- Display Technologies

- Smart TV Market

Smart TV Market Size, Share, and Growth Forecast 2026 – 2033

Smart TV Market by Screen Size (Below 32 inches, 32–43 inches, 44–55 inches, 56–65 inches, Above 65 inches), Operating System (Android TV, Tizen (Samsung), webOS (LG), Roku TV, Others), Technology (LED, OLED, QLED, Others), Sales Channel (Online, Offline), End User (Residential, Commercial), and Regional Analysis, 2026–2033

Smart TV Market Size and Trend Analysis

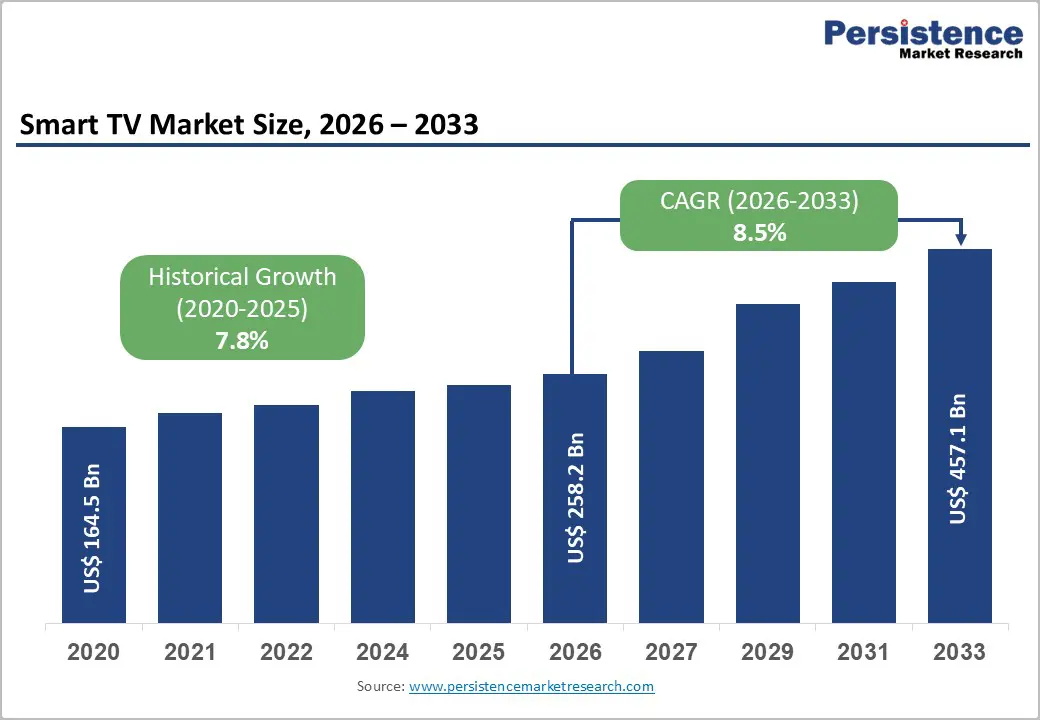

The global Smart TV market size is expected to be valued at US$ 258.2 billion in 2026 and projected to reach US$ 457.1 billion reaching a CAGR of 8.5% between 2026 and 2033. This robust growth is primarily driven by rising global broadband and 5G penetration, accelerating consumer shift toward over-the-top (OTT) content platforms, and the rapid proliferation of smart home ecosystems. Declining panel costs and increasing screen-size aspirations in emerging economies further propel market expansion, while continuous hardware-software innovation by major brands sustains premium upgrade cycles across developed markets.

Key Industry Highlights

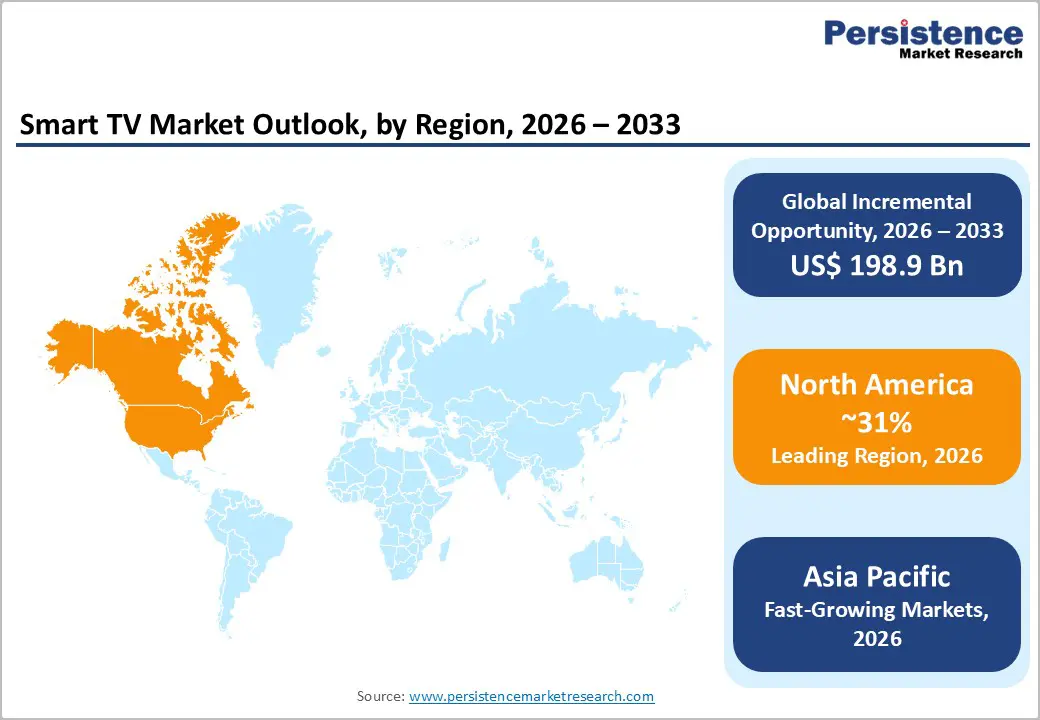

- Leading Region: North America holds approximately 31% of the global smart TV market share in 2026, driven by near-universal broadband penetration, high disposable incomes, and one of the world's most mature OTT streaming ecosystems sustaining continuous TV upgrade cycles.

- Fastest Growing Market: Asia Pacific is projected to reach a CAGR of 10.2% through 2033, fueled by rapid 5G network rollout, expanding middle-class consumer base in India and Southeast Asia, and aggressive pricing strategies by Chinese manufacturers.

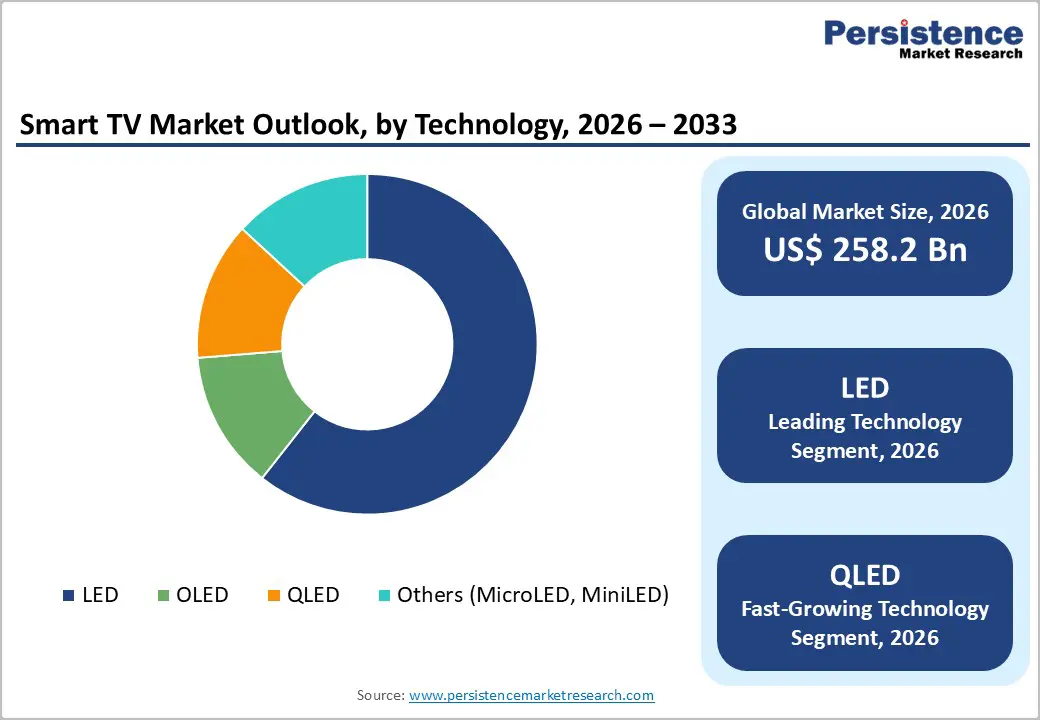

- Dominant Technology Segment: LED technology commands approximately 62% of market share by display technology in 2025, sustained by its compelling cost advantage over OLED and QLED and enduring consumer preference in mainstream and value-tier price segments globally.

- Fast-Growing Technology Segment: QLED technology is the fastest-growing display technology, driven by Samsung's aggressive market development, declining quantum dot panel costs, and the integration of MiniLED backlighting, further improving picture quality competitiveness against premium OLED displays.

- Key Opportunity: Brands investing early in MicroLED and MiniLED technology commercialization stand to capture premium segment leadership as panel costs decline and consumer awareness grows, creating a significant first-mover margin advantage, particularly in North America and Western Europe through 2030.

Market Dynamics

Drivers - Rising OTT Content Consumption and Streaming Ecosystem Integration

Smart TV manufacturers and platform developers stand to gain disproportionately from the structural shift in how consumers access video content globally. According to the International Telecommunication Union (ITU), global internet users surpassed 5.4 billion in 2023, up from 4.9 billion in 2021, with a significant share accessing streaming content via connected televisions. Netflix alone reported 301.6 million paid subscribers globally as of Q4 2024, underscoring the scale of demand for smart, streaming-capable displays. This OTT-TV convergence compels device makers to deepen integrations with content platforms, creating lock-in effects and intensifying competition around operating system quality. For stakeholders, this means smart TVs are evolving from commoditized hardware into ecosystem-anchored platforms, rewarding brands that control both the content discovery layer and the hardware experience.

Smart Home Proliferation and AIoT Integration

The positioning of smart TVs as central hubs within connected home ecosystems represents a material demand driver for manufacturers with strong IoT credentials. The Consumer Technology Association (CTA) reported that U.S. consumer technology sales reached a record US$ 512 billion in 2024, with connected home devices, including smart TVs, commanding a growing portion of household electronics budgets.

Artificial intelligence features embedded in modern smart TVs, such as voice-command interfaces, content personalization algorithms, and device interoperability through platforms like Google Home, Amazon Alexa, and Apple HomeKit, are expanding the functional value proposition beyond entertainment. Companies that embed robust AIoT capabilities are seeing greater consumer willingness to pay premium prices, signaling an upward shift in average selling prices (ASPs) and a competitive moat for innovation-led players.

Market Restraints

Market Saturation and Prolonged Replacement Cycles in Developed Economies

High penetration rates in mature markets, particularly the United States, Western Europe, and Japan, structurally suppress volume growth and compress margins for established players. Euromonitor International and trade data from the European Consumer Electronics Association indicate that TV replacement cycles have lengthened to approximately 7–10 years in saturated markets, limiting the frequency of new-device purchases. Manufacturers consequently depend more heavily on premiumization strategies, pushing OLED, QLED, and large-format screens, to sustain revenue growth. For new entrants, this dynamic creates a structurally unattractive volume play, while incumbents face narrowing addressable demand that forces increased marketing spend to pull forward replacement decisions.

Cybersecurity Vulnerabilities and Consumer Data Privacy Concerns

The growing connectivity of smart TVs introduces meaningful cybersecurity risk, a restraint that directly suppresses adoption rates among privacy-sensitive consumer segments.

The U.S. Federal Trade Commission (FTC) has raised formal concerns about smart TV data collection practices, and the European Union's General Data Protection Regulation (GDPR) imposes strict compliance requirements on device manufacturers collecting behavioral and content consumption data. Notable incidents of smart TV vulnerabilities, including those flagged by Consumer Reports and security researchers, have eroded consumer trust in connected devices within the household. For market participants, this creates both a compliance cost burden and a reputational risk that can delay purchase decisions, particularly in enterprise and public sector channels where data governance frameworks are stringent.

Opportunities - Expanding Middle-Class Consumer Base and Infrastructure Build-Out in Asia Pacific and Africa

Emerging market growth represents the most time-sensitive and scalable opportunity in the smart TV industry, particularly as infrastructure investments in broadband and 4G/5G networks enable connected device adoption in previously underserved geographies. According to the World Bank, the share of the global middle class in South Asia and Sub-Saharan Africa is projected to increase significantly through 2030, creating first-time buyers for smart consumer electronics.

India's Telecom Regulatory Authority (TRAI) reported active broadband subscriber count crossing 940 million in 2024, dramatically widening the addressable base for streaming-capable TVs. Companies like Xiaomi Corporation and TCL Technology Group are already executing on this opportunity through value-tier product strategies; however, the competitive window remains open for brands that can balance localized content, regional language interfaces, and cost-competitive pricing to capture first-time smart TV buyers before brand loyalty consolidates.

Commercialization of MicroLED and MiniLED Technology for Premium Segments

The rapid commercialization of MicroLED and MiniLED display technologies opens a high-margin opportunity for manufacturers capable of scaling production ahead of broader commoditization. Samsung Electronics began commercial deployment of its The Wall MicroLED product range at scale from 2023–2024, signaling growing feasibility of the technology beyond niche installations. According to the Society for Information Display (SID), MiniLED adoption in premium TV segments more than doubled between 2022 and 2024, with panel suppliers including AU Optronics and BOE Technology rapidly expanding capacity.

Brands that lock in supply chain relationships and build consumer awareness around superior picture quality metrics, such as local dimming precision and peak brightness, will be best positioned to command premium pricing as these technologies move from early adopter to mainstream acceptance between 2026 and 2030. The structural shift from OLED to hybrid and advanced backlight technologies could reshape segment leadership within the premium category over the forecast period.

Category-wise Analysis

Screen Size Insights

The 44–55 inches segment commands the leading share of approximately 36% of the smart TV market in 2025, reflecting a sustained consumer preference for mid-to-large format screens that balance viewing comfort, room compatibility, and price accessibility. This segment's dominance is structurally reinforced by the convergence of living room ergonomics, typical viewing distances of 2–3 meters align best with 44–55 inch displays, and the entry-level pricing of 4K LED panels at this size having dropped below US$ 400 across major markets.

The Above 65 inches segment is the fast-growing, driven by declining large-format panel costs, aspirational purchasing behavior in emerging economies, and the rise of home theater setups post-pandemic. Supply chain data from panel producers indicate strong CAGR momentum in the above-65-inch tier by 2033 as MiniLED and QLED technologies reduce the cost-per-inch premium for larger displays.

Operating System Insights

Android TV / Google TV holds the leading operating system share at approximately 38% in 2025, leveraging Google's vast developer ecosystem, deep integration with YouTube, Google Play Store, and Google Assistant, and its licensing model that enables a wide array of OEM partners, including Sony, TCL, Hisense, and Philips, to ship competitively featured smart TVs.

The platform's openness lowers barriers for content app developers, sustaining a content depth advantage that is difficult for proprietary OS rivals to replicate quickly. Roku TV is the fastest-growing OS segment, benefiting from its content-agnostic, ad-revenue monetization model and strong channel relationships with North American retailers, with Roku reporting over 89.8 million active accounts globally as of 2024.

Technology Insights

LED technology retains the dominant share of approximately 62% in 2025, underpinned by its compelling value proposition across mainstream and entry-level price tiers and continued cost efficiency advantages over competing display technologies. The structural price gap between LED and OLED, often 2–4x at comparable screen sizes, confines OLED adoption to premium segments, preserving LED's volume dominance in the mass market. However, QLED is the fastest-growing technology segment, driven by Samsung's aggressive marketing of quantum dot advantages and competitor adoption by TCL and Hisense, while MiniLED backlighting integration into QLED panels is further improving competitive positioning against OLED on brightness and contrast metrics.

Sales Channel Analysis

Offline retail channels retain a leading share of approximately 58% in 2025, reflecting the persisting consumer preference for in-store assessment of display quality, size perception, and color calibration before committing to what remains a considered, high-involvement purchase.

Large-format electronics retailers, hypermarkets, and brand-dedicated showrooms continue to exert significant influence over consumer decision-making for TVs priced above US$ 500. Nevertheless, online channels are the fastest-growing segment, propelled by rising e-commerce penetration globally, promotional events such as Amazon Prime Day and Singles' Day driving massive volume spikes, and the growing maturity of online return logistics that reduce perceived purchase risk for large-screen products.

End User Insights

The residential segment commands the dominant share of approximately 78% of smart TV end-use demand in 2025, driven by household-level upgrades, multi-TV households in developed economies, and rising first-time smart TV penetration in developing markets. Households in the U.S. own an average of 2.3 television sets, highlighting the depth of residential demand. The commercial segment, encompassing hospitality, healthcare, corporate, and retail display applications, is the fastest-growing end-use category as organizations increasingly deploy large-format smart TVs for digital signage, patient entertainment, and collaborative workspaces, with the post-pandemic recovery in hospitality and retail accelerating procurement cycles.

Regional Insights

North America Smart TV Market Trends and Insights

North America represents the leading regional market for smart TVs, holding approximately 31% of global market share in 2025, underpinned by high household income levels, near-universal broadband penetration, and one of the most mature OTT content ecosystems globally. The region's demand is structurally biased toward premium and large-format TVs, with significant volume concentrated in the 44-inch and above screen categories.

The rapid transition from linear cable TV to streaming, accelerated by cord-cutting trends tracked by the Leichtman Research Group, continues to motivate smart TV upgrades. As brands invest in proprietary smart platforms and exclusive content partnerships, North America will remain a premium battleground for OS-level differentiation.

U.S. Smart TV Market Size

The United States accounts for approximately 86% of the North American smart TV market, supported by a strong consumer electronics culture, widespread streaming adoption, and robust retail infrastructure through major chains and e-commerce platforms. The Consumer Technology Association (CTA) projects continued healthy demand for TV upgrades driven by sports broadcasting rights transitioning to OTT and expanded 8K and OLED content availability, cementing the U.S. as the single largest national market through 2033.

Europe Smart TV Market Trends and Insights

Europe constitutes the second-largest regional smart TV market, capturing approximately 24% of global share in 2025, driven by high disposable incomes, competitive retail pricing from brands like Samsung, LG, Philips, and Panasonic, and strong public broadcasting traditions evolving toward digital-first delivery. Regulatory tailwinds from the European Union's Digital Single Market strategy and energy efficiency standards (EU Ecodesign Directive) are shaping product development priorities, with manufacturers investing in lower power consumption displays. Europe is expected to sustain steady growth as aging TV fleets cycle toward replacement with energy-compliant smart models, creating predictable procurement volumes for the forecast period.

Germany Smart TV Market Size

Germany is Europe's largest individual smart TV market, contributing an estimated 19% of regional revenue, supported by high average selling prices and consumer preference for premium brands. The Gesellschaft für Unterhaltungs- und Kommunikationselektronik (gfu) reports strong year-on-year growth in large-format TV sales in Germany. Forward-looking demand will be driven by the government's accelerated broadband rollout targeting gigabit connectivity nationwide by 2030, directly enabling high-quality smart TV streaming.

U.K. Smart TV Market Size

The United Kingdom accounts for approximately 16% of European smart TV market value, with demand anchored to high streaming adoption rates, Ofcom data shows that over 78% of U.K. households subscribed to at least one streaming service as of 2024. The shift of premium sports broadcasting to platforms like Amazon Prime Video Sports and TNT Sports is a sustained upgrade catalyst. Looking ahead, the U.K.'s trajectory points toward higher average screen sizes as home media room culture deepens.

France Smart TV Market Size

France represents approximately 12% of the European smart TV market, with demand shaped by a strong public broadcasting framework transitioning to hybrid digital delivery and rising penetration of high-speed fiber broadband, Arcep data confirms France's fiber subscriber base crossing 17 million households in 2024. Consumer preference skews toward mid-range smart TVs with strong streaming platform integration. France's market trajectory is positive, supported by the ongoing decline in legacy cable subscriptions and the rise of IPTV services.

Asia Pacific Smart TV Market Trends and Insights

Asia Pacific is the fastest-growing regional smart TV market, with a projected CAGR of approximately 10.2% from 2026 to 2033, and commanded the largest volume base in 2025 reflecting the region's vast and rapidly urbanizing population. China remains the single largest national market globally, with domestic brands TCL, Hisense, and Skyworth holding dominant volume shares and aggressively expanding internationally. Across the broader region, rising middle-class affluence, improving 4G/5G network coverage, and government digitization initiatives in India, Indonesia, and Vietnam are accelerating first-time smart TV adoption. Companies scaling in this geography must prioritize affordable, feature-rich mid-range products with localized content ecosystems to capture the next wave of buyers.

India Smart TV Market Size

India represents approximately 17% of the Asia Pacific smart TV market and is among the fastest-growing country markets globally, driven by rising smartphone-linked content consumption habits, affordable 4K smart TV pricing below INR 20,000, and JioFiber's rapid broadband subscriber expansion. The Telecom Regulatory Authority of India (TRAI) confirms strong internet penetration growth. India's trajectory points to sustained double-digit demand growth as urban and semi-urban households upgrade from basic to smart TVs.

Japan Smart TV Market Size

Japan accounts for approximately 12% of the Asia Pacific smart TV market, characterized by premium technology adoption and a consumer base highly receptive to display innovation. Sony Group Corporation's BRAVIA series and Panasonic's OLED lineup maintain strong domestic demand. The Japan Electronics and Information Technology Industries Association (JEITA) tracks stable replacement-cycle demand. Japan's trajectory centers on premium OLED and 8K adoption, supporting higher average revenue per unit for the forecast period.

South Korea Smart TV Market Size

South Korea contributes approximately 9% of Asia Pacific smart TV revenues while exerting outsized global influence as the home base of Samsung Electronics and LG Electronics, the world's two largest TV manufacturers. Domestic consumers demonstrate exceptional appetite for display technology innovation, Korea was among the first markets to achieve mass-market OLED and QLED penetration. The Korea Communications Commission's ongoing 5G expansion and consumer preference for 8K content will sustain premium segment momentum.

Competitive Landscape

The global smart TV market is moderately consolidated at the top, with the five largest players, Samsung Electronics, LG Electronics, TCL Technology Group, Hisense Group, and Sony Group Corporation, collectively accounting for an estimated 65–70% of global revenue in 2025. The market rewards a dual-track competitive model: premiumization (OLED, QLED, large-format flagship products) for margin defense in developed markets, and value-tier scaling for volume capture in emerging economies. Vertical integration, particularly control over display panel supply chains, confers decisive advantages for Samsung and LG. New entrants and challenger brands like Xiaomi Corporation and OnePlus Technology are disrupting mid-range segments through digital-first go-to-market strategies and ecosystem bundling with smartphones and smart home devices. The emerging battleground is OS differentiation and advertising revenue monetization, shifting the competitive lens from pure hardware margins toward platform-driven recurring revenue models.

Key Developments

- May 2026: Sharp Corporation announced the launch of 15 AI-equipped AQUOS smart TV models in Japan featuring generative AI-powered interactive characters and personalized content recommendations, developed using OpenAI’s ChatGPT technology to enhance home entertainment experiences.

- April 2026: Lumio launched the Vision 9 (2026) smart TV lineup in India featuring a performance-first architecture powered by MediaTek Pentonic 700 chipset, targeting premium consumers with enhanced gaming, AI-driven content discovery, and faster smart TV responsiveness.

- September 2025: Dish TV India Limited launched its VZY integrated entertainment ecosystem combining live TV, OTT streaming, and smart TV features through Google TV-powered devices, targeting India’s growing connected home entertainment market with built-in DTH and streaming integration.

Global Smart TV Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 164.5 billion |

|

Current Market Value (2026) |

US$ 258.2 billion |

|

Projected Market Value (2033) |

US$ 457.1 billion |

|

CAGR (2026–2033) |

8.5% |

|

Leading Region |

North America, ~31% market share (2025) |

|

Dominant Screen Size Segment |

44–55 inches, ~36% market share (2025) |

|

Top-Ranking Operating System |

Android TV / Google TV, ~38% market share (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 198.9 billion |

Competitive Industry Landscape

The smart TV industry is dedicated to expanding by acquiring established market players and innovations. This trend is accompanied by the emergence of startups introducing their unique smart television offerings, resulting in a highly diverse and competitive market landscape.

To stay ahead of evolving market trends, companies are making substantial investments to expand production capabilities and enhance their technological features. Their goal is to develop innovative features and integrate technologies into smart televisions that can be effectively introduced and embraced by the market.

Recent Industry Developments

June 2024, Samsung, a leading TV manufacturer, is focusing on incorporating artificial intelligence into its latest Neo QLED and OLED TVs. These smart televisions offer a transformative viewing experience with double the computational power, delivering precise content display in both 4K and 8K resolutions. The innovative NQ8 AI Gen3 processor enhances image quality, while the AI Motion Enhancement PRO feature ensures sharp and clear visuals even during fast-moving scenes. Samsung's AI-driven sound technology, including AI Active Voice Amplifier Pro and Object Tracking Sound, creates an immersive audio environment, enhancing overall viewing engagement.

February 2024, VIZIO has been named an Emmy® recipient for the 75th annual Technology & Engineering Emmy® Awards by the National Academy of Television Arts & Sciences (NATAS). The NATAS Committee recognized VIZIO for its Large Scale Deployment of its Smart TV Operating System, which powers better viewing experiences for millions of consumers. VIZIO, a pioneer in the Smart TV marketplace, has been recognized for its consumer-focused vision and world-class engineering team's execution to deliver exceptional entertainment experiences for users nationwide.

Companies Covered in Smart TV Market

- Samsung Electronics

- LG Electronics

- Sony Group Corporation

- TCL Technology Group

- Hisense Group

- Xiaomi Corporation

- Panasonic Holdings Corporation

- Vizio Inc.

- Sharp Corporation

- OnePlus Technology

- Haier Smart Home

- Skyworth Group

- TPV Technology (Philips TVs)

- Toshiba (TV Division)

- Amazon (Fire TV)

- Konka Group

- Vestel Group

- Changhong Electric

Frequently Asked Questions

The global smart TV market is valued at US$ 258.2 billion in 2026 and is projected to reach US$ 457.1 billion by 2033 at a CAGR of 8.5%.

Key growth drivers include rising OTT streaming adoption, expanding broadband and 5G infrastructure, and increasing smart home ecosystem integration.

North America leads the market with around 31% share due to strong broadband penetration and high adoption of streaming services.

Key opportunities include rising first-time smart TV adoption in emerging economies and growing commercialization of MicroLED and MiniLED display technologies.

Major companies include Samsung Electronics, LG Electronics, Sony Group Corporation, TCL Technology Group, Hisense Group, and Xiaomi Corporation.