- Retail

- Smart Vending Machines Market

Smart Vending Machines Market Size, Share, and Growth Forecast 2026 - 2033

Smart Vending Machines Market by Product Type (Beverage Vending Machines, Food Vending Machines, Specialty Vending Machines), Payment Mode (Cash Payment, Cashless Payment, Cash-Based Systems), End-user (Transportation Hubs, Commercial Spaces, Healthcare Facilities, Educational Institutes, Others), and Regional Analysis, 2026 - 2033

Smart Vending Machines Market Size and Trend Analysis

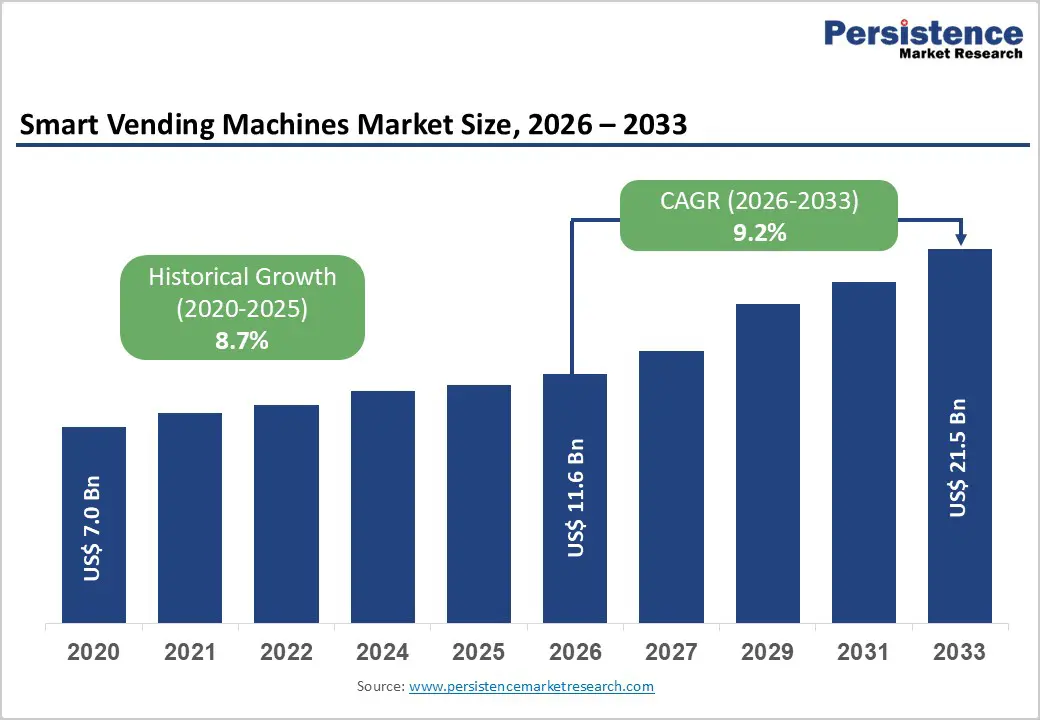

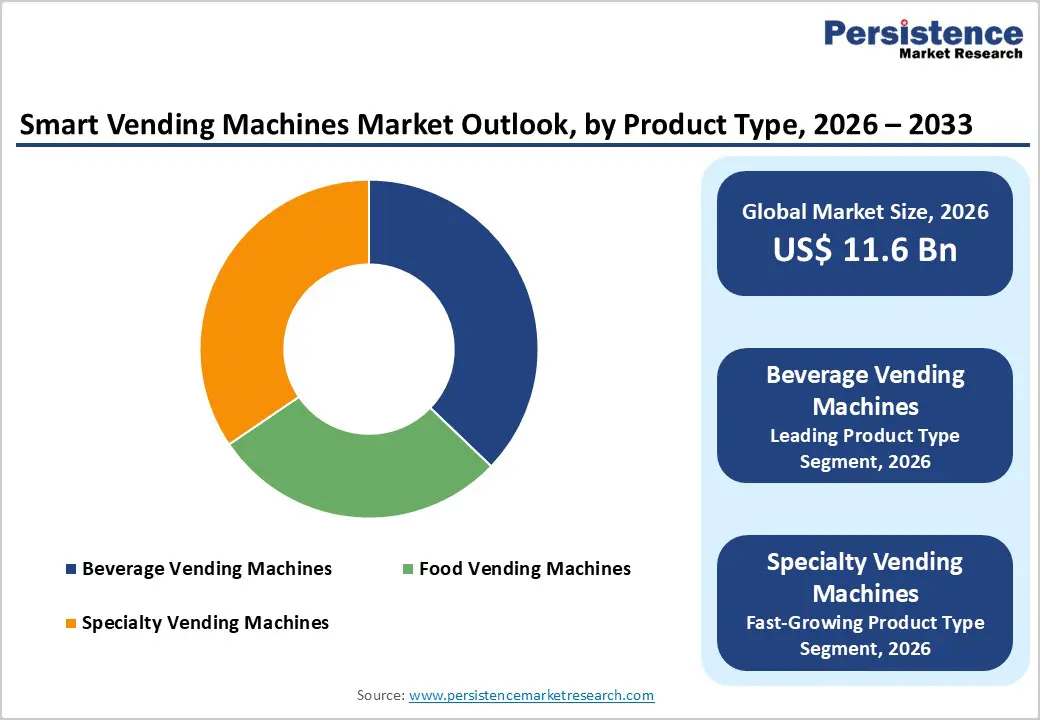

The global Smart Vending Machines market size is likely to be valued at US$ 11.6 billion in 2026, is projected to reach US$ 21.5 billion by 2033, registering a CAGR of 9.2%.

Growth is primarily driven by accelerating IoT and AI integration, enabling real-time inventory management and remote machine monitoring. Rising consumer preference for contactless, 24/7 automated retail access supported by the rapid expansion of NFC, QR code, and mobile wallet payment ecosystems is further propelling market adoption. Increasing deployments across commercial spaces, transportation hubs, and healthcare facilities globally continue to reinforce the market's long-term growth trajectory.

Key Industry Highlights:

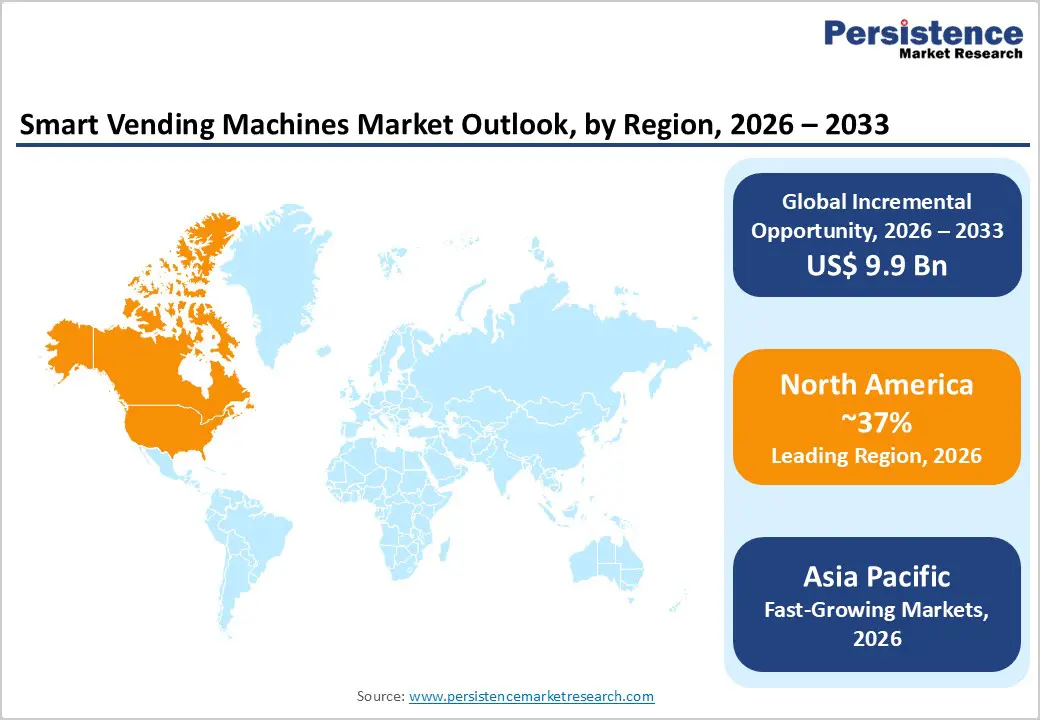

- Leading Region: North America holds the largest revenue share at approximately 34% in 2025, driven by advanced digital payment ecosystems, high vending machine density, and strong IoT-enabled and cashless vending adoption.

- Fastest Growing Region: Asia Pacific is projected to register the highest growth during 2026–2033, fueled by smart city programs, mobile payment proliferation, and surging automated retail demand across China, India, and Southeast Asia.

- Dominant Payment Type: Cashless payment commands approximately 58% market share in 2025, reflecting the accelerating global transition toward NFC, QR code, and mobile wallet-enabled vending transactions across commercial and institutional deployments.

- Fastest Growing Segment: Specialty vending machines is the fastest growing product type, driven by expanding deployments in healthcare, beauty, electronics, and fresh food categories seeking cost-efficient, unmanned automated distribution.

- Key Opportunity: Smart vending deployment for OTC pharmaceuticals and wellness products in hospitals and clinics represents the most significant near-term growth opportunity, supported by favorable FDA regulatory frameworks and rising 24/7 self-service health access demand.

Market Dynamics

Drivers - Expanding Digital Payment Infrastructure and Cashless Economy Transition

The global shift toward cashless economies is a decisive force reshaping smart vending machine adoption. According to the Bank for International Settlements (BIS), non-cash payment transactions surpassed 1.3 trillion globally in 2023, growing at double-digit annual rates. Smart vending machines equipped with NFC, contactless card readers, and mobile wallet integrations have significantly enhanced transaction speed and consumer convenience. Operators simultaneously benefit from reduced cash handling costs and improved revenue reconciliation efficiency.

This fintech-vending convergence is fundamentally transforming how consumers interact with automated retail. Deployments are accelerating across transportation hubs, commercial buildings, and educational institutions, where cashless-first infrastructure is now standard. Platforms supporting Apple Pay, Google Pay, and open-banking payment rails are enabling seamless purchasing experiences, directly driving sustained machine deployment growth worldwide.

Growing Adoption of IoT and AI-Powered Remote Machine Management

The integration of IoT sensors and AI-driven analytics into vending infrastructure has fundamentally elevated operational efficiency. According to Ericsson's Mobility Report 2023, global IoT connections are projected to exceed 35 billion by 2030, with smart retail devices representing a growing share. Operators leveraging connected vending platforms report 30–40% reductions in route servicing costs alongside measurable improvements in machine uptime and inventory accuracy.

Beyond cost savings, AI capabilities enable dynamic pricing, real-time product recommendations, and predictive restocking each directly increasing per-unit revenue. For multi-location retail operators and facility managers, this translates into a compelling return-on-investment case. The ability to remotely diagnose faults, push promotions, and monitor machine health from a centralized dashboard makes IoT-enabled vending an operationally superior and scalable retail model.

Restraints - High Initial Capital Investment and Operational Complexity

The elevated upfront costs of smart vending deployment remain a significant barrier, particularly for small and medium-scale operators. A fully connected smart vending unit costs between US$ 3,000 and US$ 10,000 compared to US$ 1,500–2,500 for conventional machines, representing a substantial capital commitment. Integration with payment gateways, cloud management platforms, and IoT infrastructure introduces additional complexity, alongside recurring software licensing and maintenance fees.

These financial barriers directly constrain deployment scalability, especially across emerging economies where operator margins are thin. Budget-constrained businesses often defer upgrades, slowing overall market penetration. Without accessible financing models or government-backed incentive programs, the capital intensity of smart vending adoption continues to suppress growth potential among the broader mid-market operator segment.

Cybersecurity Vulnerabilities and Data Privacy Concerns

Smart vending machines, as permanently networked endpoints, face growing exposure to cybersecurity threats. Connected payment terminals and consumer data collection systems present vulnerabilities susceptible to breaches and financial fraud. The European Union Agency for Cybersecurity (ENISA) reported a 25% year-on-year increase in cyberattacks targeting IoT devices within retail environments between 2021 and 2023, underscoring the scale of risk.

Regulatory compliance adds to the burden to operations. Frameworks, including the General Data Protection Regulation (GDPR) across Europe and the California Consumer Privacy Act (CCPA) in the U.S. impose strict data handling obligations on machine operators. Meeting these requirements demands ongoing legal, technical, and infrastructure investment costs that disproportionately affect smaller operators and create friction in the pace of broader smart vending deployment globally.

Opportunities - Healthcare and Pharmaceutical Vending: An Emerging High-Growth Vertical

The healthcare sector represents a compelling untapped opportunity for smart vending operators. Hospitals, clinics, and pharmacy chains are increasingly deploying automated dispensing units for over the counter (OTC) medications, personal protective equipment, and wellness products. The U.S. Food and Drug Administration (FDA) has progressively expanded frameworks for automated pharmaceutical dispensing, with several U.S. states already approving unattended OTC medication vending at scale.

With global healthcare expenditure projected to reach US$ 10.4 trillion by 2030 per World Health Organization (WHO) estimates, and hospital footfall rising steadily, smart vending offers a viable 24/7 contactless distribution channel. Post-pandemic environments have permanently normalized self-service health access, creating sustained consumer readiness. For operators, healthcare facilities deliver high transaction frequency, premium product margins, and long-term placement contracts, a combination that significantly strengthens return-on-investment cases.

Expansion in Emerging Economies Through Smart City Initiatives

Government-backed smart city programs across the Asia Pacific and Latin America are generating substantial infrastructure demand directly favorable to smart vending deployment. India's Smart Cities Mission, spanning 100 cities with cumulative investment exceeding US$ 15 billion, actively encourages automated retail integration within urban transit zones and public spaces. China's 14th Five-Year Plan similarly prioritizes digital transformation of retail and public service infrastructure at a national scale.

As smartphone penetration and mobile payment adoption accelerate across these regions, alignment with government urban development agendas offers operators favorable deployment conditions, subsidized infrastructure access, and access to rapidly expanding consumer bases. Rising middle-class populations, improving digital literacy, and growing demand for modern retail convenience collectively position emerging economies as the most strategically significant long-term growth frontier for smart vending machine operators globally.

Category-wise Analysis

Product Type Insights

Beverage vending machines dominate the product type category, commanding approximately 42% of the total smart vending machines market in 2025. This leadership reflects consistently high consumer demand across office complexes, airports, metro stations, and educational campuses. Major operators, including Coca-Cola Company and Nestlé have made significant investments in IoT-connected beverage dispensers featuring touchscreens and personalization capabilities. High replenishment frequency relative to food or specialty items ensures strong recurring revenue per machine, directly enhancing operator return on investment.

Specialty vending machines represent the fastest growing product segment, driven by diversifying consumer needs beyond traditional food and beverage categories. Deployments spanning OTC pharmaceuticals, beauty and personal care, electronics accessories, and fresh meal formats are gaining rapid traction. Retailers and healthcare operators are increasingly recognizing specialty vending as a cost-efficient, unmanned distribution channel capable of serving high-value, low-volume product categories around the clock in both public and institutional environments.

Payment Mode Insights

Cashless payment systems lead the payment mode category, accounting for approximately 58% of the smart vending machine market value in 2025. This dominance is driven by widespread adoption of contactless technologies, mobile wallets, and UPI-based platforms globally. According to Mastercard's New Payments Index 2023, over 75% of consumers across major economies now prefer cashless or contactless transactions. Multi-modal acceptance spanning NFC, QR codes, and biometric modules simultaneously reduces theft risk and reconciliation effort for operators.

Cash-Based systems are progressively being phased out in mature markets; however, hybrid cash-cashless configurations are emerging as the fastest-growing payment format. These systems cater to demographically mixed environments, particularly in emerging economies where digital payment infrastructure remains uneven. Operators deploying hybrid-enabled machines are capturing broader consumer segments while future-proofing deployments for full cashless transition.

End-user Insights

Commercial spaces constitute the dominant end-user segment, holding an estimated 35% market share in 2025. Corporate offices, shopping malls, and mixed-use complexes deliver consistently high foot traffic, favorable installation conditions, and long-term operator contracts. According to CBRE's Global Workplace Survey 2023, over 60% of large enterprises globally are expanding on-site amenity offerings to improve employee retention, a trend directly increasing demand for smart vending solutions providing snacks, beverages, and daily essentials.

Healthcare facilities represent the fastest-growing end-user segment, propelled by rising demand for 24/7 automated access to OTC medications, wellness products, and PPE within hospitals and clinics. Regulatory tailwinds, particularly the FDA's expanding framework for unattended pharmaceutical dispensing in the U.S., are accelerating institutional adoption. The combination of high footfall, premium product margins, and hygiene-conscious self-service preferences makes healthcare the most strategically significant emerging deployment vertical.

Regional Insights

North America Smart Vending Machines Market Trends and Insights

North America leads the global smart vending machines market, accounting for approximately 34% of total revenues in 2025. The region benefits from mature digital payment infrastructure, high consumer acceptance of automated retail, and a well-established vending operator ecosystem. Adoption of AI-driven inventory management and cashless-first machine configurations is accelerating across the U.S. and Canada, particularly in corporate campuses and healthcare facilities.

- U.S. Smart Vending Machines Market Size

The United States dominates the North American market and holds approximately 85% of regional revenues, reflecting an installed base of over 5 million vending machines (per National Automatic Merchandising Association – NAMA). Rapid penetration of IoT-enabled machines, growing demand in healthcare and commercial verticals, and ongoing smart city investments underpin sustained market growth.

Europe Smart Vending Machines Market Trends and Insights

Europe represents the second-largest regional market, driven by strong regulatory support for contactless payments under the EU’s Revised Payment Services Directive (PSD2) and a mature retail automation culture. Countries such as Germany, the U.K., and France are at the forefront of deploying energy-efficient and AI-enabled vending units. The region is also witnessing growing traction for healthy food and fresh meal vending formats.

- Germany Smart Vending Machines Market Size

Germany accounts for approximately 22% of European smart vending revenues in 2025, underpinned by strong industrial and commercial real estate activity, widespread NFC payment acceptance, and a growing preference for automated retail in busy transit nodes and manufacturing complexes.

- U.K. Smart Vending Machines Market Size

The United Kingdom contributes approximately 19% of Europe’s smart vending market in 2025. The country’s near-universal contactless payment adoption with over 90% of retail transactions processed via contactless cards (per UK Finance) creates a supportive environment for cashless smart vending deployment in public transport and commercial environments.

- France Smart Vending Machines Market Size

France holds approximately 15% share of the European regional market, supported by growing automated retail adoption in its extensive mass transit network and rising corporate wellness program investments driving beverage and healthy snack vending deployments across Parisian commercial districts.

Asia Pacific Smart Vending Machines Market Trends and Insights

Asia Pacific is the fastest growing market projected to record a CAGR exceeding 11.5% during 2026–2033. China remains the regional leader, home to one of the world’s largest smart vending machine fleets, with operators like Xiaomi and Alibaba’s Hema pushing AI-powered retail automation. Government-backed smart city programs and surging mobile payment adoption across China, India, Japan, and Southeast Asia drive extraordinary regional growth momentum.

- India Smart Vending Machines Market Size

India is an emerging high-potential market, estimated to represent approximately 8% of Asia Pacific revenues in 2025, growing rapidly on the back of UPI-based cashless payment proliferation, Smart Cities Mission investments, and expanding quick-service retail demand in Tier-1 and Tier-2 cities.

- Japan Smart Vending Machines Market Size

Japan, globally renowned for its vending culture, commands approximately 18% of Asia Pacific smart vending revenues in 2025. With over 5 million conventional machines nationwide, the country’s transition to IoT-connected, AI-personalized units is well underway, supported by operators like Japan Tobacco International (JTI) and Suntory Holdings.

- Southeast Asia Smart Vending Machines Market Size

Southeast Asia accounts for approximately 12% of regional market share in 2025 and is expected to be among the fastest expanding sub-regional markets. Rising urban middle-class populations, expanding modern retail formats, and high smartphone and e-wallet penetration in markets like Singapore, Thailand, and Indonesia are catalyzing demand.

Competitive Landscape

The global smart vending machines market is moderately consolidated, characterized by a small number of established multinational operators commanding significant influence alongside a rapidly expanding cohort of regional, technology-first entrants. Market leaders compete primarily through extensive distribution networks, diversified product portfolios, and deep integration with IoT and AI-enabled machine management platforms.

Strategic priorities are increasingly oriented toward expansion into healthcare and specialty vending verticals, fintech partnerships for broadened payment acceptance, and investment in cloud-based operational infrastructure. Emerging challengers are differentiating through micro-market formats, biometric authentication, and vending-as-a-service (VaaS) subscription models signaling a broader structural shift from hardware-centric to platform-driven competitive positioning across the industry.

Key Developments:

- In January 2025, Crane NXT launched its advanced CPI Evolution cashless payment module compatible with over 200 smart vending machine models, expanding its footprint across North American transit operators.

- In March 2024, Fuji Electric Co., Ltd. announced a new line of AI-enabled beverage vending machines with integrated facial recognition for personalized product suggestions, deployed initially across major Japanese railway stations.

- In September 2023, Azkoyen Group partnered with a leading European fintech to integrate open-banking payment solutions into its smart vending ecosystem, targeting cashless upgrades across Southern European transport infrastructure.

Global Smart Vending Machines Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 7.0 Billion |

|

Current Market Value (2026) |

US$ 11.6 Billion |

|

Projected Market Value (2033) |

US$ 21.5 Billion |

|

CAGR (2026–2033) |

9.2% |

|

Leading Region |

North America, ~34% market share (2025) |

|

Dominant Category – Product Type |

Beverage Vending Machines, ~42% market share (2025) |

|

Top-ranking Category – Payment Mode |

Cashless Payment, ~58% market share (2025) |

|

Incremental Opportunity (2026–2033) |

~US$ 9.9 Billion |

Companies Covered in Smart Vending Machines Market

- Azkoyen Group

- Crane Co.

- Evoca Group

- Fuji Electric Co., Ltd.

- SandenVendo

- Royal Vendors, Inc.

- Bianchi Industry S.p.A.

- Seaga Manufacturing Inc.

- Cantaloupe, Inc.

- WEIMI Smart Vending

- Automated Merchandising Systems (AMS)

- TCN Vending Machine

- Vendekin Technologies

- Winnsen Industry Co., Ltd.

- Smart Vend

Frequently Asked Questions

The global smart vending machines market is estimated at US$ 11.6 billion in 2026, projected to reach US$ 21.5 billion by 2033, growing at a CAGR of 9.2%.

Key drivers include rapid IoT and AI integration, accelerating global adoption of cashless and contactless payment systems, and rising consumer preference for 24/7 automated retail access across commercial, healthcare, and transit environments.

North America leads with approximately 34% revenue share in 2025, supported by mature digital payment infrastructure, high vending machine density, and strong operator investment in IoT-enabled machine upgrades.

The largest opportunity lies in healthcare and pharmaceutical vending deploying smart machines for OTC medications and wellness products alongside government-backed smart city programs across Asia Pacific and Latin America.

Leading companies in the smart vending machines market include Crane NXT, Azkoyen Group, Fuji Electric Co., Ltd., Sanden Holdings Corporation, Selecta Group, Cantaloupe, Inc.