Industry: Healthcare

Published Date: March-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 319

Report ID: PMRREP3430

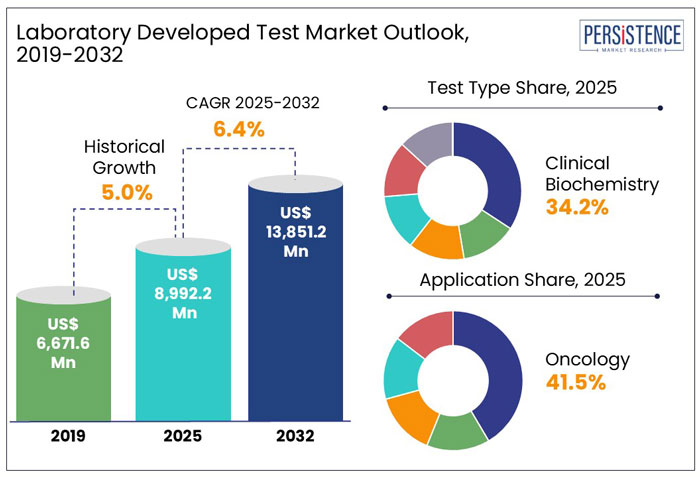

The global market for Laboratory Developed Test is estimated to grow from US$ 9.0 Bn in 2025 to US$ 13.9 Bn in 2032 at a CAGR of 6.4% over the forecast period.

As assessed by Persistence Market Research, clinical biochemistry tests are expected to account for a market value share of 34.2% by 2032. Revenue from laboratory developed tests accounted for around 3.4% share of the global clinical laboratory service market in 2024.

|

Global Market Attributes |

Key Insights |

|

Laboratory Developed Test Market Size (2025E) |

US$ 9.0 Bn |

|

Market Value Forecast (2032F) |

US$ 13.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.0% |

The global laboratory developed test market expanded at 5.0% CAGR from 2019 to 2024.

Factors such as increasing healthcare expenditure on chronic and genetic conditions as well as rising cases of cancer among the population are set to fuel the consumption of laboratory developed tests over the coming years.

Laboratory developed tests are beneficial for the detection and monitoring of oncology, genetics, infections, and autoimmune diseases. These tests are the best option for the population curious about their genetic makeup concerning the presence of any disease-related markers.

Laboratory developed testing offers several advantages such as improved quality of life, monitoring pre-existing conditions, and maintaining one’s lifestyle accordingly, which makes them preferable over hospitalization for daily checkups or the treatment of disease occurrence.

Rising adoption of laboratory developed tests among patients suffering from chronic conditions and genetic disorders will drive the market over the coming years. The global laboratory developed test market size is thus likely to see positive growth and reach a market valuation of US$ 13.9 Bn by 2032.

“Increasing Product Offerings Related to Genetic Health Risks”

Manufacturers of laboratory-designed tests across the world will have plenty of lucrative prospects in the years ahead. They have begun to recognize the value of R&D spending to provide a diversified product line.

Many companies are taking extensive measures to make their product offerings more versatile through innovations, such as providing data related to genetic health risks, ancestry, and traits.

“Rise in Global Number of Cancer Cases”

According to the World Health Organization, cancer is the leading or second-leading cause of death for those over the age of 70 in 112 of 183 nations, and third or fourth in the other 23 countries. In many countries, the rise of cancer as a significant cause of death is reflected in lower death rates from stroke and coronary heart disease when compared to cancer.

How is Laboratory Developed Test Industry Expansion Being Affected?

“Product Recalls Impacting Market Progress”

Recalls of healthcare diagnostic products are a common practice aimed at either reducing any potential errors or eradicating an existing failure. Laboratory developed tests (LDTs) have been developed to treat a variety of disorders, including contagious diseases such as COVID-19, genetic conditions, and different types of cancer.

However, because LDTs, until now, were not centrally registered or tracked, their presence in the market, performance, and usage cannot be compared to FDA-approved diagnostics. Insurance coverage and eHealth do not differentiate between a laboratory-developed test and FDA-approved diagnostics. No comprehensive database of all LDTs exists for use.

“Tight CLIA and FDA Control Over Laboratory Developed Tests”

The Clinical Laboratory Improvement Amendments program (CLIA) governs labs that do tests on patient samples to assure accurate and consistent results. LDT is a test that is developed and used within a single laboratory, according to the FDA.

LDTs are often known as 'home brew' tests because they are produced in-house. LDTs are considered as 'devices', comparable to IVDs, as defined by the FFDCA, and are thus subject to FDA regulation.

The FDA made changes to its laboratory developed tests. Key changes to the agency's policy, according to a statement, were: For all serology test developers, the agency provided clear performance threshold guidelines for specificity and sensitivity.

According to the agency, all test kits should be authenticated before being used, because false outcomes can have a negative impact on both, individual patients and society as a whole. Manufacturers should publish directions for use, including a summary of assay performance on their websites prior to obtaining an EUA.

Why is the North America Laboratory Developed Test Market a Prominent Sector?

“Innovative LDT Development and Commercialization and FDA's Evolving Policies on LDTs”

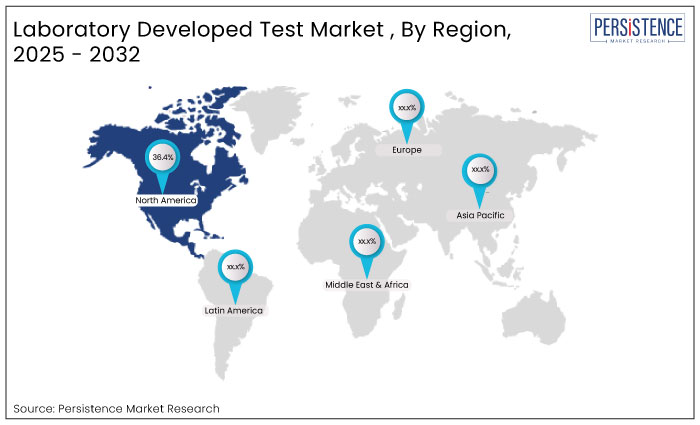

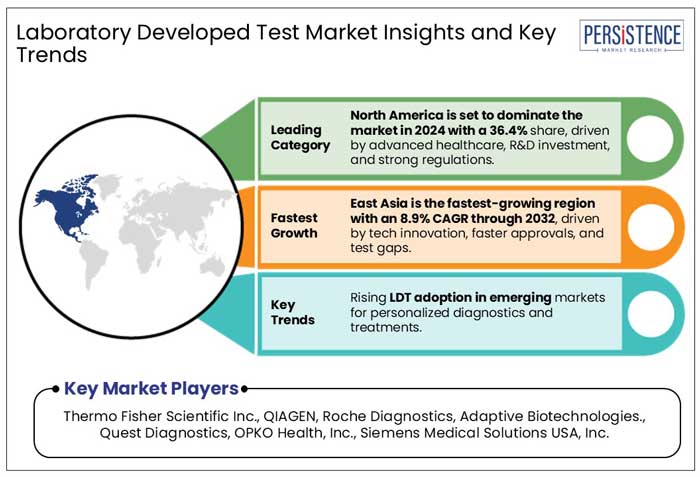

In 2024, North America laboratory developed test market contributed around 36.4% revenue share within the global market. North America’s advanced healthcare infrastructure, a well-established regulatory framework, high levels of investment in biotechnology alongside robust presence of leading biopharma companies, collectively drive growth and innovation of LDTs.

Furthermore, development and commercialization of LDTs in the U.S. have also been promoted locally by regulatory agencies like the FDA which provide clear and supportive guidelines. Rising prevalence of chronic diseases demands for precision diagnostics and personalized medicine, further boosting the adoption of LDTs. Thus, making U.S. laboratory developed test market a key driver for growth in the North American diagnostics industry.

Will Europe Be a Lucrative Market for Laboratory Developed Test Providers?

“Rise in Product Approvals Complying with Stringent Regulations”

Europe laboratory developed test market is estimated to grow at a compounded growth rate of 6.2% CAGR over the forecast duration, owing to rising chances of product approvals by regulatory agencies in the region.

Growing adoption of advanced molecular diagnostics and demand for personalized medicine drives the Germany laboratory developed test market. Enhanced testing capabilities owed to innovations in digital cytogenetics and genomics is expected to boost the Germany LDTs Market in the coming years.

Similarly, UK’s push towards precision medicine is accelerating the adoption of LDTs contributing to a substantial market expansion in the region. Additionally, increasing integration of laboratory-developed tests into routine clinical practices is expected to significantly drive the UK laboratory developed test market.

Why is East Asia Emerging as a Lucrative Market for Laboratory Developed Testing Services?

“Rising Incidence of Diabetes in East Asia Due to Unhealthy Living Choices”

East Asia is the fastest growing market for LDTs growing at a CAGR of nearly 8.9% over the forecast period, driven by improving healthcare infrastructure, rapid technological advancements, and the increasing demand for precision medicine.

Additionally, shorter regulatory approval times facilitates faster LDT adoption. Rising awareness of chronic diseases together with growing demand for personalized diagnostics, further accelerating market expansion. The region's large and diverse population also contributes to a significant need for cost-effective and accurate diagnostic solutions.

Similarly, Japan’s commitment to healthcare innovation, greater emphasis on biotechnology and advanced genetic testing, and the increasing demand for precision medicine is expected to showcase robust growth in the Japan laboratory developed test market.

As showcased above, demand for laboratory-developed tests in East Asian countries like China and Japan is bound to see an upward trend over the coming years, contributing significantly to the overall growth of the East Asia laboratory developed test market.

Which Laboratory Developed Test Type Accounts for Higher Sales?

“Ever-rising Demand for Clinical Biochemistry Tests Being Witnessed”

By test type, clinical biochemistry tests held 34.2% market share at the end of 2024.

Fluids in the body are examined using clinical biochemical testing (blood, abscesses urine, cerebral spinal fluid, and collections in body cavities and joints). They can be used to track the course of disease management in addition to establishing a primary diagnosis. This is the best option for patients to get a basic idea of their illness.

As such, clinical biochemistry test usage is higher, followed by molecular diagnostic tests, and the segment is expected to drive high demand for laboratory tests in the future, globally.

Where is the Application of Laboratory Developed Tests Higher?

“Laboratory Developed Tests Widely Used to Diagnose/Monitor Cancer”

Use of laboratory developed tests for oncology purposes accounted for the highest share of 41.5% in 2024.

Laboratory developed tests can help in the diagnosis of cancer and the monitoring of therapy response. These tests can aid in the diagnosis of cancer recurrence and the assessment of therapy response. Thus, laboratory-derived tests are more widely being used for monitoring the recurrence of cancer to provide early treatment options.

Consolidation activities such as product approval and launches, acquisitions, collaborations, and partnerships are actively looked upon in this market. Such consolidations will help market players expand their product portfolios and increase their market penetration, thereby driving their revenue share in the market.

|

Historical Data/Actuals |

2019 – 2024 |

|

Forecast Period |

2025 – 2032 |

|

Market Analysis Units |

Value: US$ Bn Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Test Type:

By Application:

By End User:

By Region:

To know more about delivery timeline for this report Contact Sales

The market is set to reach US$ 9.0 Bn in 2025.

By test type, clinical biochemistry tests is projected to dominate the global market in 2025.

Thermo Fisher Scientific Inc., Kaneka Eurogentec S.A., QIAGEN, and Roche Diagnosticsare a few leading players.

The industry is estimated to rise at a CAGR of 6.4% through 2032.

North America is projected to hold the largest share of the industry in 2025.