Industry: Energy & Utilities

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Report Type: Ongoing

Report ID: PMRREP34656

The global pipe coating market is expected to reach a value of US$9.1 Bn by the end of 2024. It is projected to grow at a CAGR of 4.8% from 2024 to 2031, reaching a market value of US$12.6 Bn by 2031.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Market Size (2024E) |

US$9.1 Bn |

|

Projected Market Value (2031F) |

US$12.6 Bn |

|

Forecast Growth Rate (CAGR 2024 to 2031) |

4.8% |

|

Historical Growth Rate (CAGR 2019 to 2023) |

4.2% |

The pipe coating market is propelled by several key factors driving demand worldwide. Growing investments in oil and gas infrastructure, coupled with increasing pipeline construction activities, underscore the need for robust coatings to protect against corrosion and enhance durability.

Stringent regulations mandating pipeline safety and environmental protection contribute to market growth, as companies seek compliant solutions.

Technological advancements in coating formulations and application methods further stimulate market expansion, offering opportunities for innovative products that meet evolving industry standards.

Market dynamics collectively shape a competitive landscape poised for continuous advancement in the pipe coating sector.

Sustainable and high-performance coatings mark the key market trends. Companies like PPG, AkzoNobel, Sherwin-Williams, Tenaris, and Hempel pioneer innovation.

Continuous innovation in coating formulations and application methods drive the market ahead. There is a noticeable shift towards eco-friendly products, with a focus on reducing environmental impact and meeting stringent regulatory standards.

Advances in erosion-resistant and anti-corrosion technologies like Sherwin-Williams Pipeclad Frac-Shun ERC, and Tenaris have expanded capabilities through acquisitions, highlighting the market's emphasis on durability, and operational efficiency.

Strategic partnerships and acquisitions, like Tenaris integration of Shawcor Coating Solutions, and Hempel collaboration with CVC Funds indicate growing emphasis on expanding capabilities. This is accelerating market growth through investments in sustainable technologies.

The market has experienced robust growth, driven historically by several key factors. Industries such as water management, oil and gas, and chemical processing have been primary users of pipe coatings to mitigate corrosion and extend the operational lifespan of pipelines.

The increasing need for infrastructure development, especially in emerging economies, has significantly contributed to market expansion. Stringent regulatory standards mandating corrosion protection to ensure pipeline safety and environmental compliance have been pivotal in shaping market dynamics.

The market is poised for continued growth driven by several compelling factors. Ongoing infrastructure projects globally, particularly in energy transportation and urban development sectors, are expected to escalate the demand for coated pipes.

These projects necessitate reliable corrosion protection solutions to ensure operational efficiency and longevity of pipelines under diverse environmental conditions.

Advancements in coating technologies that offer enhanced durability, flexibility, and resistance to abrasion and chemical corrosion are anticipated to fuel market growth.

Oil and Gas Industry Dynamics

The oil and gas industry is a significant driver for the market due to escalating global oil demand, projected to rise by 2.3 mb/d to 101.7 mb/d in 2023, despite macroeconomic challenges and slowing growth in major economies.

The remarkable surge in US oil production, which exceeded 20 mb/d, along with record outputs from Brazil and Guyana, and increased Iranian flows, highlight the pressing need for reliable pipeline infrastructure.

This growth is expected to continue into 2024 with an additional 1.2 mb/d in non-OPEC+ production.

As fluctuating crude prices and the recent dip in Russian crude exports below the $60/bbl price cap illustrate, efficient pipeline management is critical for minimizing revenue losses and operational disruptions.

The declining global refinery margins and lower crude and product inventories further emphasize the importance of advanced pipe coatings to maintain pipeline integrity, reduce maintenance costs, and adapt to varying economic and production conditions.

These dynamics underscore the growing demand for durable, corrosion-resistant coatings that ensure the efficiency and longevity of pipelines amidst increasing global oil supply and evolving market challenges.

Expansion of Agricultural Irrigation and Drainage Systems

The agricultural sector is contributing to the growth of the pipe coating market through the development and enhancement of irrigation and drainage systems.

As modern agriculture increasingly relies on efficient water management to optimize crop yields and conserve water resources, coated pipes play a vital role in ensuring the durability and reliability of irrigation infrastructure.

Coatings protect pipes from corrosion caused by fertilizers and other agricultural chemicals, extending the lifespan of irrigation systems.

The trend towards precision agriculture and the need for sustainable water usage practices are driving investments in high-quality coatings, which help minimize maintenance costs and improve the efficiency of agricultural water distribution networks.

Challenges in Harsh Terrains, and Extreme Weather Conditions

Constructing pipelines in rocky soil, mountains, rivers, and roads with challenging trench materials often leads to complications in remote areas with minimal infrastructure. These regions frequently experience severe climates, making the application and efficacy of coatings problematic.

Traditional methods like sand bedding & padding become impractical in frozen or steep environments, creating issues for both corrosion and mechanical protection. These factors challenge coating providers, affecting the pipeline integrity and market expansion.

High Installation and Maintenance Costs

The high costs associated with the installation and maintenance of advanced pipe coatings pose a notable challenge to market growth.

Deploying these coatings, especially in remote or environmentally challenging areas, involves substantial expenses related to labor, materials, and logistical complexities.

Maintenance costs are also elevated in harsh environments where coatings are subjected to extreme wear and tear. These financial burdens can deter pipeline operators from investing in new coating technologies and limit the adoption of advanced solutions, thereby restraining the market expansion.

Advancement in Eco-Friendly Coating Technologies

The rising emphasis on environmental sustainability and regulatory compliance offers a promising opportunity for the pipe coating through the development and adoption of eco-friendly coating technologies.

There is a growing demand for coatings that minimize environmental impact by reducing volatile organic compounds (VOCs), hazardous air pollutants (HAPs), and overall carbon footprint during manufacturing and application.

Innovations in bio-based, waterborne, and solvent-free coatings are gaining traction as industries seek to align with stricter environmental regulations and sustainability goals.

By investing in research and development of green coating technologies, manufacturers can differentiate themselves in the market, meet the evolving preferences of environmentally conscious consumers, and capture a significant share in the sustainable coatings segment.

Mobile Coating Technology

The introduction of mobile coating technology presents a promising opportunity for the pipe coating market.

By offering on-site coating services, this innovative approach streamlines project execution, significantly cutting down transportation and handling costs, and reducing the time required for coating applications.

Mobile coating units can provide external anti-corrosion protection, mechanical shielding, thermal insulation, and buoyancy control directly at the project site, minimizing the risks and repair costs associated with damage during transit.

These mobile facilities are easy to set up and can match the production capacity of traditional fixed plants.

Furthermore, companies can employ and train local technicians to operate these units, ensuring productivity and quality are maintained at levels comparable to fixed installations, all while enhancing cost-effectiveness and operational efficiency for pipeline constructors.

|

Category |

Projected CAGR through 2031 |

|

Product Category - Thermoplastic Polymer Coatings |

4.7% |

|

End-user - Oil & Gas |

5.1% |

Thermoplastic Polymer Coatings Segment to Account for the Significant Share

The Thermoplastic Polymer segment accounted for the significant market share of around 43.0% in 2023 and is likely to maintain its dominance during in the forthcoming years recording a CAGR of 4.7%.

These coatings, including polyethylene (PE), polypropylene (PP), and polyvinyl chloride (PVC), protect pipelines from harsh environmental conditions, preventing corrosive damage and significantly extending the life of pipeline systems.

The flexibility and impact resistance ensure that pipelines can withstand mechanical stress, thermal expansion, and chemical exposure without degradation, making them indispensable in industries such as oil and gas, chemical processing, and water distribution.

Thermoplastic polymer coatings are versatile and easy to apply, accommodating various pipeline materials and configurations, whether for new installations or rehabilitation projects.

The application methods, such as fusion bonding or extrusion, allow for efficient and consistent coating processes, reducing both installation time and costs.

This adaptability and cost-effectiveness make thermoplastic polymer coatings a preferred solution for protecting pipelines in diverse and demanding environments, driving their growing adoption and market demand.

Chemical Processing Industry to Grow Notably for Pipe Coating

In the chemical processing industry, pipelines are subjected to aggressive chemicals, high temperatures, and varying pressures, making them vulnerable to corrosion and degradation.

Pipe coatings tailored for chemical processing environments provide critical protection against these harsh conditions, preserving the integrity and performance of the pipelines.

As the chemical industry expands to meet the rising demand for various chemicals and intermediates, the need for advanced coatings to safeguard pipelines and reduce maintenance costs is growing.

The growing focus of this category on enhancing operational efficiency and ensuring safe chemical transport drives the adoption of durable and chemically resistant coating solutions.

|

Region |

CAGR through 2034 |

|

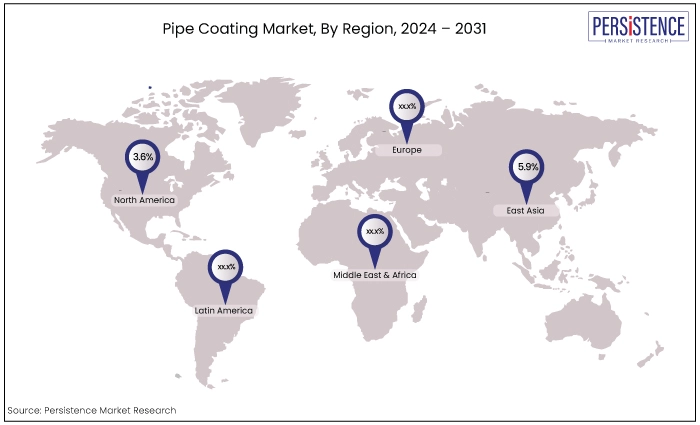

North America |

3.6% |

|

East Asia |

5.9% |

North America’s Significant Market Share Prevails

North America is the most significant shareholder in the global market and is expected to grow at a CAGR of 3.6% during the forecast period. In 2023, the US set a record by averaging 12.9 million barrels per day (b/d) of crude oil production, peaking at 13.3 million b/d in December.

This unprecedented production level underscores the region's substantial demand for pipeline infrastructure, necessitating advanced coatings to ensure durability and operational efficiency.

Geopolitically, North Americas influence is significant, with factors like OPEC+ output cuts affecting global oil prices, pushing Brent oil prices above US$90/bbl. These dynamics highlight the region's impact on international energy markets and reinforce the critical need for resilient pipeline coatings.

Ongoing investments in energy infrastructure across North America support pipeline expansion and maintenance initiatives, further driving demand for high-performance coatings.

The agricultural sector's substantial contribution, with related industries adding approximately $1.530 trillion to the U.S. GDP in 2023, also fuels demand for coatings that protect irrigation and water distribution pipelines.

These factors collectively cement North America's leading position in the pipe coating market, supported by robust production figures, geopolitical influence, infrastructure investments, and contributions from key economic sectors.

East Asia to Exhibit a Notable CAGR in Global Market

East Asia Market is projected to secure a CAGR of 5.9% in the forecast period from 2024 to 2031. East Asia, particularly led by China, plays a pivotal role in driving the global pipe coating market due to several key factors.

China’s record-high crude oil processing capacity in 2023, averaging 14.8 million barrels per day (b/d), underscores the regions robust demand for pipeline infrastructure coated to enhance durability and efficiency.

The substantial growth in refinery capacity, aimed at meeting transportation fuel needs and producing petrochemical feedstocks like naphtha and LPG, further boosts demand for advanced pipe coatings.

China strategic investments in infrastructure projects, including those in energy and petrochemical sectors, continuously propel the market for high-performance coatings.

As the region continues to modernize and expand its agricultural production capacity, driven by technological advancements and increasing consumption trends, the need for reliable pipeline coatings to support irrigation and distribution networks also grows.

The market dynamics highlight East Asia's significant contribution to the global pipe coating market, driven by robust industrialization, energy security measures, and infrastructure development initiatives.

The market is highly competitive, driven by innovation in sustainable and durable technologies.

Key players like PPG Industries, Hempel, and Sherwin-Williams are focusing on eco-friendly solutions, with PPG recognized for its sustainable products and Hempel partnering with CVC Funds to boost growth in sustainable technologies. Sherwin-Williams introduced the Pipeclad Frac-Shun ERC, an erosion-resistant coating enhancing pipeline durability.

Companies are investing in advanced coatings to reduce environmental impact and improve performance, positioning themselves strongly in sectors like oil & gas, marine, and industrial applications. Strategic partnerships and technological advancements are pivotal in maintaining a competitive edge.

May 2024

Sherwin-Williams Protective & Marine introduced the Pipeclad Frac-Shun ERC, a novel coating system designed to resist erosion inside pipes near fracking wellheads. This patent-pending erosion-resistant coating (ERC) technology significantly reduces maintenance downtime and boosts drilling productivity by protecting pipe interiors from the abrasive action of fast-moving grit. The durable powder coating effectively prevents metal loss, minimizing leaks and extending the lifespan of steel pipes.

February 2024

PPG was recognized as the leading paints, coatings, and specialty materials manufacturer on the 2024 Corporate Knights Clean200 list. This accolade highlights PPG's achievement of deriving 19% of its 2022 sales from sustainable products, as certified by third parties. Out of roughly 8,000 evaluated global firms, PPG secured the 161st position for its sustainable revenue.

November 2023

Tenaris completed the acquisition of Mattr’s pipe coating business unit (Shawcor) for $182.6 million, inclusive of estimated working capital and $16.9 million in cash. Announced on August 14, 2023, and cleared by regulators in Mexico and Norway, this deal adds nine plants across various countries and several mobile concrete plants to Tenaris's portfolio. The acquisition enhances Tenaris’s capabilities in end-to-end concrete weight, anti-corrosion, and flow assurance coating solutions for pipelines, with Tenaris committing to integrate these facilities while maintaining Shawcor's existing commitments.

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value Tons for Volume |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Type

By Form

By End Use

By Region

To know more about delivery timeline for this report Contact Sales

Surging demand for pipe coatings is driven by increasing activities in the oil and gas industry, necessitating robust coatings to ensure pipeline integrity and longevity amidst expanding infrastructure.

Some of the key players operating in the market are PPG Industries, AKZO Nobel N.V., The Sherwin Willim Company, 3M, and Shawcor.

Thermoplastic Polymer segment recorded the significant market share.

The rising emphasis on environmental sustainability and regulatory compliance offers a promising opportunity for the pipe coating market.

North America to account for the significant share of the market.