- Home Appliances

- Smart Bathroom Market

Smart Bathroom Market Size, Share, and Growth Forecast 2026 - 2033

Smart Bathroom Market by Product Type (Smart Toilet, Smart Soap Dispenser, Smart Faucets, Showers, Smart Bathroom Mirrors, Smart Bathtubs), Application (Residential, Commercial), and Regional Analysis, 2026 - 2033

Smart Bathroom Market Size and Trend Analysis

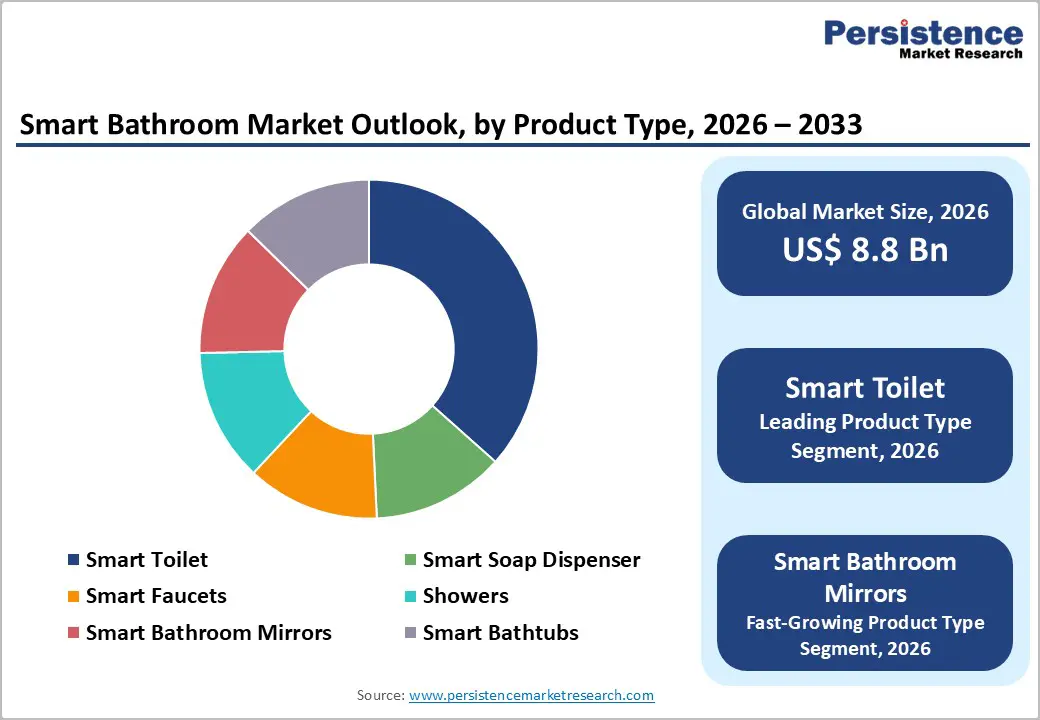

The global smart bathroom market size is expected to be valued at US$ 8.8 billion in 2026 and projected to reach US$ 18.3 billion by 2033, growing at a CAGR of 11.0% between 2026 and 2033.

The smart bathroom market is experiencing robust growth, primarily driven by the rapid integration of the Internet of Things (IoT) in residential and commercial construction, rising consumer awareness around water conservation, and surging demand for hygiene-enhancing touchless technologies accelerated by post-pandemic behavioral shifts. Urbanization trends and premiumization of home interiors, especially across North America, Europe, and Asia Pacific, are compelling homeowners and facility managers to upgrade conventional bathrooms with connected, automated fixtures. Government mandates on water efficiency and growing smart home ecosystem investments are further reinforcing sustained multi-year demand momentum across the value chain.

Key Industry Highlights:

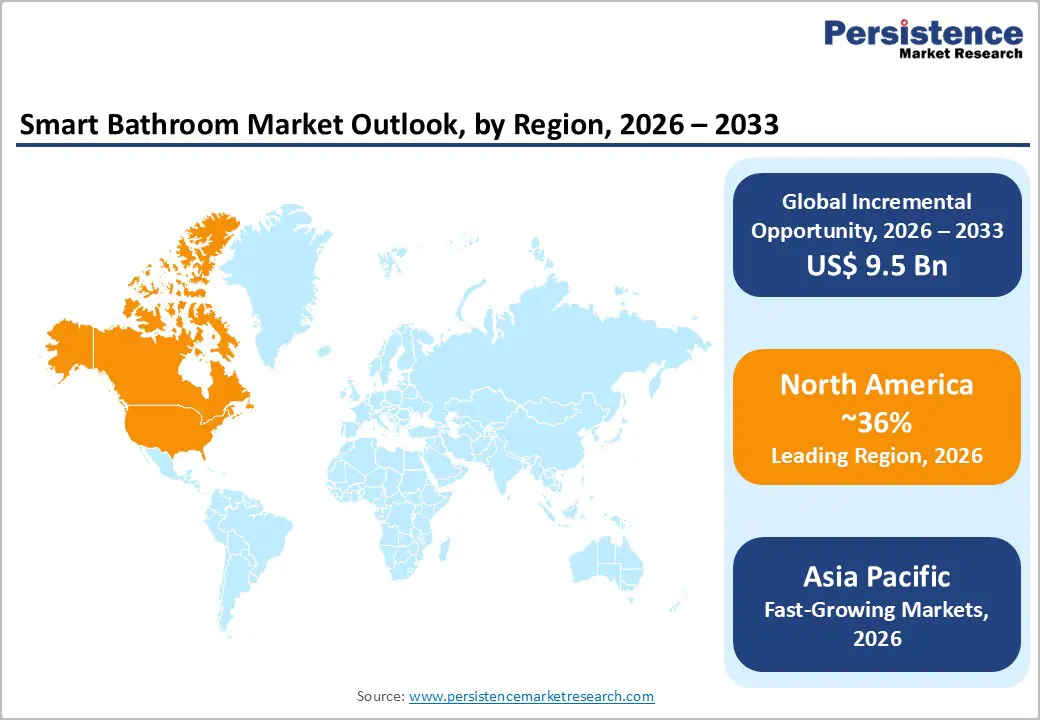

- Leading Region: North America commands approximately 36% of the global smart bathroom market in 2025, underpinned by high smart home adoption, the EPA WaterSense program, and active investment by key players including Kohler Co. and Moen Incorporated.

- Fastest Growing Region: Asia Pacific is projected to record the highest CAGR through 2033, driven by China's smart city programs, India's luxury residential growth under the Smart Cities Mission, Japan's world-leading washlet adoption, and ASEAN hospitality sector expansion.

- Dominant Segment: Smart Toilets lead the product type category with approximately 32% revenue share in 2025, supported by premium pricing, multifunctional health features, and strong demand from luxury residential and hospitality end users globally.

- Fastest Growing Segment: The Commercial application segment is the fastest-growing, driven by post-pandemic institutional retrofitting, hygiene compliance mandates from health authorities including the CDC, and aggressive hotel renovation programs in North America and Europe.

- Key Market Opportunity: Over 100,000 LEED-certified projects globally and a wellness real estate sector exceeding US$ 438 billion create a specification-driven procurement pipeline for smart, water-efficient bathroom solutions.

| Key Insights | Details |

|---|---|

| Smart Bathroom Market Size (2026E) | US$ 8.8 Billion |

| Market Value Forecast (2033F) | US$ 18.3 Billion |

| Projected Growth CAGR (2026 - 2033) | 11.0% |

| Historical Market Growth (2020 - 2025) | 8.7% CAGR |

Market Dynamics

Drivers - Proliferation of Smart Home Ecosystems and IoT Connectivity

The accelerating global rollout of smart home platforms, including Amazon Alexa, Google Home, and Apple HomeKit, is fundamentally transforming bathroom product design and consumer purchasing behavior. According to the Consumer Technology Association (CTA), smart home device revenues in the United States reached approximately US$ 9.7 billion in 2023, reflecting sustained household adoption. Smart bathroom fixtures, including voice-activated faucets, connected mirrors with integrated health monitoring, and app-controlled shower systems, are becoming integral nodes within broader home automation frameworks. The convergence of Wi-Fi 6, Zigbee, and Z-Wave connectivity standards is reducing interoperability barriers, enabling seamless integration of smart bathroom devices into unified home ecosystems. This digital connectivity wave is driving premiumization in bathroom renovation projects and expanding accessible addressable markets well beyond the luxury segment.

Rising Demand for Water Conservation and Touchless Hygiene Technologies

Water scarcity and efficiency mandates are compelling both residential and commercial end users to adopt sensor-driven smart bathroom fixtures that measurably reduce consumption. The U.S. Environmental Protection Agency (EPA) estimates that the average American household can save 20% or more on water bills by installing WaterSense-certified fixtures, a program that has certified products saving consumers over 5.9 trillion gallons of water cumulatively. Smart faucets and showers equipped with real-time flow monitoring and automatic shut-off sensors directly address these efficiency imperatives. Simultaneously, the COVID-19 pandemic created a lasting behavioral shift toward touchless bathroom technologies, with commercial operators, hotels, airports, hospitals, accelerating upgrades to sensor-activated soap dispensers, faucets, and flush systems. The World Health Organization (WHO) continues to emphasize hand hygiene infrastructure as a critical public health measure, sustaining institutional procurement.

Restraints - High Product Cost and Complex Installation Requirements

Premium smart bathroom fixtures command significant price premiums over conventional equivalents. A connected smart toilet with bidet functionality, auto-flush, and health-sensing features can retail between US$ 500 and US$ 5,000, compared to under US$ 300 for standard models. Installation often requires licensed plumbers and electricians, further elevating total cost of ownership. In cost-sensitive markets, including most of Latin America, Africa, and tier-2 and tier-3 cities across Asia, these barriers substantially restrict mass-market penetration, confining demand to affluent urban demographics and high-end hospitality operators.

Cybersecurity Vulnerabilities and Privacy Concerns

As smart bathroom devices become increasingly networked, they expose households and commercial facilities to cybersecurity risks. IoT devices, including connected bathroom fixtures, are frequently cited as vulnerable entry points in home networks. The European Union Agency for Cybersecurity (ENISA) identified IoT devices as among the most targeted endpoints in consumer environments in its Threat Landscape report. Smart mirrors with embedded cameras and health diagnostic features additionally raise significant privacy concerns among data-conscious consumers. Regulatory compliance requirements under frameworks such as the EU General Data Protection Regulation (GDPR) are increasing product development costs for manufacturers seeking to enter European markets.

Opportunities - Smart Bathroom Integration in Green Building and Wellness-Oriented Construction

The global green building movement presents a high-growth demand channel for smart bathroom equipment manufacturers. Green building certification programs, including LEED (Leadership in Energy and Environmental Design) by the U.S. Green Building Council (USGBC) and BREEAM in Europe, increasingly award credits for water-efficient, sensor-driven bathroom fixtures. The USGBC reports over 100,000 LEED-certified projects in more than 180 countries, reflecting a deep global pipeline of projects with embedded demand for smart water-saving fixtures. Concurrently, the wellness real estate sector, valued at over US$ 438 billion globally per the Global Wellness Institute, is incorporating spa-grade smart bathtubs, chromotherapy showers, and AI-powered health mirrors into residential and hospitality developments. Manufacturers that tailor product lines to green and wellness certification requirements can unlock premium, specification-driven procurement channels across commercial real estate, luxury hospitality, and healthcare facilities.

Expansion of Smart Bathroom Solutions in the Hospitality and Healthcare Sectors

The hospitality and healthcare industries represent rapidly expanding procurement channels for smart bathroom technologies beyond residential applications. Premium hotel brands including Marriott International, Hilton Hotels & Resorts, and Four Seasons Hotels are integrating smart bathroom suites featuring voice-controlled lighting, digital shower presets, and connected mirrors as competitive differentiation strategies for luxury room categories. According to the American Hotel & Lodging Association (AHLA), hotel renovation and capital expenditure spending in the U.S. exceeded US$ 6 billion in 2023. In healthcare, smart faucets and hygienic touchless dispensers are being mandated in hospital-acquired infection (HAI) prevention protocols, with the Centers for Disease Control and Prevention (CDC) emphasizing hand hygiene compliance as a top infection prevention priority. This institutional demand pipeline offers stable, high-volume procurement opportunities for smart bathroom product manufacturers with certified hygienic performance credentials.

Category-wise Analysis

Product Type Insights

Smart toilets represent the leading product type segment within the global smart bathroom market, accounting for approximately 32% of total product revenue in 2025. This dominance is driven by the segment's broad adoption across luxury residential, premium hospitality, and healthcare end users, supported by high average selling prices and significant technology content per unit. Japan's deeply embedded washlet culture, championed by TOTO Ltd. for decades, has profoundly influenced global consumer expectations around toilet hygiene and comfort. Smart toilets now incorporate features such as bidet cleansing, auto-flush, seat warming, air deodorization, and health sensing (detecting glucose and blood-related markers in urine). The American Society of Plumbing Engineers (ASPE) and similar bodies increasingly reference smart toilet performance standards in commercial construction specifications. Smart bathroom mirrors represent the fastest-growing product sub-segment, propelled by consumer health monitoring and personalized beauty tech trends.

Application Insights

The residential application segment dominates the smart bathroom market, representing approximately 62% of total market share in 2025. Homeowner investment in bathroom renovation has intensified significantly in the post-pandemic period, driven by increased time spent at home and rising disposable income levels in developed economies. The National Association of Home Builders (NAHB) consistently identifies bathrooms as among the top remodeling priorities for U.S. homeowners, with smart upgrades commanding strong ROI perceptions. Online retail channels and e-commerce platforms have dramatically expanded consumer access to smart bathroom products, lowering purchase friction. The Commercial application segment, covering hotels, airports, offices, hospitals, and retail facilities, is the fastest-growing sub-segment, fueled by post-pandemic institutional retrofitting, hospitality sector recovery, and stringent hygiene compliance mandates from health and safety regulatory bodies.

Regional Insights

North America Smart Bathroom Market Trends and Insights

North America leads the global smart bathroom market with approximately 36% market share in 2025. The United States anchors North America's market leadership through its mature smart home adoption infrastructure, high per-capita income levels, and a prolific residential remodeling culture. The Joint Center for Housing Studies of Harvard University estimates U.S. home improvement expenditure at over US$ 450 billion annually, with bathroom renovations constituting one of the top project categories. The EPA's WaterSense program provides a powerful demand-pull mechanism, as consumers and builders prioritize certified water-efficient fixtures that qualify for utility rebates in water-stressed states including California, Texas, and Arizona.

Canada complements U.S. market dynamics through strong green building adoption under the Canada Green Building Council (CaGBC) framework and expanding new residential construction in urban centers. The North American market is characterized by a robust innovation ecosystem, with companies such as Kohler Co., Moen Incorporated, and Delta Faucet Company headquartered in the region and actively investing in AI-integrated bathroom product development, voice control compatibility, and app-connected personalization features that align with evolving consumer wellness preferences.

Europe Smart Bathroom Market Trends and Insights

Europe represents the second-largest regional market for smart bathroom products, led by Germany, the United Kingdom, France, and Spain. The region benefits from the presence of globally recognized sanitary ware manufacturers including Villeroy & Boch AG, Duravit AG, and Roca Sanitario, S.A. that command strong brand equity and distribution networks. The EU Water Framework Directive and national building regulations in Germany (under EnEV/GEG standards) and the UK's Building Regulations Part G are driving the specification of water-efficient smart fixtures in both new construction and retrofit projects.

The European Green Deal's Renovation Wave initiative, targeting the deep renovation of 35 million buildings by 2030, is creating a sustained multi-year pipeline for smart bathroom upgrades in residential and commercial building stock. Smart bathroom mirrors with health diagnostics and anti-fog technology are gaining rapid traction in premium residential projects across Scandinavia and the Netherlands. The region's strict GDPR regulatory environment is compelling manufacturers to embed privacy-by-design principles in connected product architectures, differentiating European-certified brands in global export markets.

Asia Pacific Smart Bathroom Market Trends and Insights

Asia Pacific is the fastest-growing region, projected to record the highest CAGR through 2033, with the confluence of rapid urbanization, rising middle-class affluence, and government-backed smart city initiatives creating exceptional demand momentum. China is the dominant country market, benefiting from scale manufacturing capabilities of domestic players, large-scale urban housing programs under the country's 14th Five-Year Plan, and surging consumer aspiration for technologically advanced home interiors. Japan remains a global benchmark for smart toilet penetration, TOTO Ltd. reports washlet penetration exceeding 80% in Japanese households, demonstrating the commercial viability of premium smart bathroom adoption at a national scale.

India is an emerging high-growth market, driven by the Smart Cities Mission covering 100 cities and rapid growth of the luxury residential real estate segment in urban centers including Mumbai, Bengaluru, and Hyderabad. The ASEAN market, particularly Singapore, Thailand, and Malaysia, is gaining traction driven by premium hospitality sector growth and smart building regulations. The region's cost-competitive manufacturing base for electronic components and plumbing fixtures affords Asia Pacific-headquartered manufacturers structural cost advantages in global supply chains.

Competitive Landscape

The global smart bathroom market is moderately fragmented, characterized by the presence of established sanitary ware manufacturers alongside technology-driven entrants and regional suppliers. Leading participants maintain a competitive advantage through strong brand equity, extensive distribution networks, and sustained investment in research and development. Market competition is shaped by differentiation in integrated smart platforms, interoperability with major voice assistant ecosystems, water-efficiency certifications such as EPA WaterSense, and premium, design-oriented product positioning targeting residential and commercial segments.

Strategically, companies are focusing on ecosystem-based offerings that combine hardware, software, and connectivity features to enhance user experience and data-driven functionality. Partnerships with technology providers, integration of AI-enabled sensors, and expansion into direct-to-consumer digital sales channels are becoming central growth levers. While premium brands emphasize innovation and sustainability-led value propositions, emerging Asian manufacturers are strengthening their presence in mid-range segments through competitive pricing, agile product development cycles, and rapid geographic expansion.

Key Developments:

- February 2025: TOTO showcased next-generation smart, sustainable, and luxury bathroom innovations, including advanced WASHLET and vessel lavatory designs, at the KBIS 2025 trade show.

- April 2025: ARROW expanded its presence in Vietnam by partnering with DASH Co., Ltd. to open its first flagship showroom in Ho Chi Minh City, introducing smart bathroom solutions to local consumers.

- May 2025: AQUATIZ showcased cutting-edge smart bathroom solutions, unveiling a one-stop intelligent hotel bathroom concept at the Kitchen & Bath China 2025 exhibition in Shanghai.

Companies Covered in Smart Bathroom Market

- Jacuzzi Brands, LLC

- Villeroy & Boch AG

- Signature Hardware (Ferguson Enterprises, LLC)

- Pfister (Spectrum Brands, Inc.)

- Kraus USA Plumbing LLC

- Delta Faucet Company

- Moen Incorporated

- Kohler Co.

- Duravit AG

- Roca Sanitario, S.A.

- TOTO Ltd.

- LIXIL Corporation

- American Standard Brands (WABCO Holdings)

- Hansgrohe SE

- Geberit AG

- ARROW Group

- AQUATIZ

Frequently Asked Questions

The global smart bathroom market is valued at US$ 8.8 billion in 2026 and is projected to reach US$ 18.3 billion by 2033 at an 11.0% CAGR.

Key drivers include expansion of IoT-enabled smart homes (with U.S. smart home revenues near US$ 9.7 billion in 2023 per Consumer Technology Association), water conservation mandates, touchless hygiene adoption, and green building integration.

North America leads with around 36% market share in 2025, supported by high smart home penetration and strong residential renovation spending.

The major opportunity lies in green building and wellness real estate projects, supported by over 100,000 LEED-certified projects worldwide and rising health-focused construction investments.

The key companies shaping the global smart bathroom market include Kohler Co., Moen Incorporated, Delta Faucet Company, Villeroy & Boch AG, Duravit AG, TOTO Ltd., LIXIL Corporation, Roca Sanitario, S.A., Jacuzzi Brands, LLC, and Hansgrohe SE.