- Testing, Inspection, & Certification

- Road Safety Systems Market

Road Safety Systems Market Size, Share, and Growth Forecast 2026 – 2033

Road Safety Systems Market by Solution Type (Red Light & Speed Enforcement, Incident Detection & Response), by Service Type (Professional Services, Managed Services), by Application (Bridges, Highways), and Regional Analysis, 2026 – 2033

Road Safety Systems Market Size and Trends Analysis

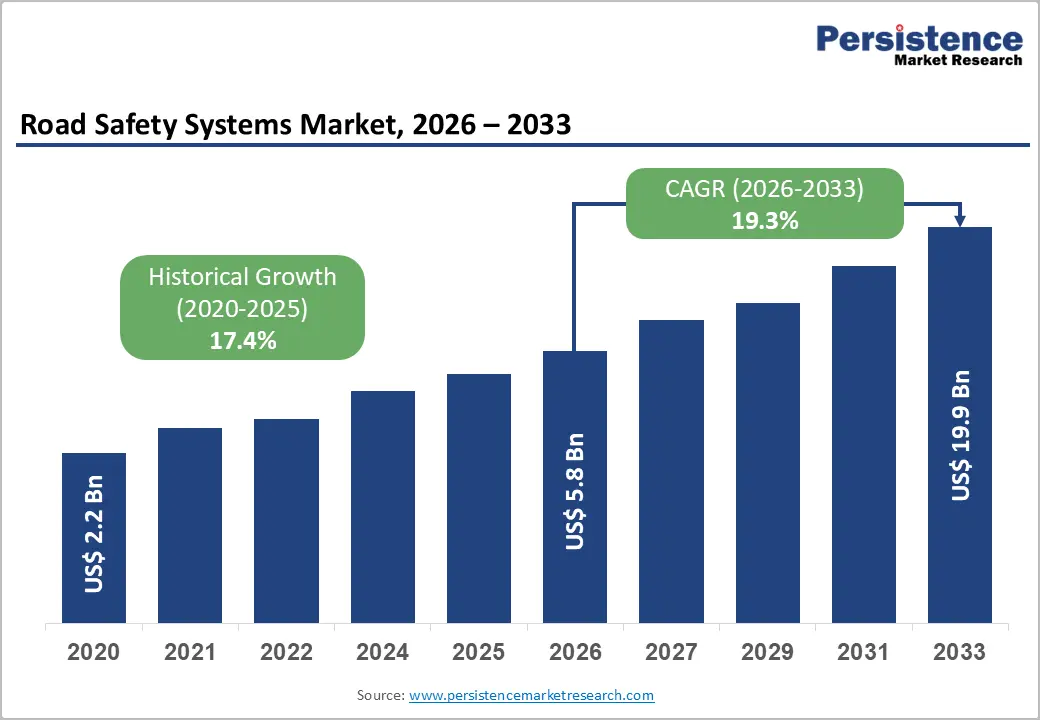

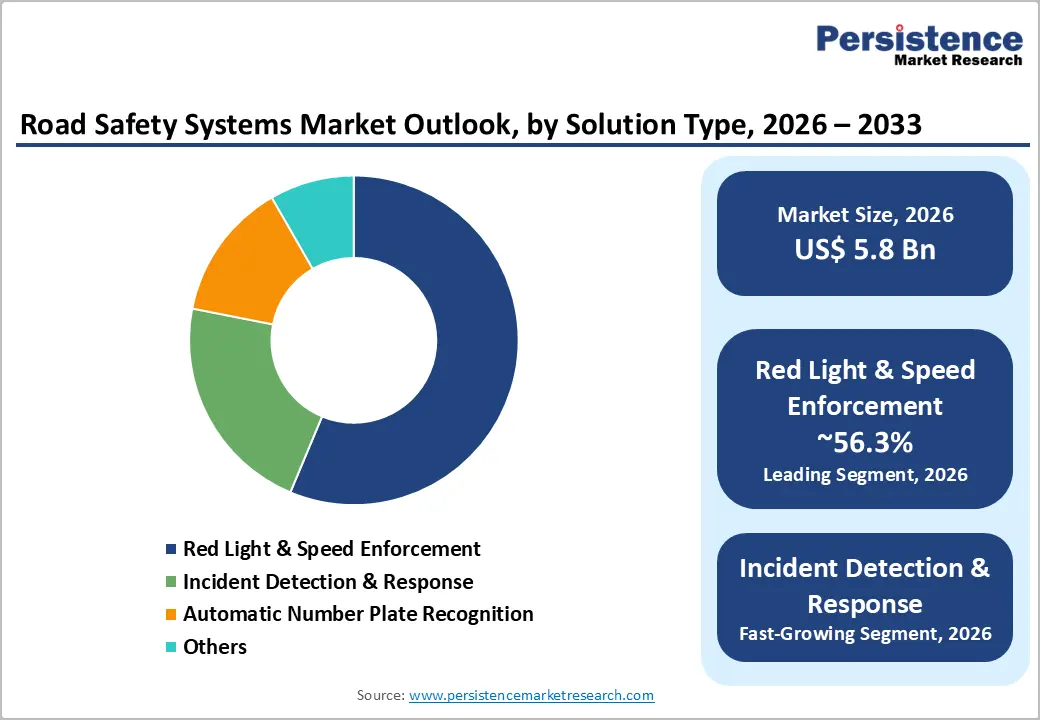

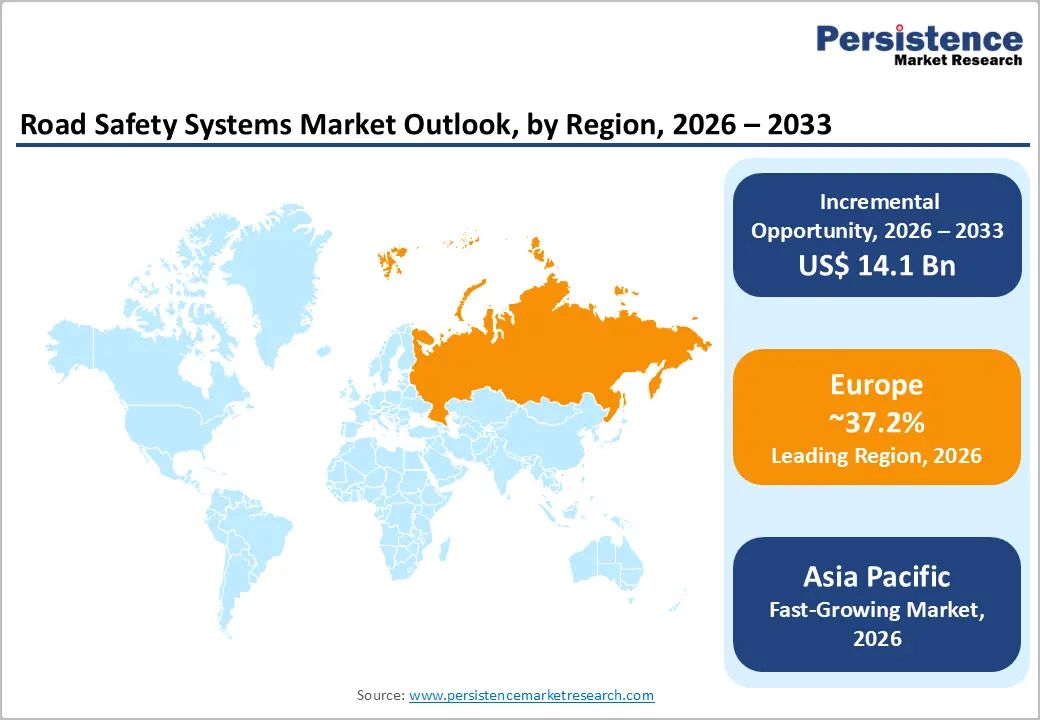

The global road safety systems market size is likely to be valued at US$5.8 billion in 2026 and is expected to reach US$19.9 billion by 2033, surging at a CAGR of 19.3% during the forecast period from 2026 to 2033, driven by the urgent need to reduce high rates of traffic fatalities and injuries. Strict government norms and increasing investment in smart infrastructure are also spurring demand.

Key Industry Highlights:

- Government Initiative: In October 2025, WHO Vietnam and the Asia Injury Prevention (AIP) Foundation officially launched the Vietnam Project 2000 Road Safety Partnership in Hanoi, joined by 15 other partners from civil society, academia, and the private sector. The initiative focused on motorcycle helmet safety, safe school zones, and child restraint systems.

- Leading Solution Type: Red light and speed enforcement, approximately 56.3% share in 2026, as speeding and signal violations remain the most common causes of severe urban road accidents.

- Dominant Service Type: Professional services, nearly 81.5% in 2026, as road safety systems require continuous integration, calibration, and regulatory compliance across multiple hardware and software platforms.

- Leading Region: Europe, with about 37.2% share in 2026, owing to its highly coordinated Intelligent Transport Systems (ITS) framework and cross-border traffic standardization policies.

- Fast-growing Region: Asia Pacific, as China, India, Japan, and South Korea are constantly investing in smart cities.

DRO Analysis

Driver

Increasing Number of Road Traffic Fatalities Worldwide

Road crashes remain one of the most persistent public health crises worldwide. Each year, 1.19 million people die on the world's roads, making road traffic injuries the leading cause of death among children and young adults between the ages of 5 and 29. What makes this more alarming is the economic dimension.

Fatal and non-fatal crash injuries are estimated to cost the world economy approximately US$3.6 trillion annually. Vulnerable road users such as pedestrians, cyclists, and motorcyclists make up more than half of all global road traffic fatalities. This persistent toll is pushing governments and private players to invest heavily in road safety systems, from smart infrastructure to in-vehicle alert technologies, as reactive measures are no longer seen as enough.

Implementation of Strict Safety Norms by Governments

Governments are no longer just setting targets, but they are enforcing them through binding regulations. India's Ministry of Road Transport and Highways (MoRTH) is a key example. MoRTH has confirmed that ADAS, including Automatic Emergency Braking, Lane Departure Warning, and Driver Drowsiness Alert, will be mandatory for all new heavy trucks and buses from October 1, 2027.

Starting April 2026, all new vehicles designed to carry more than eight passengers must also include ADAS features. These mandates are pushing automakers to adopt safety technologies at scale. At the global level, the UN Decade of Action for Road Safety (2021 to 2030) has set a target of halving road traffic deaths and injuries by 2030, creating a framework that is spurring regulatory action across multiple countries simultaneously.

Restraint

Technology Failures and Inconsistent Adoption in Certain Regions

Road safety systems are only as reliable as their design and deployment context. A peer-reviewed study published in PLOS ONE found that metal roadside barriers often fail to safely redirect vehicles in real-world crashes, even after passing standard lab tests. It is mainly as real impact angles differ from those used in testing. Beyond physical infrastructure, the adoption gap in lower-income regions is equally concerning.

Safety measures that have worked well in high-income countries may not translate equally to other contexts, given weaker enforcement, poor road conditions, and limited data systems. A February 2025 World Bank press release reinforced this, noting that traditional funding mechanisms are inadequate to meet the challenges of the global road safety crisis. It tends to leave several regions without the baseline infrastructure required to support novel safety technologies.

Opportunity

Emergence of Intelligent Transportation Systems and IoT

Intelligent Transportation Systems (ITS) paired with IoT sensors are moving road safety from reactive to predictive. A superior real-world example is Los Angeles's Automated Traffic Surveillance and Control (ATSAC) system. Starting with just 118 signals for the 1984 Olympics, it has expanded to a citywide network of over 4,850 adaptive signals that adjust timing in real time based on live traffic flow, cutting intersection delays by over 32%.

New York City's Connected Vehicle Pilot Program similarly uses AI and IoT to detect traffic incidents in real time, improving response times and reducing disruptions. These systems do more than ease congestion. They directly cut the conditions that lead to crashes, such as sudden stops, speeding, and signal confusion.

Use of Digital Twins to Visualize and Test Traffic Scenarios

Digital twins, i.e., virtual replicas of physical road environments, are opening a new frontier in infrastructure safety planning. Research published in Nature Scientific Reports (2025) demonstrated that a traffic digital twin of a road segment in Alabama could identify crash risks under varying weather and visibility conditions that traditional simulations entirely missed.

Digital twins can also continuously monitor infrastructure health, flagging road damage or signal failures before they cause accidents. They can model pedestrian and cyclist behavior to improve visibility and safety in design. Singapore has taken this further by building a digital twin of the entire city to monitor urban development and infrastructure requirements in real time.

Category-wise Analysis

Solution Type Insights

The red light and speed enforcement segment is expected to dominate with nearly 56.3% of the share in 2026. Speed and red-light violations are among the most direct causes of fatal crashes. Governments and transportation authorities are deploying automated enforcement systems such as red-light cameras and speed detection technologies to monitor violations at intersections, highways, and high-risk road corridors in real time. Modern systems, including Jenoptik's TraffiStar and VECTOR SR cameras, can simultaneously monitor up to four lanes, detect violations, and process citations without human intervention.

The incident detection and response segment is predicted to remain in the second position in 2026. The speed of response after a crash directly determines how many lives are saved. In road works and tunnels, real-time incident detection enables traffic to be steered away from hazards before situations escalate. Speed limits can be adjusted automatically, lanes closed when necessary, and drivers warned early via Variable Message Signs, in-tunnel systems, or dashboard indicators. AI is making these systems smarter than ever.

Service Type Insights

The professional services segment is projected to lead in 2026 with a share of approximately 81.5%. Road safety technology is not plug-and-play. Installing cameras, radars, back-office software, and enforcement platforms requires expert consultation, system integration, site surveys, and staff training. Professional services typically include consulting, system design, installation, integration, training, and ongoing technical support associated with traffic monitoring and enforcement technologies.

Managed services are anticipated to be the fastest-growing segment in 2026, as government bodies mainly prefer to outsource the operation and upkeep of traffic safety systems rather than manage them in-house. The segment is also expected to surge, backed by the high demand for outsourcing such services. This model shifts the burden of hardware upgrades, software maintenance, and system availability away from public agencies. Jenoptik's contract with the City of Brampton, Ontario, for instance, is structured as a full five-year managed deal covering delivery, installation, operation, and maintenance of 185 automated speed enforcement cameras.

Regional Insights

Europe Road Safety Systems Market Trends

In 2026, Europe is expected to lead with a share of approximately 37.2%, owing to binding regulations, well-established infrastructure, and long-term safety commitments. In 2024, about 19,940 people lost their lives in road crashes across the EU, and the bloc has set a Vision Zero goal of halving road deaths by 2030 and eliminating them by 2050.

The target directly funds enforcement and technology investment across member states. The EU Road Safety Exchange project, in its second phase from 2023 to 2025, extended to involve 19 countries, helping them adopt road safety measures ranging from Vision Zero policies to automated traffic fine processing centers.

Germany Road Safety Systems Market Trends

Germany is a prominent hub for intelligent transport investment in Europe. The country is home to global road safety technology leaders such as Jenoptik and Siemens, and is actively upgrading its national highway system. In February 2025, Siemens Mobility secured a EUR 2.8 billion framework with Deutsche Bahn to supply modern control and safety technology.

In May 2025, Kapsch launched a new intelligent transport system designed for urban areas of Germany. The country’s Autobahn network also demands continuous investment in speed monitoring and incident detection, keeping its road safety technology field highly active.

U.K. Road Safety Systems Market Trends

The U.K. is at a turning point. It is spending heavily on safety technology while rethinking its smart motorway strategy. In April 2023, the government scrapped plans for new smart motorways after public safety concerns and promised £900 million in safety improvements to existing stretches.

In the country’s third road investment strategy for 2025 to 2030, smart roads will become more interconnected, predictive, and automated, with digital twins playing a prominent role in planning and AI increasingly supporting operational decisions. On enforcement, National Highways confirmed plans to install HADECS 4 cameras, featuring 12MP resolution and weather-adaptive detection algorithms, on all All-Lane Running smart motorway sections by the end of 2025.

Asia Pacific Road Safety Systems Market Trends

Asia Pacific combines the world's fastest urbanization with some of its highest road fatality rates. It is a combination that is pushing urgent investment in road safety systems. Ongoing urbanization and population growth in countries such as China, India, and Southeast Asian nations have led to increased vehicle density, which in turn boosts demand for road safety solutions.

Government bodies are also coming forward with new investment plans. China invests over US$10 billion annually in urban traffic management and smart city projects. India's Smart Cities Mission has further allocated US$28 billion for infrastructure development, including AI-based traffic management solutions.

China Road Safety Systems Market Trends

China's scale of urbanization and vehicle ownership makes road safety infrastructure a national priority. It dominates the market in Asia Pacific due to its high number of automotive vehicles and population density, which together fuel traffic congestion and the demand for road safety solutions. The government has mandated interoperability standards for smart highway deployments and is channeling billions into connected road infrastructure.

Projects range from AI-assisted surveillance systems in cities to highway section speed control and vehicle-to-infrastructure communication trials. These are making China a consistent and large-volume buyer of road safety technology.

India Road Safety Systems Market Trends

India is being influenced by regulatory push and a rising fatality burden. In 2023, the country recorded approximately 4.8 lakh road accidents, resulting in 1.72 lakh fatalities. In response, the government is tightening standards significantly. India's Ministry of Road Transport and Highways (MoRTH) has confirmed that ADAS, including Automatic Emergency Braking, Lane Departure Warning, and Driver Drowsiness Alert, will be mandatory for all new heavy trucks and buses from October 1, 2027.

In February 2025, the Government of India announced a significant upgrade to Bharat NCAP, incorporating ADAS testing requirements starting in October 2027. These mandates are creating a large and near-term opportunity for technology suppliers, system integrators, and ADAS component manufacturers across India.

North America Road Safety Systems Market Trends

North America remains a large and stable market for road safety systems, augmented by consistent federal investment and a mature enforcement infrastructure. U.S. road fatalities fell an estimated 3.8% in 2024 to approximately 39,345 deaths, the first time below 40,000 since 2020. It showcases concerted investments via the Infrastructure Investment and Jobs Act, new safety programs, and sustained enforcement.

The region continues to expand automated enforcement programs, with San Francisco, Brampton, and other cities deploying new speed camera networks. However, growth is more measured compared to Asia Pacific, as North America already has a mature safety infrastructure base. The focus is shifting toward upgrading existing systems with AI analytics, connected vehicle integration, and automated response capabilities.

U.S. Road Safety Systems Market Trends

The U.S. benefits from superior federal funding frameworks and an active regulatory environment. The National Highway Traffic Safety Administration’s (NHTSA) FY 2025 budget request totaled US$1.6 billion, fully supporting vehicle safety programs under the Bipartisan Infrastructure Law. On the technology side, in April 2025, the U.S. Department of Transportation introduced a new Automated Vehicle Framework as part of its innovation agenda, and NHTSA opened approximately 33 investigations in FY 2025. Cities are also extending automated enforcement. In the U.S., the San Francisco SFMTA approved the implementation of California's first automated speed safety program, including 33 speed camera locations, expected to be fully operational in early 2025.

Competitive Landscape

The global road safety systems market is moderately fragmented, with the presence of large transportation technology firms, traffic enforcement specialists, AI-based mobility start-ups, and regional infrastructure integrators. Leading companies such as Kapsch TrafficCom, SWARCO AG, Siemens Mobility, Jenoptik AG, and Sensys Gatso Group compete through integrated Intelligent Transportation Systems (ITS), adaptive traffic control, automated speed enforcement, AI-supported surveillance, and connected road infrastructure solutions.

Competition is increasingly shifting from standalone hardware deployment to software-led interfaces that combine real-time analytics, cloud connectivity, vehicle-to-everything (V2X) communication, and predictive traffic management. Companies are focusing on interoperable platforms that can modernize existing road infrastructure instead of requiring full replacement, which has become an important differentiator for winning smart city and highway modernization contracts.

Key Industry Developments:

- In October 2025, Jenoptik Smart Mobility Solutions, together with TrafficTech Middle East, signed a contract with the Greater Amman Municipality in Jordan to deploy 41 TraffiStar SR591 red-light and speed enforcement cameras, along with nine VECTOR SR point-to-point section-control devices on key highway stretches to monitor average speeds.

- In April 2025, Frontline Road Safety acquired InfraStripe, a leading specialty contractor focused on roadway safety solutions, from Soundcore Capital Partners. The acquisition expanded Frontline's capabilities in traffic control management, traffic safety signage, and work zone services, expanding its presence across more than 10 states.

- In January 2025, Bain Capital entered into a definitive agreement to acquire Frontline Road Safety from The Sterling Group. Headquartered in Denver with over 50 locations and approximately 1,750 employees, Frontline specializes in road marking and roadway safety services.

Companies Covered in Road Safety Systems Market

- Kapsch TrafficCom AG

- SWARCO AG

- Verra Mobility

- Sensys Gatso Group AB

- Jenoptik AG

- Siemens Mobility

- Teledyne FLIR

- Dahua Technology

- Motorola Solutions

- Iteris Inc.

- Conduent Incorporated

- Others

Frequently Asked Questions

The global road safety systems market is projected to be valued at US$5.8 billion in 2026.

The market is expected to reach US$19.9 billion by 2033.

Key market trends include AI-supported traffic analytics and automated enforcement through Automatic Number Plate Recognition (ANPR).

Professional services are projected to lead with nearly 81.5% of the share in 2026, as governments prefer long-term service contracts for traffic monitoring.

The market is expected to grow at a CAGR of 19.3% from 2026 to 2033.

Kapsch TrafficCom AG, SWARCO AG, Verra Mobility, Sensys Gatso Group AB, and Jenoptik AG are a few key market players.