Sheet Molding Compound Market Segmented By Bulk Molding Compound, Low Density Sheet Molded Compound with Glass Fiber and Carbon Fiber

Industry: Chemicals and Materials

Published Date: August-2019

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 243

Report ID: PMRREP15979

The sales of sheet molding compounds (SMC) are growing at an impressive rate to record a value of ~US$ 2 billion in 2019, which has been found out by the latest research report published by Persistence Market Research (PMR). The report estimates that the automotive industry will remain a critical lever; however, an exponential rise in applications of sheet molding compounds in the consumer good industry will drive new revenue tangents.

With the rising quest for solid compound and lightweight materials, carmakers are likely to reduce their reliance on steel and are progressing towards the adoption of sheet molding compounds.

Sensing the enormous sales potential of the sheet molding compounds, manufacturers are looking at enhancing the mechanical properties of their products. Recent trends to look for, include the increasing penetration of carbon fiber for the development of low-density SMCs.

A move towards hybrid technology is highly likely to ameliorate the quality of sheet molding compounds, which will propose a market shift with new applications and greater profitability. However, changing dynamics of the regional dominance in the coming decade will remain a key feature of the sheet molding compounds market to focus on for market players, given the massive uptake of the transportation industry.

The directly proportional relationship between the weight of materials used for the manufacturing of vehicles and the consumption of fuel has enthused the transportation and automotive industries to focus intently on the light-weighted products, which has led to the development and adoption of SMC as a measure towards product weight reduction.

Crucial components of pickup truck boxes, hoods, bumpers, fenders, and deck lids are finding massive applications of sheet molding compounds, thereby growing their sales in the automotive and transportation industry.

Currently, the automotive industry accounts for a share of ~21% of the global sheet molding compounds market and will upkeep its contribution at a compound annual growth rate of ~5 percent during the forecast period 2019-2029. The growth of Europe in the automotive industry, in turn, reflects on the growth of the sheet molding compounds market.

A high concentration of automakers in Europe and the intensified competition level in the region leads to a greater focus on product differentiation. Performance of engine being an attractive feature inspires automakers to work on optimizing the fuel efficiency by leveraging various technologies and materials for the development of their products. As a result, partnerships and joint ventures with the sheet molding compounds have been a routine feature.

As the dynamics of the automotive industry changes, stringency apropos of the environmental regulations have also taken other regions by the storm, besides Europe, and China has been facing the major heat.

However, this has worked positively for the country’s economic vigor with its shift towards electrifying the future of the automobile industry. Beside China, Japan has been a key region for the automobile industry, which turns it into a key market for sheet molding compounds market.

Currently, China holds ~13% of the global market share, followed by Japan with ~10% and are likely to grow at an impressive CAGR of ~6% during the forecast period. In addition, China’s thriving consumer goods industry is also likely to exert its influence on the sales of SMCs. With ‘compact’ and ‘corrosion resistant’ being the keyword for the contemporary consumer goods market, use of sheet molding compounds will grow significantly over steel and aluminum materials.

An influx in the revenue of exponentially contributing consumer goods industry and incrementally contributing automotive industry is further passed on to the position of the East Asia, which is poised to outperform the European sheet molding compounds market in 2027. This means that the current players of the sheet molding compounds market should begin focusing on this futuristic shift of regional dominance to remain at the winning end of the competition.

The steady growth of the sheet molding compounds market, however, is likely to be challenged by the introduction of high-quality alternative - light fiber injection (LFI). The production process of light fiber injection is relatively economical, which further plays integral in controlling overhead costs and turning them cost-efficient.

On the scale of performance, LFI and SMC weigh the same, which offers an added advantage to the former with affordability to its label. As a result, the adoption of sheet molding compounds could slowdown in the long term with the rising popularity of sheet molding compounds.

Another growth deterrent is the high price of carbon fiber. As the focus of manufacturers moves towards offering lightweight materials for creating detailed and complex parts for numerous end-use industries, glass and carbon fibers are being preferred over steel and aluminum. Rising prices of carbon fiber could further shift the preference of end-use industries to long-fiber injection.

Amidst the high impact of influencers and growth deterrents, the sheet molding compound market is likely to progress at a CAGR of ~5% during the forecast period 2019-2029. Being an asset to numerous end-use industries - automotive, construction, consumer goods, healthcare, marine, aviation & defense, and electronics & electrical, sheet molding compounds are undergoing through product-level changes with advanced technologies.

This helps the market players bundle quality with their products and be able to cater to the evolving demands of end-use industries. For instance, IDI Composites International invested in a research and development facility in Noblesville for integrating advanced technologies for the discovery of new materials.

Apart from the product-level strategy, market players look at Europe as a high RoI potential market. For instance, in May 2017, Ashland Inc. announced the acquisition of a manufacturing facility of Reichhold, with an intent to strengthen its position in the sheet molding compounds market in Europe, while having a high consumer base in North America, Latin America, and Asia Pacific. However, the exponential progress of East Asia can turn out to be a game-changer for market players.

A focus on China, Japan, and South Korea and an investment in these regions, intended on catering to needs of the automotive industry and consumer goods industry will help them gain desired momentum in the sheet molding compounds market.

The report consists of a comprehensive data about the volume (Tons), value (US$ Mn) trends related to the market, market forecasts, competition dashboard, market dynamics, and current trends & developments pertaining to the global sheet molding compounds (SMC) market during the forecast period 2019 - 2029.

The global sheet molding compounds (SMC) market is estimated to be valued at ~US$ 1.9 Bn by the end of 2019, and is expected to reach ~US$ 3.2 Bn by the end of 2029, growing at a CAGR of over ~5% during the forecast period. The global sheet molding compounds (SMC) market is expected to represent an incremental opportunity of ~US$ 1.2Bn between 2019 and 2029.

Bundles of glass and carbon filaments are used to reinforce sheet molding compounds (SMC). These bundles are obtained by chopping continuous glass roving’s in-line in the compounding machine. In currently developed SMC, carbon fibers are blended with epoxy resins, vinylester, and UP (Unsaturated Polyester) resins.

Carbon fiber reinforced SMC provides smooth surface finish. Usually, SMC are thin sheets consisting of fibers and thermoset resins, which are subsequently cut and cured in a compression molding process to create composite parts.

Due to the inherent limitations of metals as well as increasing prices, many manufacturers use thermoset composites as a replacement for metal for high-performance applications, which in turn, propel the growth of the sheet molding compounds (SMC) market.

Furthermore, construction applications are expected to be driven by lower maintenance requirements and corrosion resistant qualities of reinforced products in applications such as pipe, tanks, shower enclosures, and other bathroom components, which also creates a positive impact on the market of sheet molding compounds (SMC).

The sheet molding compounds (SMC) market has witnessed consistent growth over the past years. This can be attributed to favorable economic conditions in several countries. The automotive industry is anticipated to witness acceleration due to the increasing demand for domestic as well as commercial vehicles, which is expected to create opportunities for the sheet molding compounds (SMC) market.

Sheet molding compounds (SMC) are multipurpose materials: their formulations can be adjusted and custom-made to meet the requirement of a diverse range of applications in automotive and truck manufacturing industries, which are mainly driving the market of sheet molding compounds (SMC) technology.

Sheet molding compounds (SMC) provides a surface finish to exhibit an aspect of smoothness, flatness, and light reflection similar to that of stamped steels. Sheet molding compounds (SMC) also provide flexibility and design freedom by incorporating geometric details and shape complexity, owing to the increasing demand for sheet molding compounds (SMC) from automotive and truck industries.

The production of durable equipment is expected to be stimulated by the rising demand for electrical and electronic products such as telecommunications equipment, computing systems, and requirements for productivity enhancement, which results in the upsurge demand for sheet molding compounds (SMC) from electrical and electronic industry.

Alternative for sheet molding compounds (SMC) in the market such as long fiber injections (LFI) hinder the future growth of the sheet molding compounds (SMC) market. Long fiber injection (LFI) is more cost efficient and its process is more economical as compared to sheet molding compounds (SMC), which are used to create detailed and complex parts for several end-use industries.

Moreover, long fiber injection (LFI) share same advantage as of sheet molding compounds (SMC) such as production speed, etc. In recent years, long fiber injection (LFI) gained immense popularity in various applications such as consumer goods, automotive, etc.

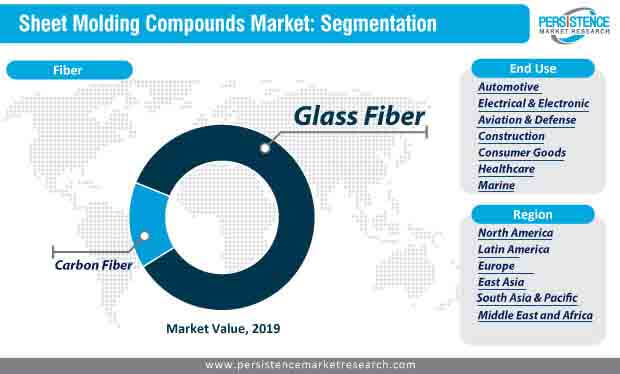

In order to offer macroscopic as well as microscopic view of the sheet molding compounds market, our analysts have segregated the market into key segments, based on the fiber, end use, and region. This comprehensive study also analyzes the incremental growth opportunity present in the sheet molding compounds market during the forecast period. The key segments of the sheet molding compounds market are:

| Attribute | Details |

|---|---|

| Fiber |

|

| End Use |

|

| Region |

|

This comprehensive research report answers the key questions concerning the leading and emerging market players regarding the growth of the sheet molding compounds during the forecast period 2019-2029. The key questions answered in this research report include:

To know more about delivery timeline for this report Contact Sales