Resist Processing Equipment Market

Industry: Industrial Automation

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 195

Report ID: PMRREP35035

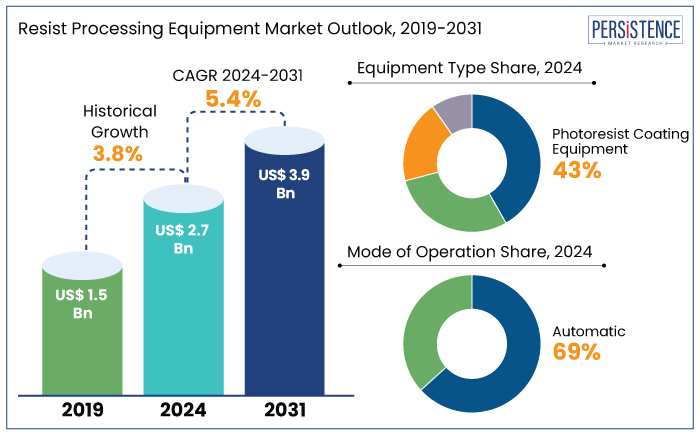

The global resist processing equipment market is projected to witness a CAGR of 5.4% during the forecast period from 2024 to 2031. It is anticipated to increase from US$ 2.7 Bn recorded in 2024 to US$ 3.9 Bn by 2031.

The resist processing equipment market is driven significantly by its applications in prominent end-use industries, particularly semiconductors and electronics. These industries are expanding rapidly due to advancements in integrated circuits and photolithography technologies, which rely heavily on high-precision resist processing equipment.

The growing demand for smaller, high-performance chips in consumer electronics and automotive applications, coupled with developments in extreme ultraviolet (EUV) lithography, continues to push the market forward. Moreover, the transition to next-generation lithography, including immersion lithography, is further boosting the need for advanced processing equipment.

The global semiconductor industry reported exports exceeding $43 billion as of recent years and continues to support over 240,000 jobs in the United States alone in terms of market statistics. The National Institute of Standards and Technology (NIST) plays a vital role by advancing metrology methods for lithography to support state-of-the-art resist technologies, demonstrating the critical role of innovation in market growth.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Resist Processing Equipment Market Size (2024E) |

US$ 2.7 Bn |

|

Projected Market Value (2031F) |

US$ 3.9 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

5.4% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

3.8% |

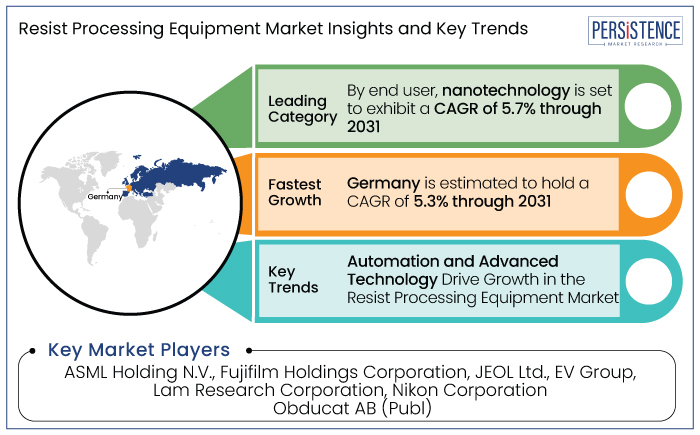

Germany is expected to record a CAGR of 5.3% through 2031 in the resist processing equipment market. The country's prominent position in semiconductor manufacturing and advancements in photolithography processes drive this growth.

Supported by a strong industrial foundation, cutting-edge research and development (R&D) capabilities, and a well-established ecosystem of semiconductor and microelectronics firms, Germany is poised to maintain its leadership in this critical sector. Additionally, government-backed initiatives and substantial investments in advanced manufacturing technologies further enhance Germany's dominance.

Germany maintains its lead through cutting-edge technological adoption and collaboration between equipment manufacturers and end users, including semiconductor fabs and electronics producers.

Compared to other countries in Europe, Germany hosts a higher number of semiconductor fabrication facilities and related industries, ensuring consistent demand for resist processing equipment. The country’s emphasis on automation and precision in manufacturing further solidifies its position as a leader in the region?.

One notable competitor in this market is ASML Holding, which has been instrumental in photolithography advancements. Recently, ASML announced developments in extreme ultraviolet (EUV) lithography technology, enhancing process efficiency and resolution for semiconductor production. This innovation aligns with Germany’s demand for advanced equipment to maintain its edge in the resist processing domain.

South Korea is poised to experience significant growth in East Asia resist processing equipment market, with an estimated CAGR of 6.3% through 2031. The country's strong presence in this market is largely attributed to its semiconductor manufacturing industry, with global giants like Samsung and SK Hynix leading the way in memory device production. Together, these companies command over 60% of the global market share in this segment.

Leadership drives a consistent demand for advanced resist processing equipment, which is critical for semiconductor fabrication, allowing South Korea to maintain its competitive edge in the global market. The dominance is further supported by South Korea’s extensive investment in semiconductor manufacturing facilities, with most fabs owned domestically. This contrasts with Japan and China, where foreign dependencies play a larger role.

South Korea’s emphasis on high-value, integrated device manufacturing (IDM) capabilities allows it to outpace regional peers in adopting cutting-edge resist processing technologies. One relevant competitor in the region is Japan-based Tokyo Electron, a leader in semiconductor equipment.

In a recent development, Tokyo Electron launched new advanced etch and resist coater systems to meet the demands of high-precision nodes for next-generation semiconductors. Consequently, reinforcing Japan's contribution to the ecosystem while competing with South Korea’s domestic suppliers?.

The photoresist coating equipment segment is expected to dominate the resist processing equipment market in the coming years, with an estimated CAGR of approximately 5%. This segment currently leads the market due to its crucial role in the production of semiconductors and microelectronics.

The growing demand for precise, high-performance materials in microchips and sensors fuels this leadership, with strong contributions from sectors such as consumer electronics, automotive, and telecommunications. As the need for miniaturized electronic components rises, the market position of photoresist coating equipment is further solidified.

Globally, this equipment type is integral in the fabrication processes of microelectromechanical systems (MEMS) and printed circuit boards (PCBs), particularly in semiconductor manufacturing. Photoresist coating is used to apply a light-sensitive material that is essential for etching intricate circuit patterns. This equipment finds extensive use in industries that require high-precision electronics, such as semiconductors, photonics, and nanotechnology?.

A prominent competitor in this market is Tokyo Electron Limited (TEL), a leading provider of semiconductor manufacturing equipment. TEL’s continuous innovations in resist processing technology have solidified its market presence.

Recently, TEL launched an advanced photoresist coating system, designed to increase throughput and improve coating uniformity for advanced semiconductor applications, reinforcing its competitive edge.

The automatic segment in resist processing equipment market is expected to witness significant growth, with a projected CAGR of 5.1% during the period from 2024 to 2031. This mode of operation commands a significant share of the market due to its efficiency, precision, and scalability, which are crucial for high-volume semiconductor and microelectronics manufacturing. Automation minimizes human error, boosts throughput, and ensures consistent quality, making it a preferred choice for industries requiring exceptional precision.

Globally, automatic resist processing systems are critical in semiconductor fabrication, where they are used for photolithography, etching, and patterning of intricate circuit designs. This mode of operation also serves high-precision applications in photonics, nanotechnology, and MEMS. The growth in automation aligns with the increasing demand for miniaturized, high-performance electronic devices?.

A key player in this segment is ASML, a leading supplier of photolithography equipment, including automated resist processing solutions. ASML’s recent development of extreme ultraviolet (EUV) lithography machines marks a significant step forward in semiconductor fabrication, enabling faster, more precise production of cutting-edge chips used in next-generation electronics.

The resist processing equipment market is poised for significant growth due to increasing demand in the semiconductor, nanotechnology, and photonics industries. As technological advancements continue in electronics and communications, there will be growing opportunities for resist processing in developing regions, particularly in Asia Pacific.

Innovations in miniaturization and the demand for high-performance chips will likely drive investments in advanced processing equipment?. Currently, the global market is experiencing a shift toward more automated, high-throughput processing systems.

The adoption of automated systems in semiconductor fabrication is particularly prominent, driven by the need for higher precision and fast production rates. As the global semiconductor industry expands, particularly with the rise of AI, 5G, and IoT technologies, the demand for resist processing equipment is intensifying?.

The trend toward automation aligns closely with the end users' focus on achieving higher operational efficiency and minimizing human error. Semiconductor manufacturers, in particular, are increasingly adopting automated resist processing technologies for photolithography, a critical step in chip production. This trend is fostering innovations that enhance production speed and accuracy, directly benefiting industries reliant on high-precision electronic components.

The resist processing equipment market was primarily driven by the booming semiconductor industry and advances in electronics manufacturing. The shift toward small, powerful electronic devices and the demand for high-precision components have propelled the development of new processing technologies. The market recorded a CAGR of 3.8% during the period from 2019 to 2023.

Key markets in North America, Europe, and Asia have consistently led the demand for resist processing equipment, particularly in semiconductor fabrication?. The combination of rising technological innovations, particularly in AI, 5G, and IoT, with a growing emphasis on automation and efficiency, has been central to market expansion. This shift is paving the way for the integration of new, cutting-edge processing systems to meet the evolving needs of industries like semiconductor and nanotechnology.

Sales of resist processing equipment are projected to record a CAGR of 5.4% during the forecast period between 2024 and 2031.

Surging Demand for Semiconductor Devices Remains a Primary Driver

The increasing global demand for semiconductor devices is a prominent driver for the resist processing equipment market. As industries like telecommunications, automotive, and consumer electronics increasingly rely on complex semiconductor systems, the need for advanced resist processing equipment has surged.

The miniaturization of devices, alongside the shift toward energy-efficient technologies, requires precision equipment to create small and efficient microchips. This is especially true in high-demand sectors such as 5G, AI, and IoT, where the performance of semiconductors plays a crucial role in device functionality and reliability?.

The growing complexity of chip designs calls for more advanced resist processing techniques that can handle intricate photolithographic patterns. The semiconductor industry's expansion is directly contributing to an uptick in the adoption of automated resist processing systems, which streamline production, reduce errors, and increase yield rates. As semiconductor fabrication scales up to meet these demands, the market for resist processing equipment will continue to experience notable growth?.

Growing Industries Reliant on Photonics and Nanotechnology

The rapid growth of industries reliant on nanotechnology and photonics is driving the demand for resist processing equipment. Nanotechnology's application in various sectors like medicine, electronics, and materials science has increased the need for precise fabrication methods. Similarly, the growing importance of photonics in telecommunications, sensors, and medical devices requires advanced resist processing techniques to fabricate microstructures with high precision at the nanoscale. These technologies demand specialized equipment capable of producing intricate patterns on substrates with minimal tolerances, a challenge addressed by modern resist processing tools?.

As the use of photonics and nanotechnology continues to expand, particularly in developing regions, the demand for resist processing equipment is expected to rise. The advancement in processing technologies like EUV (extreme ultraviolet) lithography further boosts the capabilities of equipment to handle these emerging applications.

Stringent Environmental Regulations and the Complexities of Advanced Technology

The resist processing equipment market faces notable challenges due to stringent environmental regulations and technical complexities. Increasing restrictions on hazardous materials like photoresists and solvents, driven by global sustainability goals, necessitate extensive research and development to develop eco-friendly alternatives. These regulatory demands disrupt traditional manufacturing workflows, impacting productivity and timelines?

The advanced technical nature of resist processing systems presents barriers in regions lacking skilled operators and robust infrastructure. This knowledge gap, particularly in emerging markets, hampers the adoption of high-precision systems, limiting growth opportunities for smaller enterprises. Together, these factors impose significant constraints on the industry's growth potential, requiring strategic adaptations from market players?.

Expanding Semiconductor Manufacturing in China

China's rapid growth in semiconductor manufacturing is a pivotal opportunity in the resist processing equipment market. The country has prioritized self-sufficiency in semiconductor production, with government programs like "Made in China 2025" aiming to bolster domestic capabilities.

Investments exceeding billions of dollars are funneled into building state-of-the-art fabrication plants (fabs), which require advanced resist processing technologies for photolithography and other critical steps. With initiatives like these, China has become a global leader in semiconductor equipment demand, accounting for a significant portion of global sales.

The rising number of fabs, particularly for advanced nodes, emphasizes the need for precision equipment tailored to meet production scalability and quality standards?. Leading players like Applied Materials have expanded their operations in China, offering localized services and innovative resist processing solutions. Their partnerships with fabs in China ensure the availability of cutting-edge equipment, fostering technological advancements and supporting the nation's semiconductor independence?.

Increasing Demand for Nanotechnology in the U.S.

The U.S. is witnessing significant advancements in nanotechnology, creating substantial opportunities for resist processing equipment. Applications in healthcare (drug delivery systems), electronics (miniaturized chips), and materials science (super-strong composites) are growing rapidly.

Research centers supported by both government funding and private investments are leading the charge, with precision equipment playing a central role in fabricating intricate nanostructures. As industries push the boundaries of miniaturization and precision, the U.S. is positioned as a hub for nanotechnology-driven innovation?.

Tokyo Electron has introduced high-resolution resist processing systems tailored for nanotechnology development. These systems are used in prominent U.S. research facilities and contribute to advancements in microfabrication techniques, enabling the production of nanodevices with unmatched precision and scalability.

The resist processing equipment market is highly competitive, with global players like Tokyo Electron Limited, Applied Materials, and ASML dominating the landscape. These companies compete on technology innovation, production scalability, and partnerships with leading semiconductor manufacturers.

Emerging companies from regions such as East Asia, particularly China and South Korea, are increasingly challenging established players by offering cost-efficient yet advanced solutions. This dynamic competition drives technological advancements and keeps market entry barriers high?.

Key players are adopting strategic initiatives to expand their market share and capture emerging opportunities. These include significant research and development investments to develop eco-friendly and high-precision systems, partnerships with semiconductor fabs, and acquisitions to strengthen their technological portfolios.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Equipment Type

By Distribution Channel

By End User

By Region

To know more about delivery timeline for this report Contact Sales

The market is projected to reach US$ 3.9 Bn by 2031.

The semiconductor industry holds a dominant share in the market.

Europe to account for 28% of market share in 2024.

Fujifilm Holdings Corp. and Nikon Corporation are recognized as the market leaders.

The automatic mode of operation is experiencing significant demand in the market.