- Medical Devices

- Orthopedic Implants Market

Orthopedic Implants Market Size, Share, and Growth Forecast 2026 - 2033

Orthopedic Implants Market by Product Type (Reconstructive Joint Replacements, Spinal Implants, Trauma Fixation Implants, Craniomaxillofacial (CMF) Implants, Others), Biomaterial (Metallic Biomaterials, Polymeric Biomaterials, Ceramic Biomaterials, Composite Biomaterials, Bioabsorbable Materials), Application, End-user, and Regional Analysis, 2026 - 2033

Orthopedic Implants Market Size and Trend Analysis

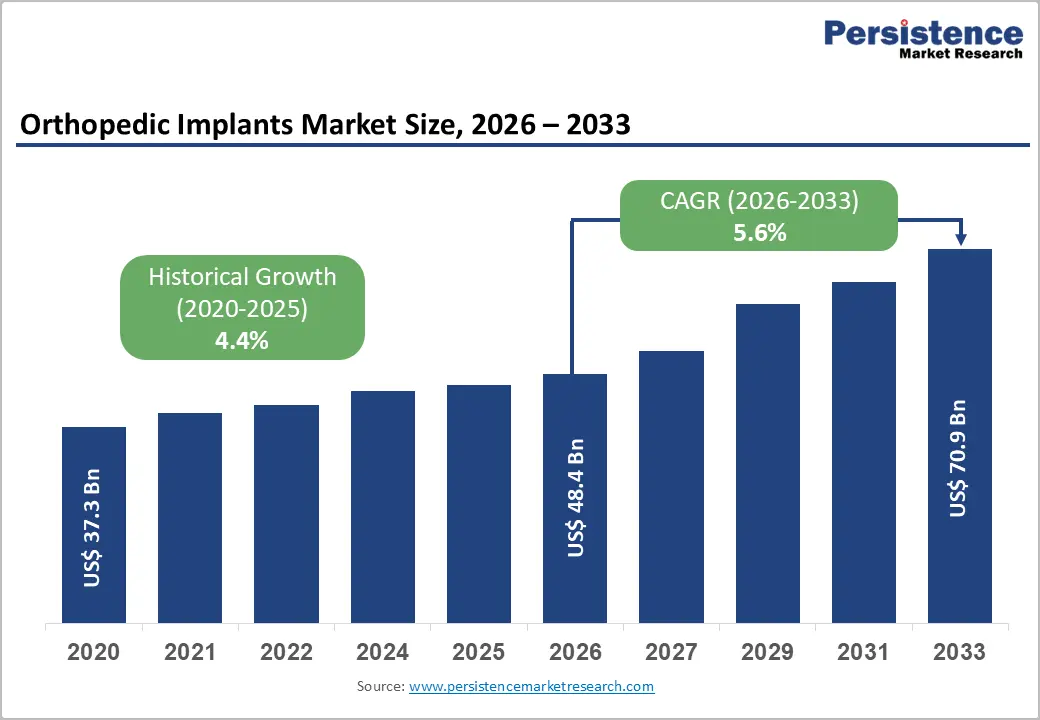

The global orthopedic implants market size is expected to be valued at US$ 48.4 billion in 2026 and projected to reach US$ 70.9 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. This robust growth trajectory is primarily driven by the escalating global burden of musculoskeletal disorders amplified by rapidly aging populations and rising obesity rates alongside accelerating adoption of minimally invasive surgical techniques, robotics-assisted orthopedic procedures, and patient-specific implant technologies.

The World Health Organization (WHO) estimates that musculoskeletal conditions affect over 1.71 billion people globally, with osteoarthritis and fractures representing the leading indications for orthopedic implant procedures. Expanding healthcare infrastructure investment in emerging economies across Asia Pacific and Latin America, combined with improving reimbursement frameworks for elective orthopedic surgeries, further sustains broad-based demand growth across all product and regional segments through 2033.

Key Industry Highlights:

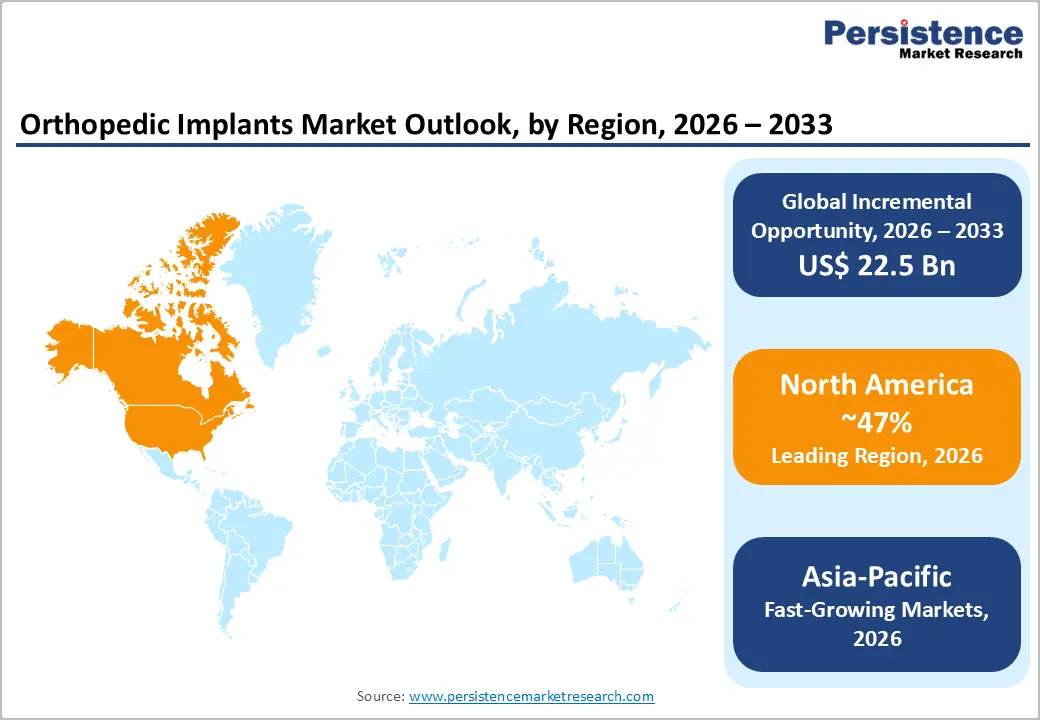

- Regional Leadership: North America dominates the global orthopedic implants market with a 47% revenue share in 2025, driven by the U.S.'s high surgical volumes, robust FDA regulatory ecosystem, leading robotics-assisted surgery adoption, and comprehensive reimbursement infrastructure supporting both inpatient and outpatient joint replacement procedures.

- Fast-growing Market: Asia Pacific is the fastest-growing regional market, propelled by the world's largest aging populations in China and Japan, rapidly expanding hospital infrastructure in India and ASEAN, and government-driven orthopedic capacity investments under programs like China's Healthy China 2030 initiative.

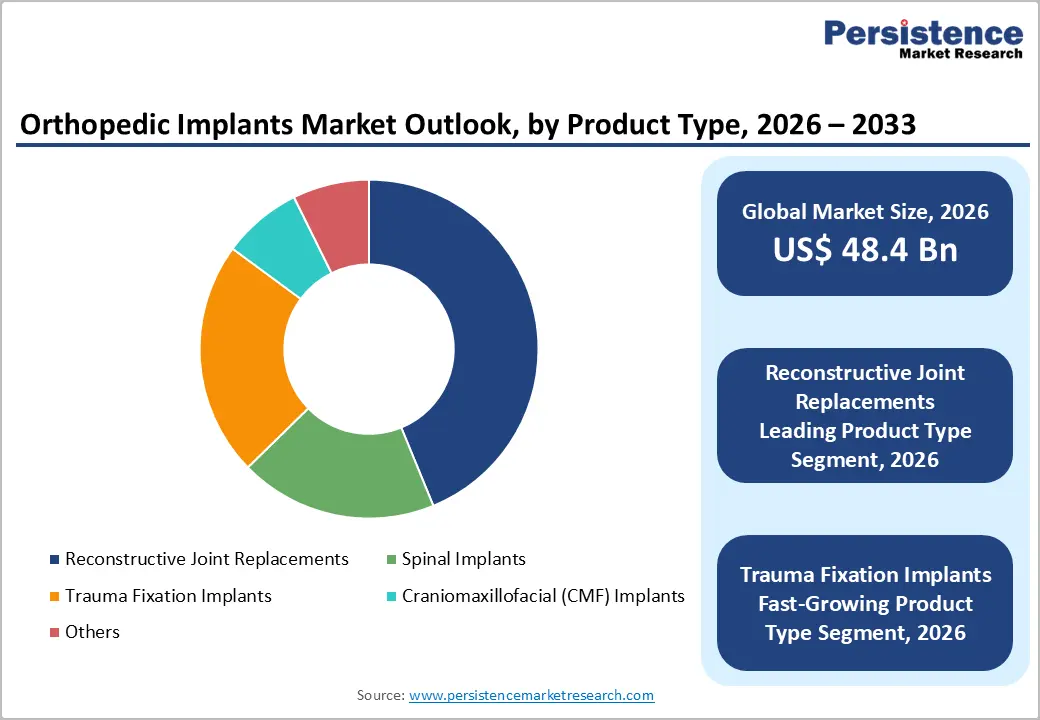

- Leading Product: Reconstructive Joint Replacements lead the product landscape with a 44% market share in 2025, anchored by rising global osteoarthritis prevalence affecting 528 million people per WHO, growing primary and revision arthroplasty volumes, and premium pricing from robotic-assisted and patient-specific implant technologies.

- Fast-growing Product: Trauma fixation implants represent the fast-growing product segment, driven by rising road traffic accident rates in emerging markets 1.19 million deaths annually per WHO expanding sports medicine demand, and growing distributor network penetration in high-growth markets across India, Brazil, and Southeast Asia.

- Key Opportunity: The rapid migration of joint replacement procedures to Ambulatory Surgical Centers (ASCs) presents a transformative opportunity, with over 5,700 Medicare-certified ASCs in the U.S. and growing global equivalents demanding ASC-optimized implant portfolios, streamlined instrument sets, and value-based commercial models from orthopedic manufacturers.

Market Dynamics

Drivers - Rise in Global Burden of Musculoskeletal Disorders and Aging Demographics

The accelerating global prevalence of musculoskeletal conditions, including osteoarthritis, rheumatoid arthritis, osteoporosis, and traumatic fractures, enable the orthopedic implants market growth. The WHO reports that osteoarthritis alone affects approximately 528 million people worldwide, a number that has increased by 113% since 1990. As populations age, the incidence of joint degeneration and fractures rises disproportionately: the International Osteoporosis Foundation (IOF) estimates that one osteoporotic fracture occurs every 3 seconds globally, resulting in over 8.9 million fractures annually.

The United Nations (UN) projects the global population aged 65 and above to double to 1.5 billion by 2050, creating a compounding patient pipeline for knee, hip, and spinal implant procedures that underpins long-term demand growth across all major markets.

Technological Advancements in Robotic-Assisted Surgery and Patient-Specific Implants

Rapid innovation in robotic-assisted orthopedic surgery platforms and patient-specific implant manufacturing is transforming clinical outcomes, driving procedure volumes, and expanding the addressable market for premium implant products. Stryker's Mako robotic arm system FDA-cleared for total knee, total hip, and partial knee arthroplasty has been shown in clinical studies published in the *Journal of Bone and Joint Surgery* to significantly reduce implant positioning variability and improve early functional outcomes.

Similarly, additive manufacturing (3D printing) is enabling patient-matched implants for complex revision and CMF cases. The U.S. FDA has cleared over 100 3D-printed orthopedic device designs, reflecting a mature regulatory pathway. These technologies command premium pricing, elevate average selling values, and are increasingly standard of care at high-volume orthopedic centers globally.

Restraints - High Procedure Costs and Reimbursement Limitations in Emerging Markets

The high cost of orthopedic implant procedures, such as total knee arthroplasty in the United States averaging US$ 30,000-50,000 per episode of care according to the Healthcare Cost and Utilization Project (HCUP) creates significant access barriers in low- and middle-income countries (LMICs). Limited reimbursement coverage for elective orthopedic procedures in public health systems across Southeast Asia, Latin America, and Africa constrains procedure volumes and shifts demand toward lower-cost, lower-margin implant products. This pricing pressure suppresses premium product penetration and revenue realization in rapidly growing population markets, creating a structural ceiling on addressable market expansion in these geographies despite high clinical need.

Post-Market Surveillance Risks and Implant Recall Events

High-profile implant recall events continue to create reputational and financial risk for orthopedic implant manufacturers and dampen physician and patient confidence. The U.S. FDA's MAUDE (Manufacturer and User Facility Device Experience) database documents thousands of adverse event reports annually for orthopedic devices. Metal-on-metal hip implant failures culminating in major recalls from multiple manufacturers generated billions of dollars in litigation costs and regulatory scrutiny. These events elevate post-market clinical follow-up requirements, increase product liability insurance costs, and create conservative adoption behavior among surgeons for novel implant technologies, collectively slowing market velocity and compressing manufacturer margins.

Opportunities

Rapid Growth of Ambulatory Surgical Centers for Outpatient Joint Replacement

The accelerating migration of orthopedic procedures particularly primary total knee and hip arthroplasty from inpatient hospital settings to Ambulatory Surgical Centers (ASCs) represents a significant commercial opportunity for implant manufacturers. The U.S. Centers for Medicare & Medicaid Services (CMS) removed total hip arthroplasty from its Inpatient-Only (IPO) list in 2020 and total knee arthroplasty in 2018, enabling Medicare reimbursement for outpatient joint replacement.

The Ambulatory Surgery Center Association (ASCA) reports that over 5,700 Medicare-certified ASCs operate in the United States, with orthopedic procedures representing the largest and fastest-growing service line by volume. Implant manufacturers offering ASC-optimized implant portfolios including streamlined instrument sets, single-use surgical tools, and value-based pricing models are capturing disproportionate share in this high-growth channel while benefiting from shorter surgical cycles and faster inventory turns.

Expansion of Trauma Fixation Implants in Emerging Markets and Sports Medicine

Rise in road traffic accident rates in rapidly motorizing emerging economies, and growing sports-related injury incidence globally. The World Health Organization (WHO) reports approximately 1.19 million road traffic deaths annually, with a disproportionate burden in low- and middle-income countries where motorization is increasing fastest. The American Academy of Orthopaedic Surgeons (AAOS) estimates that over 6 million fractures occur annually in the United States alone.

Simultaneously, rising global sports participation, particularly in the Asia Pacific, where government wellness initiatives are driving recreational activity, is elevating demand for plates, screws, and intramedullary nailing systems. Companies expanding distribution infrastructure in India, Brazil, Indonesia, and Vietnam are well-positioned to capture this high-growth trauma segment.

Category-wise Analysis

Product Type Insights

Reconstructive joint replacements dominate the orthopedic implants market with approximately 44% revenue share in 2026, underpinned by the high and growing global prevalence of end-stage osteoarthritis and the clinical effectiveness of total joint arthroplasty as a definitive treatment. Knee replacement implants represent the largest sub-segment, with the American Academy of Orthopaedic Surgeons (AAOS) projecting that total knee arthroplasty volumes in the U.S. alone could reach 1.26 million procedures annually by 2030.

Hip replacement implants constitute the second-largest sub-segment, similarly driven by aging demographics and active lifestyle expectations of the baby boomer generation. The segment benefits from consistent technology upgrades, including cementless fixation, highly cross-linked polyethylene liners, and robotic-assisted implant positioning that support premium pricing and sustain manufacturer revenue growth.

Biomaterial Analysis

Metallic Biomaterials represent the dominant biomaterial category, capturing approximately 65% of the global orthopedic implants market revenue in 2026. Titanium alloys (Ti-6Al-4V) and cobalt-chromium (CoCr) alloys remain the materials of choice for load-bearing joint replacement and trauma fixation implants due to their superior mechanical strength, corrosion resistance, fatigue performance, and established long-term clinical safety records spanning over three decades of outcome data.

Stainless steel continues to serve cost-sensitive trauma fixation applications in emerging markets. The advent of porous titanium structures fabricated via additive manufacturing has further elevated the clinical utility of metallic biomaterials by enabling osseointegration surfaces that mimic cancellous bone architecture, improving biological fixation in cementless implant designs. This continuous innovation within metallic biomaterials reinforces the category's dominant revenue position.

Application Insights

Osteoarthritis is the leading application segment, accounting for approximately 42% of the global orthopedic implants market revenue in 2025. It is the most common joint disease globally, with the WHO reporting approximately 528 million people affected predominantly in the knee, hip, and hand joints. The irreversible cartilage degradation characteristic of osteoarthritis makes joint replacement the definitive therapeutic endpoint, creating a large, stable, and growing surgical candidate pool.

Risk factors including obesity, aging, prior joint injury, and genetic predisposition, are converging to expand the incidence rate in both developed and emerging economies. The U.S. CDC reports that osteoarthritis affects approximately 32.5 million U.S. adults, and the increasing willingness of younger, more active patients to undergo early joint replacement further broadens the addressable procedural volume.

End-user Analysis

Hospitals are the leading end-user segment, contributing approximately 62% of global orthopedic implants market revenue in 2025. Hospitals serve as the primary site for complex primary joint replacements, revision surgeries, spinal fusion procedures, and major trauma fixation, all of which require advanced imaging, intraoperative navigation, and post-operative rehabilitation capabilities concentrated in hospital settings. According to the American Hospital Association (AHA), orthopedic surgery ranks among the top revenue-generating clinical service lines for U.S. health systems, reflecting deep institutional investment in orthopedic surgical infrastructure and specialist physician employment.

The emergence of high-volume orthopedic specialty hospitals combining focused clinical expertise with procedural efficiency is further consolidating high-acuity implant volume within the hospital end-user segment globally.

Regional Insights

North America Orthopedic Implants Market Trends and Insights

North America is likely to account for approximately 47% of global orthopedic implants revenue in 2026, led by high procedural volumes, strong reimbursement systems, and rapid adoption of robotic-assisted arthroplasty and smart implant technologies. The region benefits from a mature innovation ecosystem and increasing migration of joint replacement procedures to ambulatory surgical centers, which is improving procedural efficiency and expanding implant utilization across both inpatient and outpatient settings.

U.S. Orthopedic Implants Market Trends and Insights

The U.S. represented nearly 88.2% of the North American market in 2025. Demand is supported by a high incidence of osteoarthritis, more than one million annual hip and knee replacements, and broad Medicare and commercial reimbursement. Market growth is further accelerated by the adoption of Mako, ROSA, and VELYS robotic platforms and expanding outpatient arthroplasty.

Canada Orthopedic Implants Market Trends and Insights

Canada is poised for an estimated 8.9% of regional revenue in 2026. Rising procedure volumes, expanding orthopedic wait-list reduction initiatives, and increased adoption of advanced implants in provincial healthcare systems are supporting steady market growth. Demand is strongest in Ontario, British Columbia, and Quebec, where large tertiary hospitals drive most joint reconstruction procedures.

Europe Orthopedic Implants Market Trends and Insights

Europe captured approximately 26.4% of global orthopedic implants revenue in 2026, supported by aging demographics, universal healthcare coverage, and strong arthroplasty registries that guide implant selection and procurement. Adoption of robotic-assisted surgery is increasing across major markets, while the EU Medical Device Regulation (MDR) is enhancing product quality and post-market surveillance standards throughout the region.

Germany Orthopedic Implants Market Trends and Insights

Germany is likely to register roughly 24.8% of the European market in 2026. The country benefits from one of the highest joint replacement volumes in Europe, comprehensive statutory reimbursement, and strong clinical data from the EPRD registry. High hospital capacity and rapid adoption of navigation and robotic systems continue to support premium implant demand.

UK Orthopedic Implants Market Trends and Insights

The UK is likely to account for about 17.6% of regional revenue in 2026. The National Joint Registry, covering more than three million procedures, supports evidence-based implant usage and procurement. Rising elective surgery recovery and increasing investment in orthopedic capacity are driving steady demand across NHS and private healthcare providers.

Asia Pacific Orthopedic Implants Market Trends and Insights

Asia Pacific represented approximately 20.8% of global orthopedic implants revenue in 2025 and is projected to register the fastest CAGR of 8.9% through 2032. Growth is driven by rapidly aging populations, expanding hospital infrastructure, increasing trauma incidence, and broader access to joint replacement procedures. Price reforms and localization initiatives are also reshaping supplier competition across the region.

China Orthopedic Implants Market Trends and Insights

China is expected to account for for nearly 41.5% of the Asia Pacific market in 2026. Healthy China 2030 initiatives and volume-based procurement programs are expanding procedure accessibility while lowering implant prices. Strong domestic manufacturing and rising demand for hip, knee, and trauma implants continue to accelerate market expansion.

Japan Orthopedic Implants Market Trends and Insights

Japan is likely to represent around 21.8% of regional revenue in 2026. With more than 29% of the population aged 65 and older, the country maintains one of Asia’s highest per-capita arthroplasty rates. Demand is supported by universal insurance coverage and widespread use of high-performance implant systems in advanced orthopedic centers.

Competitive Landscape

The global orthopedic implants market is moderately consolidated, with five major players Zimmer Biomet, Stryker, Johnson & Johnson MedTech (DePuy Synthes), Smith+Nephew, and Medtronic commanding an estimated combined revenue share exceeding 70% of the global market.

These leaders differentiate through comprehensive product portfolios spanning reconstruction, spine, trauma, and sports medicine; proprietary robotic surgery platforms; and surgeon training ecosystems. Strategic priorities include robotics-as-a-platform investments, digital surgery integration, and direct-to-ASC go-to-market models. Mid-tier innovators including Globus Medical, Arthrex, and Enovis compete effectively in spine, sports medicine, and enabling technology niches, creating dynamic competitive pressure across high-value sub-segments.

Key Developments:

- In October 2025, Andera Partners invested in Adler Ortho, a leading developer of premium orthopedic implants and bioresorbable fixation products. The investment is intended to accelerate Adler Ortho’s international expansion and strengthen its product portfolio across joint reconstruction, trauma, and sports medicine applications. It also supports increased investment in research and development, manufacturing scale-up, and strategic acquisitions to expand the company’s presence in high-growth orthopedic markets.

- In August 2025, OIC International, Medi Mold, and AddUp formed a strategic partnership to establish a state-of-the-art orthopedic implant manufacturing facility at Andhra Pradesh Medtech Zone in India. The facility will leverage advanced 3D printing and precision engineering technologies to support localized production of high-performance orthopedic implants and strengthen India’s domestic medical device manufacturing capabilities.

Companies Covered in Orthopedic Implants Market

- Zimmer Biomet

- Stryker

- Johnson & Johnson MedTech

- Smith+Nephew

- Medtronic

- Enovis

- Arthrex Inc.

- Globus Medical

- Biotek

- CONMED Corporation

- Exactech, Inc.

- Corin Group

- Conformis, Inc.

- Orthofix US LLC

- MicroPort Orthopedics Inc.

- Others

Frequently Asked Questions

The global orthopedic implants market is projected to be valued at US$ 48.4 billion in 2026, growing from US$ 37.3 billion in 2020 at a historical CAGR of 4.4%. The market is forecast to further expand to US$ 70.9 billion by 2033, driven by rising osteoarthritis prevalence, aging demographics, and the accelerating adoption of robotic-assisted surgical platforms globally.

Demand in the orthopedic implants market is primarily driven by the rising prevalence of osteoarthritis and osteoporosis, increasing sports injuries and trauma cases, a growing geriatric population, and expanding adoption of minimally invasive and robot-assisted orthopedic procedures.

North America leads with approximately 47% revenue share in 2025, driven by the U.S.'s high joint replacement surgical volumes, leading FDA-regulated innovation ecosystem, strong commercial and Medicare reimbursement frameworks, and concentration of global orthopedic market leaders including Zimmer Biomet, Stryker, Johnson & Johnson MedTech, and Smith+Nephew.

Key growth opportunities in the orthopedic implants market include the development of 3D-printed patient-specific implants, expansion in emerging markets, increasing use of smart implants and advanced biomaterials, and growth in outpatient joint replacement procedures.

The leading global orthopedic implant companies include Zimmer Biomet, Stryker, Johnson & Johnson MedTech (DePuy Synthes), Smith+Nephew, Medtronic, Globus Medical, Arthrex Inc., Enovis, Exactech, Inc., Corin Group, Conformis, Inc., Orthofix US LLC, and MicroPort Orthopedics Inc. These companies compete through robotic surgery platforms, broad implant portfolios, surgeon training programs, and strategic expansion into ASC and emerging market channels.