Industry: Chemicals and Materials

Published Date: September-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 188

Report ID: PMRREP34759

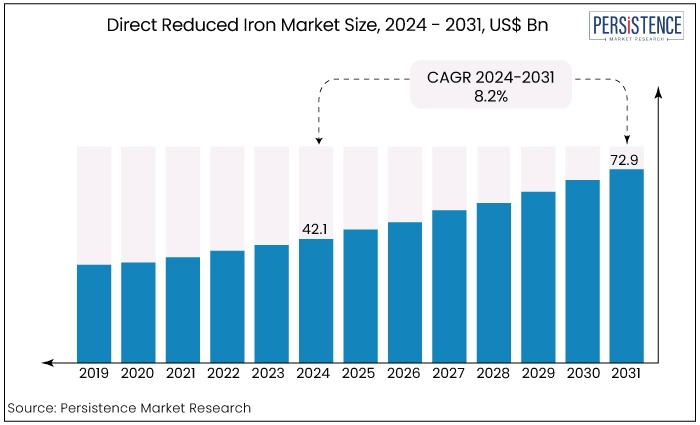

The direct reduced iron market is set to expand at a CAGR of 8.2% and expected to increase from US$42.1 Bn in 2024 to reach US$72.9 Bn by the end of 2031.

Key Highlights of the Market

|

Attributes |

Key Insights |

|

Market Size (2024E) |

US$42.1 Bn |

|

Projected Market Value (2031F) |

US$72.9 Bn |

|

Global Market Growth Rate (2024 to 2031) |

8.2% |

|

Historical Market Growth Rate (2019 to 2023) |

5.4% |

|

Revenue Share of Top Four Countries (2024E) |

~70% |

|

Country |

CAGR through 2031 |

|

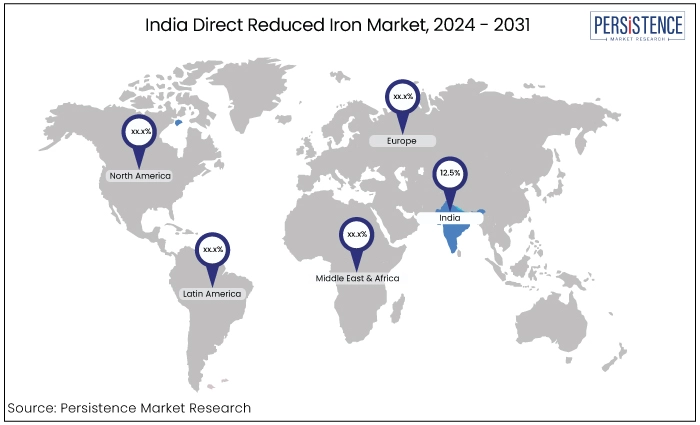

India |

12.5% |

India is the world’s largest DRI producing nation. The country holds about one-third share of the global DRI production. Increasing demand in steel industry, growing environmental concern and low energy efficiency are the leading drivers for the market to grow in Asia.

According to the data released from the World Steel Association, India along with China, together produced around 65% of the world total steel produced in 2023. The construction industry in India is anticipated to witness a significant growth rate during the forecast period.

The applications of steel from several end-use industries, such as aerospace and automotive, are expected to grow more. The government support for the expansion of the chemical industry in the country is further anticipated to drive the market growth.

|

Country |

CAGR through 2031 |

|

The United States |

13.5% |

The United States is the significantly growing market for DRI steel production. The country’s DRI production has grew from 2.99 million tons in 2017 to 5.01 million tons by 2021. The country is expected to double its production capacity by the end of forecast period.

The growing demand for green steel for sustainable manufacturing supported by the growth in consumption of DRI steel is bolstering the market in the country. According to PMR projection, the DRI market in the United States is projected to expand at a 13.5% CAGR during the forecast period.

|

Category |

Projected CAGR through 2031 |

|

Process - MIDREX |

10.7% |

The MIDREX process developed by Midrex Technologies, Inc., stands as a leading method for producing high-quality direct reduced iron, a pivotal raw material in steel manufacturing. Renowned for its efficiency and widespread adoption globally, the process applies reduction reaction on iron ore.

The MIDREX process takes place in reduction reactor facilitated by a certain gas typically a blend of natural gas and hydrogen. This reaction results in the conversion of iron oxide into iron metal. The reduction reaction is highly thermal sensitive. With controlled temperature between 800 °C to 1000 °C, process can be optimized to get maximum efficiency and secure desired metallurgical properties.

The MIDREX process also incorporates gas recycling, wherein the by-products generated during reduction notably carbon monoxide is recycled within the system, either as fuel or for further processing to extract valuable components like hydrogen.

Recognized for its environmental benefits compared to conventional steelmaking routes, MIDREX boasts lower greenhouse gas emissions and reduced energy consumption, positioning it as a sustainable choice for steel production.

|

Category |

Projected CAGR through 2031 |

|

Product Type - HDRI |

9.1% |

Hot direct iron holds a significant share in direct reduced iron market with 47% of market. HDRI is a variation of DRI produced using a similar process to hot briquetted iron, but with some differences in the final product form.

In HDRI process, iron ore is reduced to metallic iron using a reducing gas in a solid-state process. It is typically formed into compacted, not necessarily briquetted, pieces. This can affect the factors such as handling, transportation, and storage of the product.

HDRI is valued for its high iron content and low impurities, which make it desirable feedstock for steelmaking processes. They offer advantages over traditional iron production methods including higher quality steel output and contribute to environmental sustainability. Its growing demand in market is majorly due to its enhanced quality, ease in transportation and its low energy consumption. This is the leading cause the key market players are attracted towards HDRI.

|

Category |

Projected CAGR through 2031 |

|

Product Type - CDRI |

8.4% |

Cold direct reduced iron only holds around 19% share of the DRI market. CDRI is another variation of DRI with a different production process and final product characteristics compared to HDRI. In CDRI process, iron is also reduced to metallic iron using a reducing gas, but the reduction takes place at lower temperatures compared to the hot direct reduction process like HDRI.

Lower temperature allows for the production of iron in a solid-state process without the need for significant heating. This leads lower density and may have a different particle size distribution compared to HDRI.

CDRI still offers advantages over traditional iron production methods such as blast furnaces, including reduced energy consumptions and lower greenhouse gas emissions. It is used for steelmaking as a feedstock, especially in regions where natural gas is abundant and traditional iron ore sources are limited or expensive to transport. For instance,

Awareness regarding carbon emissions and taking a step ahead in achieving sustainable goals is the primary concern for manufacturing industries. The carbon emission from these industries prominently contribute to the greenhouse gas.

The focus on applying advanced processes to produce the steel is rising significantly. This trend required the countries like China, India and Japan, with around 65% of global production of steel to contribute to the direct reduced iron market.

The ongoing development activities, coupled with the government initiatives, are taking place globally. The European clean steel partnership was launched in 2021, in which the technology was developed in collaboration to reduce the CO2 emission by 85-90% from European steel industries.

The thriving demand for DRI across sectors like infrastructure, aerospace, and automotive is thrusting market expansion. This growth is strengthened by rising adoption of DRI in Electric Arc Furnaces, Blast Furnaces, and other applications globally.

According to the World Steel Association, global steel production reached 1,892 million tons in 2023 with carbon emissions of around 3,613.7 million tons. Thus, government authorities as well as manufacturing industries are increasingly prioritizing carbon emission reduction and sustainability goals. Notably, industrial carbon emissions are significant contributors to global greenhouse gas levels.

The direct reduced iron market was valued at US$32,515.9 Mn in 2019 experiencing a CAGR of 5.4% from 2019 to 2023. The impact of Covid-19 in various countries such as China, India, Japan, United States and Russia restricted the flow of resources and products. Consequently, the supply chain was drastically disrupted. Post pandemic, the government supported the business by reducing the restrictions.

The environmental concern over carbon emissions through steel making industries is boosting the demand for direct reduced iron as it reduced the carbon emission significantly. The direct reduced iron market is poised experience sustainable growth from 2024 to 2031 with a projected CAGR of 8.2%. The demand of direct reduced iron in steel making industry and the rise in steel market is boosting the direct reduced iron market.

Superiority of DRI Including Process Over Traditional Process

Blast furnace process also known as traditional process, and DRI applied electric arc furnace process (DRI-EAFs) are fundamental processes in steelmaking, each with distinct differences in operation and raw material usage.

Blast furnaces are colossal structures that utilize coke, iron ore, and limestone to produce molten iron through a chemical reduction process. These furnaces rely on injecting hot air or oxygen-enriched air to facilitate combustion, reaching temperatures exceeding 2,000°C. This process generally emits around 2.4 tons of CO2 per ton of crude steel produced.

DRI-EAFs are smaller and utilize electricity as the primary heat source to melt direct reduced iron (DRI) into molten steel. This electric arc process, generated between graphite electrodes and the metallic charge, enables EAFs to melt steel efficiently. The amount of CO2 emitted from this process is around 1.3 tons per ton of crude steel produced.

The choice between blast furnaces and EAFs depends on various factors, including production volume, raw material availability, energy costs, and environmental considerations. Blast furnaces, although energy-intensive and reliant on coke combustion, are advantageous for high-volume steel production and utilize raw materials such as iron ore efficiently.

Growth in Steel Industry

The global steel market with a value of US$984.3 Bn in 2024 and projected to expand at a CAGR of 3.8% by 2031 plays a critical role in numerous manufacturing and construction sectors worldwide. As demand surges, the production of steel, whether from scrap or new raw materials, continues to rise.

The utilization of DRI in EAFs holds significant importance within the steelmaking sector. It exhibits a consistent quality and ow sulphur and phosphorus content along with insignificant impurities. It also offers steel manufacturers greater raw material flexibility, reducing reliance on traditional materials like iron ore and coke.

Incorporating DRI enhances supply chain resilience, fostering adaptability to market fluctuations and evolving industry dynamics. Furthermore, adopting DRI in EAF operations provides compelling environmental and economic benefits.

DRI production typically consumes less energy compared to conventional ironmaking processes, aligning with sustainability goals and reducing greenhouse gas emissions. This shift not only improves operational efficiency and lowers production costs but also enhances the overall quality of steel output.

Higher and Volatile Operating Cost of DRI Plants

Establishing DRI plants presents a formidable financial hurdle, primarily due to the substantial capital investment required. This investment encompasses various expenses including implementation of cutting-edge technologies, land acquisition, procurement of equipment, and development of infrastructure. Such significant upfront costs act as a deterrent for potential new entrants, limiting market accessibility and competition within the DRI sector.

The operating costs of DRI plants are susceptible to volatility, primarily driven by fluctuations in raw material prices. Notably, the prices of essential inputs such as natural gas and iron ore can fluctuate considerably, directly impacting the profitability of DRI producers. For instance, sudden spikes in natural gas prices can inflate production expenses, consequently squeezing profit margins.

Unpredictable shifts in iron ore prices can disrupt cost projections and profitability forecasts, posing additional challenges for DRI plant operators in managing their financial performance amidst market uncertainties.

Technological Advancements in the DRI Process

Recent studies have explored innovative and environmentally sustainable methods for producing DRI. Utilizing H2 gas or natural gas as a reducing agent in DRI production helps conserve energy and minimize carbon emissions.

The production of green H2 involves electrolyzing water using renewable energy sources. The adoption of H2 gas is increasingly advocated in the market to enhance energy efficiency.Key industry players like Kobe Steel Ltd., ArcelorMittal, and Voestalpine AG are actively investing in DRI plants that rely on green H2. Government initiatives are also facilitating the transition by reducing regulatory burdens for industries establishing green H2-based DRI facilities. For example,

The key players are focusing more on developing countries to keep up with the growing demand for DRI. This strategic realignment reflects a concerted effort to increase production capabilities to effectively trade the escalating requirements of these burgeoning markets.

Companies are teaming up with each other to find new ways to make money by working together to take advantage of their different strengths and skills. For instance,

Recent Developments in the Direct Reduced Iron Market

On November 2023, JSPL has teamed up with Tenova to launch hydrogen based ENERGIRON technology in DRI plant in Oman which will be operational from 2026.

On August 9, 2023, Midrex Technologies and Primetals Technologies were selected by Blastr Green Steel to provide key equipment for a new direct reduction iron (DRI) plant. The plant, which will be situated in Finland, will utilize hydrogen-based technology to produce low-carbon DRI, with operations expected to begin in 2026.

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Countries Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Process Type

By Product Type

By Region

To know more about delivery timeline for this report Contact Sales

The market is anticipated to secure a CAGR of 8.2% during the forecast period.

The market is estimated to be valued at US$42.1 Bn in 2024.

MIDREX process to stand out in the market exhibiting 10.7% CAGR through 2031.

A key opportunity lies in the technological advancements in the DRI process.

Some of the prominent players in the market are MIDREX, ArcelorMIttal SA, and Kobe Steel Ltd.