- Retail

- Processed Potato Products Market

Processed Potato Products Market Size, Share, and Growth Forecast 2026 - 2033

Processed Potato Products Market by Product Type (Potato Chips, Frozen Potato, Dehydrated Potato, Canned Potatoes, Others), Application (Ready to Cook Products, Snacks, Others), Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Wholesale, HoReCa Supply Chains), and Regional Analysis, 2026 - 2033

Processed Potato Products Market Size and Trend Analysis

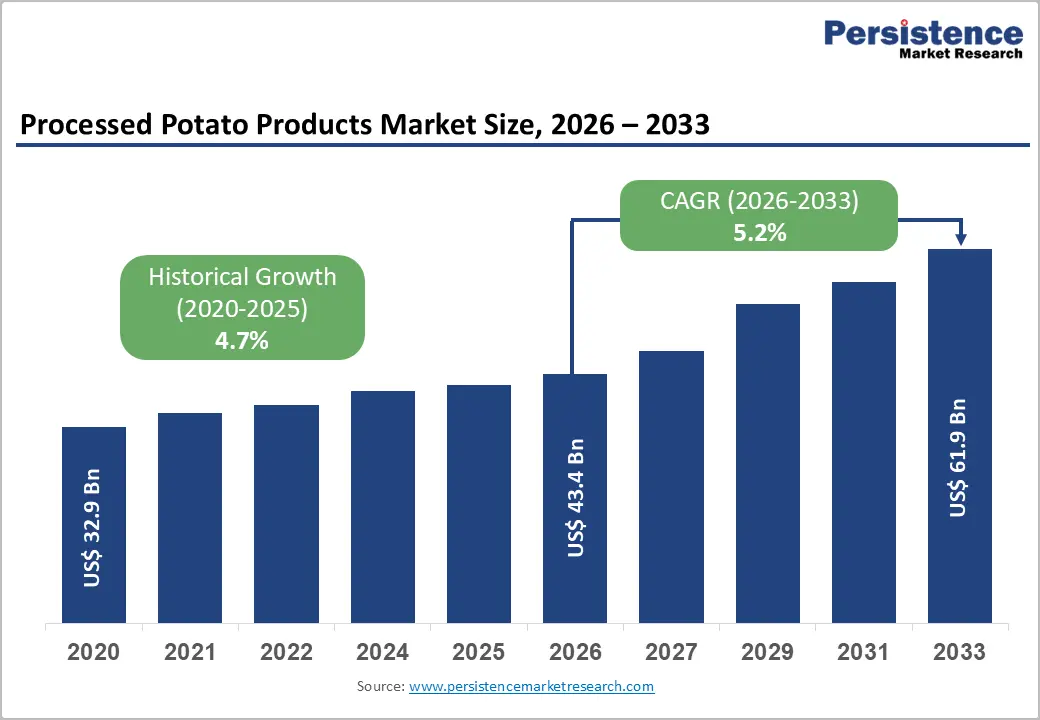

The global processed potato products market size is expected to be valued at US$ 43.4 billion in 2026 and projected to reach US$ 61.9 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033. Growth is driven by rising demand for convenient, ready-to-eat foods and expanding quick-service restaurant (QSR) networks worldwide, especially in emerging economies.

Strong global potato production exceeding 374 million metric tonnes ensures a steady raw material supply for processors. Increasing urbanization and shifting dietary patterns toward packaged snacks further support consumption growth. Expanding retail penetration and foodservice modernization are also reinforcing steady adoption across both developed and developing regions, sustaining long-term market momentum.

Key Industry Highlights:

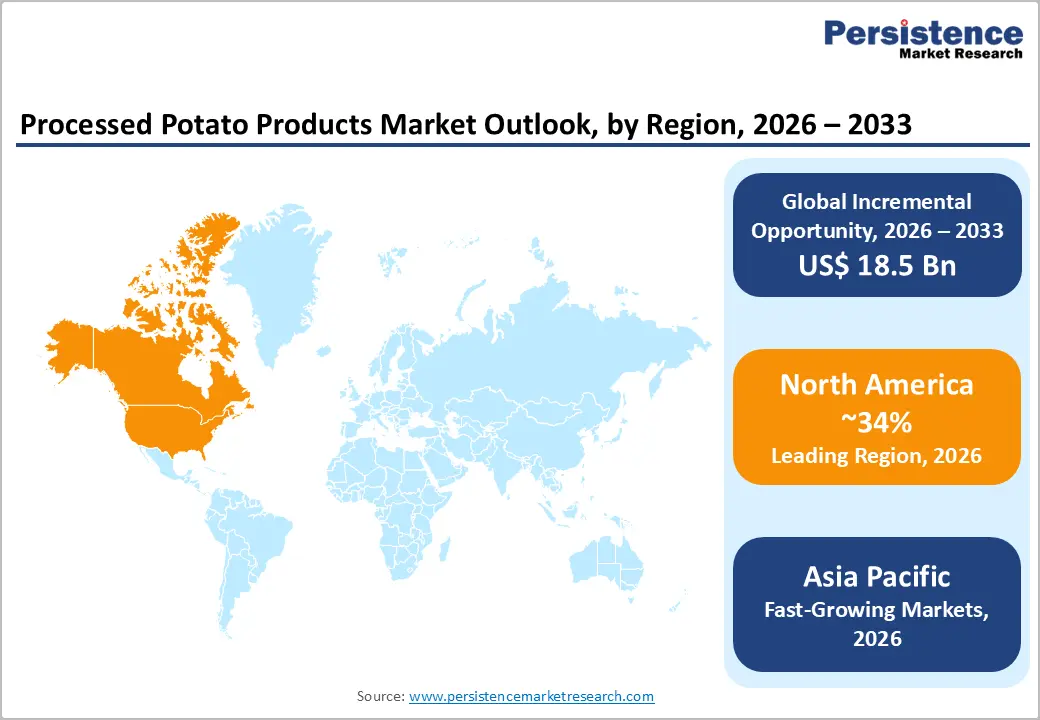

- Leading Region: North America holds the largest share of approximately 34% of the global Processed Potato Products market in 2025, supported by its deeply established snacking culture and world-leading QSR infrastructure.

- Fastest Growing Region: Asia Pacific is projected to be the fastest-growing regional market at a CAGR of 6.8% from 2025 to 2032, driven by urbanization, rising disposable incomes, and expanding modern retail.

- Dominant Segment: The Snacks application segment leads with approximately 52% market share in 2025, underpinned by global grazing eating trends and high snack food frequency.

- Fastest Growing Segment: Online Retail is the fastest-growing distribution channel, driven by rapid e-commerce penetration, subscription grocery models, and social commerce-driven product discovery.

- Key Opportunity: The growing consumer demand for healthier, clean-label potato snacks present a high-value innovation opportunity. Better-for-you variants can command 30-50% price premiums and are among the fastest-growing sub-segments, offering manufacturers differentiated positioning in saturated snack food markets.

Market Dynamics

Drivers - Rising QSR Expansion and Convenience Food Consumption Demand

The rapid expansion of quick-service restaurants (QSRs) and fast-casual dining outlets is a major driver for processed potato products. Strong foodservice growth, particularly in the U.S. where fast-food sales exceeded US$ 350 billion in 2023, is increasing demand for frozen formats like fries and hash browns. Global chains such as McDonald’s, Yum! Brands are aggressively expanding in emerging cities.

Foodservice operators are increasingly prioritizing standardized, pre-processed potato products to reduce preparation time and ensure consistency in taste and quality. Industry associations highlight rising B2B procurement of frozen potatoes, reinforcing stable institutional demand. This shift toward efficiency-driven kitchen operations continues to strengthen long-term consumption across global foodservice channels. These procurement trends are also encouraging long-term supply contracts between processors and global foodservice brands.

Urbanization and Evolving Dietary Patterns in Emerging Economies

Rapid urbanization in Asia Pacific, Africa, and Latin America is significantly reshaping food consumption behavior toward packaged and convenience-based products. The World Bank projects strong urban population growth in Sub-Saharan Africa, expanding the consumer base for processed snacks. Rising exposure to Western dietary habits is further accelerating demand for potato-based snack products across developing regions.

In India, annual snack consumption is growing at 12-15% with potato chips and related products holding nearly 45% share of organized snacks. Increasing disposable incomes, retail expansion, and aggressive FMCG branding are further strengthening penetration. These structural changes are making processed potato products a mainstream dietary choice in emerging economies.

Market Restraints

Volatile Potato Supply and Rising Production Cost Pressures

Potato cultivation is highly exposed to climatic variability, pest attacks, and irregular water availability, resulting in fluctuating yields and unstable farm-gate pricing. According to the USDA, drought conditions in key producing regions have previously pushed potato input costs up by 20-30%, creating significant cost unpredictability for processors across global supply chains and reducing profit stability. These fluctuations force manufacturers to either absorb margin pressure or increase product prices, which can negatively impact demand consistency.

Additionally, geopolitical tensions, energy inflation, and cold-chain logistics costs are further increasing expenses, particularly for frozen potato products that require continuous temperature-controlled storage and transportation throughout global distribution networks.

Rising Health Awareness and Regulatory Food Restrictions Impacting Demand

Growing awareness of obesity, diabetes, and cardiovascular diseases is shifting consumers away from high-fat and high-sodium processed potato products. The World Health Organization recommends limiting sodium intake to under 2,000 mg per day, while many snack products contribute significant sodium levels per serving, raising concerns among health-conscious populations globally.

At the same time, regulatory actions such as EU front-of-pack labeling requirements and sugar or fat taxes in countries such as Mexico and Hungary are increasing compliance pressure on manufacturers. These policies are driving reformulation efforts while discouraging consumption of traditional fried potato snacks, ultimately restraining growth in certain mature and health-sensitive markets.

Opportunities - Innovation in Better-for-You and Clean-Label Potato Snack Formats

The rising global preference for health-focused snacking is creating strong opportunities for processed potato manufacturers to expand into better-for-you (BFY) product categories. Clean-label potato chips with fewer ingredients, baked or air-popped formats, reduced sodium content, and fiber-fortified variants are gaining traction among health-conscious consumers. The Specialty Food Association identified BFY snacking as a top growth category in 2024.

Manufacturers introducing premium variants such as avocado-oil fried, non-GMO, and organic-certified potato snacks are achieving higher pricing potential, often 30-50% above standard products. Millennials and Gen Z consumers are driving this shift toward “permissible indulgence,” supported by increasing retail shelf space for healthier snack alternatives. Nielsen IQ reports strong double-digit growth in this segment across major global markets.

Expansion of Online Retail and Direct-to-Consumer (DTC) Distribution Channels

The rapid expansion of e-commerce and online grocery platforms is creating significant growth opportunities for processed potato product brands worldwide. According to the International Trade Centre, online food retail is expected to exceed 15% of total grocery sales by 2028, compared to about 8% in 2022. Platforms such as Amazon, JD.com, and regional delivery apps are enabling wider consumer access.

Direct-to-consumer (DTC) models allow brands to bypass traditional retail margins, reduce listing fees, and build stronger customer relationships. Companies can also leverage consumer data for personalization and subscription-based sales models. Additionally, social commerce through platforms like Instagram and TikTok is enabling rapid product discovery, allowing agile snack brands to achieve faster market penetration and viral growth.

Category-wise Analysis

Product Type Insights

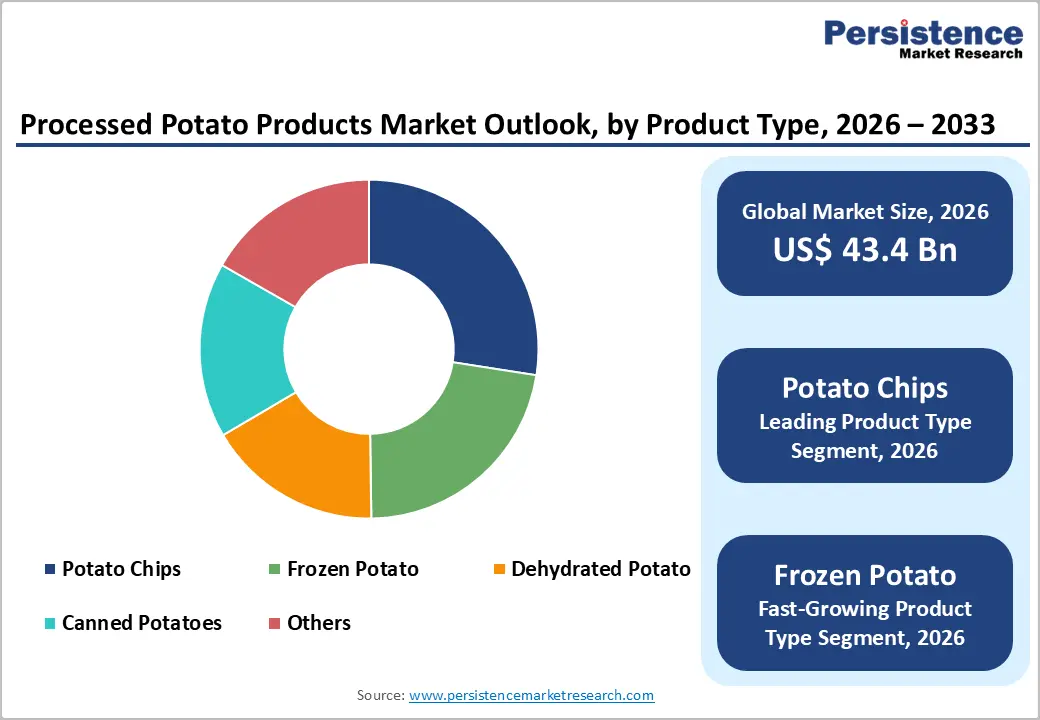

Potato chips dominate the processed potato products market by product type, holding approximately 38% of total revenue in 2025. Their leadership is supported by strong consumer familiarity, wide availability across retail formats, and extensive flavor innovation. In the U.S., the Snack Food Association highlights chips as the largest snack category, generating over US$ 9 billion in annual retail sales.

This dominance is further strengthened by continuous product innovation and premiumization trends. Manufacturers are introducing kettle-cooked, ridged, and globally inspired flavors to attract diverse consumer groups. Strong branding from global players such as Lay’s and Frito-Lay ensures high repeat purchase rates, while aggressive retail penetration across both developed and emerging economies sustains category leadership.

Application Insights

The snacks application segment leads the processed potato products market, accounting for approximately 52% market share in 2025. This dominance is driven by rising snacking frequency, smaller household sizes, and the growing preference for convenient on-the-go food options. Salty snacks remain the most consumed category, strongly supported by potato-based formats like chips and sticks.

The fastest-growing segment is ready-to-cook and convenience-focused snack consumption, driven by urban lifestyles and changing eating patterns. Increasing demand for portion-controlled packs, office snacking, and children-oriented snack products is expanding adoption. Growing retail availability and convenience-oriented product formats are further accelerating consumption across both developed and emerging markets globally.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution channel segment with approximately 43% market share in 2025. Their leadership is supported by wide product assortments, strong promotional activity, and high consumer footfall. Global retailers such as Walmart, Carrefour, Tesco, and Kroger allocate significant shelf space to potato-based snacks and frozen products, ensuring strong volume sales.

The fastest-growing channel is online retail, driven by increasing e-commerce penetration and shifting consumer buying behavior. Digital grocery platforms and quick-commerce services are expanding accessibility, offering convenience, discounts, and home delivery. Rising smartphone usage and changing shopping preferences are accelerating online adoption, making it a key growth avenue for processed potato product manufacturers worldwide.

Regional Insights

North America Processed Potato Products Market Trends and Insights

North America leads the global processed potato products market with an estimated 34% market share in 2025, underpinned by the region's deeply entrenched snacking culture, highly developed cold-chain infrastructure, and the commanding presence of multinational food manufacturers. The United States and Canada collectively represent the most mature markets, with per capita consumption of potato chips and frozen potato products among the highest globally. Innovation in premium, organic, and BFY potato snack formats is a defining trend, as leading brands aggressively reformulate products to align with clean-label consumer expectations.

- U.S. Processed Potato Products Market Size

The United States accounts for approximately 28% of global processed potato products revenue in 2025, translating to an estimated market value of around US$ 11.5 billion. Robust QSR demand for frozen french fries, the world's largest potato chip retail market, and strong club-store and convenience retail formats collectively underpin this outsized national share.

Europe Processed Potato Products Market Trends and Insights

Europe represents the second-largest regional market for Processed Potato Products, accounting for approximately 27% of global revenue in 2025. The region benefits from a long-established potato consumption culture across Germany, the United Kingdom, France, Belgium, and the Netherlands. EU regulatory frameworks on food labeling and reduced-fat products are steering manufacturers toward healthier formulations, while private-label potato products are capturing a growing share in cost-conscious consumer segments amid inflationary pressures.

- Germany Processed Potato Products Market Size

Germany is the leading national market for processed potato products within Europe, holding approximately 22% of the regional market share in 2025. Germany's status as one of the world's top potato-producing nations, combined with advanced food processing capabilities and high retail snack penetration, reinforces its market leadership position in frozen and dehydrated potato products.

- U.K. Processed Potato Products Market Size

The United Kingdom accounts for approximately 18% of European Processed Potato Products revenue in 2025. The UK's strong crisps (potato chips) consumption heritage, with "crisps" being a staple British snack combined with a vibrant foodservice sector and growing demand for premium flavored variants, supports a resilient and innovation-driven market.

- France Processed Potato Products Market Size

France holds approximately 14% of the market revenue in 2025 in Europe. Growing QSR penetration, the popularity of aperitif snacking culture, and rising demand for premium and gourmet potato chip varieties are key growth enablers. French retailers are also increasingly featuring organic and regionally sourced potato snack lines to appeal to discerning consumers.

Asia Pacific Processed Potato Products Market Trends and Insights

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of approximately 6.8% from 2025 to 2032. Rising disposable incomes, rapid urbanization, and the explosive growth of organized retail and e-commerce platforms are the primary growth engines across India, China, Japan, and Southeast Asia. China represents the largest national market in the region, with PepsiCo and local brands such as Oishi (Liwayway Holdings) aggressively competing for market share through both modern retail channels and booming social commerce platforms.

- India Processed Potato Products Market Size

India is among the most promising individual country markets within Asia Pacific, with an estimated market share of approximately 12% of the regional value in 2025. Rapid expansion of organized snack food retail, a youthful population base exceeding 600 million consumers below age 25, and aggressive product launches by PepsiCo India and Haldiram's are driving robust double-digit demand growth for potato chips and snacks.

- Japan Processed Potato Products Market Size

Japan holds approximately 15% of the Asia Pacific processed potato products market in 2025. The Japanese market is characterized by high consumer preference for premium, uniquely flavored, and limited-edition potato chip products. Domestic producers such as Calbee, Inc. dominate with sophisticated product portfolios, while convenience store (konbini) channel penetration remains a significant demand driver.

- Southeast Asia Processed Potato Products Market Size

Southeast Asia accounts for an estimated 10% of Asia Pacific market revenue in 2025. Markets such as Indonesia, Vietnam, Thailand, and the Philippines are experiencing rapid snack food market expansion driven by a growing middle class, urbanization, and the proliferation of modern minimarket chains. Local flavor innovations and affordable price points are key competitive drivers for brand penetration in these emerging economies.

Competitive Landscape

Multinational food companies holding significant influence alongside a wide base of regional and local manufacturers. Competition is primarily shaped by scale advantages in production, strong distribution networks, and established brand presence across retail and foodservice channels. Product diversification and global supply chain integration remain key strengths for leading participants.

Market players are actively focusing on expanding processing capacities, strengthening procurement networks, and enhancing operational efficiency. Strategic investments in healthier product innovation, clean-label offerings, and sustainability initiatives are becoming central to long-term positioning. At the same time, private-label growth and evolving consumer preferences are intensifying competitive pressure across both premium and value segments globally.

Key Developments:

- In January 2025, McCain Foods Limited announced a CAD 600 million investment to expand its potato processing facility in Alberta, Canada, increasing frozen french fry production capacity to meet growing global foodservice demand.

- In March 2024, Lamb Weston Holdings, Inc. completed its acquisition of the remaining stake in its joint venture with Meijer, consolidating its European frozen potato operations and strengthening supply chain capabilities across the EU market.

- In September 2024, PepsiCo Inc. launched an expanded line of Lay's reduced-fat and baked potato chip varieties across 15 markets in the Asia Pacific, targeting health-conscious millennial consumers and addressing evolving regulatory requirements on high-fat snack labeling.

Companies Covered in Processed Potato Products Market

- McCain Foods Limited

- Lamb Weston Holdings, Inc.

- J.R. Simplot Company

- PepsiCo, Inc. (Frito-Lay)

- The Kraft Heinz Company

- Aviko B.V. (Royal Cosun)

- Farm Frites International B.V.

- Agristo NV

- Intersnack Group GmbH & Co. KG

- Cavendish Farms Corporation

- Emsland Group

- Idahoan Foods, LLC

- Calbee, Inc.

- Conagra Brands, Inc.

- Kellogg Company

Frequently Asked Questions

The global Processed Potato Products market is valued at US$ 43.4 billion in 2026 and projected to reach US$ 61.9 billion by 2033.

The primary drivers include the rapid global expansion of quick-service restaurants (QSRs), rising urbanization and adoption of convenience food habits in emerging economies, growing per capita snack food consumption.

North America leads the global Processed Potato Products market with approximately 34% market share in 2025.

The most significant near-term opportunity lies in better-for-you (BFY) and clean-label potato snack innovation.

The leading companies operating in the global Processed Potato Products market include PepsiCo, Inc. (Frito-Lay), McCain Foods Limited, Lamb Weston Holdings, Inc., Intersnack Group GmbH & Co. KG, Calbee, Inc., and Aviko B.V. (Royal Cosun).