- Metalworking & Fabrication

- Metal Sheet Bending Machine Market

Metal Sheet Bending Machine Market Size, Share, and Growth Forecast 2026 - 2033

Metal Sheet Bending Machine Market by Product Type (Press Brake, Folding Machine, Roll Bending Machine), End User (Automotive, Aerospace, Construction, Manufacturing), by Regional Analysis, 2026 - 2033

Metal Sheet Bending Machine Market Size and Trend Analysis

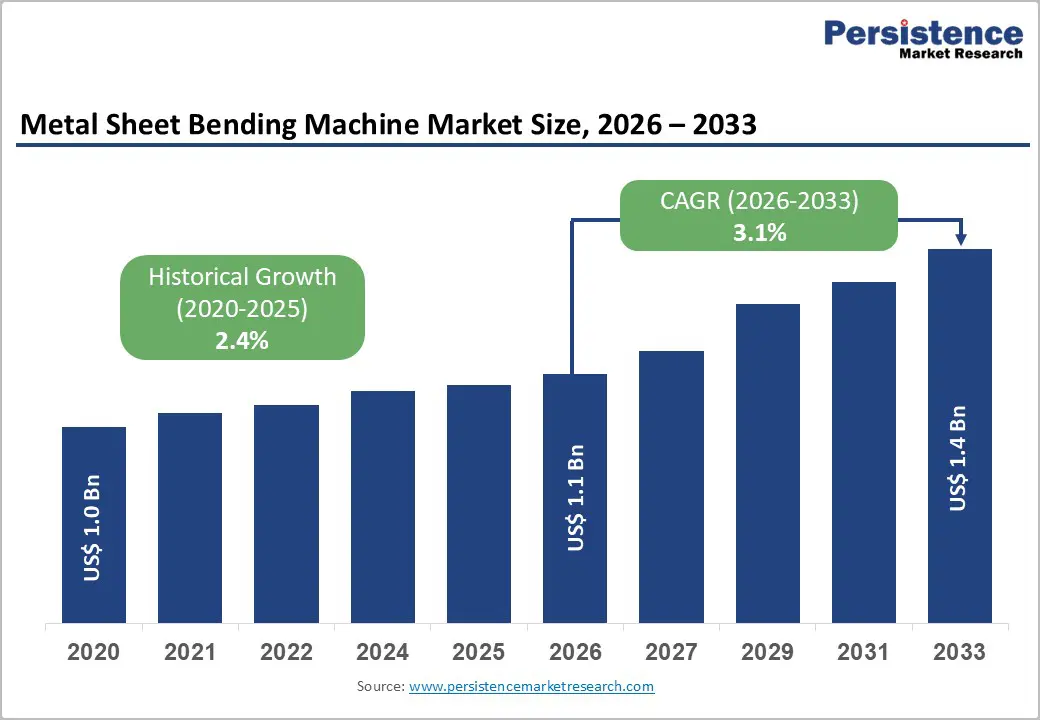

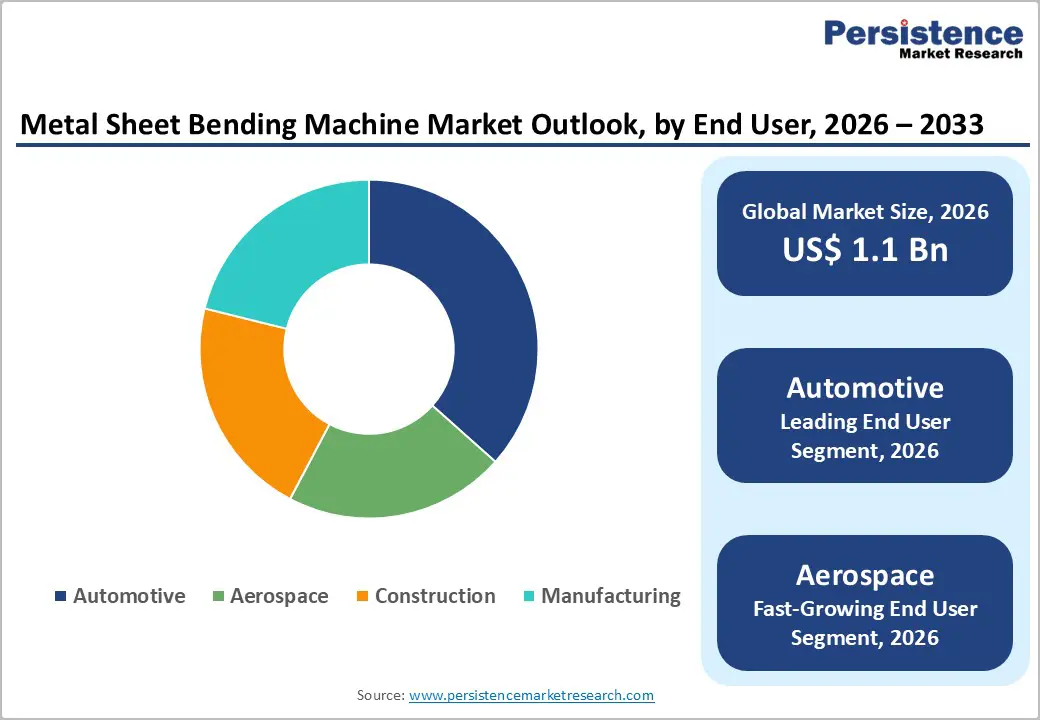

The global metal sheet bending machine market size is expected to be valued at US$ 1.1 billion in 2026 and projected to reach US$ 1.4 billion by 2033, growing at a CAGR of 3.1% between 2026 and 2033.

The market is poised for steady expansion, underpinned by accelerating industrialization across emerging economies and a broad-based recovery in automotive and construction output. Global manufacturing output, as tracked by the United Nations Industrial Development Organization (UNIDO), has rebounded consistently since 2021, fueling capital investment in precision metal fabrication equipment. Rising demand for energy-efficient, CNC-integrated bending solutions further reinforces the long-term growth trajectory, as manufacturers increasingly prioritize automated forming technologies to reduce scrap rates and improve throughput across high-mix, low-volume production environments.

Key Industry Highlights

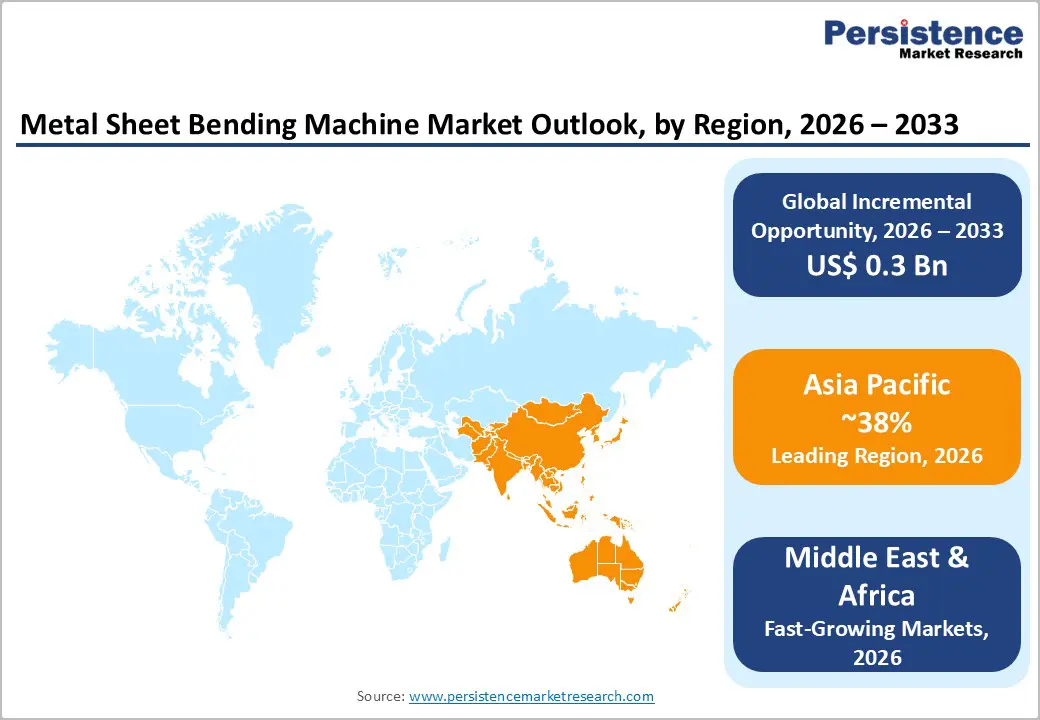

- Leading Region: Asia Pacific leads the global Metal Sheet Bending Machine market, holding approximately ~38% revenue share in 2025, driven by China’s massive automotive and construction manufacturing base and Japan’s advanced precision fabrication industry.

- Fastest Growing Region: Middle East & Africa is the fastest growing regional market over 2026 - 2033, supported by ambitious infrastructure development programs, growing construction activity, and expanding industrialization efforts in Saudi Arabia, UAE, and South Africa.

- Dominant Product Type: Press Brake dominates the Product Type segment with ~45% market share in 2025, underpinned by unmatched versatility across sheet thicknesses, broad tooling compatibility, and widespread adoption in CNC-automated fabrication environments.

- Fastest-Growing Product Type: Aerospace is the fastest-growing end-user segment over 2026 - 2033, propelled by record commercial aircraft order backlogs at Airbus and Boeing, rising defense spending across NATO member states, and tightening tolerances driving demand for high-precision bending solutions.

- Key Opportunity: Robotic bending cell integration represents the key market opportunity, offering manufacturers automated, lights-out forming capabilities that reduce labor dependency, increase throughput consistency, and deliver strong ROI in high-mix automotive and aerospace component production.

| Key Insights | Details |

|---|---|

| Metal Sheet Bending Machine Market Size (2026E) | US$ 1.1 Billion |

| Market Value Forecast (2033F) | US$ 1.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 3.1% |

| Historical Market Growth (2020 - 2025) | 2.4% |

Market Dynamics

Drivers - Rising Industrial Automation and CNC Integration in Metal Fabrication

The global shift toward smart manufacturing and Industry 4.0 adoption is a primary catalyst for the metal sheet-bending machine market. Modern press brakes and folding machines equipped with CNC controls, real-time angle correction, and offline programming capabilities are increasingly replacing conventional mechanical bending equipment. According to the International Federation of Robotics (IFR), global robot installations in general industry, including metal fabrication, reached a record 553,052 units in 2022, indicating robust investment in automation. CNC press brakes, in particular, enable consistent bend angles within a ±0.1° tolerance, dramatically reducing rework costs. As manufacturers in North America, Europe, and the Asia Pacific modernize their shop floors to remain globally competitive, procurement of advanced bending machinery is becoming a critical capital expenditure priority across small and mid-sized fabrication enterprises.

Sustained Growth in the Automotive and Construction Sectors

Demand from end-user industries, particularly automotive and construction, remains a fundamental growth driver for the metal sheet-bending machine market. The global automotive industry, which consumes significant volumes of precision-bent sheet metal components for body panels, chassis structures, and brackets, is in the midst of a major transformation driven by the development of electric vehicle (EV) platforms. The International Energy Agency (IEA) reported that global EV sales surpassed 14 million units in 2023, up 35% year-on-year, spurring investments in new stamping and bending lines at tier-1 and tier-2 suppliers. Simultaneously, infrastructure development across the Asia Pacific and the Middle East, with public construction spending projected to grow substantially through the late 2020s according to the World Bank, is generating elevated demand for structural sheet metal components, directly driving bending machine procurement.

Restraints - High Initial Capital Expenditure and Total Cost of Ownership

One of the most significant barriers to market expansion is the elevated initial investment required for advanced metal sheet-bending machines, particularly CNC and hydraulic press brakes from premium European and Japanese manufacturers. Entry-level CNC press brakes can range from US$ 30,000 to over US$ 250,000, while high-tonnage systems with automated tool changers and adaptive bend sensing can cost well above US$ 500,000. For small and medium-sized enterprises (SMEs), which constitute the vast majority of the global metal fabrication workforce, as noted by the European Commission’s SME Performance Review, this financial threshold poses a formidable hurdle to adoption. Additionally, maintenance, tooling replacement, and software licensing add substantially to the total cost of ownership, dampening replacement cycles, especially in price-sensitive developing markets.

Shortage of Skilled Operators and Programmers

Even as bending machines become increasingly automated, they still require skilled CNC programmers, tooling specialists, and maintenance technicians to operate at optimal capacity. The global manufacturing sector is facing a pronounced skills gap: the Manufacturing Institute in the United States estimates that over 2.1 million manufacturing jobs could remain unfilled through 2030 due to workforce shortages. Operating and programming modern bending machines, which require proficiency in CAD/CAM integration, bend simulation software, and quality inspection protocols, presents a real barrier for facilities that lack technical training infrastructure. This talent shortfall limits the operational efficiency gains that investments in advanced bending equipment are designed to deliver, effectively reducing ROI for end users and moderating procurement urgency across several regional markets.

Opportunity - Adoption of Automated Robotic Bending Cells for High-Volume Production

The integration of robotic material handling with press brakes and folding machines represents a significant and growing opportunity for market participants. Fully automated bending cells, comprising a robot arm, automated tool changer, and vision-guided part positioning, are gaining traction in automotive, appliance, and HVAC manufacturing, where repetitive high-volume bending of standardized geometries is commonplace. Industry data from the Association for Manufacturing Technology (AMT) in the United States indicate a consistent rise in orders for automation-integrated fabrication systems, particularly post-pandemic, amid intensifying labor cost pressures. Vendors that develop pre-engineered robotic bending cell packages with plug-and-play integration, simplified programming interfaces, and ROI-focused leasing models stand to capture substantial market share among mid-sized manufacturers transitioning from manual to automated forming workflows over the 2026 - 2033 forecast period.

Expanding Aerospace Manufacturing and Defense Procurement Programs

The aerospace and defense sector presents a compelling long-term growth opportunity for specialized metal sheet-bending machine suppliers. Commercial aircraft production is recovering robustly following pandemic disruptions. Airbus delivered 735 commercial aircraft in 2023 and is targeting significantly higher output through 2026 to clear its order backlog of over 8,500 aircraft, according to the company’s official delivery reports. Each commercial aircraft contains thousands of precision sheet metal components requiring controlled bending to tight tolerances, including fuselage skins, nacelle panels, and structural ribs. Additionally, rising global defense budgets, with NATO members increasingly committing to the 2% of GDP defense spending target, are driving demand for military aerospace and armored vehicle sheet-metal components. Manufacturers offering multi-axis bending machines with aerospace-grade accuracy certifications (e.g., AS9100) are well-positioned to capitalize on this expanding order pipeline.

Category-wise Analysis

Product Type Insights

The press brake segment holds the leading position in the metal sheet bending machine market by product type, accounting for an estimated ~45% share of total market revenue in 2025. Press brakes, available in hydraulic, electro-hydraulic, and all-electric variants, are the most versatile and widely deployed bending machines across metal fabrication shops globally, capable of forming a broad range of material thicknesses and lengths in a single setup. Their compatibility with quick-change tooling systems, offline programming via software platforms such as TRUMPF TruTops Bend and Amada Dr. ABE_Bend, and integration with adaptive crowning systems make them indispensable in high-mix production environments. The proliferation of energy-efficient all-electric press brakes, which consume up to 50% less energy than conventional hydraulic models according to manufacturer benchmarks, has further reinforced adoption rates, particularly among European fabricators seeking to comply with energy regulations under the EU Industrial Emissions Directive.

End-user Insights

The automotive end-user segment commands the largest share of the metal sheet bending machine market, estimated at approximately ~35% of total demand in 2025. Automotive manufacturing requires an extensive array of precision-bent sheet metal components, including body-in-white structural members, door panels, underbody brackets, and battery enclosure housings for electric vehicles, that demand high repeatability and tight angular tolerances. The global light vehicle production volume, as reported by the International Organization of Motor Vehicle Manufacturers (OICA), reached approximately 93.5 million units in 2023, underscoring the scale of downstream component demand. The ongoing EV transition is particularly impactful: battery enclosures and thermal management components for EVs introduce new forming requirements, prompting automotive tier suppliers to invest in precision CNC press brakes and robotic bending cells capable of processing high-strength aluminum and advanced high-strength steel alloys.

Regional Insights

North America Metal Sheet Bending Machine Market Trends and Insights

North America remains a leading region in the global metal sheet bending machine market, driven primarily by the United States, which hosts one of the world’s most advanced manufacturing ecosystems. The U.S. Bureau of Economic Analysis reports that manufacturing contributes approximately 11% to national GDP, with metal fabrication constituting a critical subsector. The resurgence of domestic automotive production, aerospace manufacturing centered in states such as Washington, Texas, and Connecticut, and significant infrastructure investment under the Infrastructure Investment and Jobs Act (2021), which allocated over US$ 1.2 trillion, have collectively generated sustained demand for metal forming equipment.

The U.S. market is further characterized by a strong innovation ecosystem, with leading OEMs such as Amada and Trumpf maintaining dedicated technology centers and training facilities to support customer productivity. The adoption of smart press brakes with IoT connectivity and predictive maintenance capabilities is advancing more rapidly in North America than in most other regions, supported by robust digital infrastructure and a culture of lean manufacturing optimization. Canada’s growing aerospace sector, particularly around Montreal and Toronto, also contributes meaningfully to regional market demand.

Europe Metal Sheet Bending Machine Market Trends and Insights

Europe represents a mature but technologically sophisticated market for metal sheet-bending machines, with Germany, Italy, France, Spain, and the United Kingdom collectively accounting for the bulk of regional demand. Germany, as Europe’s foremost industrial economy, leads the region. The country’s machine tool and metalworking equipment sector is among the world’s largest, with the German Machine Tool Builders’ Association (VDW) reporting total machine tool production of approximately €14.9 billion in 2023. German manufacturers such as LVD Group and EHT Werkzeugtechnik GmbH are recognized globally for engineering excellence in bending technology, and their export-driven business models reinforce Europe’s competitive stature.

Regulatory harmonization across the European Union, particularly directives relating to machinery safety (EU Machinery Regulation 2023/1230), energy efficiency (Ecodesign Directive), and workplace ergonomics, is shaping product development priorities for European bending machine manufacturers. The transition toward all-electric press brakes is most pronounced in Europe due to energy cost pressures and decarbonization commitments. Italy’s thriving sheet metal fabrication industry and France’s defense and aerospace manufacturing base also contribute to steady regional demand, while Spain and Eastern European nations are emerging as growing markets for installations as manufacturing operations expand.

Asia Pacific Metal Sheet Bending Machine Market Trends and Insights

Asia Pacific is both the leading region and the fastest-growing market for metal sheet-bending machines, driven by the industrial powerhouses of China, Japan, India, and the ASEAN manufacturing corridor. China alone accounts for a dominant share of regional demand, supported by its massive automotive production base. The China Association of Automobile Manufacturers (CAAM) reported Chinese vehicle production of approximately 30.16 million units in 2023, and vast construction and infrastructure investment under policy frameworks such as the Belt and Road Initiative. Chinese domestic manufacturers compete vigorously on price, while multinational OEMs compete on precision, automation, and after-sales support.

Japan remains a technology leader in the region, with firms such as Amada Co., Ltd. and Mitsubishi Electric Corporation investing continuously in next-generation servo-electric and hybrid press brake platforms. India is emerging as a high-growth market: the country’s Production Linked Incentive (PLI) scheme for advanced manufacturing and the National Infrastructure Pipeline (NIP), with a projected outlay of over INR 111 trillion (~US$ 1.3 trillion), are catalyzing large-scale investments in fabricated metal components. ASEAN nations, particularly Vietnam, Thailand, and Indonesia, are experiencing rapid expansion of their industrial bases as global supply chains diversify away from single-country dependencies, generating incremental demand for metal-forming equipment.

Competitive Landscape

The global metal sheet bending machine market is moderately consolidated, characterized by a limited number of multinational manufacturers controlling a significant revenue share alongside a broad base of regional and mid-sized producers. Tier-one participants compete primarily through technological leadership, leveraging advanced CNC platforms, servo-electric drive systems, and integrated digital control architectures to deliver higher precision, energy efficiency, and automation compatibility. Their strategies emphasize continuous R&D investment, expansion of global service networks, and long-term customer partnerships supported by training and lifecycle maintenance contracts.

At the same time, regional and value-oriented manufacturers target small and medium fabricators through competitive pricing, flexible customization, and shorter lead times. These players focus on application-specific configurations and localized after-sales support to strengthen customer retention. Across the competitive spectrum, companies are increasingly adopting smart manufacturing strategies, including cloud-enabled machine monitoring, predictive maintenance solutions, subscription-based software models, and turnkey robotic bending cells to enhance productivity, recurring revenue streams, and overall value proposition.

Key Developments:

- September 2025: TRUMPF unveiled a completely redesigned TruBend 3000 bending machine series at Blechexpo 2025, offering up to 40% faster throughput, improved precision, easier programming, and energy savings compared to its predecessor.

Companies Covered in Metal Sheet Bending Machine Market

- Sahinler Metal

- Amada Co., Ltd.

- Trumpf GmbH + Co. KG

- Koritnik Kovinarstvo Peskanje

- Adendorff

- ROJEK (CZ)

- CIDAN Machinery Americas

- HM Transtech

- Bystronic AG

- LVD Group

- Baileigh Industrial, Inc.

- Haco Group

- EHT Werkzeugtechnik GmbH

- Mitsubishi Electric Corporation

- Meyer Burger Technology AG

- Prima Power (Finn-Power)

- Ermaksan Makine San. ve Tic. A.S.

- Dener Makine

Frequently Asked Questions

The global Metal Sheet Bending Machine market is valued at US$ 1.1 billion in 2026 and is projected to reach US$ 1.4 billion by 2033 at a CAGR of 3.1%.

Demand is driven by Industry 4.0 adoption, increasing use of CNC and servo-electric press brakes, EV-led automotive growth, and rising infrastructure investments.

Asia Pacific leads the market with around 38% revenue share in 2025, supported by strong automotive production and industrial expansion.

The major opportunity lies in automated robotic bending cells that enable lights-out manufacturing, reduce labor costs, and improve production efficiency.

Key players include Amada Co., Ltd., Trumpf GmbH + Co. KG, Bystronic AG, LVD Group, and Mitsubishi Electric Corporation, among others competing through innovation and global service networks.