- Processed Food

- Sugar-free Confectionery Market

Sugar-free Confectionery Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Sugar-free Confectionery Market by Product Type (Chocolate Confectionery, Sweet & Candy Confectionery, Chewing Gum, Mints, Toffees & Caramels, and Others), by Ingredient (Natural Sweeteners, Artificial Sweeteners, and Sugar Alcohols (Polyols)) by Distribution Channel (Hypermarkets & Supermarkets, Convenience Stores, Pharmacies, Online Retail, Specialty Stores, and Others), and Regional Analysis from 2026 - 2033

Sugar-free Confectionery Market Share and Trend Analysis

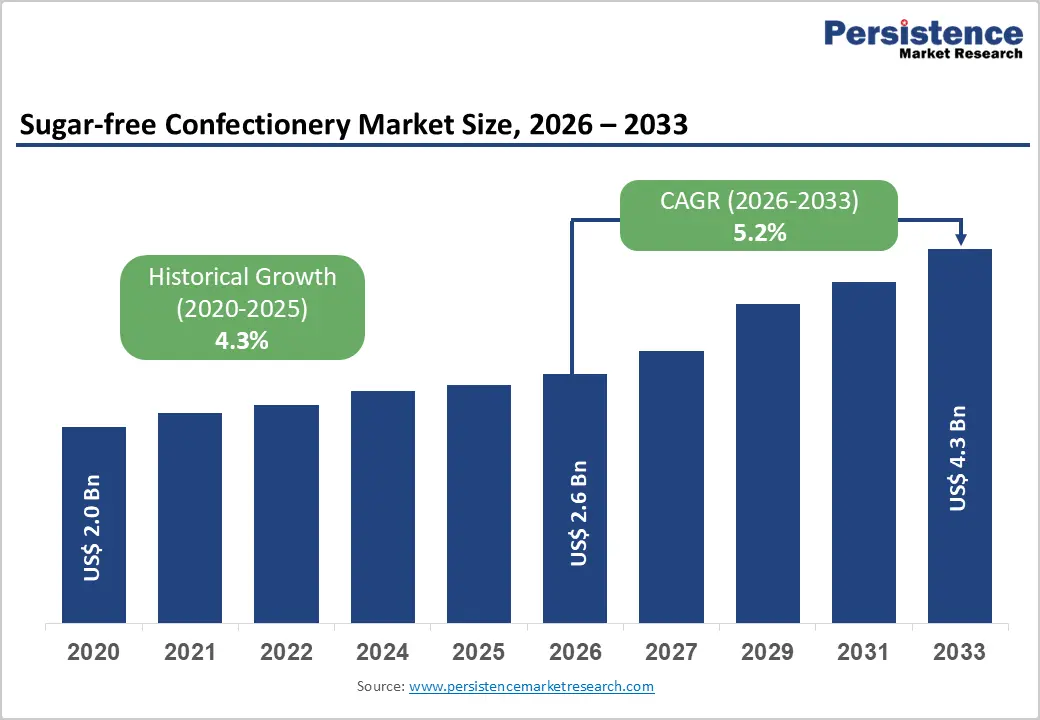

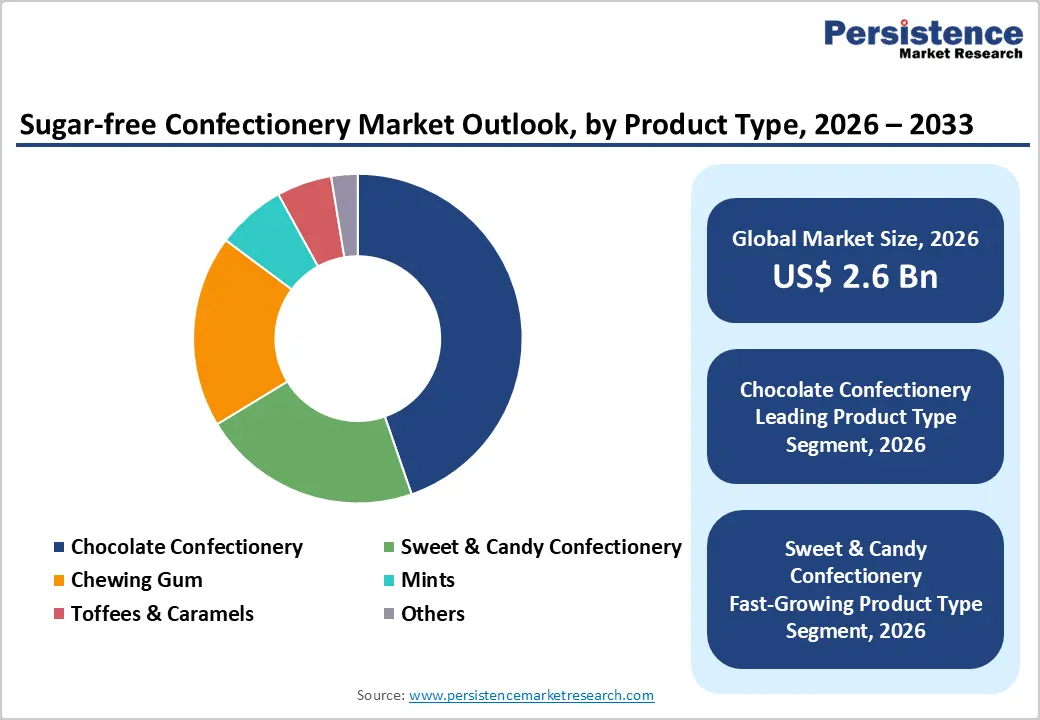

The global sugar-free confectionery market size is estimated to grow from US$ 2.6 billion in 2026 to US$ 4.3 billion by 2033. The market is projected to record a CAGR of 5.2% during the forecast period from 2026 to 2033. Rising preference for low-sugar and healthier indulgence options is significantly shaping consumption patterns across confectionery categories.

Consumers are actively reducing sugar intake while still seeking enjoyable snacking experiences, driving demand for sugar-free chocolates, candies, and gums. Products formulated with alternatives such as stevia, erythritol, and monk fruit are gaining traction due to improved taste profiles and lower glycemic impact. These offerings are increasingly integrated into daily consumption, particularly among diabetic, fitness-oriented, and weight-conscious individuals.

Key Industry Highlights:

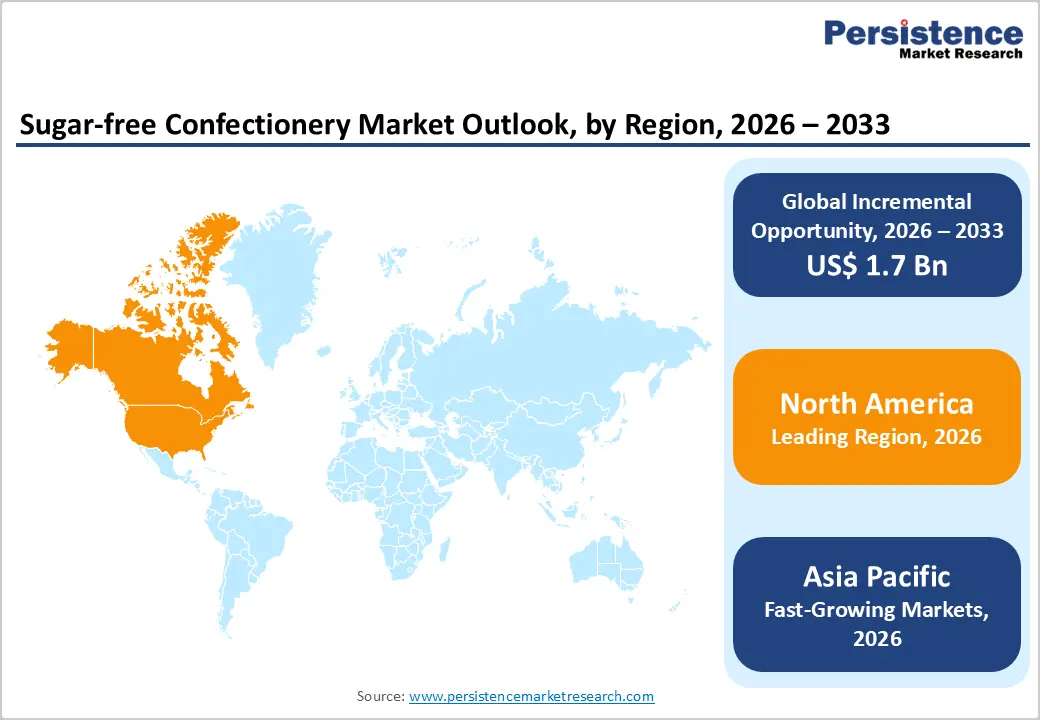

- Leading Region: North America accounts for 46.7% of the global market, supported by strong health awareness, high adoption of low-sugar diets, advanced retail infrastructure, and continuous product innovation.

- Fastest-Growing Region: Asia Pacific is emerging as the fastest-growing region, driven by rising disposable incomes, increasing diabetes prevalence, expanding urban population, and growing penetration of modern retail channels

- Leading Product Type Segment: Chocolate Confectionery dominates with 44.7% share, attributed to strong consumer preference for indulgent yet low-sugar alternatives and continuous innovation in sugar-free chocolate formulations.

- Fastest-Growing Product Type Segment: Sweet & Candy Confectionery is witnessing rapid expansion due to increasing demand for variety, evolving taste preferences, and introduction of innovative sugar-free candy formats.

- Leading Ingredient Segment: Natural Sweeteners lead with 38.5% share, supported by rising demand for clean-label products, plant-based ingredients, and favorable regulatory trends.

- Fastest-Growing Ingredient Segment: Artificial Sweeteners are expanding steadily due to cost efficiency, wider availability, and their ability to support large-scale confectionery production.

| Key Insights | Details |

|---|---|

|

Sugar-free Confectionery Market Size (2026E) |

US$ 2.6 Bn |

|

Market Value Forecast (2033F) |

US$ 4.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Dynamics

Driver – Rising Health Awareness and Shift Toward Low-Sugar Consumption Patterns

The increasing consumer shift toward reduced-sugar and calorie-conscious diets, and the incidences of lifestyle disorders such as diabetes, obesity, and metabolic syndrome has significantly altered purchasing behavior, pushing consumers to seek alternatives that deliver indulgence without excessive sugar intake. Sugar-free confectionery products, including chocolates, candies, and gums, are gaining traction as they align with these evolving health priorities while still satisfying taste expectations.

Advancements in sweetener technologies have further strengthened market adoption. Ingredients such as stevia, erythritol, and monk fruit now offer improved taste profiles, minimizing the bitterness or aftertaste traditionally associated with sugar substitutes. This has enabled manufacturers to replicate the sensory experience of conventional confectionery more effectively.

Additionally, increased penetration of fitness-oriented lifestyles, ketogenic diets, and diabetic-friendly product positioning is expanding the consumer base beyond niche segments. Retailers are also allocating greater shelf space to sugar-free variants, supported by targeted marketing campaigns emphasizing clean-label claims and functional benefits. As health-conscious consumption becomes mainstream, sugar-free confectionery continues to gain momentum across both developed and emerging markets.

Restraints – Formulation Challenges, Cost Pressures, and Consumer Perception Barriers

Despite strong growth potential, the industry faces notable constraints related to formulation complexity and pricing dynamics. Replicating the taste, texture, and mouthfeel of traditional sugar-based confectionery remains a technical challenge, as sugar plays multiple functional roles beyond sweetness, including bulk, preservation, and structure. While alternative sweeteners have improved significantly, achieving consistent product quality across different formats still requires advanced processing capabilities and higher R&D investments.

Cost considerations also act as a limiting factor. Natural sweeteners and specialty polyols often carry higher input costs compared to conventional sugar, leading to premium pricing of finished products. This can restrict adoption in price-sensitive markets, where consumers may prioritize affordability over health attributes.

Additionally, lingering consumer skepticism around artificial sweeteners and concerns regarding potential side effects can influence purchasing decisions. Regulatory scrutiny around labeling, health claims, and permissible ingredient usage further adds to compliance complexity. These combined factors create operational and market-entry challenges, potentially slowing down widespread adoption in certain regions despite increasing awareness.

Opportunity – Expansion of Natural Sweeteners, Premium Product Innovation, and Digital Retail Growth

A significant growth avenue lies in the accelerated adoption of natural and plant-derived sweeteners, which are reshaping product development strategies across the confectionery landscape. As consumers increasingly demand transparency and clean-label ingredients, manufacturers are investing in formulations that incorporate stevia, monk fruit, and other naturally sourced alternatives. This shift enhances product appeal and allows brands to position themselves within premium and health-focused segments.

Innovation in product offerings presents another key opportunity. Food businesses are introducing functional confectionery enriched with added benefits such as vitamins, probiotics, and energy-boosting ingredients, transforming traditional sweets into value-added products. Premiumization, including artisanal sugar-free chocolates and organic variants, is also gaining traction among affluent consumers seeking high-quality indulgence.

Furthermore, the rapid expansion of e-commerce and direct-to-consumer channels is reshaping distribution dynamics. Digital platforms enable niche brands to scale efficiently, improve consumer reach, and offer personalized product experiences. Emerging markets, supported by rising disposable incomes and increasing health awareness, provide additional untapped potential. Collectively, these factors position the industry for sustained innovation-driven growth in the coming years.

Category-wise Analysis

By Product Type, Chocolate Confectionery Maintains Market Leadership Driven by Strong Consumer Preference and Product Innovation

Chocolate confectionery is projected to hold 44.7% of the global sugar-free confectionery market in 2026, securing its position as the leading segment. Its dominance is largely attributed to strong consumer inclination toward indulgent yet healthier alternatives, where sugar-free chocolates offer a balance between taste and calorie reduction. Continuous advancements in formulation technologies, including the use of stevia, erythritol, and other natural sweeteners, have significantly improved taste profiles and texture, overcoming earlier limitations associated with sugar-free products.

Additionally, manufacturers are actively expanding premium product lines, including dark, organic, and functional chocolates infused with added nutrients or health benefits. The segment also benefits from high visibility across retail shelves and strong brand penetration globally. Increasing demand for guilt-free snacking, especially among diabetic and fitness-conscious consumers, continues to reinforce chocolate confectionery’s leading position across both developed and emerging markets.

By Ingredient, Natural Sweeteners Segment Dominates Owing to Clean-label Demand and Regulatory Preference

Natural sweeteners are expected to account for 38.5% of the global market in 2026, emerging as the dominant ingredient segment. This leadership is primarily driven by growing consumer preference for clean-label and plant-based ingredients, as well as increasing skepticism toward synthetic additives. Sweeteners such as stevia and monk fruit are gaining widespread acceptance due to their low glycemic index and perceived health benefits. Regulatory support across major regions is further accelerating the transition toward naturally derived alternatives, particularly as governments push for reduced sugar consumption and transparent labeling practices.

In addition, advancements in extraction and blending technologies have enhanced the taste and stability of natural sweeteners, making them more viable for large-scale confectionery production. Food manufacturers are increasingly reformulating their product portfolios to align with these evolving preferences, while also leveraging sustainability narratives. This shift positions natural sweeteners as a critical growth driver within the ingredient landscape of sugar-free confectionery.

By Distribution Channel, Hypermarkets & Supermarkets Lead Due to Wide Product Availability and Strong Consumer Footfall

Hypermarkets and supermarkets are anticipated to capture 39.8% of total market share in 2026, maintaining their dominance in the distribution landscape. Their leadership is supported by extensive shelf space, diverse product assortments, and the ability to cater to both mass-market and premium consumer segments. These retail formats offer strong product visibility and enable consumers to compare multiple brands and formulations, which is particularly important in the evolving sugar-free category.

In addition, strategic product placement, in-store promotions, and sampling initiatives play a key role in influencing purchasing decisions. The presence of established retail chains across developed and emerging economies ensures consistent accessibility to sugar-free confectionery products. While online channels are gaining traction, physical retail continues to dominate due to immediate product availability and consumer trust. The expansion of organized retail infrastructure, particularly in developing regions, further strengthens the position of hypermarkets and supermarkets as the primary sales channel.

Regional Insights

North America Sugar-free Confectionery Market Trends

North America is projected to account for 46.7% of the global sugar-free confectionery market in 2026, establishing itself as the leading regional market. The United States plays a pivotal role, driven by high awareness regarding sugar reduction, widespread prevalence of diabetes, and strong demand for low-calorie indulgent products. Consumers in the region increasingly seek healthier alternatives without compromising on taste, which has accelerated the adoption of sugar-free chocolates, candies, and gums.

The presence of major confectionery manufacturers and continuous product innovation further contribute to market expansion. Companies are actively investing in reformulation strategies, incorporating natural sweeteners and functional ingredients to cater to evolving consumer expectations.

Well-developed retail infrastructure, including supermarkets, specialty health stores, and online platforms, ensures high product accessibility. Rising interest in keto, low-carb, and diabetic-friendly diets also supports demand growth. Marketing strategies focused on clean-label claims and premium positioning continue to influence purchasing behavior, reinforcing North America’s stronghold in both value and volume consumption.

Europe Sugar-free Confectionery Market Trends

Europe is expected to witness steady growth in the sugar-free confectionery market in 2026, supported by a well-established regulatory framework and strong consumer inclination toward healthier food choices. Countries such as Germany, the United Kingdom, France, Italy, Spain, and the Netherlands represent key markets, characterized by high awareness of sugar-related health concerns and increasing demand for reduced-sugar alternatives. Stringent regulations regarding sugar content and labeling standards are encouraging manufacturers to innovate and reformulate existing products. Consumers in the region show a clear preference for natural ingredients, sustainability, and ethical sourcing, which is driving demand for clean-label sugar-free confectionery.

Retailers are expanding their private-label portfolios, offering competitively priced sugar-free options alongside branded products. Furthermore, advancements in packaging and product preservation are improving shelf life and quality, enhancing overall consumer experience. The integration of premium and organic product lines also contributes to market growth, positioning Europe as a mature yet innovation-driven market.

Asia Pacific Sugar-free Confectionery Market Trends

Asia Pacific sugar-free confectionery market is projected to reach a CAGR of approximately 7.0% between 2026 and 2033, making it the fastest-growing regional segment globally. Growth is primarily fueled by rapid urbanization, rising disposable incomes, and increasing awareness of lifestyle-related health issues such as diabetes and obesity. Countries including China, India, Japan, and South Korea are witnessing a gradual shift in consumer preferences toward healthier snacking options. The region benefits from a large population base and expanding middle-class segment, creating substantial demand potential for sugar-free products. Manufacturers are increasingly introducing affordable and region-specific product variants to cater to diverse taste preferences.

Additionally, the rapid expansion of modern retail formats and e-commerce platforms is improving product accessibility across urban and semi-urban areas. Government initiatives promoting healthier diets and sugar reduction are further supporting market development. Continuous innovation in flavors, formats, and packaging, combined with aggressive marketing strategies, is positioning Asia Pacific as a key growth engine in the global sugar-free confectionery industry.

Competitive Landscape

The global sugar-free confectionery market is highly competitive, with strong participation from The Hershey Company, Société des Produits Nestlé S.A., Lily’s Sweets LLC, ChocZero Inc., and SmartSweets Inc. These companies leverage advanced ingredient sourcing, sugar substitute innovation, and strong retail partnerships while focusing on clean-label formulations and reduced-calorie offerings. Growing health awareness, rising diabetic population, and demand for functional indulgence are driving investments in natural sweeteners, product innovation, premiumization, private-label expansion, and e-commerce distribution across global retail channels.

Key Developments:

- In February 2026, Sugar Free D’lite launched a Valentine’s campaign highlighting women as key decision-makers, leveraging established emotional associations around gifting and mindful indulgence. The initiative also aimed to strengthen brand positioning by connecting with modern consumers seeking healthier yet emotionally meaningful choices.

- In October 2024, Zydus Wellness expanded its Sugar-Free portfolio into the packaged foods category with the introduction of Sugar-Free D’lite cookies. This launch is designed to provide consumers with a no-added-sugar indulgence, enabling them to enjoy sweet snacks while managing calorie intake and maintaining a healthier lifestyle.

Companies Covered in Sugar-free Confectionery Market

- The Hershey Company

- Société des Produits Nestlé S.A.

- Lily’s Sweets LLC

- ChocZero Inc.

- SmartSweets Inc.

- See’s Candy Shops, Inc.

- August Storck KG

- Chocoladefabriken Lindt & Sprüngli AG

- Perfetti Van Melle Group B.V.

- Albanese Confectionery Group, Inc.

- Asher’s Chocolate Co.

- Dr. John’s Healthy Sweets

- Atkinson Candy Company

- Abdallah Candies Inc.

- Xlear, Inc.

- Others

Frequently Asked Questions

The global sugar-free confectionery market is projected to be valued at US$ 22.6 Bn in 2026.

Rising diabetes prevalence, increasing health consciousness, and growing demand for low-calorie/clean-label alternatives are primarily driving the sugar-free confectionery market.

The global sugar-free confectionery market is poised to witness a CAGR of 5.2% between 2026 and 2033.

Innovation in natural sweeteners, premium product development, and expansion of online/D2C retail channels are creating key growth opportunities in the market.

The Hershey Company, Société des Produits Nestlé S.A., Lily’s Sweets LLC, ChocZero Inc., and SmartSweets Inc. are some of the key players in the sugar-free confectionery market.