- Beverages

- Performance Beverages Market

Performance Beverages Market Size, Share, and Growth Forecast, 2026 - 2033

Performance Beverages Market by Product Type (Energy Drinks, Sports Drinks, Protein Drinks, Hydration Drinks), Ingredient Type (Vitamins & Minerals, Amino Acids, Botanicals, Caffeine), End-user (Athletes, Others), and Regional Analysis for 2026 - 2033

Performance Beverages Market Size and Trends Analysis

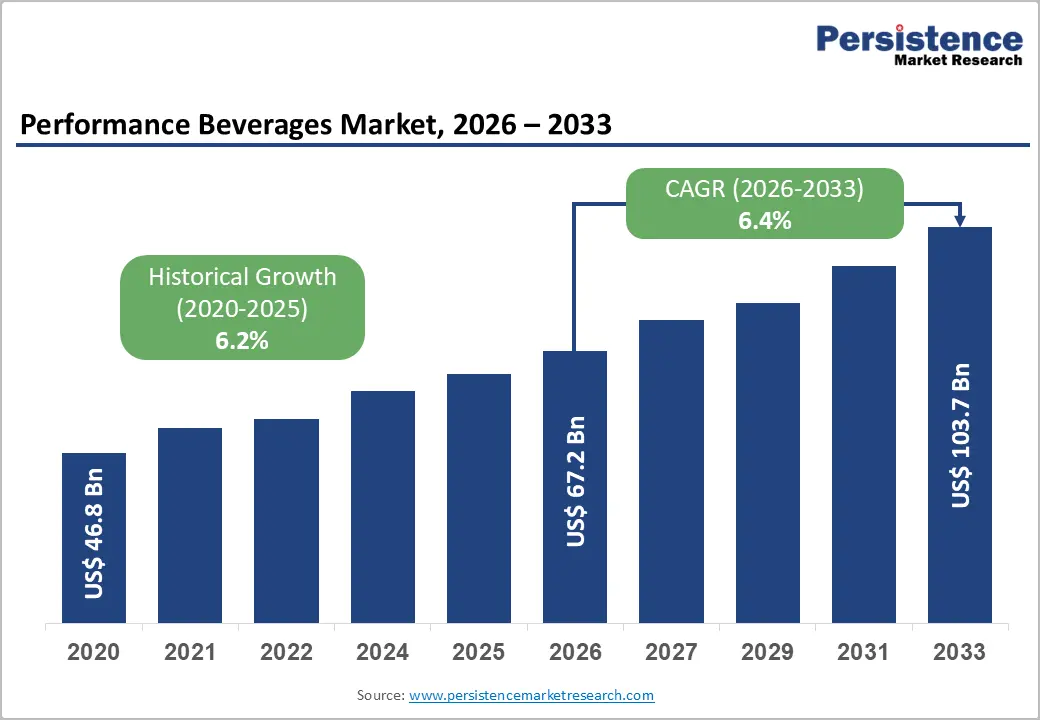

The global performance beverages market size is likely to be valued at US$67.2 billion in 2026 and is expected to reach US$103.7 billion by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033, driven by rising demand for functional hydration, energy support, and recovery-focused drinks across fitness and everyday wellness consumers.

Growth is supported by increasing adoption of low-sugar, clean-label, and nutrient-enhanced formulations containing caffeine, electrolytes, amino acids, and vitamins. Consumer adoption is widespread, with 46% of U.S. adults consuming energy drinks at least once monthly (2026 data), showing mainstream penetration beyond athletes. The FDA (2024 - 2026) continues to regulate caffeine safety with a recommended limit of 400 mg/day for healthy adults, shaping formulation standards and labeling transparency across the industry (National Center for Complementary and Integrative Health (NCCIH).

Key Industry Highlights:

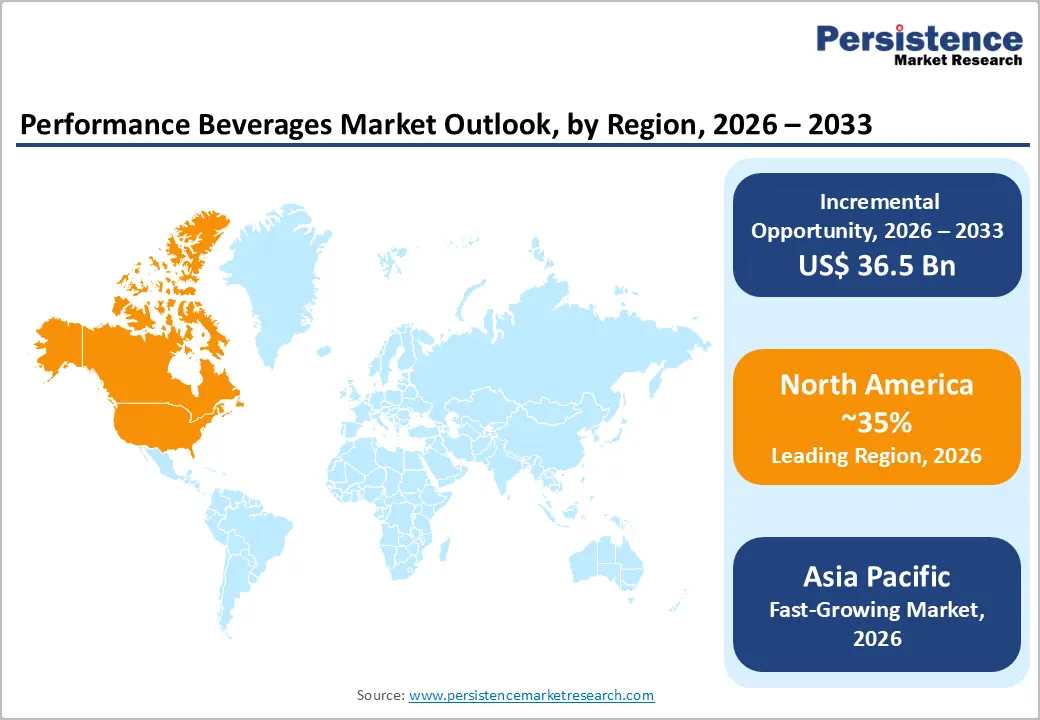

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong demand for energy, sports, and functional drinks supported by a mature fitness culture and high consumption of convenience-based nutritional beverages.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rapid urbanization, rising fitness awareness, and strong demand for energy, sports, and functional hydration drinks.

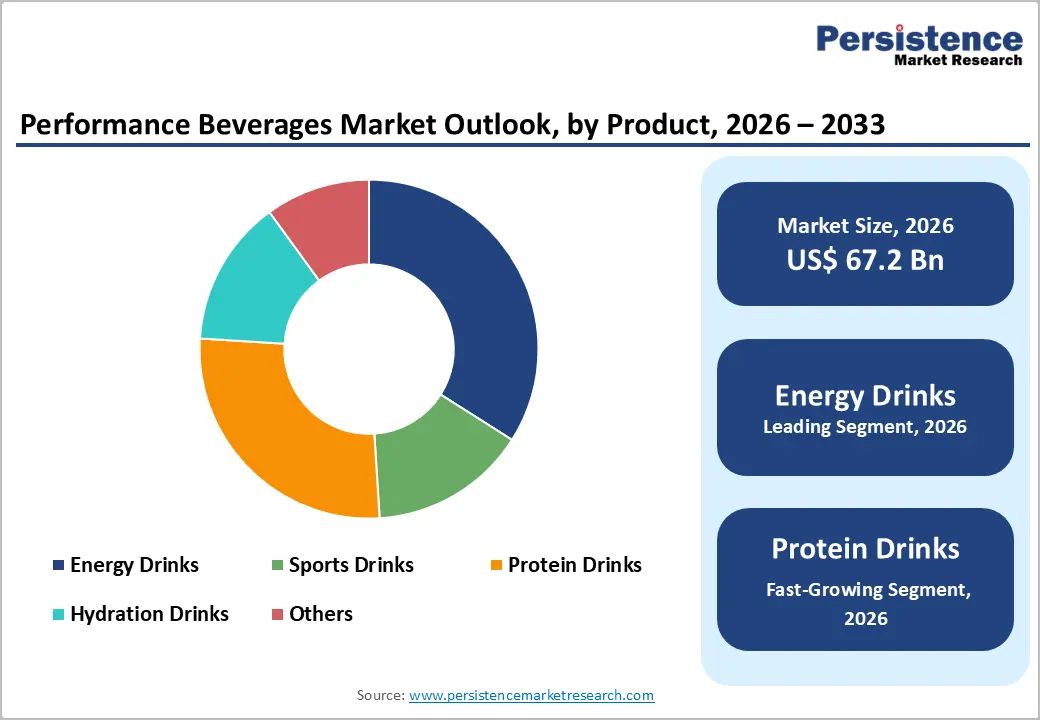

- Leading Product Type: Energy drinks are projected to represent the leading product type in 2026, accounting for 35% of the revenue share, driven by strong demand for instant energy and convenient, caffeine-based performance beverages.

- Leading Ingredient Type: Vitamins & minerals are anticipated to be the leading ingredient type, accounting for over 40% of the revenue share in 2026, supported by their essential role in hydration, energy metabolism, and widespread use in functional beverage formulations.

- Key Opportunity: The rapid shift from traditional high-sugar energy drinks to clean-label, low-sugar, and personalized performance beverages integrating functional ingredients for everyday health, hydration, and cognitive support.

DRO Analysis

Driver - Rising Participation in Sports, Fitness, and Active Lifestyles

The performance beverages market is strongly driven by rising participation in sports, fitness, and active lifestyles, especially in urban populations. According to the WHO (2024), over 1.8 billion adults are insufficiently active, leading to increased awareness of structured fitness routines and preventive health behaviors. This shift is increasing demand for energy drinks, sports drinks, and protein-based hydration solutions.

In 2025, global gym membership penetration increased significantly in major markets such as the U.S. and India, directly influencing the consumption of functional beverages designed for endurance, hydration, and post-workout recovery.

Fitness participation trends continue to accelerate, with wearable technology adoption rising sharply; fitness app usage is increasing significantly year-on-year, supporting higher engagement in active lifestyles. This digital fitness ecosystem encourages real-time hydration and energy replenishment behaviors, increasing the consumption frequency of performance beverages. Organized sports participation among youth and adults is expanding across Asia-Pacific and North America, reinforcing demand for functional drinks.

Restraint - Health Concerns Over Additives

One of the key restraints in the performance beverages market is growing health concerns over artificial additives, high caffeine content, and excessive sugar levels. The U.S. Food and Drug Administration (FDA, 2024) continues to monitor caffeine intake safety, recommending a daily limit of about 400 mg for healthy adults due to potential cardiovascular and neurological effects. Increasing consumer awareness of obesity and metabolic disorders is reducing demand for traditional high-sugar energy drinks.

According to the FDA safety monitoring reports (2025), energy drink-related adverse event evaluations remain under observation, especially among younger consumers aged 12-24. This has led to stricter labeling requirements and voluntary industry reformulations. The increasing prevalence of lifestyle diseases such as diabetes and hypertension is shifting consumer preference toward natural and low-calorie alternatives. Traditional formulations face declining acceptance, compelling companies to invest heavily in clean-label and plant-based innovations to maintain market relevance.

Opportunity - Technological Convergence with Personalized Nutrition and Clean-Label Innovation

Consumers are increasingly seeking products that align with their individual fitness goals, metabolic needs, and daily routines. Companies are increasingly leveraging biometric data to develop customized hydration and energy solutions tailored to individual metabolic needs. According to digital health analytics (2026), over 30% of fitness consumers now prefer personalized dietary recommendations, creating strong demand for adaptive performance beverages.

Clean-label innovation is reshaping product development, with growing consumer preference for natural, transparent, and minimally processed ingredients. Manufacturers are focusing on plant-based sources, natural caffeine, botanical extracts, and reduced sugar formulations to meet evolving health expectations. This trend is driving reformulation strategies and new product launches that emphasize purity, sustainability, and nutritional value.

Category-wise Analysis

Product Type Insights

Energy drinks are expected to lead the performance beverages market, accounting for approximately 35% of revenue in 2026, driven by strong demand for instant energy, mental alertness, and convenient consumption formats. These beverages are widely adopted across both fitness-focused consumers and everyday users seeking quick stimulation during work, travel, or physical activity. For instance, Red Bull, which has successfully positioned itself as a lifestyle energy drink brand, is widely consumed across sports, gaming, and professional environments.

Protein drinks are likely to represent the fastest-growing segment, supported by increasing awareness of muscle recovery, weight management, and overall fitness nutrition. This trend is particularly strong among gym-goers, working professionals, and health-conscious individuals seeking convenient nutrition. For example, Premier Protein, which offers ready-to-drink protein shakes tailored for recovery and daily nutrition, is gaining popularity among both athletes and general consumers.

Ingredient Type Insights

Vitamins and minerals are projected to lead the market, capturing around 40% of the revenue share in 2026, as they form the foundational component of most performance beverages. These ingredients play a crucial role in supporting hydration, energy metabolism, and overall bodily functions, making them essential in both sports and everyday functional drinks. A notable example includes Gatorade, which utilizes electrolytes and essential minerals to support hydration and endurance, reinforcing the importance of vitamins and minerals in performance-focused formulations.

Amino acids are likely to be the fastest-growing ingredient, driven by increasing demand for targeted performance benefits such as muscle recovery, endurance, and fatigue reduction. Consumers are shifting toward functional beverages that deliver scientifically backed results, encouraging the inclusion of branched-chain amino acids (BCAAs) and essential amino acids (EAAs) in formulations. For example, MusclePharm BCAA Energy Drink, which combines BCAAs with energy-support ingredients, reflects the rising integration of amino-based formulations in mainstream performance beverages.

End-user Insights

Fitness enthusiasts are expected to lead the performance beverages market, accounting for approximately 55% of revenue in 2026, driven by reflecting the shift of performance beverages from professional sports to mainstream lifestyle consumption. This group includes gym-goers, runners, and individuals engaged in regular physical activity who rely on functional drinks for hydration, energy, and recovery. For instance, Muscle Milk, which targets fitness-conscious individuals seeking convenient protein intake for muscle recovery and strength building.

Teenagers are likely to represent the fastest-growing segment, supported by increasing participation in sports, rising influence of social media, and growing exposure to fitness and energy-focused lifestyles. Younger consumers are highly influenced by branding, digital marketing, and peer trends, leading to higher adoption of energy and performance beverages. Despite this, brands continue to innovate with low-sugar and functional variants to appeal to this demographic. For instance, Gatorade is widely consumed among young athletes for hydration during sports activities.

Regional Insights

North America Performance Beverages Market Trends

North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong consumer demand. The U.S. leads regional consumption due to a well-established fitness culture, high adoption of functional drinks, and continuous innovation in energy, protein, and hydration beverages. Recent trends (2025-2026) show increasing demand for low-sugar, clean-label, and plant-based formulations, along with the growing popularity of ready-to-drink protein beverages.

Canada is focusing on sustainability and clean-label trends, while Mexico is benefiting from increasing youth consumption and sports participation. Monster Beverage Corporation strengthened its regional position through the acquisition of Bang Energy in 2023, highlighting ongoing consolidation and innovation in high-performance energy drink categories. The U.S. is witnessing rapid growth in personalized nutrition and functional beverage innovation, with consumers increasingly seeking beverages enriched with protein, vitamins, and adaptogens.

Europe Performance Beverages Market Trends

Europe is likely to be a significant market for performance beverages in 2026, due to strong demand for functional, health-oriented drinks and a shift toward preventive nutrition. The U.K. is witnessing increasing adoption of functional beverages such as energy drinks, kombucha, and adaptogen-based products, supported by rising wellness awareness and lifestyle-driven consumption patterns. Germany remains the largest and most mature market, backed by high health literacy, strong purchasing power, and a well-established retail network that promotes clean-label and scientifically validated products.

The region is also witnessing a clear shift toward low-sugar, plant-based, and functional hydration beverages, influenced by changing consumer lifestyles and declining consumption of traditional sugary drinks. Recent developments highlight growing investment in healthier beverage categories, with Danone S.A. expanding its focus on bottled water and functional hydration products in the U.K. and France to align with rising demand for healthier alternatives.

Asia Pacific Performance Beverages Market Trends

The Asia Pacific region is likely to be the fastest-growing region in 2026, driven by its large population base and highly developed e-commerce ecosystem, enabling rapid distribution of functional drinks such as energy beverages and fortified hydration products. The market is also witnessing strong innovation in low-sugar and clean-label formulations, supported by evolving food regulations and consumer preference for healthier alternatives.

In China, domestic brands are expanding functional beverage portfolios through digital-first strategies and premium positioning. India is seeing increased adoption of herbal and Ayurvedic-based performance drinks, reflecting consumer preference for natural and immunity-focused products. Japan continues to lead in innovation with nootropic and functional beverages targeting mental performance and workplace productivity. For example, Otsuka Pharmaceutical Co., Ltd., which continues to expand its functional hydration and health drink portfolio across Asia.

Competitive Landscape

The global performance beverages market exhibits a moderately fragmented structure, driven by the presence of both multinational beverage giants and emerging niche brands focusing on functional and clean-label innovations. The market is characterized by high competitive intensity, with a few dominant players holding significant influence through strong brand equity, extensive distribution networks, and continuous product innovation.

With key leaders including The Coca-Cola Company, Danone S.A., and Nestlé S.A., the market continues to evolve through innovation and portfolio diversification. These players compete through product differentiation, clean-label formulations, sugar reduction, and expansion into functional hydration, protein, and plant-based beverages. Strategic initiatives such as mergers, acquisitions, and new product launches are common to strengthen market positioning.

Key Industry Developments:

- In March 2026, Syncron unveiled new performance beverages ELIXIR and HYDRATE, expanding its functional drink portfolio with athlete-developed formulations focused on energy, hydration, recovery, and cognitive performance. The products incorporate ingredients such as green tea-based caffeine, nootropics, amino acids, and electrolytes, reflecting the growing trend toward clean-label and multi-functional beverages designed for both athletic and everyday performance needs.

- In February 2026, C4 expanded its performance energy portfolio with the launch of Mango Fuego, a new tropical-spicy flavored energy drink designed to support energy, focus, and endurance, while aligning with the growing demand for zero-sugar, high-caffeine functional beverages and bold flavor innovation in the performance drinks market.

- In April 2026, Hive Mind Mead expanded its beverage portfolio with the launch of Tavern Mead, a traditionally crafted drink made from 100% honey, aimed at offering a more authentic, clean-label alternative to mass-market formulations while reinforcing the growing consumer demand for natural, minimally processed beverages.

Companies Covered in Performance Beverages Market

- PepsiCo Inc.

- The Coca-Cola Company

- Red Bull GmbH

- Monster Beverage Corporation

- Glanbia Plc

- Abbott Laboratories

- Nestlé S.A.

- Danone S.A.

- GNC Holdings Inc.

- Rockstar Inc.

- Living Essentials LLC

- Arizona Beverage Company

- Vital Pharmaceuticals, Inc. (VPX)

- Otsuka Pharmaceutical Co., Ltd.

- Amway Corporation

- Herbalife Nutrition Ltd.

- Unilever

Frequently Asked Questions

The global performance beverages market is projected to reach US$67.2 billion in 2026.

The performance beverages market is driven by rising fitness participation, increasing demand for functional hydration and energy, and growing consumer preference for convenient, health-oriented drinks.

The performance beverages market is expected to grow at a CAGR of 6.4% from 2026 to 2033.

Key market opportunities lie in the growth of personalized nutrition and clean-label, low-sugar performance beverages with advanced functional ingredients.

PepsiCo Inc., The Coca-Cola Company, Red Bull GmbH, Monster Beverage Corporation, Glanbia Plc, and Abbott Laboratories are the leading players.