- Food Ingredients & Additives

- Reduced Starch Syrup Market

Reduced Starch Syrup Market Size, Share, and Growth Forecast, 2026 - 2033

Reduced Starch Syrup Market by Product Type (Liquid, Powdered, Others), Starch Type (Low-saccharified Syrup, Maltose Syrup, Confectionery Syrup, Glucose-based Reduced Syrups, Others), Application (Food & Beverages, Pharmaceuticals, Cosmetics, Personal Care Products), and Regional Analysis for 2026 - 2033

Reduced Starch Syrup Market Share and Trends Analysis

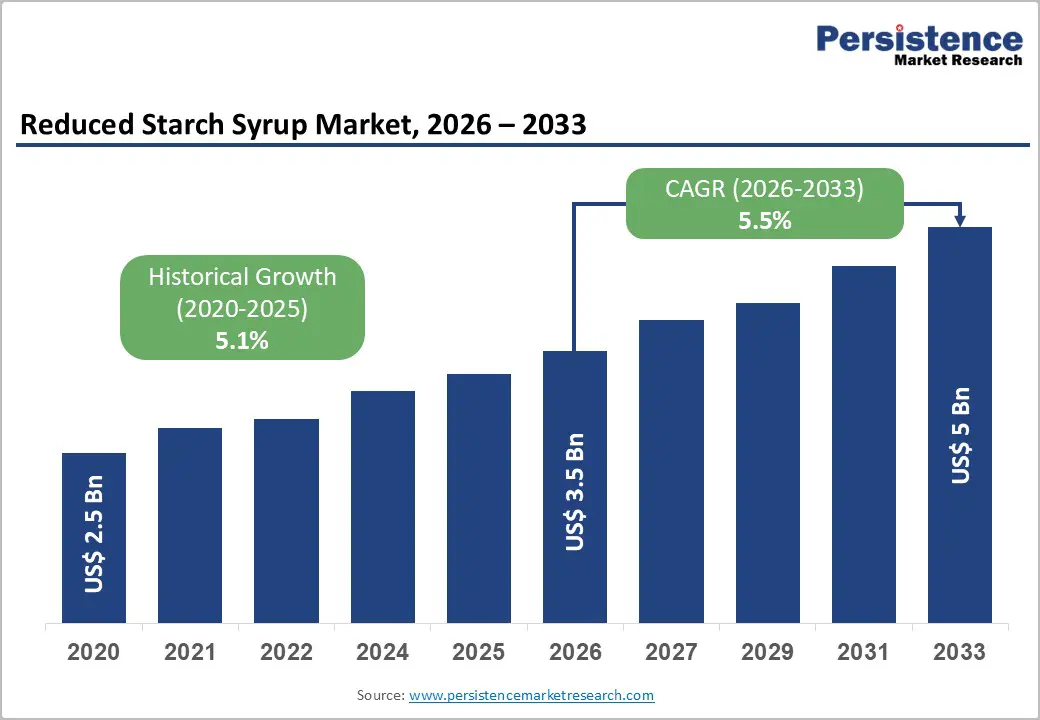

The global reduced starch syrup market size is likely to be valued at US$3.5 billion in 2026 and is estimated to reach US$5 billion by 2033, growing at a CAGR of 5.5% during the forecast period 2026−2033, driven by rising demand for functional sweeteners in food and beverage manufacturing, driven by glycemic shifts and pharmaceutical excipient adoption requiring stability and viscosity control, transition from sugar syrups toward modified carbohydrate systems aligned with World Health Organization (WHO) and United States Food and Drug Administration (FDA) food regulations, enzymatic hydrolysis sugar reduction policies, emerging economies, infrastructure investment, and innovation drivers.

Key Industry Highlights:

- Leading Starch Type: Glucose-based reduced starch syrup is expected to hold roughly 58% revenue share in 2026 due to broad functional applicability across confectionery, bakery, and pharmaceutical formulations.

- Fastest-growing Starch Type: Low-saccharified syrup is forecast to register the fastest growth between 2026 and 2033, driven by rising demand for reduced glycemic ingredients.

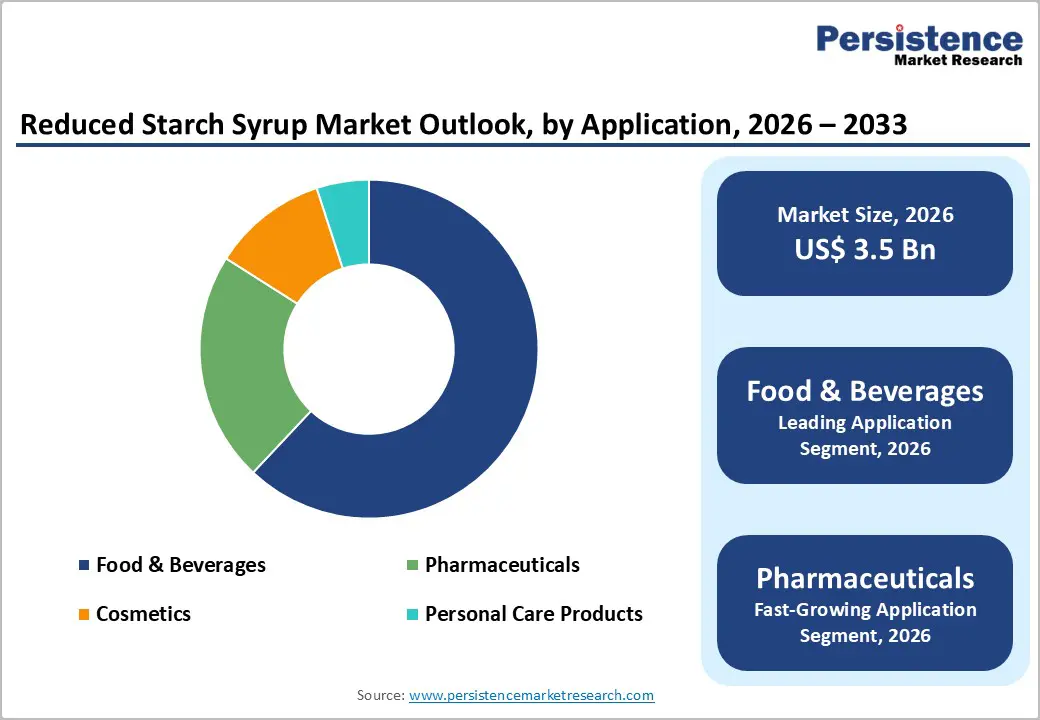

- Leading Application: Food and beverages are estimated to account for around 62% revenue share in 2026, supported by extensive integration in processed foods, beverages, and standardized industrial formulations.

- Fastest-growing Application: Pharmaceuticals is projected to be the fastest-growing segment, driven by increasing adoption in oral liquid dosage forms, nutraceuticals, and excipient standardization.

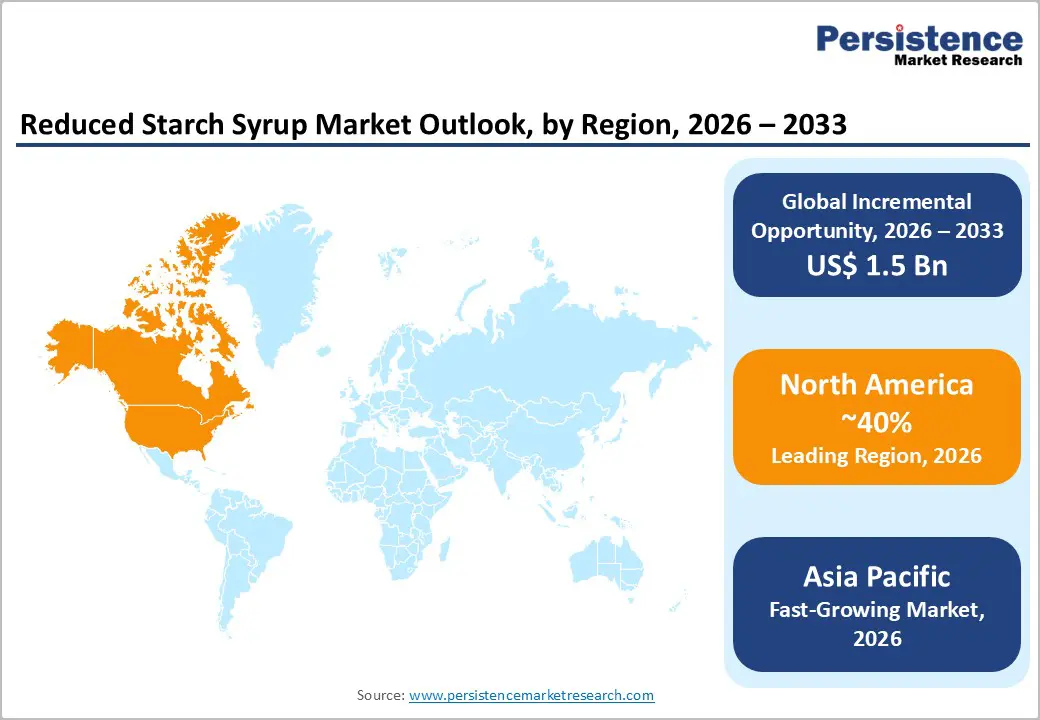

- Regional Leadership: North America is projected to capture approximately 40% market share by 2026, while Asia Pacific is forecast to record the fastest growth due to the rapid expansion of food manufacturing, pharmaceutical production, and urban consumption patterns.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players such as Cargill, Archer Daniels Midland, and Ingredion leveraging integrated starch processing networks, enzymatic conversion technologies, and large-scale distribution capabilities to maintain competitive positioning across global supply chains.

DRO Analysis

Driver - Expansion of Pharmaceutical and Nutraceutical Formulation Requirements

Expansion of pharmaceutical and nutraceutical formulation requirements strengthens demand for reduced starch syrup as a multifunctional excipient and sweetening base. Drug and supplement makers need ingredients that support taste masking, viscosity control, and uniform delivery in syrups, chewables, and liquid nutrition products. The 2025 United States Department of Agriculture (USDA) added-sugars rule for school meals set product-based limits of 6 grams per dry ounce for breakfast cereals, which reinforces formulation pressure across adjacent health products.

This policy climate pushes manufacturers toward ingredients that preserve palatability while meeting tighter label targets. The syrup fits that need through stable sweetness, consistent flow, and easier process integration in high-volume batches. Nutraceutical brands also favor it for cleaner ingredient statements and better consumer acceptance in daily-use formats. As prescription-style wellness products and fortified supplements expand, procurement shifts toward inputs that cut reformulation risk, simplify compliance, and support repeat production at scale.

Restraint - Volatility in Agricultural Starch Feedstock Supply and Pricing Pressure

Volatility in agricultural starch feedstock supply disrupts steady production planning across carbohydrate processing industries. Reduced starch syrup output relies on the consistent availability of corn, wheat, and other starch crops. Weather variation, soil conditions, and seasonal yield differences create irregular raw material flow. This leads to uncertainty in procurement schedules and limits long-term supply contracts. Production planning becomes less efficient when input availability shifts across harvest cycles. Manufacturers face difficulty in maintaining stable output levels for industrial food and pharmaceutical application systems.

Pricing pressure from unstable agricultural feedstock markets increases operational cost burden for syrup producers. Frequent fluctuations in corn and wheat prices raise input expenses and reduce margin stability. Procurement teams adjust sourcing strategies more often, leading to inefficiencies in supply chain coordination. Transportation and storage expenses also rise under unstable commodity conditions. Buyers reduce bulk commitments due to uncertain pricing trends. This weakens demand predictability and restricts smooth scaling of production capacity across manufacturing networks.

Opportunity - Integration of Bio-Processing Technologies and Enzymatic Conversion Innovation

Integration of bio-processing technologies and enzymatic conversion innovation improves starch transformation efficiency in syrup production. Advanced enzyme systems enhance conversion yield and reduce energy consumption in manufacturing operations. This creates cost advantages for large-scale processors and supports stable output quality. Improved process control increases product consistency across batches. Food manufacturers benefit from higher purity levels and reduced waste generation.

Enzymatic conversion innovation enables precise control of sweetness, viscosity, and functional stability in syrup formulations. This flexibility supports wider use in beverages, bakery products, and pharmaceutical preparations. Automated bio-processing platforms improve production reliability and reduce operational variation. Growing demand for clean-label ingredients encourages investment in enzyme-based processing systems. Enhanced efficiency supports scalable manufacturing models and improves resource utilization.

Category-wise Analysis

Application Insights

Food and beverages are likely to be the leading segment with an estimated 62% revenue share in 2026, due to structured integration across processed food manufacturing systems. Widespread use in bakery, confectionery, and beverage products supports strong demand. Examples include soft drinks, flavored syrups, cakes, and candies. Manufacturers use starch-based syrups for viscosity control, sweetness balance, and texture stability. Sugar reduction regulations and reformulation trends further drive adoption across retail and food service supply chains.

The pharmaceuticals segment is expected to witness the fastest growth between 2026 and 2033, as formulation innovation expands across liquid dosage systems and nutraceutical applications. Increasing use in oral syrups, cough formulations, pediatric medicines, and vitamin tonics supports demand. Manufacturers focus on viscosity control, stability, and compliance with United States Pharmacopeia (USP) and European Medicines Agency (EMA) standards, while nutraceutical drinks and dietary supplements drive additional uptake.

Starch Type Insights

The glucose-based reduced syrups segment is poised to lead with a forecast over 58% market share in 2026, owing to strong functional versatility and broad industrial adoption. Use in bakery products, soft drinks, confectionery items, cough syrups, and vitamin tonics supports demand. Functional stability, viscosity control, and compatibility across food and pharmaceutical formulations drive preference among manufacturers and strengthen large-scale supply chain integration.

The low-saccharified syrup segment is anticipated to be the fastest-growing segment between 2026 and 2033, driven by increasing demand for reduced glycemic ingredient systems and reformulation initiatives. Adoption in beverages, low-sugar snacks, diet drinks, and functional foods supports expansion. Food manufacturers shift toward healthier positioning, while e-commerce channels improve product reach. Regulatory sugar reduction policies and strict labeling standards in developed markets further strengthen uptake across retail and industrial applications.

Regional Insights

North America Reduced Starch Syrup Market Trends

North America is expected to lead with an estimated 40% of the reduced starch syrup market share in 2026, supported by advanced food processing infrastructure and high industrial standardization across ingredient manufacturing systems. Strong adoption across the U.S., Canada, and Mexico supports large-scale utilization in beverage, bakery, and pharmaceutical production. Companies such as Archer Daniels Midland, Cargill, and Ingredion drive integration through a consistent supply of functional carbohydrate solutions. United States Food and Drug Administration nutrition labeling regulations encourage reformulation toward controlled glycemic ingredients.

High concentration of multinational food and beverage producers strengthens procurement of starch-based syrups across standardized product lines. PepsiCo, Coca-Cola, General Mills, and Kraft Heinz integrate these ingredients in beverages, cereals, sauces, and bakery products. Demand stability is reinforced by clean label strategies and nutraceutical expansion across urban consumption centers. Advanced enzymatic processing and large-scale production facilities improve efficiency and consistency, supporting continuous ingredient substitution across diversified industrial applications in packaged food ecosystems.

Europe Reduced Starch Syrup Market Trends

Europe demonstrates strong regulatory-driven demand due to strict sugar reduction policies and structured nutritional labeling frameworks across food manufacturing systems. Germany shows high utilization in bakery, confectionery, and beverage production, supported by advanced industrial processing capacity. France reflects steady adoption in premium food and functional beverage categories, driven by clean label formulation strategies. The U.K. records consistent demand across soft drinks, sauces, and processed food systems influenced by public health nutrition guidelines. Italy integrates starch-based syrups in bakery and dairy desserts to improve texture, stability, and sensory balance.

Food manufacturers prioritize ingredient standardization and controlled glycemic profiles in formulation design. Companies such as Cargill, Tate and Lyle, and Ingredion maintain established supply networks across industrial food production systems. Expansion of convenience food consumption strengthens steady demand across retail and food service channels. Advancements in enzymatic conversion technology improve production efficiency and consistency, supporting wider adoption across diversified food and beverage manufacturing applications and industrial supply chains.

Asia Pacific Reduced Starch Syrup Market Trends

Asia Pacific is forecast to be the fastest-growing market for reduced starch syrup, stimulated by the rapid expansion of processed food manufacturing and rising demand for cost-efficient functional ingredients. China shows strong uptake through large-scale beverage and bakery production systems supported by modern ingredient processing facilities. India records increasing adoption across packaged foods, confectionery, and dairy-based beverages, driven by expanding urban consumption.

Japan and South Korea demonstrate advanced utilization in premium beverages, nutritional drinks, and pharmaceutical formulations supported by high-precision manufacturing standards. Companies such as Tate & Lyle, Roquette Frères, and Kerry Group expand supply networks across regional food systems. Growing integration in convenience foods and functional nutrition products strengthens demand. Expansion of retail modernization and e-commerce platforms improves ingredient accessibility.

Competitive Landscape

The global reduced starch syrup market reflects a moderately consolidated structure dominated by multinational ingredient manufacturers and regional starch processors. Leading companies such as Cargill, Archer Daniels Midland, Ingredion, Tate and Lyle, and Roquette maintain integrated supply chains across starch procurement, enzymatic processing, and global distribution networks. Market positioning depends on efficiency and compliance.

Competitive balance remains between global leaders and mid-scale producers across diversified food and pharmaceutical applications. Differentiation focuses on formulation expertise and production consistency. Innovation in functional syrups supports expansion in beverages, bakery, and nutraceutical products. Strategic alliances and capacity expansion initiatives strengthen supply resilience and improve access to high-demand industrial segments across global manufacturing ecosystems.

Key Industry Developments:

- In October 2025, Roquette introduced AMYSTA™ L 123, a label-friendly thermally soluble pea starch developed through a chemical-free process using heat treatment and spray drying to support clean-label food formulations and improved texture performance in processed food applications across global markets.

- In June 2025, Ingredion Incorporated partnered with Agrana to expand starch production capacity in Romania, which secures regional supply for European markets and accelerates delivery of customized reduced starch syrup variants to local manufacturers.

Companies Covered in Reduced Starch Syrup Market

- Cargill

- Archer Daniels Midland

- Ingredion

- Tate & Lyle

- Roquette

- Grain Processing Corporation

- AGRANA Beteiligungs-AG

- Tereos Group

- Nihon Shokuhin Kako

- Avebe

- Global Bio-Chem Technology Group

- BENEO GmbH

- Daesang Corporation

- Samyang Corporation

Frequently Asked Questions

The reduced starch syrup market is projected to reach US$3.5 billion in 2026.

Rising demand for functional sweetening agents, sugar reduction regulations, and expanding use in processed food, beverage, and pharmaceutical formulations drive the reduced starch syrup market.

The reduced starch syrup market is poised to witness a CAGR of 5.5% from 2026 to 2033.

Expansion of clean label formulations, enzymatic processing innovation, and growing adoption in nutraceutical and pharmaceutical applications create key opportunities in the reduced starch syrup market.

Some of the key market players include Cargill, Archer Daniels Midland, Ingredion, Tate and Lyle, and Roquette.