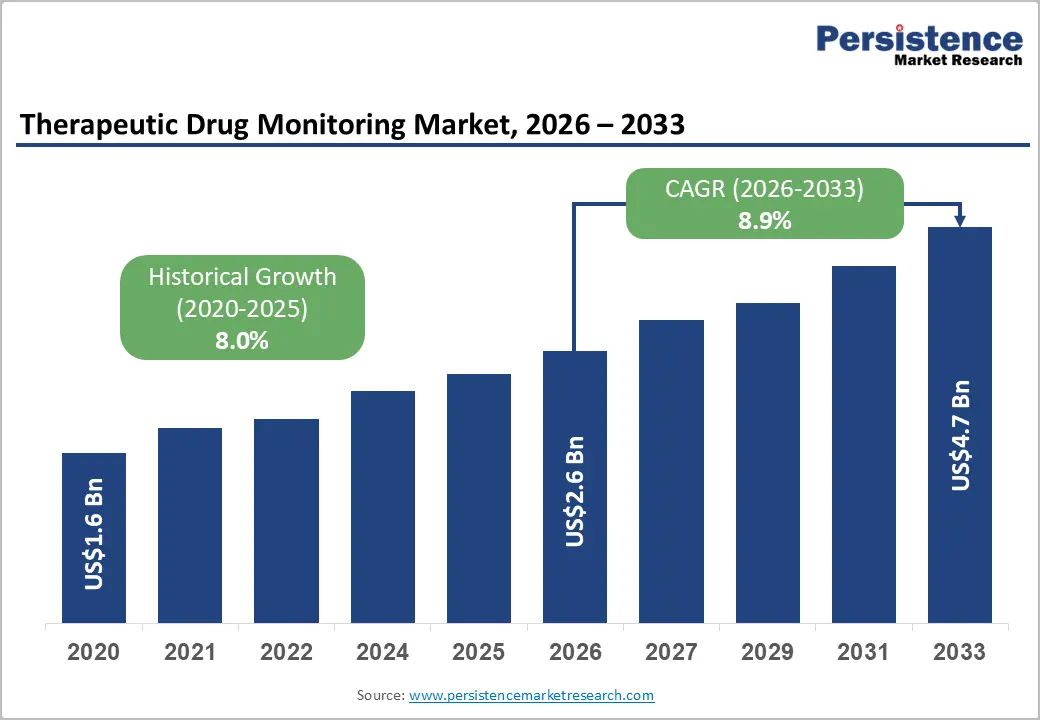

The global therapeutic drug monitoring market size is likely to be valued at US$2.6 billion in 2026 and is projected to reach US$4.7 billion by 2033, growing at a CAGR of 8.9% during the forecast period 2026 - 2033, driven by the rising demand for precision medicine, increasing use of narrow therapeutic index drugs, and stronger clinical focus on dose optimization to reduce adverse drug reactions.

Growing adoption of immunosuppressants and antiepileptic therapies further supports demand. Additionally, advancements in chromatography-based and mass spectrometry-based platforms are enhancing diagnostic accuracy, while regulatory emphasis from the U.S. FDA and EMA continues to reinforce structured therapeutic monitoring adoption globally.

Key Industry Highlights:

- Product Leadership: Kits & consumables are expected to lead with around 60% share in 2026, while instruments are likely to be the fastest-growing segment due to rising adoption of advanced diagnostic platforms.

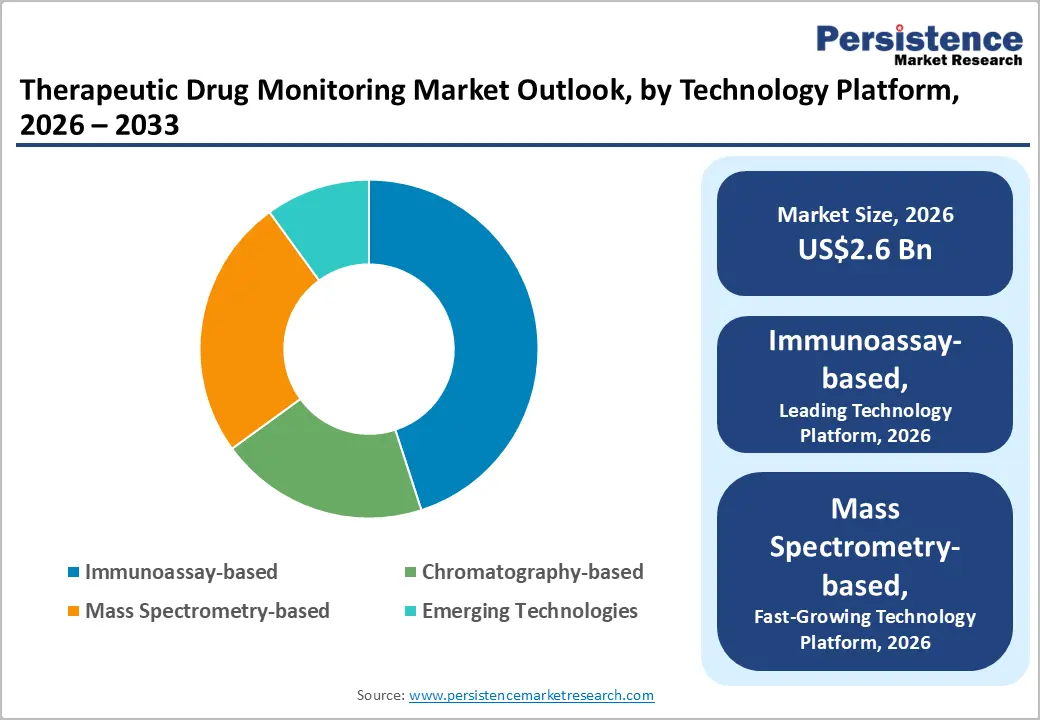

- Technology Leadership: Mass spectrometry-based platforms are projected to be the fastest-growing segment at strong double-digit growth, while immunoassay-based systems are expected to lead with approximately 45% share in 2026 due to widespread clinical use.

- Drug Class Dynamics: Antiepileptic drugs are expected to lead with nearly a 38% share in 2026, while immunosuppressants are likely to be the fastest-growing segment, driven by rising transplant procedures and chronic disease burden.

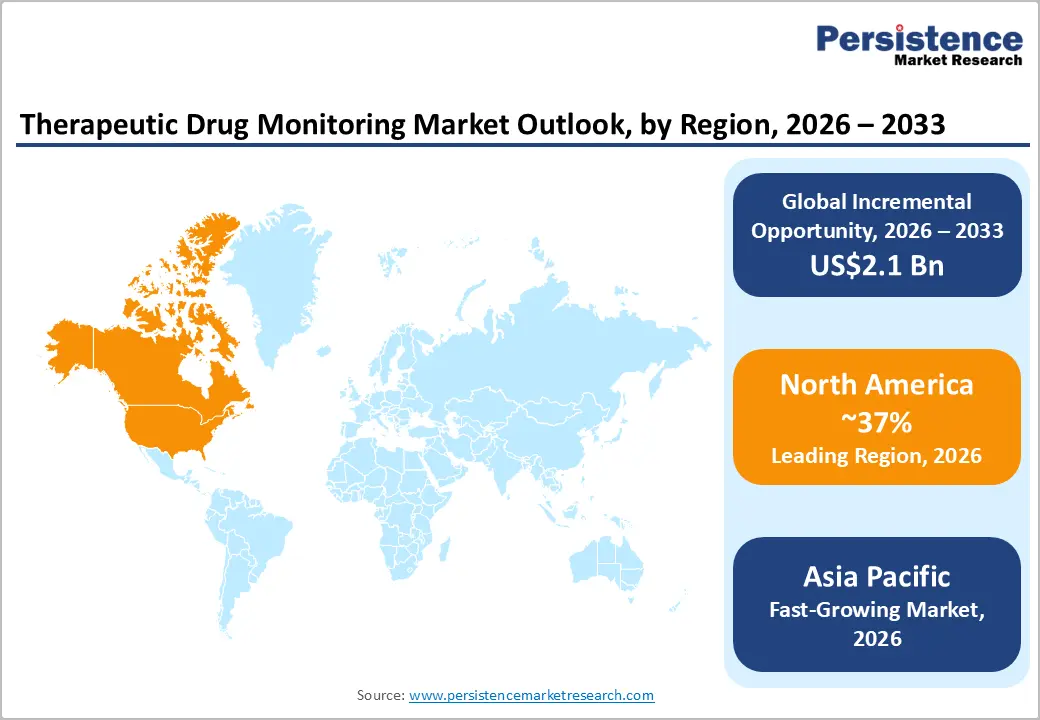

- Regional Leadership: North America is expected to lead the market with around a 35% share in 2026, while Asia Pacific is anticipated to be the fastest-growing region due to expanding healthcare infrastructure and rising diagnostic adoption.

- Competitive Environment: Market competition is driven by automation, AI-enabled diagnostics, and capacity expansion strategies by key players to strengthen laboratory efficiency and global reach.

DRO Analysis

Driver - Rising Demand for Precision Medicine and Drug Safety Optimization

The strongest driver for the Therapeutic Drug Monitoring (TDM) market is the rapid expansion of precision medicine, supported by clinical safety and regulatory frameworks. According to the U.S. FDA, adverse drug reactions impact nearly 20-25% of hospitalized patients, often linked to improper dosing of narrow-therapeutic-index drugs. TDM is increasingly applied for drugs such as immunosuppressants (e.g., tacrolimus) and antiepileptics (e.g., phenytoin) to maintain therapeutic plasma concentration within FDA-defined safety ranges.

The WHO Global Patient Safety Action Plan (2021-2030) also prioritizes medication optimization to reduce preventable harm. With over 150,000 global organ transplants annually (WHO/GODT estimates), demand for immunosuppressant monitoring is rising steadily. Growing integration of LC-MS/MS and advanced immunoassay platforms in hospital laboratories is improving dosing precision, reducing toxicity-related hospitalizations, and lowering overall treatment costs, thereby accelerating global TDM adoption.

Restraint - High Capital and Operational Cost of Advanced Analytical Systems

A major restraint for the therapeutic drug monitoring market is the high cost of advanced analytical technologies, particularly LC-MS/MS systems, which typically range between US$250,000 and US$500,000 per unit, excluding installation and validation. This limits adoption in small and mid-sized diagnostic laboratories, especially in price-sensitive healthcare systems.

Operational complexity further adds pressure, as these systems require skilled personnel and strict adherence to CLSI quality control standards, which can account for 15-20% of annual laboratory operating costs. In many developing regions, reimbursement limitations force hospitals to prioritize immunoassay testing over high-end mass spectrometry platforms, slowing adoption despite increasing demand for high-accuracy therapeutic monitoring solutions.

Opportunity - Expansion of Personalized Medicine in Emerging Economies

A key opportunity in the therapeutic drug monitoring market is the rapid expansion of personalized medicine infrastructure in emerging economies such as India, China, Brazil, and Southeast Asia. Rising prevalence of chronic diseases, including epilepsy affecting over 10 million patients in India (ICMR estimates), is increasing the need for dose-optimized therapies requiring routine monitoring.

India performs around 12,000-15,000 organ transplants annually, while China continues to scale transplant programs, significantly boosting demand for immunosuppressant monitoring. Government initiatives such as Ayushman Bharat and China’s hospital modernization programs are accelerating adoption of automated immunoassay systems. This is expected to generate an incremental opportunity of US$800-1,000 million by 2033, supported by laboratory automation and expansion of centralized diagnostic networks.

Category-wise Analysis

Product Insights

Kits & consumables are expected to dominate the therapeutic drug monitoring market with an estimated 60% share in 2026, owing to their recurring use in routine therapeutic testing. Reagents, assay kits, calibrators, and controls are required for every test cycle, creating consistent demand across hospital and reference laboratories. Their leadership is supported by rising monitoring volumes for immunosuppressants and antiepileptic drugs, particularly as global organ transplant procedures exceed 150,000 annually, according to the Global Observatory on Donation and Transplantation (GODT).

Instruments are projected to be the fastest-growing product segment, registering an estimated 9% CAGR through 2033. Growth is driven by increasing adoption of LC-MS/MS and chromatography systems for high-precision drug quantification. Large healthcare systems in North America and Europe are expanding advanced laboratory capabilities to support precision medicine initiatives, while automation and AI-enabled workflows are improving throughput and reducing analytical variability.

Technology Platform Insights

Immunoassay-based platforms are anticipated to lead the market with approximately a 45% share in 2026, supported by their cost efficiency, rapid turnaround times, and widespread availability. These systems are routinely used for monitoring antiepileptic and immunosuppressant drugs in hospital laboratories. Their compatibility with automated analyzers makes them suitable for high-volume testing environments, helping maintain their strong position despite increasing competition from advanced analytical technologies.

Mass spectrometry-based platforms are expected to witness the fastest growth, expanding at an estimated 9.2% CAGR during 2026 - 2033. Their superior sensitivity and specificity make them increasingly preferred for transplant medicine and complex pharmacokinetic assessments. Adoption is accelerating as hospitals seek improved analytical accuracy, while regulatory emphasis on medication safety and therapeutic optimization continues to support the transition toward LC-MS/MS-based testing.

Drug Class Insights

Antiepileptic drugs are projected to remain the leading drug class, accounting for approximately 38% of market revenue in 2026. Their dominance stems from the need for frequent monitoring of drugs such as phenytoin and valproic acid, which have narrow therapeutic windows. According to the World Health Organization (WHO), epilepsy affects more than 50 million people globally, creating a substantial and recurring demand for therapeutic drug monitoring across neurology care settings.

Immunosuppressants are expected to be the fastest-growing drug class segment, recording an estimated 9.8% CAGR through 2033. Rising organ transplantation volumes and increasing autoimmune disease management are key growth drivers. Data from the Global Observatory on Donation and Transplantation indicate that transplant procedures continue to increase worldwide, requiring long-term monitoring of drugs such as tacrolimus and cyclosporine to prevent graft rejection and ensure treatment efficacy.

Regional Analysis

North America Therapeutic Drug Monitoring Market Trends

North America is expected to account for approximately 37% of the global therapeutic drug monitoring market in 2026, driven by the region's strong focus on precision medicine, transplant care, and medication safety programs. The region records some of the world's highest healthcare spending levels, with the U.S. alone spending over US$5 trillion annually on healthcare. The growing prevalence of chronic diseases, which affect nearly 6 in 10 U.S. adults according to the CDC, is increasing the use of narrow therapeutic index drugs that require regular monitoring.

As a result, healthcare providers are increasingly integrating therapeutic drug monitoring into routine clinical workflows to improve treatment outcomes and reduce adverse drug reactions.

U.S. Therapeutic Drug Monitoring Market Trends

The U.S. is projected to hold nearly 81% of the North America market in 2026. The country performs over 45,000 organ transplants annually, creating substantial demand for immunosuppressant monitoring. Continued adoption of LC-MS/MS systems, FDA-supported precision medicine initiatives, and increasing investment in hospital laboratory automation are further strengthening market growth. The expanding use of personalized treatment protocols is making therapeutic drug monitoring a critical component of patient management.

Canada Therapeutic Drug Monitoring Market Trends

Canada is expected to account for around 19% of the regional market. The country's emphasis on personalized healthcare, growing transplant activity, and increasing laboratory modernization investments are supporting adoption. Public healthcare funding and the expanding use of advanced diagnostics in major provinces are helping integrate therapeutic drug monitoring into routine patient care, particularly for chronic disease management and specialty therapeutics.

Europe Therapeutic Drug Monitoring Market Trends

Europe is anticipated to represent approximately 29% of the global TDM market in 2026, supported by strong regulatory oversight and widespread access to healthcare services. The region's rapidly aging population is increasing demand for long-term therapies that require dose optimization and safety monitoring. According to the European Commission, individuals aged 65 years and older already account for more than 21% of the EU population, driving higher utilization of immunosuppressants, antiepileptics, and other monitored therapies. This demographic trend is making therapeutic drug monitoring increasingly important for reducing medication-related complications.

Germany Therapeutic Drug Monitoring Market Trends

Germany is expected to account for nearly 34% of the Europe market in 2026. As Europe's largest healthcare market, Germany continues to invest heavily in laboratory automation and precision medicine infrastructure. The country performs some of the highest numbers of transplant procedures in Europe, increasing demand for immunosuppressant monitoring. Strong adoption of mass spectrometry-based testing across university hospitals further supports market expansion.

U.K. Therapeutic Drug Monitoring Market Trends

The U.K. is projected to hold approximately 18% of the regional market. Increasing adoption of pharmacogenomics through NHS initiatives is supporting personalized dosing strategies. Investments in diagnostic modernization and AI-enabled laboratory workflows are enhancing testing efficiency, while the rising prevalence of chronic neurological disorders is driving greater use of therapeutic drug monitoring across hospital networks.

Asia Pacific Therapeutic Drug Monitoring Market Trends

Asia Pacific is expected to account for approximately 25% of the global therapeutic drug monitoring market in 2026 and is projected to be the fastest-growing regional market through 2033. The region's large patient population, rising burden of chronic diseases, and expanding healthcare access are significantly increasing demand for therapeutic monitoring. According to the WHO, Asia carries a substantial share of the global epilepsy burden, while growing transplant activity across major economies is increasing the need for immunosuppressant monitoring.

Healthcare modernization programs and diagnostic infrastructure investments are enabling broader adoption of advanced monitoring technologies.

China Therapeutic Drug Monitoring Market Trends

China is anticipated to hold nearly 38% of the Asia Pacific market in 2026. Government-backed precision medicine programs, hospital modernization initiatives, and increasing deployment of advanced diagnostic technologies are driving growth. As one of the world's largest healthcare markets, China is rapidly expanding tertiary care capacity, creating greater demand for therapeutic monitoring in oncology, transplant medicine, and chronic disease management.

India Therapeutic Drug Monitoring Market Trends

India is expected to account for approximately 17% of the regional market in 2026 and is among the fastest-growing countries in the region. The country performs an estimated 12,000-15,000 organ transplants annually, creating significant demand for immunosuppressant monitoring. Additionally, with more than 10 million epilepsy patients, according to ICMR estimates, the need for antiepileptic drug monitoring continues to rise. Government initiatives such as Ayushman Bharat and increasing investments in diagnostic laboratory networks are accelerating adoption of therapeutic drug monitoring technologies across the country.

Competitive Landscape

The global therapeutic drug monitoring market is moderately consolidated, with leading players such as Thermo Fisher Scientific, Roche, Abbott, and Siemens Healthineers holding a significant share of market revenue. These companies leverage broad diagnostic portfolios, strong hospital relationships, and continuous investments in immunoassay, mass spectrometry, and laboratory automation technologies to maintain their competitive position.

The specialized players, such as Waters Corporation, Agilent Technologies, and Bio-Rad Laboratories, are strengthening their presence in high-precision therapeutic monitoring applications. High regulatory requirements, capital investment needs, and clinical validation standards create barriers to entry, while growing adoption of precision medicine, AI-enabled diagnostics, and laboratory automation is encouraging strategic partnerships and gradual market consolidation.

Key Industry Developments

- In April 2026, Labcorp launched the first FDA-cleared rapid fentanyl test manufactured in the United States, capable of delivering results in approximately 10 minutes. The innovation strengthened rapid toxicology and therapeutic monitoring capabilities in emergency and acute care settings while enabling faster clinical decision-making.

- In March 2025, Bruker Corporation expanded its therapeutic drug monitoring portfolio by integrating RECIPE ClinMass® and ClinDART® assay kits with its EVOQ® mass spectrometry platform. The development enhanced access to standardized LC-MS/MS-based testing workflows and improved efficiency for high-precision drug monitoring applications.

Companies Covered in Therapeutic Drug Monitoring Market

- Thermo Fisher Scientific

- Roche

- Abbott

- Siemens Healthineers

- Danaher Corporation

- Bio-Rad Laboratories

- Agilent Technologies

- Waters Corporation

- PerkinElmer

- Sysmex Corporation

- Ortho Clinical Diagnostics

- Becton Dickinson

- DiaSorin

Frequently Asked Questions

The global therapeutic drug monitoring market is projected to reach US$2.6 billion in 2026.

Rising adoption of precision medicine, increasing use of narrow therapeutic index drugs, and growing demand for medication safety drive market growth.

The therapeutic drug monitoring market is expected to grow at a CAGR of 8.9% from 2026 to 2033.

Emerging economies, expanding transplant procedures, and increasing investment in personalized medicine create significant growth opportunities.

Key players include Thermo Fisher Scientific, Roche, Abbott, and Siemens Healthineers.