- Food Packaging

- Nano-enabled Packaging Market

Nano-enabled Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Nano-enabled Packaging Market by Technology Type (Active Packaging and Intelligent / Smart Packaging), Application (Shelf-Life Enhancement/Barrier Improvement, Antimicrobial Packaging, Smart Monitoring & Sensing, and Anti-Counterfeiting & Traceability), Packaging Format (Flexible Packaging, Rigid Packaging), Industry (Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics, Consumer Electronics, and Others) and Regional Analysis for 2026 - 2033

Nano-enabled Packaging Market Size and Trends Analysis

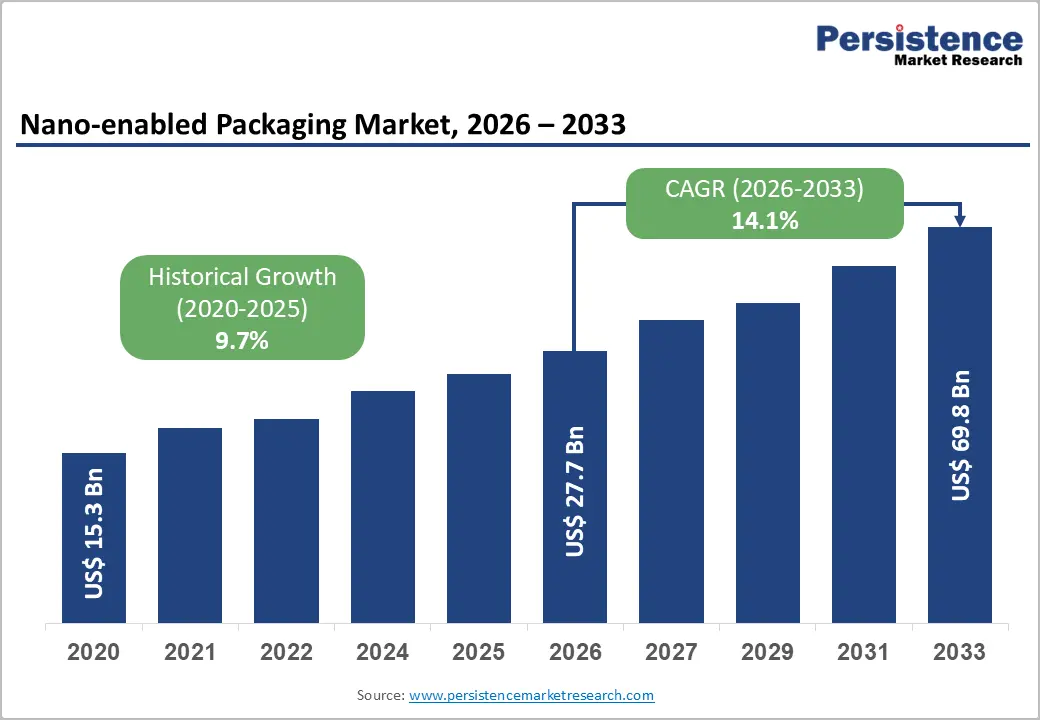

The global nano-enabled packaging market is likely to be valued at US$ 27.7 billion in 2026 and is projected to reach US$ 69.8 billion by 2033, growing at a CAGR of 14.1% during the forecast period. This substantial growth trajectory reflects the rise in demand for advanced preservation technologies, heightened regulatory emphasis on product safety, and the sector's strategic pivot toward sustainable packaging solutions.

Driven by nanotechnology innovations in barrier enhancement, antimicrobial protection, and intelligent monitoring systems, the market is positioned to transform how manufacturers across food, pharmaceuticals, and consumer goods sectors address shelf-life extension, product authenticity, and supply chain transparency. The expansion from US$ 15.3 billion in 2020 to US$ 69.8 billion by 2033 represents a compound evolution addressing critical industry challenges such as food waste mitigation, pharmaceutical stability assurance, and consumer safety verification.

Key Industry Highlights:

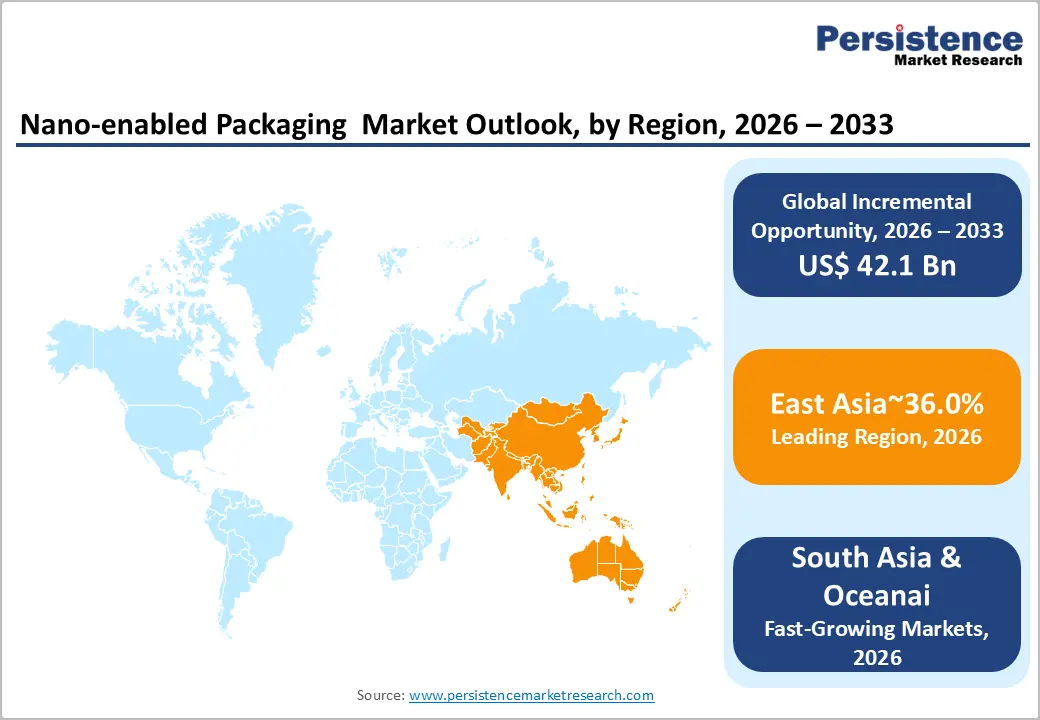

- Regional Leadership: North America leads the global nano-enabled packaging market with 24% share, driven by mature regulatory frameworks, high-cost manufacturing favoring advanced technologies, and strong demand from the food, beverage, and pharmaceutical sectors.

- High-Growing Region: East Asia holds 28% share and is the fastest-growing region, fueled by large-scale manufacturing, rapid urbanisation, electronics production, and government-led Industry 4.0 initiatives.

- Leading Technology Segment: Active packaging dominates with 72% market share, reflecting widespread use of antimicrobial, oxygen-scavenging, and controlled-release barrier mechanisms across food, beverage, and pharmaceuticals.

- Fastest-Growing Technology Type: Intelligent (smart) packaging is the fastest-growing segment, driven by IoT integration, real-time monitoring, and regulatory mandates for cold-chain traceability and product authentication.

- Key Growth Drivers: Extended shelf-life solutions reducing food waste, temperature- and moisture-stable pharmaceutical packaging, and nanosensor-enabled cold-chain and supply-chain visibility are primary market growth drivers.

| Key Insights | Details |

|---|---|

|

Nano-enabled Packaging Market Size (2026E) |

US$ 27.7 Bn |

|

Market Value Forecast (2033F) |

US$ 69.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.7% |

Market Dynamics

Driver - Accelerating Food Waste Reduction Through Extended Shelf-Life Solutions

Food waste represents one of the most pressing global sustainability challenges, with the United Nations estimating that one-third of food production is lost or wasted annually. The Nano-enabled Packaging Market directly addresses this crisis through advanced barrier technologies. Nanoclay-integrated polymer composites, particularly montmorillonite (MMT) based systems, reduce oxygen transmission rates by 10-100 times compared to conventional polymeric films, fundamentally extending product freshness.

The European Union-funded NanoPack initiative demonstrated that active nano-enabled packaging films increased bread shelf-life by three weeks, preventing premature spoilage and directly reducing consumer waste. India's food processing sector, valued at US$ 354.5 billion in 2024 and projected to reach US$ 535 billion by FY26, represents a critical growth nexus where nano-enabled packaging solutions address the sector's dual mandate of food security and waste minimisation.

The Market's trajectory directly correlates with the food and beverage sector's contribution of 8.8 percent to India's manufacturing GVA, underscoring the commercial imperative to adopt advanced preservation technologies. In the United States, where food and beverage manufacturing accounts for 16.8% of total manufacturing sales and employs 1.7 million workers, the adoption of nano-barrier coatings enables manufacturers to meet stringent shelf-life requirements for export markets while reducing logistics-related product loss. These quantifiable shelf-life extensions transform the economic proposition of nano-enabled packaging, converting premium pricing into measurable waste reduction metrics and supply-chain cost savings.

Pharmaceutical Sector Demand for Temperature-Stable, Moisture-Resistant Protection

The pharmaceutical industry's escalating requirement for precise environmental protection constitutes a second material driver of the Nano-enabled Packaging Market. Nanocellulose and nanoclays enhance moisture vapor transmission rates (MVTR) by factors of 10-50x, critical for temperature-sensitive biologics, anti-cancer therapies, and personalised medicine formulations increasingly prevalent in modern pharmacotherapy.

The European healthcare landscape underscores the urgency: the EU faces a shortage of 1.2 million health professionals, while one-third of the EU's population is projected to exceed age 65 by 2050, driving exponential demand for chronic disease medications requiring sophisticated packaging architectures. India's pharmaceutical sector, supported by Ayushman Bharat and Tele-MANAS government initiatives alongside rising foreign direct investments, prioritises cost-effective nano-packaging solutions that maintain drug efficacy without inflating end-user costs. Brazil's healthcare market, valued at US$ 135 billion and serving 51 million private insurance subscribers alongside a universal public healthcare system through ANVISA regulatory oversight, demonstrates the regulatory imperative for packaging solutions ensuring drug stability throughout extended supply chains in tropical climates.

The Market's pharmaceutical segment, identified as the fastest-growing application area, directly reflects this regulatory-driven demand for enhanced barrier properties, tamper-evident integration, and real-time environmental monitoring capabilities that nanotechnology uniquely enables. Controlled-release nanocoating mechanisms reduce antimicrobial leaching while maintaining efficacy, addressing both regulatory safety concerns and pharmaceutical manufacturing economics.

IoT and Cold-Chain Management Integration Enabling Real-Time Supply Chain Visibility

Nanosensor integration within nano-enabled packaging enables unprecedented supply-chain transparency and cold-chain integrity verification. Embedded nanosensors detect temperature fluctuations, humidity changes, and microbial contamination in real-time, interfacing with Internet-of-Things (IoT) platforms and artificial intelligence algorithms to optimize logistics performance and demand forecasting.

The electronics manufacturing sector, which generated US$ 101 billion in FY23 and contributed 3.4percent to India's GDP, increasingly requires sophisticated component packaging with environmental monitoring; the sector's projected growth to US$ 300 billion by FY26 necessitates packaging solutions ensuring product integrity through complex global supply chains.

The market's convergence with Industry 4.0 infrastructure transforms packaging from passive containment to active data-generation nodes, enabling pharmaceutical manufacturers, food producers, and consumer electronics firms to respond dynamically to supply-chain disruptions, optimise inventory management, and verify product authenticity. This functionality becomes commercially indispensable as regulatory mandates increasingly require traceability documentation and environmental impact verification. The market's ability to integrate nano sensor data with blockchain-based supply chain records addresses both regulatory compliance and brand protection imperatives, positioning nano-enabled packaging as strategic infrastructure rather than commodity procurement.

Restraint - Manufacturing Scale-Up and Quality Control Complexity

While nanotechnology offers superior barrier properties through optimal exfoliation and dispersion morphologies, commercial production at scale introduces significant cost pressures and quality variability. The achievable barrier improvements documented in laboratory settings, i.e., oxygen transmission rates below instrument detection thresholds at 51 nm thickness via layer-by-layer assembly, remain difficult to replicate consistently in high-volume manufacturing environments. Polymer-nanoclay nanocomposite (PCNC) barrier properties demonstrate acute sensitivity to organic modifier chemistry, d-spacing uniformity, degree of exfoliation, and processing parameters such as extrusion methodology variables that introduce cost premiums of 20-40% relative to conventional polymers.

The pharmaceutical industry's stringent stability testing requirements often mandate 36 months under accelerated conditions, mandate extended validation periods for nano-enabled packaging materials, delaying market entry and escalating R&D expenditure. These manufacturing and validation hurdles particularly constrain smaller packaging firms and developing-economy manufacturers, thereby fragmenting the Nano-enabled Packaging Market among capital-intensive producers and limiting price-driven market penetration in price-sensitive segments.

Opportunities - Bio-based Nanomaterials and Circular-Economy Packaging Innovation

The convergence of sustainability mandates, Extended Producer Responsibility (EPR) regulations, and consumer preference for eco-friendly packaging creates a substantial opportunity for bio-based nano-enabled solutions. Nanocellulose derived from agricultural waste, cellulose nanocrystals (CNCs), and chitosan-based nanoparticles offer exceptional barrier properties while maintaining complete biodegradability, addressing the structural limitation of petroleum-derived nanocomposites that have persisted in landfills for centuries.

The market's sustainability convergence with global circular-economy frameworks enables premium pricing and regulatory preference. Amcor's investment in Nfinite Nanotechnology's smart nanocoatings specifically targets recyclable and compostable substrates, demonstrating the commercial viability of bio-based nano-packaging architectures. The January 2025 Amcor-Berry Global merger and accompanying AmFiber Performance Paper patent signal industry-wide recognition that bio-based nano-packaging represents the next-generation competitive standard. Regulatory developments, including the EU's Single-Use Plastics Directive and India's Plastic Waste Management Rules, create market preference for packaging solutions demonstrating complete recyclability alongside enhanced functionality.

The opportunity extends to developing nanocellulose composite systems that simultaneously enhance mechanical strength, barrier performance, and biodegradation rates, creating a competitive advantage through cost-neutral sustainability compliance.

Personalized Pharmaceutical Packaging and Precision Medicine Integration

The pharmaceutical industry's accelerating transition toward personalized medicine treatments tailored to individual patient genomics, biomarkers, and therapeutic trajectories creates demand for customized micro-packaging solutions with unprecedented precision and stability characteristics. Nanotechnology enables controlled-release mechanisms through engineered nanoparticle surface chemistry, permitting exact dosage administration and reducing adverse event incidence. Temperature-responsive nanocoatings can maintain pharmaceutical stability within narrow thermal windows throughout extended supply chains, particularly critical for biopharmaceuticals, monoclonal antibodies, and emerging cell-based therapies requiring ultra-cold logistics infrastructure.

The market opportunity encompasses diagnostic integration: nano-enabled packaging incorporating biosensors can monitor patient compliance, therapeutic efficacy through biomarker detection in transdermal patches or inhalation devices, and medication stability throughout the treatment course. This functionality transforms packaging from passive containment to active therapeutic partners, enabling digital health integration and real-world evidence generation. Regulatory pathways for these integrated solutions remain nascent but are evolving through FDA accelerated pathways and EMA scientific advice mechanisms.

The opportunity particularly benefits pharmaceutical companies developing high-value, low-volume therapies where packaging innovations justify premium manufacturing investments and where precision and safety represent competitive imperatives rather than commoditised attributes. India's rising pharmaceutical sector prominence, supported by cost-competitive manufacturing and global export markets, positions the nation to emerge as a leader in personalised-medicine packaging innovation.

Category-wise Analysis

Technology Type Insights

Active packaging represents the dominant technology paradigm, commanding 72% of the 2026 nano-enabled packaging market. This dominance reflects the segment's maturity, commercial scalability, and broad applicability across food, beverage, and pharmaceutical sectors. Active nano-enabled packaging systems incorporate antimicrobial agents such as silver nanoparticles, metal oxide nanoparticles including TiO2 and ZnO), oxygen scavengers, and controlled-release preservative mechanisms directly into packaging matrices or surface coatings. The segment's market leadership derives from quantifiable shelf-life extensions exemplified by the NanoPack initiative's three-week extension for bread products that deliver measurable return-on-investment for food manufacturers and retailers managing spoilage-related losses.

While active packaging dominates current market share, intelligent (smart) packaging represents the fastest-growing segment, driven by IoT integration, real-time monitoring capabilities, and regulatory mandates for supply-chain traceability. Intelligent nano-enabled packaging incorporates nanosensors detecting temperature fluctuations, humidity changes, oxygen levels, and microbial contamination, interfacing with mobile applications and supply-chain management platforms to provide real-time product status visibility.

Industry Insights

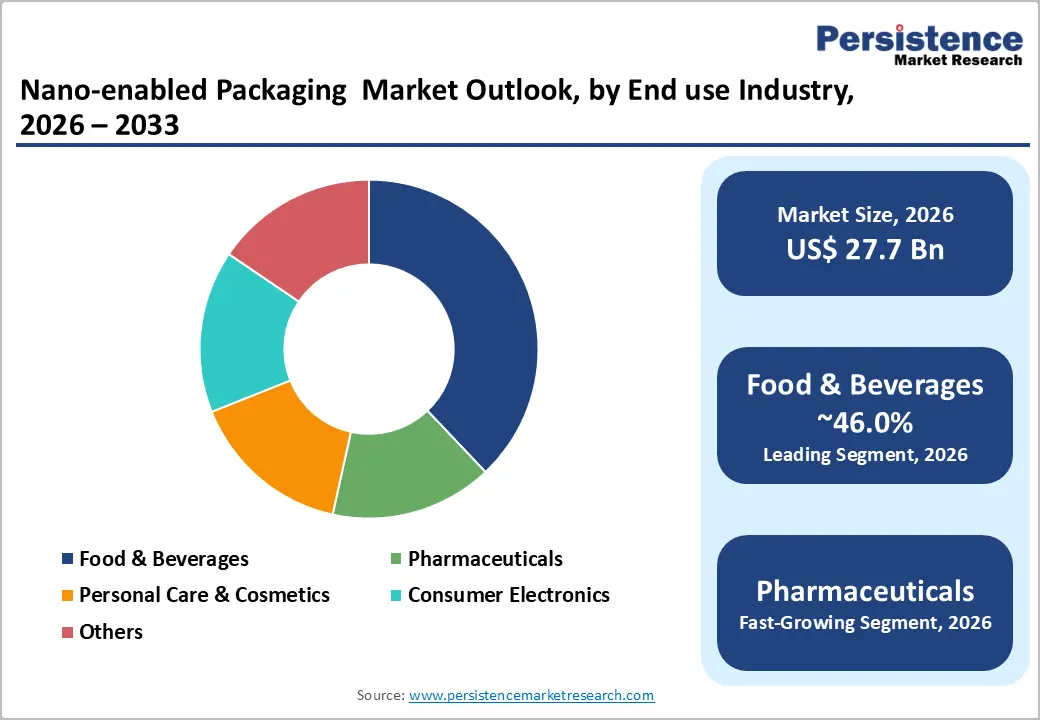

The food and beverage sector dominates nano-enabled packaging adoption at 46% market share, reflecting the sector's substantial scale, stringent shelf-life requirements, and acute economic sensitivity to spoilage-related losses. The sector's dominance encompasses diverse applications: oxygen barriers for carbonated beverages and shelf-stable juices, antimicrobial coatings for fresh-cut produce and prepared foods, and intelligent monitoring systems enabling real-time contamination detection throughout cold-chain distribution.

The European food services sector, employing 10.9 million people and generating €280.7 billion in value added (2022), demonstrates the economic scale justifying investment in advanced packaging technologies. The sector's labour-intensive structure and compressed margins create a competitive incentive for technologies reducing spoilage-related waste and extending distribution window for prepared foods.

India's food processing sector, valued at US$ 354.5 billion (2024) and projected at US$ 535 billion (FY26), represents a critical growth market where nano-enabled packaging enables SME manufacturers to compete in international markets through superior product stability and extended shelf-life relative to conventional packaging. Government initiatives, including 41 Mega Food Parks, extensive cold-chain expansion, and PLI allocations exceeding Rs. 1,400 crores, create infrastructure supporting nano-packaging adoption across India's fragmented food manufacturing landscape.

The pharmaceutical sector, though currently a smaller adopter of nano-enabled packaging, is the fastest-growing segment due to regulatory focus on stability, cold-chain integrity, and anti-counterfeiting. Growth is driven by temperature-sensitive biologics, stricter supply-chain monitoring mandates (FDA, EMA, ANVISA), and rising counterfeiting risks. India, with initiatives like Ayushman Bharat and Tele-MANAS and US$13.4 B FDI (2000–2025), is emerging as a hub for nano-enabled pharmaceutical packaging, leveraging cost-competitive manufacturing. Global demand is further supported by Brazil’s US$135 B healthcare market and Europe’s aging population, boosting the adoption of advanced packaging solutions.

Regional Insights and Trends

North America Nano-enabled Packaging Market Trends

North America holds 24% of the global Nano-enabled Packaging Market, characterized by mature regulatory infrastructure, high-cost manufacturing favouring advanced technology adoption, and stringent food safety standards (FDA) and pharmaceutical requirements (FDA, DEA) driving nano-packaging investment. The United States' food and beverage manufacturing sector's 16.8 percentage share of total manufacturing sales and employment of 1.7 million workers reflects the sector's substantial economic scale and competitive sensitivity to shelf-life and food safety innovations. Leading companies, including Amcor, Sealed Air, and Honeywell, have headquartered their North American operations, driving continuous innovation in active and intelligent packaging solutions.

The pharmaceutical sector's concentration in North America, driving regulatory pathways and technology standardization reflects the region's alignment with FDA approval frameworks and intellectual property protection standards, incentivising investment in novel nano-enabled solutions. January 2025 strategic developments, including the Amcor-Berry Global merger forming the world's largest consumer packaging company with a US$ 180 million annual sustainability-focused R&D allocation, signal North America's commitment to maintaining technological leadership.

East Asia Nano-enabled Packaging Market Trends

East Asia commands 28% of the global Nano-enabled Packaging Market, reflecting the region's dominant position in manufacturing scale, supply-chain infrastructure, and food & beverage consumption. China and India's combined population exceeding 2.8 billion, coupled with rapid urbanization and rising processed food consumption, creates unprecedented demand for shelf-life extension technologies. The region's electronics manufacturing concentration particularly semiconductors, smartphones, and consumer electronics requiring sophisticated component packaging generates substantial demand for nano-enabled solutions protecting components throughout complex global supply chains.

The region's government-led strategic initiatives such as China's advanced manufacturing initiatives) create regulatory preference for domestic nano-packaging innovation, enabling rapid technology adoption and manufacturing scale-up. The region's growth trajectory exhibits the fastest acceleration, with nanosensor-enabled intelligent packaging gaining particular traction in cold-chain logistics supporting pharmaceutical and specialty food distribution across geographically dispersed markets with limited infrastructure standardisation.

Europe Nano-enabled Packaging Market Trends

Europe represents 22% of the global market, distinguished by stringent sustainability regulations, regulatory emphasis on nanomaterial safety assessment, and mature market conditions favoring premium-pricing for eco-friendly nano-enabled solutions. The European Union's regulatory framework, including REACH directives, Single-Use Plastics Directive, and Extended Producer Responsibility (EPR) mandates, creates compliance pressures driving adoption of sustainable nano-enabled packaging solutions offering superior environmental profiles relative to conventional alternatives.

The EU's circular-economy strategic initiatives and Green Deal objectives create policy-driven preference for nano-enabled packaging, demonstrating complete recyclability and measurable waste reduction. Europe's highly fragmented food manufacturing landscape (2.0 million enterprises employing 10.9 million workers in food services alone) creates opportunities for specialised nano-packaging suppliers addressing niche applications and regional market requirements.

Competitive Landscape

The global nano-enabled packaging market exhibits a consolidated structure, with a handful of major companies dominating the landscape due to their advanced technology capabilities, strong R&D investments, and global distribution networks. Amcor, Klöckner Pentaplast, Sealed Air, Tetra Pak International, Sonoco Products Company, and BASF SE are key players driving innovation in nano-coatings, barrier films, and active packaging solutions. These companies leverage strategic partnerships, acquisitions, and continuous product development to maintain competitive advantage.

High entry barriers, such as sophisticated manufacturing processes and stringent regulatory compliance, limit new entrants. Market competition is centered around technological differentiation, sustainability initiatives, and the ability to provide multifunctional packaging solutions. As demand grows for food safety, extended shelf life, and smart packaging, these leading players are likely to further consolidate their position while exploring emerging markets.

Key Industry Developments:

- In November 2025, USDAnalytics reported that the global Nano-Enabled Packaging market is projected to grow from $41.0 billion in 2025 to $126.1 billion by 2034 at a 13.3% CAGR, driven by nanoclay high-barrier coatings, nanosensor-enabled intelligent packaging, and bio-based nanomaterials adoption by companies like Amcor, Sonoco, BASF, Honeywell, and Tetra Pak, enabling reduced food waste, improved cold-chain integrity, and sustainable, regulatory-compliant packaging solutions.

- In April 2023 – Amcor initiated a joint research collaboration with Nfinite Nanotechnology to evaluate ultrathin nanocoatings that add high-performance oxygen barriers to recyclable and compostable packaging. The proof-of-concept focuses on replacing conventional aluminum or silicon oxide vacuum deposition with open-air, high-speed nanocoating processes, improving barrier performance for paper-based and bio-based substrates while supporting cost-effective, scalable nano-enabled packaging solutions.

Companies Covered in Nano-enabled Packaging Market

- Amcor

- Klöckner Pentaplast

- Sealed Air

- Tetra Pak International S.A.

- Sonoco Products Company

- CCL Industries Inc.

- BASF SE

- DuPont Teijin Films

- Avery Dennison

- Checkpoint Systems, Inc.

Frequently Asked Questions

The global nano-enabled packaging market is projected to be valued at US$ 27.7 Bn in 2026.

The Active Packaging segment is expected to account for approximately 72% of the Global Nano-enabled Packaging Market by Technology Type in 2026.

The market is expected to witness a CAGR of 14.1% from 2026 to 2033.

The Nano-enabled Packaging Market growth is driven by advanced barrier technologies extending food shelf-life, regulatory-driven demand for temperature- and moisture-stable pharmaceutical packaging, and IoT-enabled nanosensors providing real-time supply-chain visibility and cold-chain integrity.

Key market opportunities in the Nano-enabled Packaging Market lie in bio-based, circular-economy nanomaterials for sustainable packaging and personalised pharmaceutical packaging integrating nanosensors for precision medicine and real-time patient compliance monitoring.

Key players in the Nano-enabled Packaging Market include Amcor, Klöckner Pentaplast, Sealed Air, Tetra Pak International, Sonoco Products Company, and BASF SE.