Industry: Healthcare

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 196

Report ID: PMRREP2895

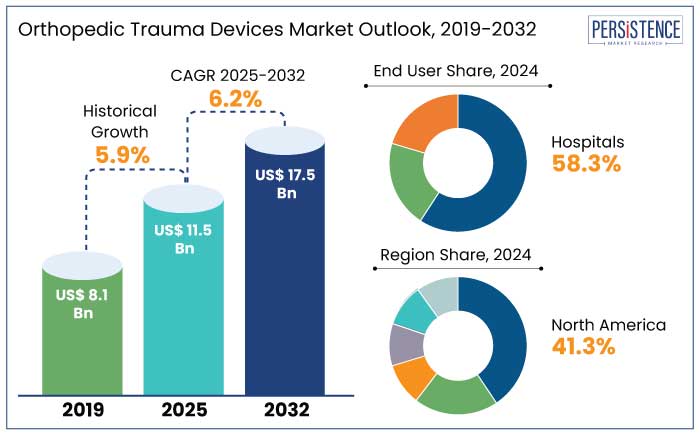

The global orthopedic trauma devices market is estimated to reach a size of US$ 11.5 Bn in 2025. It is predicted to rise at a CAGR of 6.2% through the assessment period to reach a value of US$ 17.5 Bn by 2032.

Increased incidence of fractures, sports-related injuries, and degenerative bone diseases is expected to propel the demand for orthopedic trauma devices.

Asia Pacific, particularly countries like India and China, is witnessing a surge in sports injuries due to increasing participation in athletic activities, contributing to market expansion. In March 2024, Johnson & Johnson launched its advanced 3D-printed titanium implants for orthopedic trauma, enhancing patient-specific solutions and recovery outcomes.

Advancements in implant materials like bio-ceramics and biocompatible polymers address challenges such as stiffness and iatrogenic injuries. 3D printing technology is transforming therapy by allowing for the development of bespoke implants and anatomical models, improving precision in musculoskeletal care.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Orthopedic Trauma Devices Market Size (2025E) |

US$ 11.5 Bn |

|

Projected Market Value (2032F) |

US$ 17.5 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

6.2% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

5.9% |

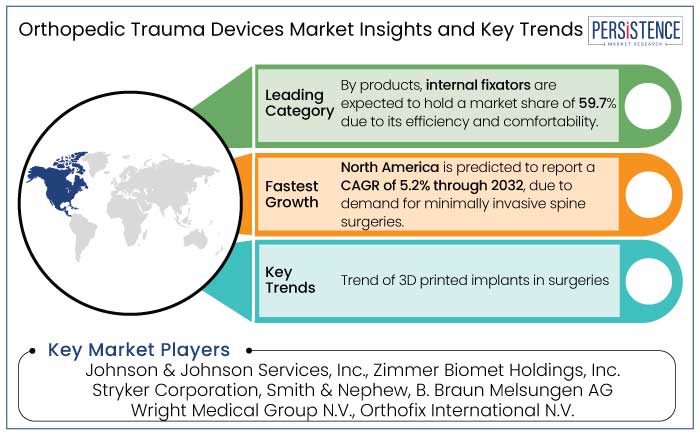

North America is projected to hold a 41.3% market share in 2025 with a forecast CAGR of 5.2% during the forecast period, reflecting robust demand for advanced trauma care solutions. The demand for orthopedic trauma devices in North America is poised for significant growth, driven by the rising prevalence of arthritis, back pain, and neck pain.

Advancements in minimally invasive spine surgeries, such as the development of specialized orthopedic devices, are enhancing surgical precision and recovery times. In January 2024, Medtronic launched a new MIS spinal fixation system in the U.S., designed to reduce operative time and improve patient outcomes.

The demand for orthopedic procedures is expanding due to the growing geriatric population, increased awareness, and favorable government reimbursement policies.

The orthopedic trauma device market in Asia Pacific is expected to a market share of 27.4% in 2025, due to an aging population and advancements in medical technology, with a projected CAGR of 7.5% through 2032.

Aging population, industrialization, and urbanization in China are contributing to an increase in traumatic fractures, especially among young and middle-aged patients. Health insurance policies in Asia Pacific countries are improving access to advanced trauma care, driving market growth due to technological innovations.

Internal fixators, such as rods, screws, metal plates, and wires, are expected to maintain dominance in the global orthopedic trauma devices market, accounting for 59.7% of market share in 2025. These devices ensure proper healing, reduce hospital stays, and expedite patient recovery.

Advanced materials like titanium and bio-absorbable polymers are transforming orthopedic care, enhancing the durability, compatibility, and ease of use of internal fixators for better patient outcomes.

Hospitals are projected to maintain a 58.3% share of the global market in 2025. The increasing global prevalence of injuries and trauma, estimated by the WHO to be over 50 Mn non-fatal injuries annually, is propelling the hospitals segment.

Advancements in technology and minimally invasive procedures have made hospitals the preferred location for orthopedic surgeries. Hospitals benefit from reimbursement policies that ease the financial burden on patients, further driving procedure volumes.

The presence of trauma centers and highly skilled medical professionals ensures timely and effective treatment, cementing hospitals' critical role in the orthopedic devices market. The integration of digital imaging and robotic-assisted surgery is enhancing the efficiency and outcomes of orthopedic care.

The global orthopedic trauma devices market is propelling due to the rising incidence of road accidents and sports-related injuries. According to the WHO, road traffic injuries claim 1.3 Mn lives annually and cause up to 50 Mn non-fatal injuries, creating demand for trauma devices.

The aging population, especially in Japan and Italy, has increased osteoporosis and fracture cases, thereby boosting the demand. Technological developments have improved surgical results and durability, such as titanium-based implants and biocompatible materials. For example,

The adoption of 3D printing in customized orthopedic implants is also gaining traction, offering patient-specific solutions. Improved healthcare infrastructure in emerging regions like India and Brazil and expanded insurance coverage in developed regions are facilitating access to advanced trauma care.

The global orthopedic trauma maneuvers market recorded a CAGR of 5.9% in the historical period from 2019 to 2023. Implants for bone fixation are often used in orthopedics, and the materials used have changed from being inert to matching the form of bone. For external fixation, bioactive, biocompatible, and absorbable materials are utilized to preserve fracture length, alignment, and rotation all of which are critical for trauma centers.

External fixation is crucial for fracture treatment due to its rapid application, reduced blood loss, and minimally invasive nature. It minimizes injection risk and wound complications by allowing time for soft tissue swelling in severe injuries.

An increase in small fractures, major injuries, accidents, deaths, trauma from traffic accidents, falls, osteoarthritis, and orthopedic sports injuries is expected to boost the need for external fixation worldwide. Demand for orthopedic pain devices is estimated to record a considerable CAGR of 6.2% during the forecast period between 2024 and 2032.

Surge in Adoption of Minimally Invasive Surgical Procedures Drive the Demand

The increasing use of minimally invasive surgical procedures is driving a surge in the demand for advanced trauma fixation devices. According to a 2023 report by the National Center for Biotechnology Information, MIS procedures in orthopedics have increased by 22% in the past five years. This shift has spurred innovation in trauma fixation devices designed for precise placement through smaller incisions.

The trend towards MIS is transforming orthopedic trauma care, promoting the use of advanced, biocompatible fixation technologies for cost efficiency and improved patient outcomes.

Rising Road Accidents and Sports Injuries Require Advanced Trauma Treatments

The increasing incidence of road accidents and sports injuries is driving the demand for advanced trauma treatment solutions and surgical interventions. The World Health Organization reports that road traffic accidents cause around 1.3 Mn deaths annually and cause injuries to 20 to 50 Mn people globally.

A 2023 report by the American Academy of Orthopaedic Surgeons (AAOS) indicates a 15% rise in ligament and fracture injuries among athletes, underscoring the need for effective trauma management.

Limitations of Fixators Hinder the Adoption

For long-bone fractures, external fixation or joint replacements may be a better option than internal fixation, depending on the location. These techniques do have certain drawbacks, though, such as the possibility of infection and the size of the functional output. Additionally, joint contractures, a longer bone-healing period, and an elevated risk of infection at the sites where pins and wires enter the body might result from external fixators.

Orthopedic implants must be made of carefully selected materials to prevent bone fractures, abnormalities, or insufficient healing. The three biomaterials utilized to treat bone deformities and fractures are ceramics, metals, and polymers; each has certain benefits and drawbacks for its intended usage.

Adoption of 3D Printing Reshapes the Orthopedic Applications

3D printing technology is transforming the demand for orthopedic trauma devices by producing bespoke implants based on the anatomy of each patient to improve surgical results by guaranteeing a perfect fit and a quicker recovery. According to a 2023 report by the American Academy of Orthopaedic Surgeons, 3D printing applications in orthopedics grew by 18% over the prior year.

Advancements in Implant Materials and Designs Enhance Surgical Outcomes

The use of advanced implant materials and designs is reforming orthopedic trauma care, improving surgical outcomes, and expediting patient recovery. Modern implants, crafted from advanced materials like titanium alloys and bio-ceramics, provide superior strength, biocompatibility, and reduced infection risk.

Implants made with 3D printing may be precisely customized to meet the anatomy of the patient, improving fit and restorative functionality.

Businesses must innovate and set themselves apart in the highly competitive orthopedic trauma device market by utilizing cutting-edge materials to enhance performance and durability. To increase their market presence and reach more people, they are also developing strategic alliances and growing their distribution networks.

Start-ups in the sector are focusing on innovative developments, such as creating personalized implant materials and 3D printing technologies for personalized medical solutions. The trend towards minimally invasive surgical techniques is a significant shift, as these methods can improve patient outcomes and speed up recovery times.

An inventive pioneer in the sector is Spentys, a Belgian-based company that specializes in orthopedic immobilization devices. They provide each patient with customized orthoses, combining cost-effectiveness with individualized attention to improve patient comfort and the effectiveness of orthopedic therapies.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Product

By End User

By Region

To know more about delivery timeline for this report Contact Sales

The market is set to reach US$ 17.5 Bn by 2032.

Orthopedic trauma injuries are prevalent in falls, car crashes, bicycle accidents, gunshot wounds, and motorized scooter accidents.

The market is estimated to be valued at US$ 11.5 Bn in 2025.

Johnson & Johnson Services, Inc., Zimmer Biomet Holdings, Inc., Stryker Corporation, and Smith & Nephew are a few key players.

Advancements in implant materials and designs provides a key opportunity for the market players.