- Medical Devices

- Lower Limb Prosthetics Market

Lower Limb Prosthetics Market Size, Share and Growth Forecast, 2026-2033

Lower Limb Prosthetics Market by Product (Prosthetic Foot, Prosthetic Knee, Prosthetic Leg), Technology (Conventional Lower Extremity, Electric-powered Lower Extremity, Hybrid Lower Extremity), End-user (Hospitals, Clinics), and Regional Analysis for 2026 - 2033

Lower Limb Prosthetics Market Share and Trends Analysis

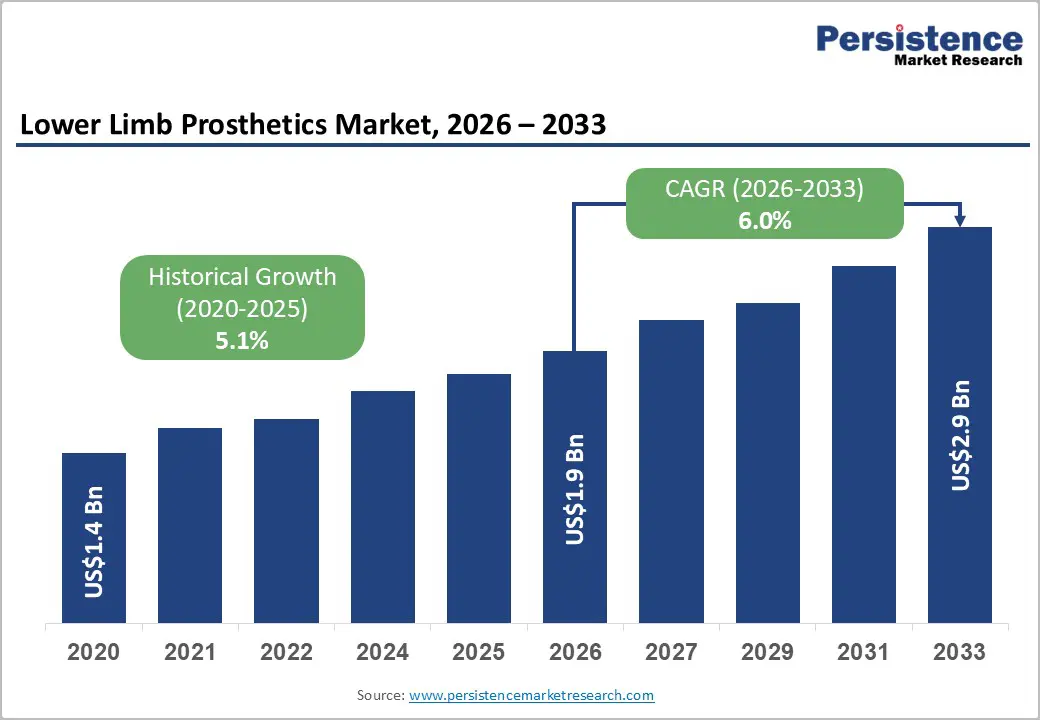

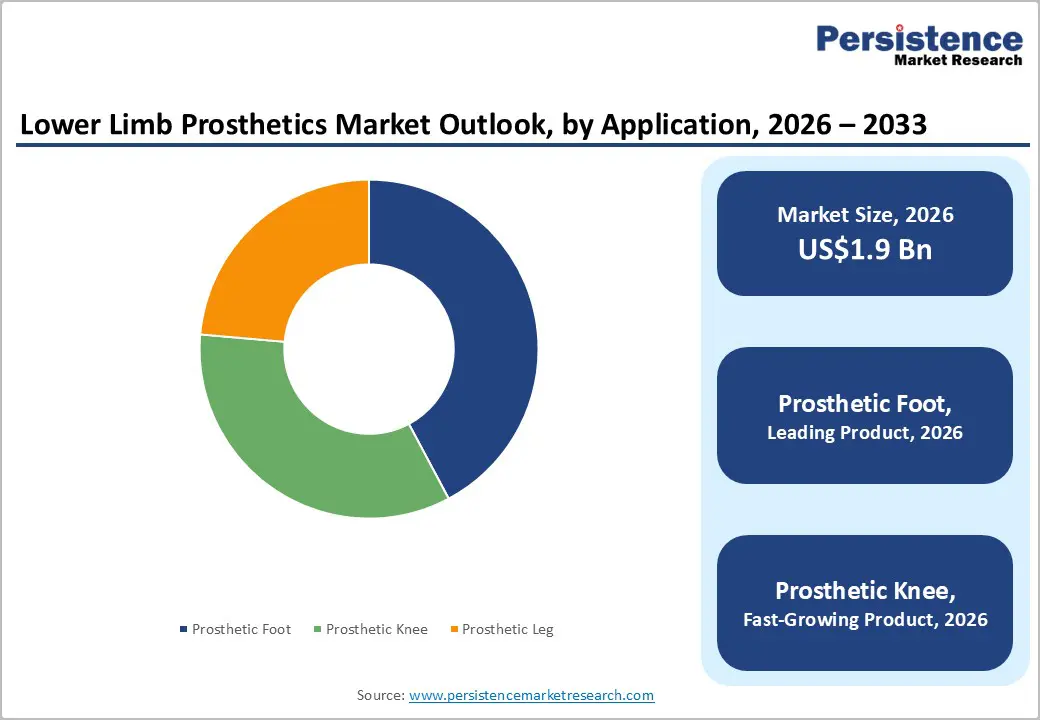

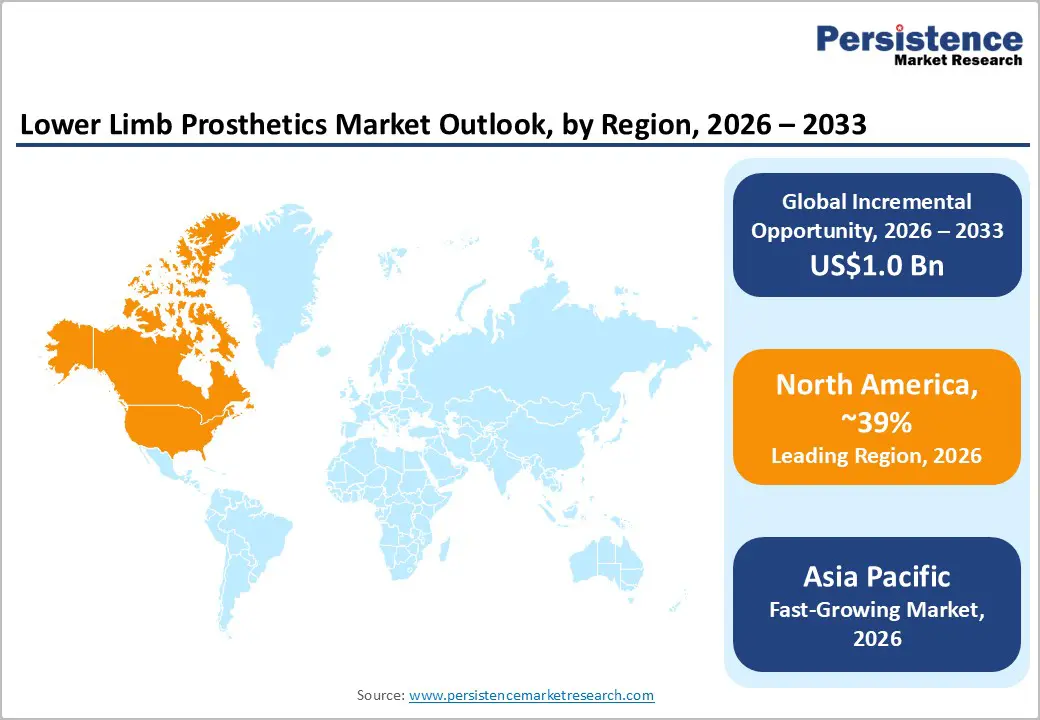

The global lower limb prosthetics market size is likely to be valued at US$1.9 billion in 2026 and is projected to reach US$2.9 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by growing healthcare expenditure, wider adoption of advanced prosthetic devices, and continuous innovation in microprocessor-controlled prosthetics.

Public reimbursement support in developed economies and increasing rehabilitation infrastructure in emerging countries continue to improve patient access to lower extremity prosthetics. In parallel, manufacturers are investing in lightweight materials, sensor integration, and AI-enabled gait technologies to improve mobility outcomes and long-term patient comfort.

Key Industry Highlights:

- Dominant Market Drivers: Rising diabetic amputations, traumatic injuries, and aging populations continue to drive demand for advanced lower limb prosthetics, supported by expanding rehabilitation access and smart mobility adoption.

- Leading Product Segment: Prosthetic foot is projected to lead with around 42% market share in 2026, while prosthetic knee is expected to be the fastest-growing segment at 6.8% CAGR through 2033 due to rising adoption of microprocessor-controlled systems.

- Dominant Technology Segment: Conventional lower-extremity systems are anticipated to dominate with nearly 51% revenue share in 2026, whereas electric-powered lower-extremity prosthetics are likely to record the fastest growth at 7.2% CAGR during 2026–2033.

- Dominant End-user: Hospitals are expected to account for approximately 58% of market revenue in 2026, while clinics are projected to witness the fastest growth through 2033, driven by expanding outpatient rehabilitation services.

- Regional Leadership: North America is poised to dominate with around a 39% share in 2026, supported by strong reimbursement systems, advanced rehabilitation infrastructure, and continuous prosthetic innovation investments.

- Competitive Environment: Competitive dynamics include AI-enabled prosthetics, robotic mobility systems, digital rehabilitation platforms, and strategic expansion across Asia Pacific to strengthen manufacturing and patient access capabilities.

DRO Analysis

Driver - Rising Incidence of Limb Amputations and Mobility-Related Disabilities is Accelerating Demand for Lower Limb Prosthetics

The growing global burden of lower limb amputations remains a major growth driver for the lower limb prosthetics market. Amputations are increasingly associated with diabetes, peripheral vascular disease, road accidents, military injuries, workplace trauma, bone cancer, severe infections, and congenital limb disorders.

According to the International Diabetes Federation, more than 640 million adults are projected to live with diabetes by 2030, increasing the risks of diabetic foot complications and amputations. In parallel, the World Health Organization reports that road traffic injuries continue to cause substantial long-term disabilities globally, particularly in developing economies.

Healthcare providers are expanding rehabilitation infrastructure and prosthetic accessibility programs to improve mobility outcomes and quality of life. Rising adoption of advanced prosthetic devices, improved reimbursement frameworks, and continuous innovation in bionic prosthetics and AI-enabled mobility systems are further accelerating prosthetic adoption across hospitals, rehabilitation centers, and specialty orthopedic clinics.

Restraint - High Prosthetic Device Costs and Limited Reimbursement Access Restrict Large-Scale Adoption

The cost burden associated with advanced prosthetic limb systems continues to limit broader market penetration, particularly in middle-income and low-income countries. Microprocessor-controlled knees and electric-powered prosthetics can cost between US$20,000 and US$70,000, depending on customization and rehabilitation requirements. Additional expenses related to maintenance, socket replacements, alignment adjustments, and physiotherapy further increase the lifetime ownership cost for patients.

Reimbursement policies remain inconsistent across healthcare systems. While North America and parts of Europe provide partial coverage for selected prosthetic technologies, many countries still classify advanced prosthetics as non-essential medical devices. This creates affordability barriers for patients requiring high-performance mobility solutions. Long approval timelines for technologically advanced prosthetics also delay commercialization and increase regulatory compliance costs for manufacturers. These structural limitations may slow adoption rates despite growing clinical demand.

Opportunity - Expansion of Smart Prosthetics, 3D Printing, and Advanced Mobility Devices Creates Long-Term Growth Opportunities

The increasing adoption of AI-enabled prosthetics, robotic mobility systems, and sensor-based gait technologies is creating major growth opportunities in the lower limb prosthetics market. Manufacturers are developing connected prosthetic devices with adaptive movement control, real-time gait monitoring, and remote diagnostics to improve mobility efficiency and rehabilitation outcomes.

The growing use of 3D-printed prosthetics is also improving customization, reducing production costs, and shortening fitting timelines. According to the World Health Organization, more than 2.5 billion people globally require assistive products, while only a fraction currently have adequate access, highlighting substantial unmet demand.

Emerging economies across Asia Pacific, Latin America, and the Middle East are expanding rehabilitation infrastructure and orthopedic care investments. In addition, ongoing developments in osseointegration implants, myoelectric prosthetics, and neural-controlled mobility systems are expected to accelerate the commercialization of next-generation advanced prosthetic devices during the forecast period.

Category-wise Analysis

Product Insights

The prosthetic foot is expected to remain the leading product segment, accounting for nearly 42% of the global market share in 2026. The segment continues to benefit from the growing number of transtibial amputations caused by diabetes, vascular diseases, and traumatic injuries, creating sustained demand for lightweight and energy-efficient mobility systems. Manufacturers are increasingly focusing on carbon-fiber materials, shock absorption, and energy-return technologies to improve gait stability and patient comfort. Reflecting this trend, DRDO and AIIMS Bibinagar introduced India’s first indigenous carbon-fiber foot prosthesis, “ADIDOC,” in 2025, strengthening accessibility to affordable advanced prosthetic devices across emerging healthcare markets.

Prosthetic knee is projected to emerge as the fastest-growing product segment, registering an estimated CAGR of 6.8% through 2033. Growth is being driven by the increasing adoption of microprocessor-controlled knee systems designed to improve balance, gait symmetry, and fall prevention among transfemoral amputees. Rising demand from elderly rehabilitation, military recovery programs, and active lifestyle users is further accelerating segment expansion. In 2025, rehabilitation researchers from the University of Washington reported improved mobility outcomes associated with microprocessor-controlled prosthetic knee systems, reinforcing the growing clinical acceptance of AI-enabled prosthetic technologies.

Technology Insights

Conventional lower extremity prosthetics are anticipated to dominate the market with approximately 51% revenue share in 2026, primarily due to their affordability, durability, and simplified maintenance requirements. These systems remain highly preferred across public healthcare programs and developing economies, particularly for elderly patients and first-time prosthetic users seeking reliable long-term mobility support. Governments and healthcare organizations are also focusing on expanding access to cost-effective prosthetic care. Supporting this trend, India strengthened domestic production of affordable carbon-fiber prosthetic technologies in 2025 under broader healthcare accessibility initiatives.

Electric-powered lower extremity prosthetics are expected to witness the fastest growth, expanding at a CAGR of nearly 7.2% during the forecast period. The segment is gaining momentum as robotic prosthetics, AI-assisted gait systems, and sensor-integrated mobility technologies continue to improve patient independence and movement precision. Demand is particularly increasing among active users requiring adaptive terrain response and real-time motion control. In 2025, Ottobock launched the Taleo Adapt hydraulic prosthetic foot system, highlighting the industry’s growing emphasis on connected mobility technologies and next-generation smart prosthetics.

End-user Insights

Hospitals are projected to remain the leading end-user segment, accounting for around 58% of global market revenue in 2026. The segment benefits from large patient inflow, integrated rehabilitation infrastructure, and access to multidisciplinary orthopedic specialists capable of managing complex prosthetic procedures and long-term recovery programs. Increasing investments in trauma care units and prosthetic rehabilitation centers are further strengthening hospital adoption of advanced mobility systems. In 2025, rehabilitation-focused hospitals in Japan expanded the use of microprocessor-controlled prosthetic systems within structured post-amputation recovery programs to improve patient mobility outcomes.

Clinics are anticipated to emerge as the fastest-growing end-user segment through 2033, supported by rising demand for outpatient rehabilitation and personalized prosthetic care services. Specialized orthopedic clinics are increasingly adopting digital scanning, customized socket fabrication, and rapid fitting technologies to improve patient convenience and shorten rehabilitation timelines. The shift toward community-based rehabilitation models is also expanding access to prosthetic care beyond large hospitals. In 2025, several prosthetic providers across Asia Pacific expanded digitally assisted fitting and rehabilitation services to improve accessibility in semi-urban and rural patient populations.

Regional Insights

North America Lower Limb Prosthetics Market Trends

North America is expected to capture nearly 39% of the global lower limb prosthetics market share in 2026, supported by well-established reimbursement systems, advanced rehabilitation infrastructure, and strong adoption of intelligent mobility technologies. The region continues to experience rising demand for advanced prosthetic devices due to increasing diabetes-related amputations, vascular complications, and trauma injuries. The growing integration of robotic rehabilitation, sensor-enabled prosthetics, and customized 3D-printed solutions is reshaping patient recovery pathways and strengthening long-term market expansion.

U.S. Lower Limb Prosthetics Market Trends

The U.S. is anticipated to contribute close to 82% of the North American market share, primarily driven by its highly developed prosthetic research ecosystem and early adoption of AI-assisted mobility systems. The country is witnessing increasing collaboration between rehabilitation centers, orthopedic specialists, and prosthetic manufacturers to improve patient mobility outcomes and personalized care delivery. Reflecting this momentum, the U.S. Department of Veterans Affairs expanded advanced prosthetic rehabilitation programs for military amputees in 2025, accelerating deployment of microprocessor-controlled prosthetic systems across specialized care facilities.

Canada Lower Limb Prosthetics Market Trends

Canada is estimated to hold around 18% of the regional market share, benefiting from publicly funded healthcare programs and a growing emphasis on patient-focused rehabilitation services. The country is steadily advancing the adoption of digital fitting technologies and precision-based prosthetic customization to improve rehabilitation efficiency and long-term comfort. Building on this trend, Canadian rehabilitation centers increased investments in digitally assisted prosthetic programs in 2025, supporting wider access to modern orthopedic rehabilitation and mobility care solutions.

Europe Lower Limb Prosthetics Market Trends

Europe continues to hold a significant position in the global market, supported by universal healthcare coverage, favorable reimbursement frameworks, and rising demand for technologically advanced mobility solutions. Regional healthcare systems are increasingly prioritizing lightweight composite materials, AI-assisted gait technologies, and sustainable prosthetic manufacturing practices to improve clinical outcomes and patient mobility. Simultaneously, implementation of the European Union Medical Device Regulation is reinforcing product quality standards and strengthening confidence in long-term prosthetic safety and performance.

Germany Lower Limb Prosthetics Market Trends

Germany is projected to account for nearly 30% of the European market share, driven by its strong orthopedic manufacturing base and highly developed rehabilitation infrastructure. The country has emerged as a key innovation hub for adaptive gait systems, smart prosthetic sensors, and digitally connected rehabilitation technologies aimed at improving mobility restoration. In line with this progress, German rehabilitation institutes expanded clinical research programs focused on intelligent prosthetic technologies in 2025 to enhance recovery timelines and long-term rehabilitation efficiency for amputee patients.

U.K. Lower Limb Prosthetics Market Trends

The U.K. is expected to represent approximately 21% of the regional market share, supported by rising investments in disability inclusion initiatives and modernization of rehabilitation services through the National Health Service. Increasing deployment of AI-enabled prosthetic fitting systems and digitally assisted recovery platforms is helping healthcare providers deliver more personalized rehabilitation support. Reflecting this shift, NHS-backed rehabilitation centers expanded use of microprocessor-controlled prosthetic systems in 2025 for trauma and vascular disease patients, strengthening adoption of next-generation mobility technologies across the country.

Asia Pacific Lower Limb Prosthetics Market Trends

Asia Pacific is poised to emerge as the fastest-growing regional market, fueled by expanding healthcare infrastructure, rising diabetes prevalence, and increasing incidence of traumatic amputations. Governments across the region are actively strengthening disability rehabilitation programs, local prosthetic manufacturing capabilities, and assistive mobility initiatives to improve patient accessibility and long-term care delivery. In addition, competitive manufacturing costs and rapidly evolving medical technology ecosystems are encouraging international prosthetic manufacturers to expand their regional presence.

China Lower Limb Prosthetics Market Trends

China is projected to contribute nearly 38% of the Asia Pacific market share, supported by its large patient population and rapidly expanding orthopedic device industry. The country is increasingly modernizing rehabilitation services while integrating AI-powered prosthetic technologies into public healthcare systems to improve mobility outcomes and accessibility. Reflecting this transition, Chinese medical technology companies accelerated development of robotic rehabilitation platforms and intelligent mobility systems in 2025, reinforcing the country’s growing influence in the global smart prosthetics market.

Japan Lower Limb Prosthetics Market Trends

Japan is estimated to account for around 21% of the regional market share, supported by its aging population and longstanding leadership in robotic prosthetics and rehabilitation robotics. Healthcare providers are increasingly incorporating electric-powered lower extremity systems and robotic-assisted gait technologies to enhance mobility precision and reduce rehabilitation burdens among elderly amputees. Supporting this trend, Japanese rehabilitation hospitals expanded integration of microprocessor-controlled prosthetic systems in 2025, further strengthening the country’s focus on technologically advanced and patient-centric mobility care.

Competitive Landscape

The global lower limb prosthetics market is moderately consolidated, with leading companies such as Ottobock, Össur, Hanger, Inc., and Blatchford Group accounting for a notable share of global revenue. These players maintain competitive strength through advanced prosthetic technologies, strong rehabilitation partnerships, and continuous investments in AI-enabled mobility systems and bionic prosthetics. Innovation in microprocessor-controlled knees, robotic prosthetics, and sensor-integrated mobility devices continues to drive product differentiation across premium rehabilitation markets.

Regional manufacturers and specialized prosthetic providers are expanding their presence through customized prosthetic solutions, cost-efficient manufacturing, and digitally assisted fitting technologies. Market entry barriers remain high due to regulatory requirements, R&D intensity, and the technical complexity of advanced mobility systems. However, rising demand for personalized rehabilitation, 3D-printed prosthetics, and smart mobility technologies is creating opportunities for emerging players. Strategic partnerships, regional expansions, and selective acquisitions are expected to further intensify market competition.

Key Industry Developments:

- In May 2026, Ottobock introduced ICONIQ, a digitally manufactured 3D-printed silicone liner designed to improve prosthetic socket fit, comfort, and customization, enabling more precise patient-specific fitting and faster prosthetic alignment workflows.

- In December 2025, first-in-human implantation of RESTORE™ Neuromuscular Interface System

Surgeons at the Medical University of Vienna completed the first human implantation of the RESTORE™ system by Blue Arbor Technologies, enabling neural signal-based prosthetic control with intuitive multi-joint movement capability.

Companies Covered in Lower Limb Prosthetics Market

- Össur

- Ottobock SE & Co. KGaA

- Hanger Inc.

- Blatchford Group

- Fillauer LLC

- WillowWood Global LLC

- Proteor SAS

- Steeper Group

- College Park Industries

- Freedom Innovations

- Endolite India Ltd.

- Alps South LLC

- Bauerfeind AG

- Naked Prosthetics

- Motorica LLC

Frequently Asked Questions

The global lower limb prosthetics market is expected to reach approximately US$1.9 billion in 2026.

Rising amputation cases, increasing trauma incidence, and advancements in electric-powered prosthetic technologies drive the market.

The lower limb prosthetics market grows at a CAGR of around 6% from 2026 to 2033.

Key opportunities include expansion of advanced bionic prosthetics, rising healthcare access in emerging economies, and rehabilitation infrastructure development.

Össur, Ottobock, Blatchford, and WillowWood are key players in the lower limb prosthetics market.