Comprehensive Snapshot of Luxury Watches Market Including Regional and Country Analysis in Brief.

Industry: Consumer Goods

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 188

Report ID: PMRREP33558

According to Persistence Market Research, the global luxury watches market is poised for significant growth, projected to rise from USD 45,007.0 million in 2025 to USD 61,190.1 million at a CAGR of 4.5% by 2032. This is driven by the rising disposable incomes, evolving consumer preferences, and the appeal of luxury watches as both status symbols and investment assets.

Leading brands such as Rolex, Patek Philippe, and Omega are driving innovation through material advancements, intricate dial artistry, and expanded collections to cater to collectors and enthusiasts. Luxury watchmakers are embracing bold design transformations, incorporating vibrant dials, transparent casebacks, and intricate embellishments. Rolex’s Day-Date 40 with a slate ombré dial and Patek Philippe’s Cubitus collection with a square-shaped case highlight this trend.

The growing demand for women’s luxury watches is shaping market strategies, as seen in Patek Philippe’s expansion of the Twenty~4 collection. Digital platforms and authentication services are further strengthening the secondhand market, with rare timepieces appreciating due to limited supply.

The industry’s focus on limited editions, heritage craftsmanship, and innovation ensures continued market relevance. As consumer preferences evolve, luxury watchmakers are poised to sustain steady expansion through design excellence and strategic market positioning.

Key Industry Highlights :

|

Market Attribute |

Key Insights |

|

Market Size (2025E) |

US$ 45,007.0 Mn |

|

Projected Market Value (2032F) |

US$ 61,190.1 Mn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

4.5% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

3.5% |

Companies are scaling their production, expanding retail presence, and reviving historic brands to strengthen their position in an evolving industry. Rolex made a significant investment with a new manufacturing facility in Bulle, Switzerland, in June 2024, and set to open in 2029. This expansion aims to address the supply-demand gap, following the production of 1.24 million timepieces in 2023 and CHF 10.1 billion ($11.5 billion) in sales. This is expected to accelerate sales for the luxury watches market.

Heritage restoration is gaining momentum as brands capitalize on the rising interest in vintage models. In 2023, Jaeger-LeCoultre’s initiative to offer fully restored vintage watches reflects this shift, preserving historical designs to attract collectors. Strengthening its retail presence, the brand made a grand opening as flagship boutique at WF Central in Beijing on October 1, 2024. With a prime location in Wangfujing, the boutique enhances brand prestige and caters to affluent consumers seeking timepieces with rich heritage.

Counterfeit watches remain a major restraint, with over 40 million fakes in circulation annually, surpassing the Swiss watch industry's total production by 25%. High consumer demand for affordable alternatives fuels market growth damaging brand reputation, revenues, and trust. Advanced replication techniques make it harder to differentiate genuine timepieces from high-quality replicas.

Despite anti-counterfeiting technologies such as blockchain and micro-engraving, counterfeiters exploit online marketplaces and unauthorized retailers. Fake timepieces account for 20 to 35% of all counterfeit consumer goods, with flaws in craftsmanship and timekeeping eventually revealing their authenticity. Strict enforcement and consumer education are crucial to maintaining the integrity of the market.

Opportunities in the secondhand market allow brands to drive revenue, strengthen equity, and engage new demographics. Once seen as competition, the resale segment is now perceived as a strategic tool for customer acquisition and investment-driven demand. Leading companies such as Rolex, Audemars Piguet, and Richemont embrace authenticated resale programs to control pricing, ensure authenticity, and reinforce brand prestige.

Rising interest from younger buyers fuels this growth with 54% of Gen Z and younger millennials increasing their watch spending in the past two years. Additionally, 66% of buyers consider resale value a key factor in buying decisions. By leveraging blockchain authentication, AI-driven demand forecasting, and direct resale programs, brands enhance trust, track market trends, and refine supply chain strategies.

Beyond financial gains, the resale market fosters deeper engagement through digital experiences and community-driven initiatives. Online platforms, social media, and user-generated content elevate brand storytelling and exclusivity, positioning watches as both luxury assets and financial investments. As resale platforms become more sophisticated, the proactive integration of first-hand and second-hand strategies will unlock new revenue channels. Investments in NFTs, digital collectibles, and online watch communities will further strengthen the market presence, ensuring long-term growth, relevance and driving better engagement.

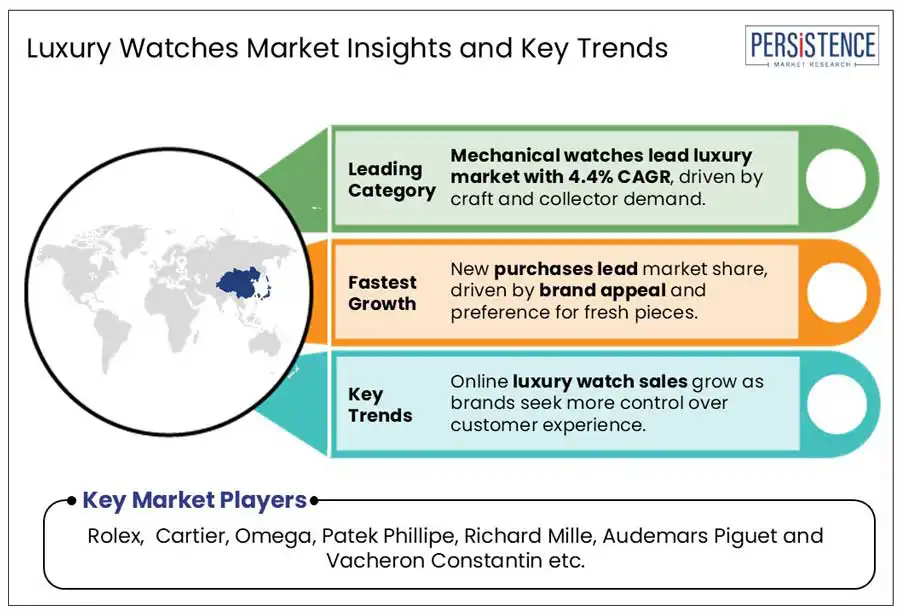

The new purchase type segment is expected to account for a large share in the global market, accounting for 68.2% in 2024. The luxury watches market is witnessing strong demand for high-complication timepieces, driven by collectors valuing craftsmanship and exclusivity.

Brands such as Patek Philippe and Rolex are introducing advanced complications and premium materials to enhance appeal. Limited-edition launches, such as Breitling’s redesigned Avenger collection, further strengthen market differentiation. As innovation and heritage remain central, intricate horological advancements continue to drive industry growth.

The online store dominates the luxury watches market, contributing 29.3% to overall sales in 2024, driven by the growing shift toward direct-to-consumer (DTC) strategies. Luxury watch brands are heavily investing in e-commerce and omnichannel experiences to meet evolving consumer demands.

Online watch sales will surpass $6 billion, accounting for 10-15% of premium to ultra-luxury watch sales. This shift has led brands to reclaim control over customer relationships, with $2.4 billion in annual revenue expected to shift from retailers to watchmakers. Zenith exemplifies this trend, achieving 50% of its sales through DTC channels by 2020. While online sales continue to surge, in-store experiences remain vital, as 90% of Chinese consumers still consider brand boutiques a key purchase influence.

Europe holds 30.2% global share driven by a strong legacy of craftsmanship, technological advancements, and premium brand positioning. Switzerland remains the epicenter, with iconic brands like Rolex, Patek Philippe, and Richard Mille continuously innovating to cater to evolving consumer preferences. The region benefits from a robust network of luxury retailers and a growing demand for exclusive timepieces among high-net-worth individuals. Recent investments in production capacity and acquisitions by key brands further strengthen Europe’s dominance.

East Asia accounts for 32% global share driven by strong consumer demand, cultural appreciation for craftsmanship, and a rising base of high-net-worth individuals. China, Japan, and South Korea are key contributors, with a growing interest in both heritage brands and contemporary designs.

Regional expansion by major players, strategic brand collaborations, and exclusive boutique openings further strengthen market growth. Innovation in materials and high complications continue to attract collectors, solidifying the region’s significance.

The global luxury watches market is fairly consolidated, with only a handful of players commanding a significant portion of the market share. The top five companies—Rolex, Patek Philippe, Audemars Piguet, Cartier, and Omega collectively hold around 55% of the market.

Manufacturers are actively diversifying their offerings to appeal to collectors and luxury enthusiasts. Rolex is strengthening its market position through exclusive product launches and capacity expansion, while Patek Philippe focuses on technical sophistication and aesthetic refinement. This competitive landscape highlights a focus on brand prestige, innovation, and strategic partnerships to sustain dominance in the luxury watch market.

|

Attribute |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2024 |

|

Market Analysis |

US$ Mn for Value Unit of Volume |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Mechanism

By Price Range

By Purchase Type

By Distribution Channel

By Region

To know more about delivery timeline for this report Contact Sales

The market is projected to witness a CAGR of 4.5%, growing from US$ 45,007.0 Million in 2025 to US$ 61,190.1 Million by 2032.

Mechanism segment to captured a share of 44.5% in 2024.

East Asia is poised to dominate the market during the forecast period.

Europe captured a significant share of 29.9% in 2024.

The top manufacturers include Rolex, Richard Mille, Cartier, Omega, Audemars Piguet, Patek Phillipe, IWC Schaffhausen, which are the leading participants in the Global Market.