- LED & Lighting (Optoelectronics)

- LED Chips Market

LED Chips Market Size, Share, and Growth Forecast 2026 - 2033

LED Chips Market by Chip Technology (Conventional LED Chips, Mini-LED Chips, Micro-LED Chips), by Semiconductor Material (GaN/InGaN LED Chips, AlGaInP LED Chips, Silicon-based & Other Materials, Other Specialty Materials), Application (General Lighting, Automotive Lighting, Backlighting / Displays, Signs & Signals, Consumer Electronics, Industrial & Specialty Lighting), and Regional Analysis, 2026-2033

Global LED Chips Market Size and Trend Analysis

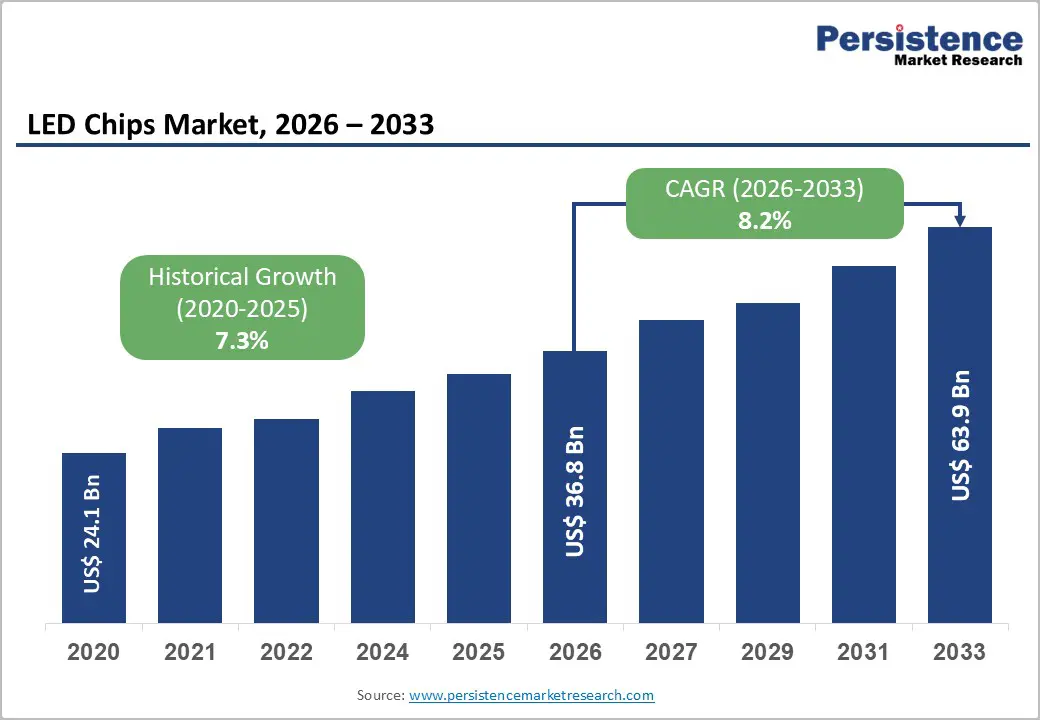

The global LED Chips market size is expected to be valued at US$ 36.8 billion in 2026 and projected to reach US$ 63.9 billion by 2033, growing at a CAGR of 8.2% between 2026 and 2033. Sustained demand momentum is being shaped by the worldwide transition toward energy-efficient solid-state lighting, accelerating adoption of LED-backlit and Mini-LED displays in televisions and notebooks, and expanding penetration in automotive headlamps and ambient lighting.

According to the U.S. Department of Energy, LED installations have already displaced over 47% of conventional lighting sockets in the U.S., while electrification of vehicles and the rapid scale-up of high-resolution video walls are reinforcing chip demand from the GaN and InGaN ecosystems.

Key Industry Highlights:

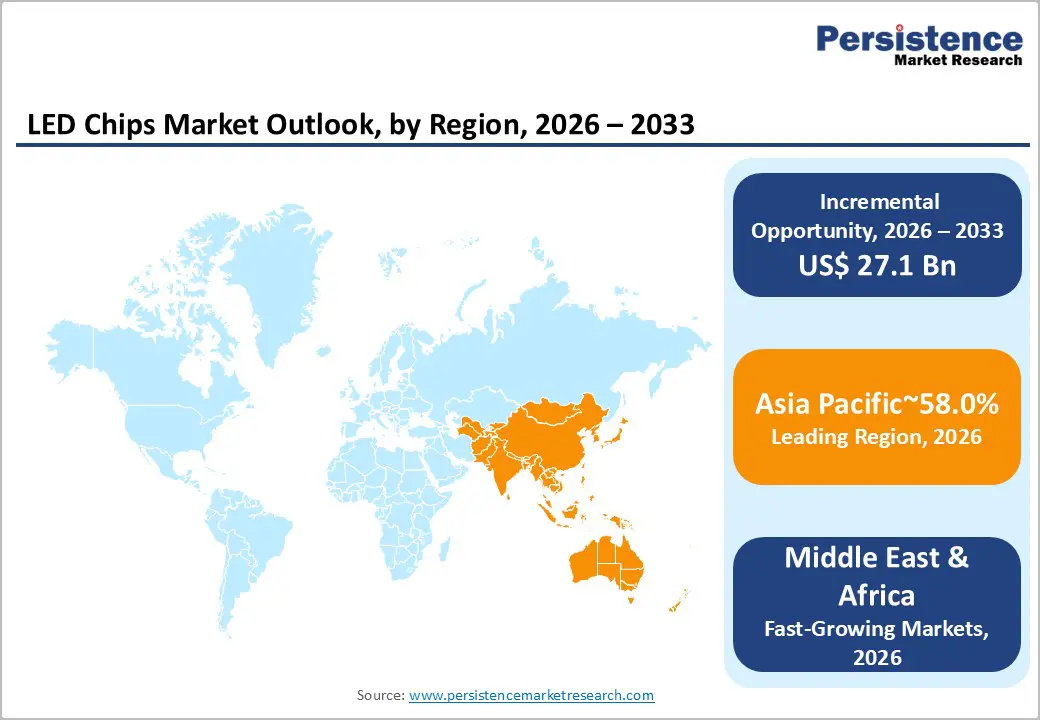

- Leading Region: Asia Pacific dominates with a 58% revenue share in 2025, anchored by China's vertically integrated chip manufacturing ecosystem, dominant Mini-LED TV production, and aggressive deployment of LED-based street lighting and consumer electronics infrastructure.

- Fast-Growing Market: Asia Pacific is also the fastest-expanding region, supported by India's PLI-backed electronics manufacturing push, Southeast Asia's rapid urbanisation, and surging Mini-LED demand across Chinese television OEMs serving global premium display markets.

- Dominant Technology: Conventional LED Chips lead the chip technology category with an 84% market share in 2025, supported by mature production economics, broad application footprint across general lighting, and the lowest cost-per-lumen across solid-state lighting platforms.

- Fast-Growing Technology: Micro-LED Chips represent the fastest-growing technology with a projected 9.3% CAGR between 2026 and 2033, fueled by premium video walls, AR/VR micro displays, and emerging large-format television commercialisation led by Samsung and Sony.

- Key Market Opportunity: Automotive lighting electrification, adaptive matrix headlamps under NHTSA FMVSS No. 108, and horticulture-specific deep-red and UV chips offer high-margin growth pockets for chip manufacturers serving electric vehicles and controlled-environment agriculture.

DRO Analysis

Drivers - Energy-Efficiency Mandates and Phase-Out of Inefficient Lighting

Stringent regulatory frameworks targeting carbon emissions and lighting efficiency are firmly anchoring LED chip demand worldwide. The U.S. Department of Energy estimates that widespread LED adoption could cut national lighting electricity consumption by nearly 75% by 2035, saving approximately 569 TWh annually.

The European Union's Single Lighting Regulation (EU 2019/2020) and the Ecodesign Directive have effectively eliminated halogen and fluorescent lamps from the bloc since September 2023, channelling demand toward LED-based luminaires. Similarly, India's UJALA scheme has distributed over 368 million LED bulbs, while China's Green Lighting Programme continues to enforce minimum efficacy thresholds. These structural policy shifts are converting legacy lighting sockets into recurring demand pools for LED chip manufacturers, especially within the GaN-on-sapphire value chain.

Adoption of Mini-LED and Micro-LED in Premium Displays

Display manufacturers are aggressively migrating from edge-lit LCDs toward Mini-LED backlight units to deliver higher contrast and HDR performance. Apple Inc. has integrated Mini-LED panels across the iPad Pro and MacBook Pro product lines, with each panel embedding more than 10,000 LED chips, while Samsung Electronics and TCL have made Mini-LED a standard feature in their premium QLED and Q-series televisions.

According to industry shipment trackers, Mini-LED TV shipments crossed 6.5 million units in 2024, more than doubling the prior-year volume. Micro-LED, though early in its commercialisation curve, is gaining traction in luxury video walls and AR/VR microdisplays, with Samsung's "The Wall" series and Sony's Crystal LED portfolio expanding the addressable opportunity for high-density chip manufacturers.

Restraints - Volatile Pricing and Wafer Substrate Cost Pressures

LED chip producers continue to grapple with pricing volatility tied to sapphire and silicon carbide wafer costs, electricity tariffs, and rare-earth phosphor inputs. Average selling prices for mid-power LED chips have eroded by an estimated 8–12% annually over the last decade due to oversupply from Chinese epi-wafer foundries, compressing gross margins for Tier-1 producers.

The Taiwan Semiconductor Industry Association has flagged that thin-margin commoditised chip lines are being replaced or shuttered as players pivot to higher-value Mini-LED and automotive segments, slowing top-line momentum across the conventional category.

Technical Complexity and Yield Challenges in Micro-LED Mass Transfer

The commercialisation of Micro-LED technology is hindered by mass-transfer yield, defect inspection, and colour uniformity issues that drive up production costs significantly. According to the IEEE Electron Devices Society, transferring tens of millions of sub-50-micron chips onto a single backplane with placement accuracy below ±1.5 µm remains a critical bottleneck, with current yields well below mass-production economics.

The absence of standardised inspection protocols and the limited availability of high-throughput pick-and-place equipment continue to delay broader rollout into mainstream television and smartphone displays.

Opportunities - Automotive Lighting, Electrification, and Adaptive Driving Beam Systems

The transition toward electric and autonomous vehicles is creating a high-margin opportunity for LED chip suppliers serving automotive OEMs. According to the International Energy Agency (IEA), global electric car sales surpassed 17 million units in 2024, with each modern vehicle integrating between 80 and 200 LEDs for headlamps, daytime running lights, signaling, and interior ambient lighting.

Adaptive Driving Beam (ADB) and matrix headlight systems approved in the United States in 2022 under NHTSA FMVSS No. 108 use thousands of individually addressable Mini-LED pixels per headlamp module. Premium automakers, including Audi AG, BMW Group, Mercedes-Benz, and Hyundai Motor Company, have already commercialised digital matrix headlamps, while emerging players in China and India are following suit, opening a sustained pipeline for high-brightness automotive-grade chips compliant with AEC-Q102 standards.

Horticulture and Specialty Lighting Applications

LED chips tuned to specific photosynthetically active radiation (PAR) wavelengths are powering the rapid build-out of indoor vertical farms and greenhouse cultivation systems. The Food and Agriculture Organisation (FAO) has estimated that global vertical farming output is expanding at double-digit annual rates, with operational facilities concentrated in North America, the Netherlands, Japan, and the United Arab Emirates.

Speciality deep-red (660 nm) and far-red (730 nm) chips, alongside UV-A and UV-C disinfection chips deployed in HVAC and water treatment systems, present a high-margin niche where manufacturers, including OSRAM Licht AG (ams OSRAM) and Seoul Semiconductor, have launched dedicated horticulture portfolios. Demand from food security programs, pharmaceutical-grade controlled environment agriculture, and post-pandemic disinfection mandates is reinforcing the long-term opportunity for application-specific chip designs.

Category-wise Analysis

Chip Technology Insights

Conventional LED Chips dominate the global LED chips market with an estimated 84% revenue share in 2025, anchored by their entrenched role across general illumination, signage, indicator lamps, and entry-level backlighting applications. The category benefits from mature epitaxy and packaging processes, abundant production capacity across China, Taiwan, and South Korea, and the lowest cost-per-lumen profile in the industry.

According to the U.S. Department of Energy's Solid-State Lighting Program, LED luminous efficacy in commercial conventional chips has crossed 220 lm/W, narrowing the performance gap with niche technologies while retaining cost leadership. Standardized GaN-on-sapphire wafer platforms, well-established AEC-Q101 automotive certifications, and robust supply chains supporting outdoor, residential, and industrial luminaires reinforce the segment's leadership across both developed and emerging markets.

Semiconductor Material Analysis

GaN/InGaN LED Chips lead the semiconductor material category with an estimated 63% market share in 2025, owing to their superior efficiency in producing blue and green emissions and their foundational role in white-light LED architectures based on phosphor down-conversion. The material system underpins virtually all general lighting, mobile display backlights, and automotive front-lighting modules.

According to research published by the IEEE Photonics Society, InGaN quantum-well structures deliver internal quantum efficiencies above 80% for blue emission, supporting both high-brightness illumination and Mini-LED backlight applications. The maturity of GaN-on-sapphire and emerging GaN-on-silicon wafer platforms commercialised by manufacturers such as Nichia Corporation, Cree LED (SMART Global Holdings), and Sanan Optoelectronics has further reinforced the dominance of nitride-based chemistry across the value chain.

Application Insights

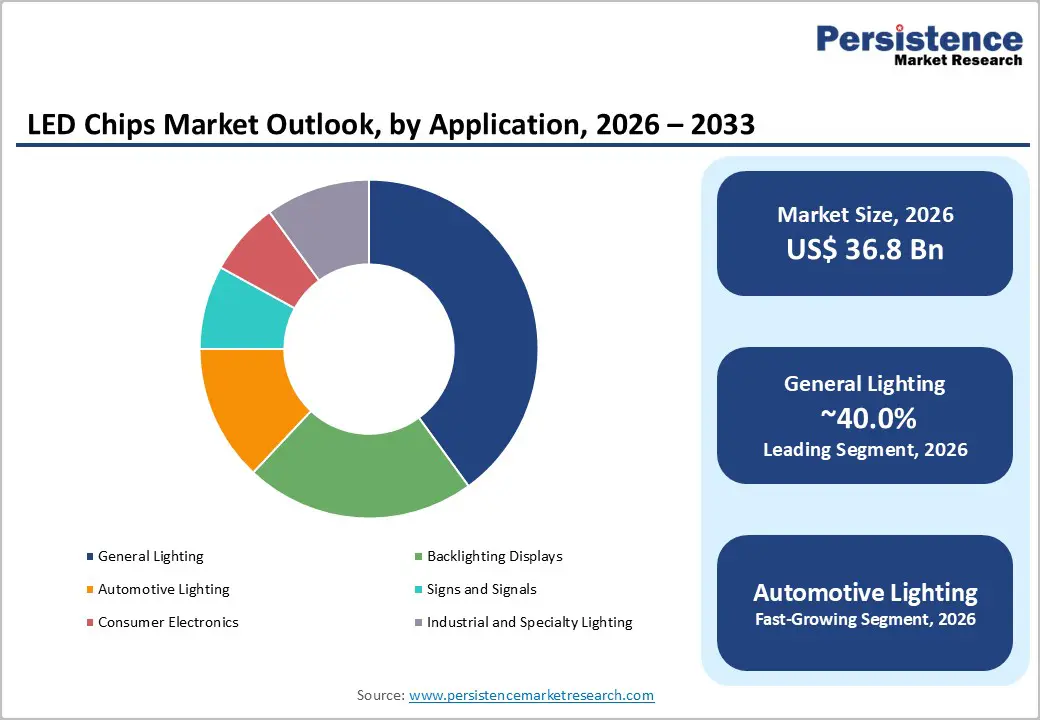

The general lighting segment leads the application category with an estimated 41% market share in 2025, supported by widespread retrofitting of incandescent and fluorescent installations across residential, commercial, and municipal infrastructure.

According to the International Energy Agency (IEA), LEDs accounted for more than 50% of the global lighting market by sales in 2023, up from less than 5% a decade earlier, underscoring the structural shift in lighting demand. Smart-city street lighting programs, including India's Street Lighting National Programme (SLNP), which has retrofitted over 13 million conventional streetlights with LEDs, alongside the EU's mandatory phase-out of fluorescent tubes under the RoHS Directive, continue to anchor demand. The proliferation of connected lighting platforms, occupancy-based dimming, and tunable-white luminaires in office and hospitality settings further sustains the segment's leadership.

Regional Insights

North America LED Chips Market Trends and Insights

North America holds a share of 17.0% in 2025, supported by strong demand from commercial retrofits, premium display manufacturing, automotive front-lighting, and policy-driven energy-efficiency mandates. The region benefits from federal incentives under the Inflation Reduction Act (IRA) and DOE Solid-State Lighting Program investments, alongside accelerating Mini-LED adoption in premium consumer electronics produced by Apple Inc. and other domestic OEMs.

U.S. LED Chips Market Size

The U.S. LED Chips market value stands at US$5.1 billion in 2025, driven by aggressive municipal streetlight retrofits funded under the Energy Efficiency and Conservation Block Grant (EECBG) Program, mandatory federal building lighting upgrades under Section 433 of the Energy Independence and Security Act, and rising integration of Mini-LED backlights in laptops, tablets, and high-end televisions. Strong demand from Tesla Inc., Ford Motor Company, and General Motors for advanced automotive matrix lighting further amplifies chip consumption.

Europe LED Chips Market Trends and Insights

Europe holds a share of 15.0% in 2025, propelled by the bloc's mandatory phase-out of fluorescent lamps under the Ecodesign Directive and RoHS revisions, coupled with the deep penetration of LED chips in German and French automotive lighting modules. Premium luminaire manufacturers and stringent CE efficacy thresholds underpin steady demand across both architectural and infrastructure projects.

Germany LED Chips Market Size

The German LED Chips market value stands at US$ 1,530.0 Million in 2025, driven by the country's powerhouse automotive lighting sector led by HELLA GmbH & Co. KGaA, OSRAM Licht AG, and Marelli, which supply matrix and laser headlamp modules to Volkswagen AG, BMW Group, and Mercedes-Benz Group AG. Industrial automation upgrades and Industrie 4.0–linked smart factory lighting deployments reinforce sustained chip demand.

U.K. LED Chips Market Size

The U.K. LED Chips market value stands at US$ 765.0 Million in 2025, driven by the UK Net Zero Strategy mandating decarbonization of public buildings, the Public Sector Decarbonisation Scheme (PSDS) financing LED retrofits worth over £2.5 billion, and aggressive deployment of horticultural lighting in commercial greenhouses across Kent and Lincolnshire. Smart-city projects in London and Manchester further strengthen connected LED lighting infrastructure demand.

Asia Pacific LED Chips Market Trends and Insights

Asia Pacific holds a share of 58% in 2025, anchored by China's manufacturing dominance through Sanan Optoelectronics, HC SemiTek, and Changelight, alongside strong demand from Taiwanese display fabs and Japanese automotive OEMs. The region houses over 70% of global LED epitaxy capacity, and rising Mini-LED adoption across Chinese television brands such as TCL and Hisense continues to reinforce regional leadership.

China LED Chips Market Size

The China LED Chips market value stands at US$11.8 billion in 2025, driven by massive domestic capacity expansion under the "Made in China 2025" initiative, the world's largest streetlight retrofit program covering more than 28 million luminaires, dominant Mini-LED TV manufacturing for global brands, and aggressive vertical integration across MOCVD reactor ownership by Sanan Optoelectronics and HC SemiTek.

India LED Chips Market Size

The India LED Chips market value stands at US$2.2 billion in 2025, driven by the UJALA scheme distributing over 368 million LED bulbs, the Street Lighting National Programme (SLNP) retrofitting 13 million streetlights, fiscal incentives under the Production Linked Incentive (PLI) Scheme for white goods and IT hardware, and rising domestic demand from automotive OEMs, including Tata Motors and Mahindra & Mahindra.

Competitive Landscape

The global LED chips market exhibits a moderately consolidated structure, with the top ten manufacturers accounting for an estimated 65–70% of global chip output. Leading players such as Nichia Corporation, OSRAM Licht AG (ams OSRAM), Cree LED, Seoul Semiconductor, Sanan Optoelectronics, and Epistar Corporation are differentiating through proprietary phosphor formulations, automotive-qualified chip platforms, and vertically integrated MOCVD capacity.

Strategic emphasis is shifting toward Mini-LED and Micro-LED capacity expansion, GaN-on-silicon wafer migration to reduce production costs, and licensing partnerships with display OEMs. Capacity rationalisation in conventional chip lines, alongside R&D investments exceeding 8–10% of revenue at top players, reflects the industry's pivot toward high-value speciality applications.

Key Developments:

- In Feb 2026, Cree LED, a Penguin Solutions brand, announced the launch of OptiLamp™ LEDs, a next-generation LED chip technology that integrates driver electronics and intelligence directly into each LED pixel, marking a significant advancement in integrated LED display architecture.

- In Oct,2025, Nichia Corporation, a global leader in LED chip manufacturing and inventor of high-brightness blue and white LEDs, announced the development of a next-generation high-power UV-C LED light source technology designed to accelerate the transition toward mercury-free industrial and environmental applications.

Companies Covered in LED Chips Market

- Nichia Corporation

- ams OSRAM AG (including OSRAM Opto Semiconductors)

- Cree LED

- Lumileds Holding B V

- Samsung LED

- Seoul Semiconductor Co Ltd (including Seoul Viosys)

- Epistar Corporation (Ennostar Group)

- Sanan Optoelectronics Co Ltd

- Everlight Electronics Co Ltd

- Toyoda Gosei Co Ltd

- LITE ON Technology Corporation

- Bridgelux Inc

- Luminus Devices Inc

- ROHM Co Ltd

- Stanley Electric Co Ltd

Frequently Asked Questions

The global LED Chips market is projected to reach a value of US$ 36.8 billion in 2026 and is expected to grow to US$ 63.9 billion by 2033, expanding at a CAGR of 8.2% during the forecast period.

Key demand drivers include stringent energy-efficiency mandates such as the EU Ecodesign Directive, accelerating Mini-LED and Micro-LED adoption in premium displays by Apple Inc. and Samsung Electronics, and rising automotive matrix headlamp deployment under NHTSA FMVSS No. 108.

Asia Pacific leads the global LED Chips market with a commanding 58% revenue share in 2025, supported by China's dominant chip manufacturing ecosystem, Taiwan's display fabrication strength, and rapidly expanding electronics production capacity across India and Southeast Asia.

Automotive lighting electrification, adaptive driving beam systems, and specialty horticulture and UV-C disinfection LED chips represent the most significant opportunities, supported by 17 million annual electric vehicle sales and rapid vertical farming expansion globally.

Key market players include Nichia Corporation, OSRAM Licht AG (ams OSRAM), Cree LED, Seoul Semiconductor, Samsung Electronics, LG Innotek, Epistar Corporation, Sanan Optoelectronics, HC SemiTek, and Lumileds Holding B.V., among others.