- Executive Summary

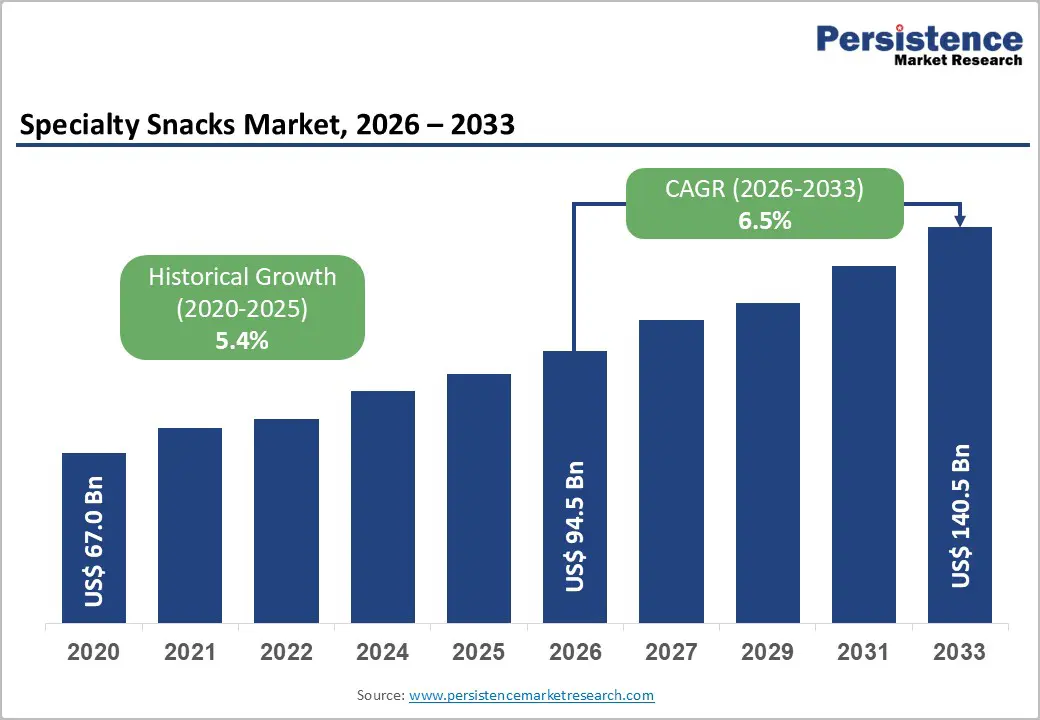

- Global Specialty Snacks Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 – 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors – Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2025A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Distribution Channel

- Global Specialty Snacks Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Current Market Size (US$ Bn) Analysis and Forecast, 2026 – 2033

- Global Specialty Snacks Market Outlook: Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Product Type, 2020 – 2025

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 – 2033

- Chips

- Nuts & Seeds

- Popcorn

- Pretzels

- Market Attractiveness Analysis: Product Type

- Global Specialty Snacks Market Outlook: Distribution Channel

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Distribution Channel, 2020 – 2025

- Current Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2026 – 2033

- Supermarkets

- Online Stores

- Convenience Stores

- Specialty Stores

- Market Attractiveness Analysis: Distribution Channel

- Global Specialty Snacks Market Outlook: Flavor

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Flavor, 2020 – 2025

- Current Market Size (US$ Bn) Analysis and Forecast, By Flavor, 2026 – 2033

- Savory

- Sweet

- Spicy

- Market Attractiveness Analysis: Flavor

- Key Highlights

- Global Specialty Snacks Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2020 – 2025

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2026 – 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Specialty Snacks Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Product Type

- By Distribution Channel

- By Flavor

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- U.S.

- Canada

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 – 2033

- Chips

- Nuts & Seeds

- Popcorn

- Pretzels

- Current Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2026 – 2033

- Supermarkets

- Online Stores

- Convenience Stores

- Specialty Stores

- Current Market Size (US$ Bn) Analysis and Forecast, By Flavor, 2026-2033

- Savory

- Sweet

- Spicy

- Market Attractiveness Analysis

- Europe Specialty Snacks Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Product Type

- By Distribution Channel

- Flavor

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 – 2033

- Chips

- Nuts & Seeds

- Popcorn

- Pretzels

- Current Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2026 – 2033

- Supermarkets

- Online Stores

- Convenience Stores

- Specialty Stores

- Current Market Size (US$ Bn) Analysis and Forecast, By Flavor, 2026-2033

- Savory

- Sweet

- Spicy

- Market Attractiveness Analysis

- East Asia Specialty Snacks Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Product Type

- By Distribution Channel

- By Flavor

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- China

- Japan

- South Korea

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 – 2033

- Chips

- Nuts & Seeds

- Popcorn

- Pretzels

- Current Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2026 – 2033

- Supermarkets

- Online Stores

- Convenience Stores

- Specialty Stores

- Current Market Size (US$ Bn) Analysis and Forecast, By Flavor, 2026-2033

- Savory

- Sweet

- Spicy

- Market Attractiveness Analysis

- South Asia & Oceania Specialty Snacks Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Product Type

- By Distribution Channel

- By Flavor

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 – 2033

- Chips

- Nuts & Seeds

- Popcorn

- Pretzels

- Current Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2026 – 2033

- Supermarkets

- Online Stores

- Convenience Stores

- Specialty Stores

- Current Market Size (US$ Bn) Analysis and Forecast, By Flavor, 2026-2033

- Savory

- Sweet

- Spicy

- Market Attractiveness Analysis

- Latin America Specialty Snacks Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Product Type

- By Distribution Channel

- By Flavor

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 – 2033

- Chips

- Nuts & Seeds

- Popcorn

- Pretzels

- Current Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2026 – 2033

- Supermarkets

- Online Stores

- Convenience Stores

- Specialty Stores

- Current Market Size (US$ Bn) Analysis and Forecast, By Flavor, 2026-2033

- Savory

- Sweet

- Spicy

- Market Attractiveness Analysis

- Middle East & Africa Specialty Snacks Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Product Type

- By Distribution Channel

- By Flavor

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2026 – 2033

- Chips

- Nuts & Seeds

- Popcorn

- Pretzels

- Current Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2026 – 2033

- Supermarkets

- Online Stores

- Convenience Stores

- Specialty Stores

- Current Market Size (US$ Bn) Analysis and Forecast, By Flavor, 2026-2033

- Savory

- Sweet

- Spicy

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

- PepsiCo ,Inc.

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- Mondelez International, Inc.

- General Mills, Inc.

- Kellanova

- Intersnack Group GmbH & Co. KG

- Conagra Brands, Inc.

- Hain Celestial Group, Inc.

- The Hershey Company

- Three Squirrels Inc.

- Bestore Co., Ltd.

- Tyson Foods, Inc.

- Primal Kitchen

- Hippeas

- RXBAR

- Saffron Road Food

- PepsiCo ,Inc.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Processed Food

- Specialty Snacks Market

Specialty Snacks Market Size, Share, and Growth Forecast, 2026 - 2033

Specialty Snacks Market by Product Type (Chips, Nuts & Seeds, Popcorn, Pretzels), Distribution Channel (Supermarkets, Convenience Stores, Online Stores, Specialty Stores), Flavor (Savory, Sweet, Spicy), and Regional Analysis for 2026-2033

Key Industry Highlights

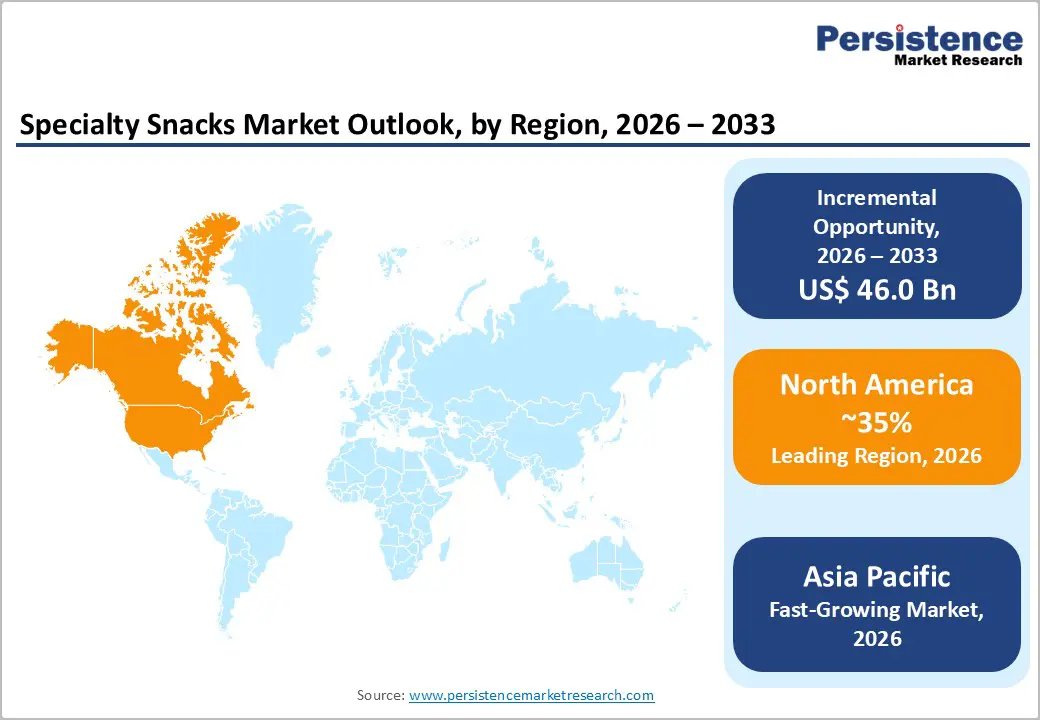

- Dominant Region: North America is poised to command around 35% market share in 2026, supported by robust consumer spending on premium and innovative food items.

- Fastest-growing Market: The Asia Pacific market is expected to grow the fastest through 2033, on the back increasing consumption of premium snack offerings by middle-class households.

- Product Type Leadership: Nuts & seeds are likely to lead with approximately 45% revenue share in 2026, whereas chips are set to be the fastest-growing segment during the 2026-2033 forecast period.

- Distribution Channel Dominance: Supermarkets are slated to capture roughly 52% of the revenue share in 2026, and online stores are expected to post the highest 2026-2033 CAGR.

- June 2025: Amza Superfoods showcased its award-winning Tibetan Tsamba snacks and flaxseed butters at the Summer Fancy Food Show in New York, highlighting nutrient-dense, whole-food products made from ancient grains and sustainable ingredients to promote modern wellness.

| Key Insights | Details |

|---|---|

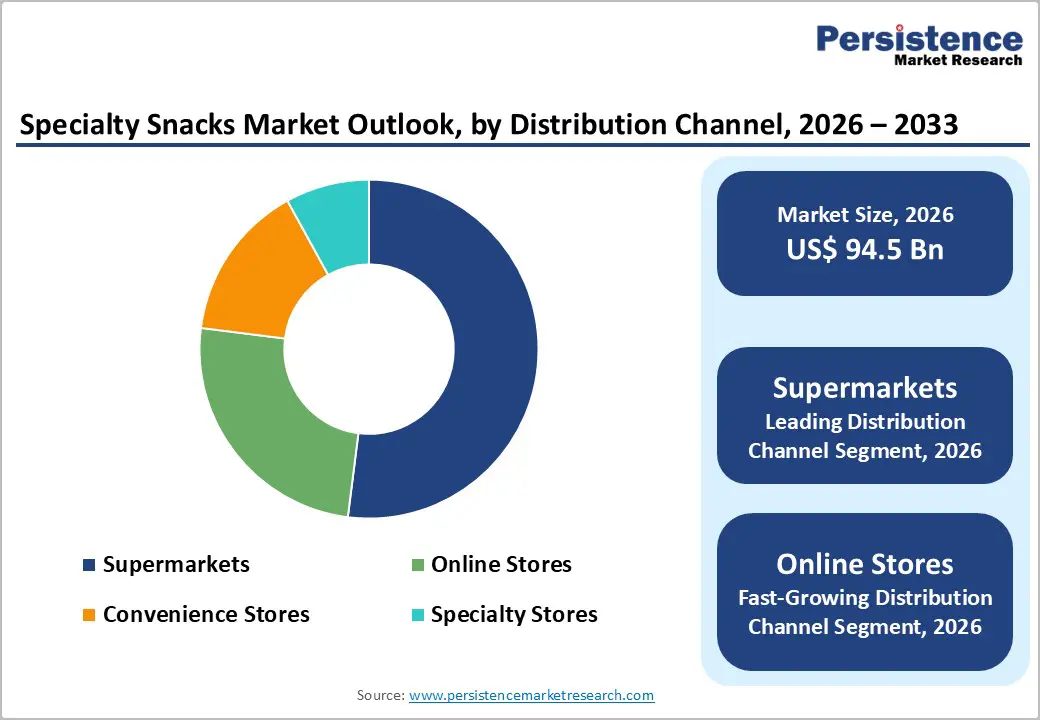

| Specialty Snacks Market Size (2026E) | US$ 94.5 Bn |

| Market Value Forecast (2033F) | US$ 140.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Health-Oriented and Functional Snacking

Consumers are increasingly shifting toward nutritionally enhanced snack formats as health awareness and lifestyle-related concerns continue to influence purchasing behavior. Buyers are prioritizing options such as protein-fortified products, reduced-sugar formulations, gluten-free alternatives, and plant-based offerings that align with dietary preferences and wellness objectives. Food manufacturers are responding by reformulating existing recipes and introducing specialized product lines that deliver measurable functional benefits, including digestive support, sustained energy release, and immune system reinforcement. Regulatory guidance is also shaping innovation priorities, as agencies such as the U.S. Food and Drug Administration (FDA) are promoting balanced nutrition through updated dietary recommendations, while policy initiatives such as the European Union (EU) Farm to Fork Strategy are encouraging sustainable food production systems. This alignment between regulatory direction and consumer demand is strengthening the strategic importance of functional snacking within the broader food industry.

The growing emphasis on health-oriented consumption is also driving premiumization across the snack sector. Organic products are gaining momentum among quality-conscious consumers, which is prompting companies to invest in clean-label ingredients, transparent sourcing practices, and clear nutritional communication. Brands are differentiating through natural flavor development, ethically sourced raw materials, and sustainability commitments that resonate with value-driven buyers. Supply chains are evolving to support consistent access to high-quality inputs, and research & development (R&D) teams are creating prototypes that integrate sensory appeal with nutritional performance. Market leaders are strengthening competitive positioning by capturing consumers who prioritize quality and functionality over price sensitivity, while emerging companies are identifying niche opportunities based on regional tastes and specialized dietary needs.

Innovation and Product Diversification

Manufacturers are actively experimenting with new flavors, novel ingredients, and advanced packaging formats to address diverse consumer preferences through creative product combinations. Companies are introducing plant-based alternatives that appeal to vegan and flexitarian audiences while developing protein-enriched variants for fitness-oriented consumers. Producers are crafting offerings with distinctive tastes, such as matcha-infused crisps or turmeric-spiced nuts, while teams are exploring bold profiles inspired by global cuisines. Packaging specialists are designing resealable pouches and environmentally responsible wraps, and engineers are refining portion-controlled formats to improve convenience and reduce waste.

Continuous innovation is strengthening customer retention and attracting new buyer segments by combining product variety with perceived quality enhancement. Companies are maintaining loyalty among existing consumers while generating interest through digital engagement campaigns and targeted sampling initiatives. Organizations are expanding into underserved demographics, including time-constrained professionals and health-focused households, through differentiated positioning strategies. Similarly, supply networks are adapting to secure specialty ingredients from geographically dispersed regions, and R&D centers are prototyping hybrid concepts that integrate indulgent taste with nutritional functionality, thereby supporting sustainable brand growth.

Raw Material Price Volatility and Supply Chain Fragility

Specialty snack producers are facing elevated exposure to commodity price volatility because they rely heavily on premium raw materials such as nuts, seeds, ancient grains, and alternative protein sources. Input costs are rising when supply shortages occur due to adverse weather conditions or geopolitical trade disruptions, while agricultural producers are experiencing inconsistent harvest yields that reduce predictability. Processing companies are struggling to secure stable procurement volumes at predictable prices, which is compressing operating margins as firms absorb a portion of the cost increases to maintain consumer affordability. Businesses are attempting to balance quality expectations with competitive pricing by expanding local sourcing strategies to reduce transportation expenses and by diversifying supplier networks across multiple regions to mitigate concentration risks.

Smaller brands are experiencing greater financial strain than multinational corporations because limited purchasing scale restricts their negotiating leverage and access to sophisticated risk mitigation tools. Independent companies often lack participation in bulk procurement agreements and commodity hedging instruments, while large conglomerates are using futures contracts to stabilize input costs over longer planning horizons. Boutique operators are reacting more slowly to market fluctuations, which is constraining operational flexibility and diverting capital toward cost management rather than growth initiatives. Product innovation timelines are extending as constrained budgets delay experimentation and commercialization efforts. Some organizations are investing in controlled-environment agriculture such as vertical farming to secure consistent ingredient supply to improve cost predictability and enhancing operational agility over time.

Regulatory Complexity across Jurisdictions

Variations in international regulations governing labeling, ingredient approvals, and permissible health claims are complicating cross-border expansion strategies of specialty snack companies. Regulatory authorities are enforcing distinct compliance frameworks, as the European Food Safety Authority (EFSA) is maintaining stringent requirements for front-of-pack nutritional disclosure across Europe, while the U.S. FDA is regulating additive usage and marketing claims within the United States. In Asia, governments are requiring independent evaluations for novel ingredients before market entry. Producers are navigating these fragmented systems during export planning by modifying formulations to meet local regulatory expectations and by engaging technical specialists to manage documentation reviews and product validation processes.

The fragmented regulatory environment is slowing product launches and increasing compliance expenditures, impacting profitability and limiting portfolio flexibility. Industry leaders are responding by sequencing geographic expansion toward priority markets and establishing regulatory compliance teams early within product development cycles. Companies are partnering with regional consultants who possess jurisdiction-specific expertise, while standardizing core formulations where feasible to simplify adaptation across territories. Digitally enabled compliance tracking platforms are helping organizations monitor regulatory updates and maintain documentation accuracy, which can improve operational efficiency over time. Proactive ingredient validation across multiple regions is accelerating approval timelines, enabling agile companies to convert regulatory complexity into a competitive advantage through preparedness and strategic foresight.

Plant-Based and Sustainable Snack Innovation

Consumers are increasingly prioritizing sustainability when selecting snacks, favoring brands that demonstrate environmentally responsible practices across sourcing and production. Manufacturers are responding by incorporating alternative protein sources such as pea protein, chickpea flour, algae-derived ingredients, and insect-based components to reduce environmental impact while maintaining nutritional value. Companies are designing products that resonate with younger demographics, while emphasizing transparent manufacturing processes to strengthen consumer confidence. Supply chains are integrating ethical agricultural practices, and brands are communicating traceability through detailed ingredient origin narratives on packaging. Industry leaders are experimenting with nature-inspired formulations that align with global sustainability objectives, creating offerings that support both human nutrition and ecological balance while reinforcing brand credibility.

Continuous innovation is strengthening long-term customer engagement and enabling expansion into previously underserved markets, particularly within emerging economies. Organizations are refreshing portfolios with seasonal limited-edition products that stimulate digital engagement among younger consumers, while collaborations with culinary professionals are introducing culturally diverse flavor profiles suited to urban populations. Forward-looking brands need to broaden market reach through targeted digital marketing initiatives and influencer partnerships that enhance visibility and credibility. Agile organizations can sharpen their competitive edge by adapting rapidly to evolving preference patterns across global markets.

Private Label Premiumization and Retailer Co-Manufacturing

Major global retailers such as Walmart, Costco, and Tesco are expanding premium private label portfolios within the specialty snacks category to capture higher margins and strengthen customer loyalty. These chains are developing proprietary products that incorporate distinctive flavors and health-oriented ingredients to attract quality-conscious consumers, while leveraging shelf placement control to position store brands prominently alongside national competitors. Retailers are emphasizing formulations that balance convenience with indulgence to meet evolving consumption preferences, and suppliers are collaborating closely with private label programs to ensure consistent production volumes and rapid replenishment across extensive distribution networks.

Flexible specialty snack manufacturers are identifying substantial growth opportunities through co-manufacturing partnerships and white-label production agreements with large retail organizations worldwide. These collaborations are enabling producers to secure predictable revenue streams without incurring the significant costs associated with building independent brand recognition in saturated markets. Retail partners are benefiting from reduced customer acquisition expenses and reliable supply continuity. Manufacturers are allocating greater resources toward product innovation, quality assurance, and process optimization rather than large-scale marketing investments across fragmented channels, thereby improving efficiency and strengthening long-term competitiveness.

Category-wise Analysis

Product Type Insights

Nuts and seeds are likely to lead in 2026, accounting for approximately 45% of the specialty snacks market revenue share, owing to their high nutritional density, including healthy fats, protein content, and essential micronutrients that support daily wellness. Growing adoption of plant-based dietary patterns is further strengthening demand, as these ingredients provide reliable protein and sustained energy for vegan and flexitarian consumers. Manufacturers are increasing market appeal through flavored coatings, seasoning innovations, and roasting techniques that attract broader consumer groups beyond traditional health-focused buyers. Convenient packaging formats and blended snack assortments are positioning nuts and seeds as portable options suited to fast-paced lifestyles. This combination of functional nutrition and sensory appeal is reinforcing their strong performance across international markets.

Chips are expected to register the fastest growth during the 2026 to 2033 forecast period because continuous innovation in flavors, textures, and ingredient bases is maintaining high consumer engagement. Producers are offering traditional potato-based products alongside alternatives derived from vegetables and grains, as well as baked variants with reduced oil content to appeal to health-conscious consumers. This diversified portfolio is addressing both indulgence-oriented snack preferences and demand for cleaner dietary options without compromising taste satisfaction. Ongoing experimentation with bold seasoning profiles, premium raw materials, and differentiated textures is ensuring that chips remain widely consumed across demographic groups and usage occasions, supporting sustained category expansion globally.

Distribution Channel Insights

Supermarkets are slated to hold roughly 52% of the specialty snacks market share in 2026, fueled by their broad geographic presence across urban and suburban locations is enabling access for large consumer populations. Consumers are benefiting from one-stop convenience by combining discretionary snack purchases with routine grocery trips, which is reinforcing repeat visitation patterns. Strategic merchandising tactics such as end-cap placements and promotional aisles are increasing visibility for premium products that may receive less attention in smaller retail formats. Loyalty programs, competitive pricing structures, and seasonal product introductions are further strengthening customer retention and sustained demand within this channel.

Online stores are projected to register the fastest growth from 2026 to 2033, as digital commerce adoption continues to expand among convenience-oriented consumers. E-commerce platforms are enabling access to extensive product portfolios through user-friendly mobile applications and websites, eliminating the need for physical store visits. Digital channels are supporting informed purchasing decisions by providing detailed ingredient disclosures, nutritional information, allergen labeling, and verified customer reviews that enhance transparency. Consumers are also discovering niche flavors and limited-edition products that may not be widely available in physical retail environments, deepening engagement and encouraging experimentation.

Regional Insights

North America Specialty Snacks Market Trends

North America is projected to account for approximately 37% of the specialty snacks market value in 2026, supported by strong consumer expenditure on premium food products that align with evolving lifestyle preferences. Buyers are consistently investing in offerings that combine indulgence with perceived health value, which is sustaining demand across both metropolitan and suburban populations. The region is home to some of the world’s largest retail chains, primarily Walmart and Costco, which have extensive distribution networks that ensure broad product availability from domestic and international suppliers. Major corporations such as PepsiCo, Mondelz, and General Mills are leveraging scale advantages to introduce innovative flavors, packaging formats, and category extensions tailored to local consumption patterns, thereby strengthening competitive positioning.

Health-oriented consumption trends are further accelerating regional growth as consumers increasingly prioritize clean-label ingredients, plant-based formulations, and functional enhancements such as protein enrichment and nutrient-dense components. Shoppers are demonstrating willingness to experiment with novel snack concepts that combine familiar textures with globally inspired flavor profiles, which is encouraging product diversification. Time-constrained professionals are favoring portable packaging formats, while households are seeking multi-occasion snack options that support shared consumption. Integration of digital commerce platforms is expanding market penetration through personalized recommendations, subscription purchasing models, and targeted promotional strategies that increase repeat buying frequency.

Europe Specialty Snacks Market Trends

Europe is expected to stand as the second-largest market for specialty snacks, driven by rising demand for organic and natural products that reflect consumer priorities related to health and sustainability. Shoppers across the region are actively seeking products free from synthetic additives and are favoring certifications such as EU Organic labels that confirm compliance with strict production standards. Health-focused consumption patterns are influencing purchasing decisions, with strong demand for snacks containing whole grains, nuts, and plant-based protein sources that support active lifestyles. Environmental awareness is also accelerating adoption, as consumers are requesting responsibly sourced ingredients and packaging solutions that minimize waste through recyclable or compostable materials.

Brands are strengthening customer loyalty by communicating carbon-conscious supply chains and fair-trade sourcing partnerships that resonate with environmentally aware households and urban professionals. Regulatory oversight from authorities such as the EFSA is ensuring stringent standards related to labeling accuracy, allergen disclosure, and approval of novel ingredients, which is reinforcing consumer confidence in product safety and quality. These regulatory safeguards are encouraging experimentation with premium snack options that may encounter skepticism in less regulated markets. In Germany, the market is witnessing stable demand driven by disciplined consumption habits, while the U.K. and France are contributing to innovation through diverse flavor combinations influenced by regional culinary traditions.

Asia Pacific Specialty Snacks Market Trends

Asia Pacific is expected to become the fastest-growing market for specialty snacks as rising disposable income levels are enabling middle-income households to explore premium products that combine indulgence with nutritional value, moving beyond traditional staple foods toward more sophisticated options. Dietary patterns are evolving under global cultural influence, with urban consumers adopting Western-style snacking habits while retaining regional taste preferences through fusion products such as wasabi-coated peas and spice-seasoned nuts. Rapid urbanization is accelerating this transition, as expanding metropolitan populations include time-constrained professionals seeking convenient and healthier alternatives to conventional meals. Digital commerce platforms and modern retail channels are widening product accessibility by delivering curated selections directly to homes and workplaces.

Key regional markets are driving this momentum through distinct growth factors. China is leading due to its large consumer base and digitally engaged younger population that is embracing innovative textures and bold flavor profiles through online platforms such as Tmall. India is demonstrating strong expansion supported by favorable demographics and increasing interest in fitness-oriented diets, with domestic manufacturers developing products that incorporate locally preferred spices and functional ingredients. Japan is emphasizing premium artisanal snack formats characterized by high-quality raw materials and minimalist packaging designs that appeal to health-conscious consumers. Government initiatives that promote food processing clusters and industrial development zones are facilitating manufacturing scale expansion across the region.

Competitive Landscape

The global specialty snacks market structure is moderately fragmented, with PepsiCo, Mondelz, General Mills, Kellanova, and Conagra controlling nearly 40% of the total revenues. Competitive intensity remains high as established multinational corporations and emerging niche brands compete to secure consumer loyalty and retail visibility. Market leaders are sustaining momentum through continuous product innovation, targeted marketing initiatives, and close monitoring of evolving consumer preferences that influence long-term demand patterns. These organizations are leveraging brand recognition, distribution scale, and category expertise to maintain competitive positioning while responding rapidly to shifts in health awareness and flavor experimentation trends.

Large companies are allocating substantial investment toward R&D to introduce differentiated flavors, novel textures, and nutritionally enhanced product formats that align with emerging consumption trends. Strategic mergers and acquisitions are enabling portfolio expansion and facilitating entry into high-growth segments and underpenetrated geographic markets. This approach is allowing firms to accelerate innovation cycles, strengthen supply capabilities, and enhance market reach simultaneously. As competition intensifies, companies that combine technological advancement, consumer insight, and strategic expansion initiatives will have reinforced their leadership positions while capturing new growth opportunities across the specialty snacks landscape.

Key Industry Developments

- In February 2026, Hippeas unveiled its most significant packaging redesign in a decade, placing chickpeas prominently on packs with clearer nutrition messaging to strengthen brand differentiation and category ownership amid rising competition.

- In February 2026, Zappfresh, a leading fresh and frozen food provider, launched Meevaa Foods, its new brand targeting the frozen vegetarian ready-to-eat and ready-to-cook snacks segment in India. The initial lineup features 12 products such as samosas, momos, kebabs, patties, tikkis, spring rolls, and gravies.

- In January 2026, BEEST Snacks introduced zero-sugar, ultra-high-protein Crunchy Jerky Chips and a Crunchy Charcuterie Trail Mix, positioned as clean-ingredient, real-food snacks that deliver chip-like texture and up to 24 grams of protein per ounce to redefine savory snacking.

Companies Covered in Specialty Snacks Market

- PepsiCo, Inc.

- Mondelez International, Inc.

- General Mills, Inc.

- Kellanova

- Intersnack Group GmbH & Co. KG

- Conagra Brands, Inc.

- Hain Celestial Group, Inc.

- The Hershey Company

- Three Squirrels Inc.

- Bestore Co., Ltd.

- Tyson Foods, Inc.

- Primal Kitchen

- Hippeas

- RXBAR

- Saffron Road Food

Frequently Asked Questions

The global specialty snacks market is projected to reach US$ 94.5 billion in 2026.

Health-conscious trends, which boost demand for clean-label, protein-rich, and low-sugar specialty formats are driving the market.

The market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Major opportunities lie in functional snacks with plant-based proteins and sustainable packaging that attract health-focused millennials and Gen Z.

PepsiCo, Inc., Mondelez International, Inc., General Mills, Inc., Kellanova, and Conagra Brands, Inc. are some of the key players in the market.