- Pharmaceuticals

- Oral Solid Dosage Contract Manufacturing Market

Oral Solid Dosage Contract Manufacturing Market Size, Share, and Growth Forecast, 2026 - 2033

Oral Solid Dosage Contract Manufacturing Market by Product Type (Tablets, Capsules, Powders, Granules, Others), Mechanism (Immediate Release, Others), End-user (Large Size Companies, Medium & Small Size Companies, Others), and Regional Analysis for 2026 - 2033

Oral Solid Dosage Contract Manufacturing Market Size and Trends Analysis

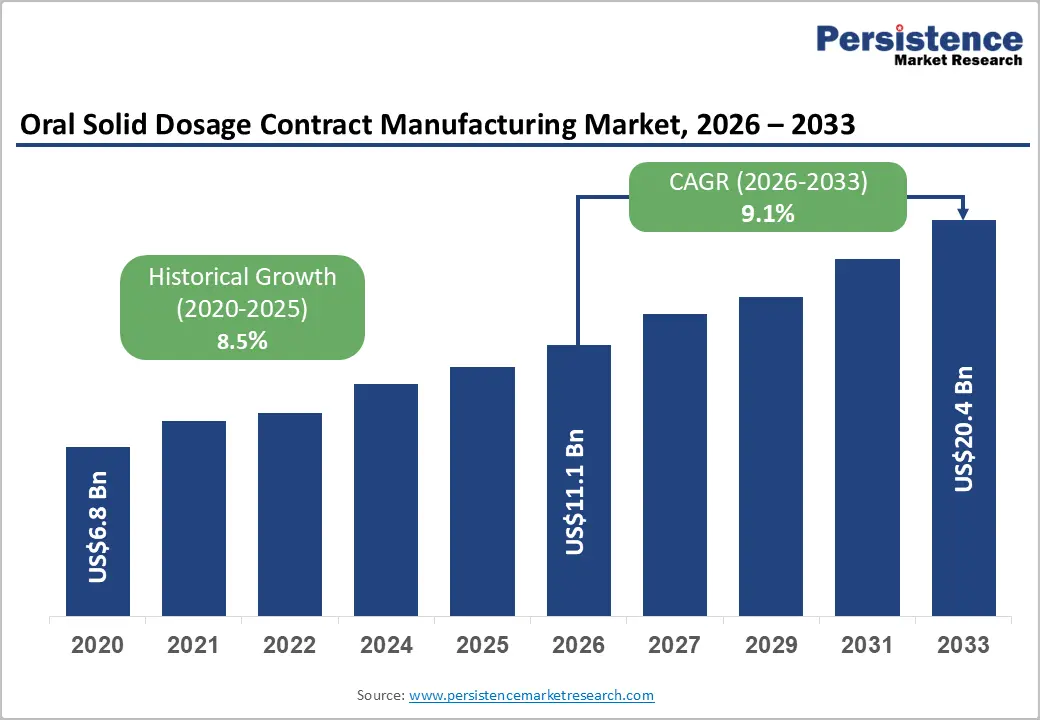

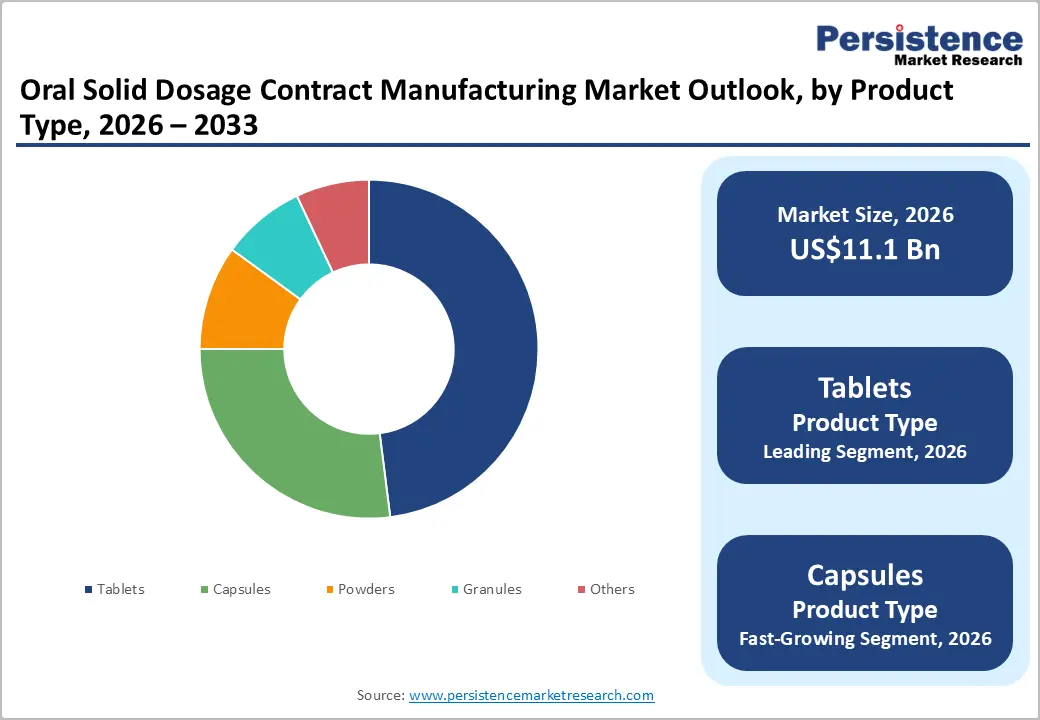

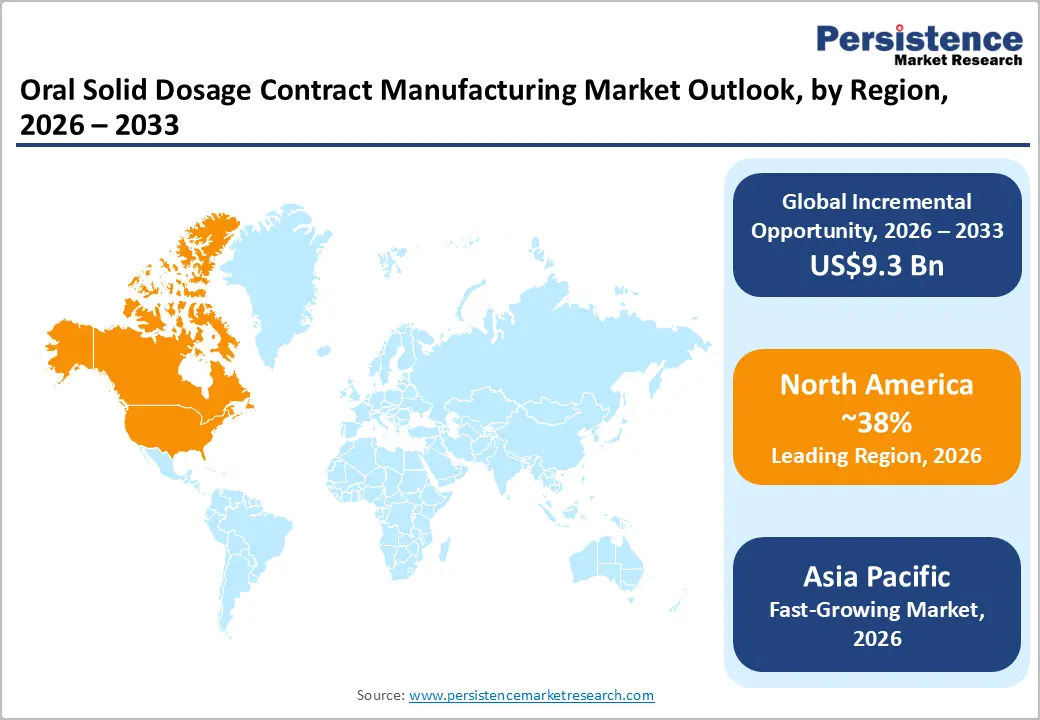

The global oral solid dosage (OSD) contract manufacturing market size is likely to be valued at US$11.1 billion in 2026, and is expected to reach US$20.4 billion by 2033, growing at a CAGR of 9.1% during the forecast period from 2026 to 2033, driven by the pharmaceutical industry’s increasing reliance on outsourcing manufacturing activities to specialized contract development and manufacturing organizations (CDMOs) to minimize capital investments, shorten drug commercialization timelines, and access advanced expertise in tablet and capsule formulation, process scale-up, and large-scale commercial manufacturing.

Key Industry Highlights:

- Dominant Region: North America is expected to dominate the market with approximately 38% revenue share in 2026, driven by the world's highest pharmaceutical consumption, robust FDA-regulated cGMP manufacturing infrastructure, and the extensive outsourcing strategies of major pharmaceutical companies headquartered in the U.S.

- Fastest Growing Region: Asia Pacific is projected to be the fastest-growing regional market, advancing at a CAGR of approximately 10.5% through 2033, driven by cost-competitive manufacturing capacity in India and China, expanding regulatory compliance capabilities, and growing investments in advanced OSD manufacturing infrastructure.

- Leading Product Type: Tablets are expected to dominate with approximately 52% share in 2026, reflecting their universal clinical adoption across therapeutic areas, scalable manufacturing economics, and extensive patient acceptance across global pharmaceutical markets.

- Dominant Mechanism: Immediate release formulations are estimated to dominate with approximately 58% of market revenue in 2026, underpinned by their broad applicability across generic and branded pharmaceutical portfolios and lower technical complexity relative to modified release systems.

DRO Analysis

Driver - Pharmaceutical Outsourcing Acceleration and CDMO Strategic Partnerships

The pharmaceutical industry's accelerating shift toward a fully-integrated outsourcing model driven by the strategic imperative to reduce fixed manufacturing infrastructure costs, optimize capital deployment, and achieve faster product commercialization timelines is the most powerful structural demand driver sustaining the oral solid dosage contract manufacturing market's growth trajectory. According to the Pharmaceutical Research and Manufacturers of America (PhRMA), global pharmaceutical R&D investment exceeded US$102 billion in 2023, intensifying pressure on pharmaceutical companies to redirect capital from manufacturing asset investment toward innovation-focused expenditures.

Large multinational pharmaceutical companies, including AstraZeneca, Novartis, Pfizer, and GlaxoSmithKline, have systematically divested captive manufacturing assets over the past decade, transitioning to asset-light operating models that rely on preferred CDMO partnerships for OSD commercial production. This structural outsourcing shift is creating a durable and growing demand base for OSD contract manufacturing services that is largely independent of short-term pharmaceutical market cycles.

Restraint - Regulatory Complexity and cGMP Compliance Investment Burden

The market operates under one of the most stringent regulatory compliance frameworks in global manufacturing, with cGMP requirements mandated by the U.S. FDA, European Medicines Agency (EMA), Japan's PMDA, and national regulatory authorities across all major pharmaceutical markets. Maintaining multi-regional regulatory compliance across the FDA, EMA, WHO, and emerging market pharmaceutical regulatory authority standards represents a substantial and growing operational cost burden for OSD CDMOs, requiring continuous investment in quality management systems, analytical equipment, facility upgrades, personnel training, and regulatory intelligence capabilities.

The FDA warning letters and import alerts directed at OSD manufacturing facilities, particularly those located in India and China, create significant market disruption risk for CDMOs serving regulated pharmaceutical markets, with facility remediation programs potentially requiring 12-24 months and tens of millions of dollars in corrective investment.

Opportunity - Continuous Manufacturing Technology Adoption and Industry 4.0 Integration

The pharmaceutical industry's progressive adoption of continuous manufacturing technology for OSD production, driven by FDA encouragement of manufacturing technology modernization through its Emerging Technology Program and pharmaceutical quality systems guidance, represents a transformational commercial opportunity for technically advanced OSD CDMOs. Continuous manufacturing platforms for tablet production, including continuous wet granulation, continuous direct compression, and continuous coating systems, offer significant advantages over traditional batch manufacturing, including reduced material handling, improved process analytical technology (PAT) integration, smaller facility footprint, and lower per-unit production costs at commercial scale.

CDMOs that invest early in continuous OSD manufacturing platforms are positioned to capture a growing share of new product commercialization outsourcing from pharmaceutical companies seeking manufacturing partners with advanced process technology capabilities. The integration of Industry 4.0 technologies, including real-time PAT monitoring, artificial intelligence-driven process optimization, digital batch records, and predictive maintenance systems into OSD manufacturing operations, is creating operational differentiation opportunities for technologically advanced CDMOs to command premium pricing and preferred partner positioning with innovation-oriented pharmaceutical clients.

Category-wise Analysis

Product Type Insights

Tablets are expected to dominate the market by product type, commanding approximately 52% of global revenue in 2026. Their market leadership reflects the universal clinical adoption of tablet dosage forms across virtually all therapeutic categories from cardiovascular and central nervous system drugs to oncology and anti-infective agents, and their established manufacturing economics that enable cost-competitive production at commercial scale under multi-regional cGMP regulatory frameworks.

Capsules represent the fastest-growing product type segment in the OSD contract manufacturing market, driven by their significant formulation flexibility advantages for poorly soluble drug compounds, lipid-based drug delivery systems, and spray-dried amorphous solid dispersions that cannot be effectively formulated as conventional compressed tablets.

Mechanism Insights

Immediate release formulations are expected to dominate the mechanism segment, holding approximately 58% of total revenue in 2026. Their overwhelming market leadership reflects the predominance of immediate-release solid dosage forms across the global pharmaceutical market, encompassing the vast majority of generic drug products, over-the-counter medications, and established branded pharmaceuticals produced in commercial volumes by OSD CDMOs for pharmaceutical clients across regulated and emerging markets.

Controlled release formulations represent the fastest-growing mechanism segment, driven by pharmaceutical companies' focus on improving patient adherence through reduced dosing frequency, extending product lifecycles with modified-release formulations, and enhancing therapeutic outcomes via sustained drug release.

End-user Insights

Large size pharmaceutical companies are anticipated to dominate the end-user segment, commanding approximately 55% of the OSD contract manufacturing market revenue in 2026. Their dominant position reflects the extensive and growing OSD manufacturing outsourcing programs of multinational pharmaceutical companies, including AstraZeneca, Novartis, Sanofi, Pfizer, AbbVie, and GlaxoSmithKline, that have systematically transitioned from captive manufacturing models to preferred CDMO partnership strategies.

Medium and small-sized pharmaceutical companies represent the fastest-growing end-user segment, fueled by the rapid growth of specialty pharmaceutical companies, virtual pharmaceutical companies, and emerging market generic drug manufacturers that rely almost entirely on CDMO partners for OSD manufacturing capability without the capital investment required to establish and maintain in-house manufacturing infrastructure.

Regional Insights

North America Oral Solid Dosage Contract Manufacturing Market Trends

North America is projected to dominate the oral solid dosage contract manufacturing market, holding approximately 38% of the total revenue in 2026, representing the largest regional market globally. The region's market leadership reflects the world's most commercially advanced pharmaceutical industry ecosystem, characterized by the highest per-capita pharmaceutical expenditure, the largest concentration of innovative and generic pharmaceutical companies, and a robust regulatory framework that drives consistent demand for FDA-regulated cGMP OSD contract manufacturing services.

U.S. Oral Solid Dosage Contract Manufacturing Market Insights

The U.S. represents the single largest national OSD contract manufacturing market globally, driven by the enormous scale of U.S. pharmaceutical consumption, the extensive outsourcing strategies of U.S.-headquartered multinational pharmaceutical companies, and the structural demand from the U.S. generic pharmaceutical industry for FDA-compliant tablet and capsule manufacturing.

Canada Oral Solid Dosage Contract Manufacturing Market Insights

Canada's market is characterized by a well-regulated pharmaceutical manufacturing environment operating under Health Canada GMP standards that are closely harmonized with FDA and ICH pharmaceutical quality guidelines. Canadian OSD CDMOs benefit from their geographic proximity to the U.S. pharmaceutical market, regulatory environment compatibility with FDA requirements, and growing integration with North American pharmaceutical supply chains.

Europe Oral Solid Dosage Contract Manufacturing Market Trends

Europe represents the second-largest regional market, accounting for approximately 29% of global revenue in 2026. The European OSD contract manufacturing market is characterized by a highly sophisticated regulatory environment governed by EMA GMP guidelines, national medicines agency oversight, and EU Good Manufacturing Practice Directive requirements that support a well-developed CDMO ecosystem serving both domestic European and international pharmaceutical clients.

Germany Oral Solid Dosage Contract Manufacturing Market Trends

Germany is the leading European OSD contract manufacturing market, underpinned by its position as Europe's largest pharmaceutical market by consumption and production value, its concentration of global pharmaceutical companies including Boehringer Ingelheim, Merck KGaA, and Bayer AG, and the country's advanced pharmaceutical manufacturing infrastructure. Germany's strong expertise in pharmaceutical formulation development, particularly in modified-release technologies and bioavailability enhancement, is driving increased OSD contract manufacturing demand from European and global pharmaceutical companies seeking specialized capabilities.

U.K. Oral Solid Dosage Contract Manufacturing Market Trends

The U.K. market is shaped by the Medicines and Healthcare products Regulatory Agency (MHRA) GMP regulatory framework, the strategic outsourcing priorities of major U.K.-headquartered pharmaceutical companies, including AstraZeneca and GSK, and the growing specialty pharmaceutical sector. Post-Brexit regulatory developments have increased the complexity of pharmaceutical supply chain management between the U.K. and EU, creating opportunities for U.K.-based CDMOs that can offer domestic MHRA-regulated manufacturing services for the U.K. market while maintaining EU GMP certification for the European market supply.

Asia Pacific Oral Solid Dosage Contract Manufacturing Market Trends

Asia Pacific is projected to be the fastest-growing regional OSD contract manufacturing market, driven by cost-competitive manufacturing cost structures in India and China, rapidly expanding pharmaceutical markets across Southeast Asia, and growing regulatory compliance capabilities enabling Asia Pacific CDMOs to serve regulated pharmaceutical markets in North America and Europe.

India Oral Solid Dosage Contract Manufacturing Market Trends

India is the dominant market in Asia Pacific, driven by the country's position as the world's largest generic pharmaceutical producer by volume, an enormous cost-competitive OSD manufacturing infrastructure spanning hundreds of WHO-GMP and FDA-inspected facilities, and the global pharmaceutical industry's well-established sourcing relationships with Indian CDMOs for regulated market-compliant tablet and capsule manufacturing.

China Oral Solid Dosage Contract Manufacturing Market Trends

China's market is growing rapidly due to the expanding domestic pharmaceutical industry, strong government support, and improving regulatory compliance. Enhanced GMP standards by the NMPA are strengthening manufacturing quality and helping Chinese CDMOs compete more effectively in global contract manufacturing markets.

Competitive Landscape

The global oral solid dosage contract manufacturing market is characterized by intense competition among a diverse universe of CDMOs ranging from large, vertically integrated global contract manufacturing platforms to specialized regional CDMOs with focused OSD manufacturing capabilities and niche formulation technology expertise.

Catalent Inc. maintains a leading position in the global OSD contract manufacturing market through its comprehensive OSD technology platform encompassing OptiMelt hot-melt extrusion, GPEx cell line development integration, Zydis fast-dissolve technology, and commercial-scale modified release tablet and capsule manufacturing across its global network of FDA and EMA-approved facilities. Lonza's Dosage Form Services division offers integrated small molecule and OSD manufacturing from active pharmaceutical ingredient synthesis through finished dosage form production, providing pharmaceutical clients with a fully integrated CDMO solution for tablet and capsule products.

Key Industry Developments:

- In March 2026, Forma Life Sciences, Inc. launched as an independent, operator-owned contract development and manufacturing organization (CDMO), specializing in oral solid dosage formulation development, clinical manufacturing, and commercial drug product manufacturing across the United States. The company expanded its service portfolio to support pharmaceutical clients with end-to-end drug product development and manufacturing solutions.

- In August 2025, Piramal Pharma Solutions and NewAmsterdam Pharma opened a dedicated oral solid dosage (OSD) suite at Piramal’s facility in Sellersville, Pennsylvania. The expansion enhanced the site's development and manufacturing capabilities for a wide range of OSD formulations, improved operational efficiency, and strengthened support for the future commercialization of NewAmsterdam Pharma’s investigational therapy, subject to regulatory approval.

Companies Covered in Oral Solid Dosage Contract Manufacturing Market

- Catalent Inc.

- Lonza

- Aenova Group

- Boehringer Ingelheim International GmbH

- Jubilant Pharmova Limited

- Patheon Pharma Services

- Recipharm AB.

- Corden Pharma International

- Siegfried Holding AG

- Piramal Pharma Solutions

- AbbVie Contract Manufacturing

- Next Pharma AB

Frequently Asked Questions

The global oral solid dosage contract manufacturing market is projected to reach US$11.1 billion in 2026.

The oral solid dosage contract manufacturing market is primarily driven by the pharmaceutical industry's accelerating shift toward asset-light outsourcing strategies, growing demand for complex OSD formulations requiring specialized CDMO expertise, expanding generic pharmaceutical market volumes, and cost-efficiency imperatives driving pharmaceutical companies toward contract manufacturing partnerships for tablet and capsule production.

The oral solid dosage contract manufacturing market is poised to witness a CAGR of 9.1% from 2026 to 2033.

Key opportunities include continuous manufacturing technology adoption, enabling operational cost reduction and quality improvement, emerging market pharmaceutical growth creating new CDMO demand in Asia Pacific and Latin America, and growing specialty OSD formulation demand driving premium-priced contract manufacturing services for bioavailability enhancement and controlled release drug delivery systems.

Key players include Catalent Inc., Lonza, Aenova Group, Boehringer Ingelheim International GmbH, Jubilant Pharmova Limited, Patheon Pharma Services, Recipharm AB, Corden Pharma International, Siegfried Holding AG, Piramal Pharma Solutions, AbbVie Contract Manufacturing, and Next Pharma AB.