- Automotive

- India Taxi Market

India Taxi Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

India Taxi Market by Booking Type (Online Booking, Offline Booking), Service Type (Ride‑Hailing, Ride‑Sharing/Carpooling, Traditional Taxi Services, Subscription/Corporate Mobility Services), Vehicle Type (Passenger Cars, Two‑Wheelers, Three‑Wheelers, Vans/MPVs), Analysis for 2026–2033

India Taxi Market Trends & Analysis

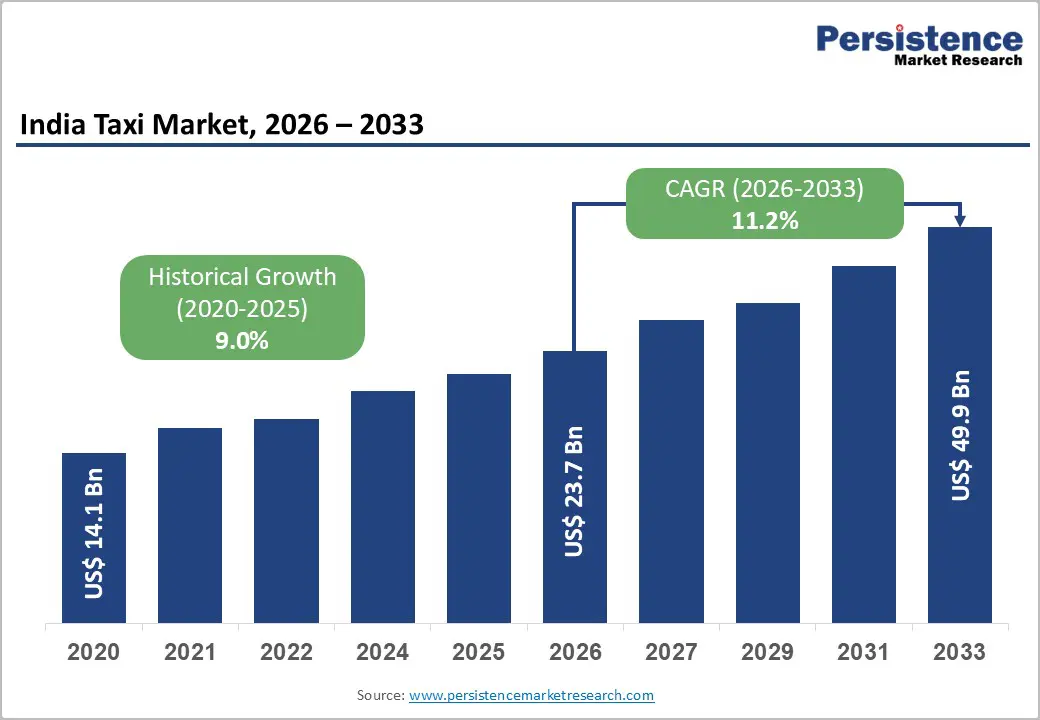

India Taxi Market size is projected at US$ 23.7 billion in 2026 and is projected to reach US$ 49.9 billion by 2033, growing at a CAGR of 11.2% between 2026 and 2033. Independent estimates indicate the market could rise from about US$ 21 Bn in 2025 to over US$ 44 Bn by 2032, implying similar double digit growth for app based and shared mobility services. This growth is driven by rapid urbanization, rising smartphone and internet penetration, and consumer shift toward app based ride hailing and ride sharing. NITI Aayog projects that shared miles could reach 35% of all kilometers travelled by 2030 and 50% by 2040, reflecting a structural move away from private ownership to shared mobility. Government policies such as the Motor Vehicle Aggregator Guidelines 2020 and the proposed 2025 update further shape the digital taxi ecosystem.

Key Industry Highlights:

- Digital Dominance: Online booking accounts for about 78.6% share and is also the fast growing booking mode at roughly 12.9% CAGR, as smartphone penetration and MoRTH aggregator guidelines accelerate app based adoption across metros and Tier 2/3 cities.

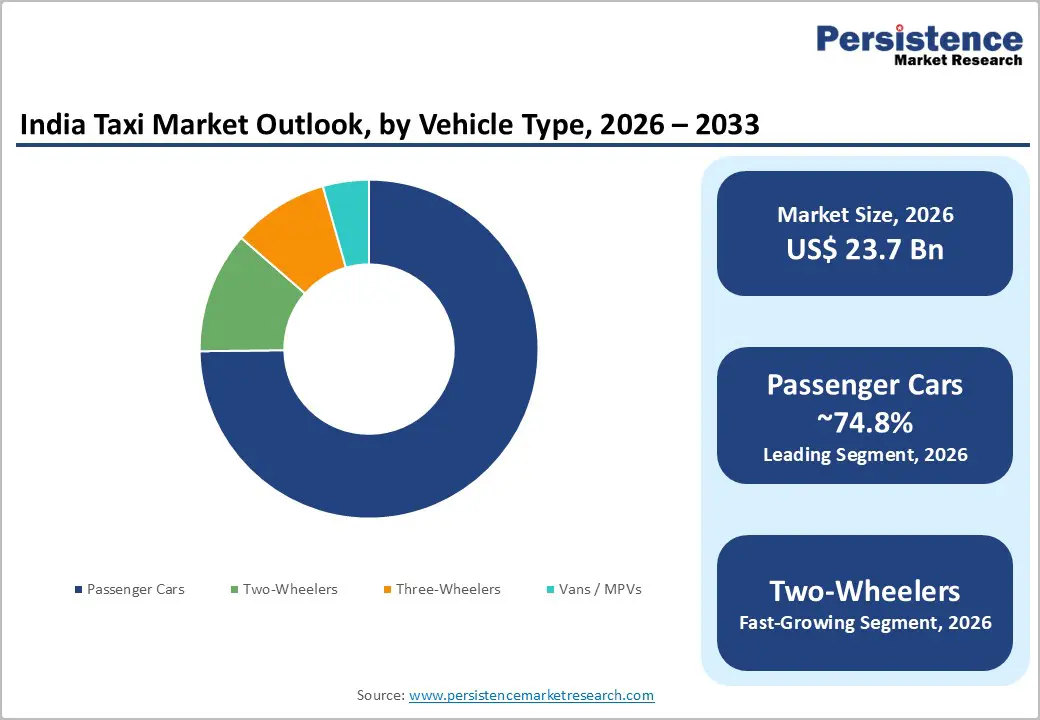

- Service & Vehicle Mix: Ride hailing holds about 68.4% share, while ride sharing / carpooling grows near 13.6% CAGR; Passenger cars contribute ~74.8% of revenues, but two wheelers (bike taxis) are the fast growing vehicle segment at a positive CAGR.

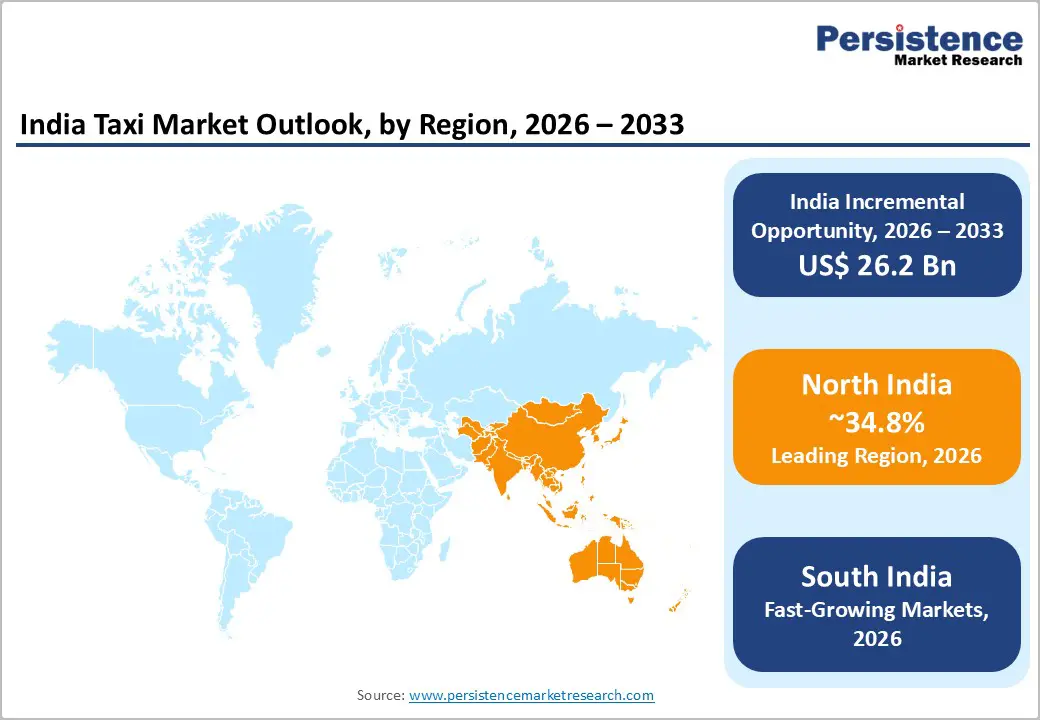

- Regional Leaders: North India leads with 34.8% share, West India holds about 30.1% and grows near 11.5% CAGR, while South India is the fastest growing region at around 12.6% CAGR, supported by tech hubs and open mobility pilots.

- Platform Dynamics: Rapido has emerged as a market share and MAU leader in ride hailing, BluSmart has crossed INR 500 crore ARR with India’s largest EV fleet, and open network models like Namma Yatri are reshaping pricing and driver commission structures.

- Policy & Shared Mobility: NITI Aayog anticipates shared miles reaching 35% by 2030, and MoRTH’s Aggregator Guidelines 2020 and 2025 aim to regulate safety, commissions, and driver welfare, supporting long term growth of ride hailing and ride sharing ecosystems.

- EV & Corporate Mobility: EV only platforms and corporate mobility services are expanding rapidly, with BluSmart targeting 10,000 EVs and corporates increasingly demanding low carbon commute solutions, creating multi billion dollar opportunities in EV fleets, charging and subscription based transport.

Market Dynamics Analysis

Drivers - Digital adoption and app based aggregation

India’s smartphone base exceeded 750 million users by mid 2020s, with low cost data plans enabling mass adoption of app based services, including e-hailing and ride sharing. The Motor Vehicle Aggregator Guidelines 2020, issued by the Ministry of Road Transport & Highways (MoRTH), created a national framework for licensing and regulating app based aggregators, clarifying responsibilities around data, safety and driver earnings. A 2025 guidelines update further strengthened driver protections, mandatory verification and dispute resolution, enhancing trust for both drivers and riders.

As a result, online booking (app based/e hailing) accounts for an estimated 78.6% of India taxi bookings. It is also the fast growing booking segment at about 12.9% CAGR, gradually displacing offline street hail and call based models. Platforms such as Ola, Uber, Rapido, BluSmart, inDrive, Namma Yatri and others have scaled across hundreds of cities, normalizing digital payments, upfront pricing and GPS based routing.

Policy Push for Shared, Electric, and Connected Mobility

NITI Aayog and Rocky Mountain Institute estimate that a shared, electric, and connected mobility paradigm could help India save US$ 60 Bn in fuel costs by 2030, cutting energy use 64% and CO emissions 37% versus business as usual. A dedicated NITI Aayog shared mobility report projects that shared miles could reach 35% of all miles travelled by 2030, supported by ridesharing, pooled services and strong public transit. These findings inform national and state level policies on EV incentives, urban transport, and open digital ecosystems such as ONDC.

EV centric operators such as BluSmart are now running over 7,300 electric cabs with a target of a 10,000 EV fleet in 2024. This demonstrates the feasibility of all electric taxi platforms in dense corridors. State governments, particularly in Delhi NCR, Karnataka, and Telangana, are piloting EV mandates for fleets and aggregators and enabling open, zero commission models such as Namma Yatri on ONDC’s open mobility network, which promotes driver friendly, interoperable ride hailing. These policy and innovation trends create tailwinds for ride hailing, ride sharing, and subscription fleets, especially in North and South India.

Restraints - Regulatory uncertainty and state wise fragmentation

Despite national guidelines, aggregator regulation remains primarily a state subject, leading to divergent rules on fare caps, surge pricing, bike taxis, and commissions across states such as Karnataka, Maharashtra and Delhi. Policy reversals such as temporary bans on bike taxis or differing permit norms create operational uncertainty, delay expansion into certain cities and limit the scalability of uniform business models, impacting growth for two wheeler and three wheeler segments.

Driver Supply, Unit Economics and Service Quality

Driver attrition, fluctuating incentives and rising fuel costs can reduce active driver supply during peak periods, undermining reliability. MoRTH’s Aggregator Guidelines 2025 seek to address concerns around low driver earnings, arbitrary de platforming and lack of social security by mandating training, grievance redressal and transparent commission practices. While necessary for long term sustainability, these measures may compress short term margins and require platforms to rebalance incentives and pricing, creating near term friction in driver acquisition and service levels.

Opportunities - Two wheeler and three wheeler taxis in Tier 2/3 cities

Bike taxi and auto rickshaw aggregation represents one of the highest growth opportunities in India’s taxi market. Rapido, originally a bike taxi specialist, now commands nearly half of India’s ride hailing market by monthly active users, with about 50 million MAUs by mid 2024 compared with Uber’s 30 million, and significant share in four wheeler cabs as well. In parallel, platforms such as Jugnoo and Namma Yatri aggregate auto rickshaws in cities such as Chandigarh and Bengaluru, leveraging open network models and low commissions.

Given India’s large two wheeler and three wheeler base and the relatively low cost of these modes, the Two Wheelers (bike taxis) segment is projected as the fastest growing vehicle type at about 17.4% CAGR, with three wheelers also expanding as e-rickshaw adoption rises in peri urban and semi urban corridors. By 2033, these segments could collectively capture a significant double digit share of market value, particularly in North and South India’s Tier 2/3 cities, while enhancing first /last mile connectivity to metro and bus networks.

EV first and Corporate Mobility Platforms

Operators such as BluSmart Mobility, headquartered in Gurugram, are building EV only ride hailing and charging networks, with more than 7,300 EVs and a target of 10,000 EVs by end 2024. BluSmart’s annual recurring revenue (ARR) surpassed INR 500 crore in FY24, and its cars have driven over 460 million electric kilometres, avoiding an estimated 34 million kg of CO. Similar models from corporate focused providers like Savaari and lithium fleet operators offer dedicated employee transport and intercity services using cleaner vehicles

As ESG mandates tighten and corporate India seeks low emission commutes, subscription / corporate mobility services can capture rising wallet share, especially in IT/ITeS hubs in Bengaluru, Hyderabad, Gurugram and Pune. If EV centric taxi and corporate mobility fleets account for even 10–15% of India’s taxi market value by 2033, this could represent US$ 5–7 Bn in annual revenue, plus significant charging and software as a service opportunities across major urban clusters.

Category wise Analysis

Booking Type Insights

Online booking (App based / E hailing) is the leading booking type, with an estimated 78.6% share of India taxi transactions by value, reflecting widespread smartphone penetration, digital payments and strong aggregator footprints in metros and Tier 2 cities. App based platforms offer upfront pricing, ETA visibility, safety features and ratings, which outperform offline street hail and stand based taxis in terms of convenience and perceived safety.

Offline bookings remain relevant around airports, railway stations and smaller towns but continue to lose share to digital channels across North, South and West India. Offline booking growth is comparatively modest as younger consumers default to apps for both intra city and intercity trips.

Service Type insights

Within service types, Ride Hailing (on demand taxi services) is the leading segment, accounting for roughly 68.4% share of India taxi market value, driven by platforms such as Ola, Uber, Rapido and BluSmart that provide door to door, point to point transport in passenger cars and two wheelers across 250+ cities. Traditional metered and radio taxis have seen a relative decline but still serve airport and corporate contracts, while subscription services remain niche but on a growing curve.

Ride Sharing/Carpooling is the fast growing service type, likely to reach 13.6% CAGR as NITI Aayog’s shared mobility vision and corporate sustainability goals push higher vehicle occupancy and pooled routes. App based platforms are expanding pooled rides, corporate shuttles, and subscription passes, especially in congested corridors in Bengaluru, Delhi NCR, Hyderabad, and Mumbai.

Vehicle Type Insights

Passenger cars (hatchback, sedan, SUV) are the leading vehicle type, with an estimated 74.8% share of taxi market value, reflecting the dominance of four wheeler cabs in airport transfers, corporate travel, intercity trips, and premium on demand rides. Ola, Uber, Meru, Savaari, Red Taxi and BluSmart operate large car fleets across major cities, while cars also underpin most subscription and corporate mobility contracts, particularly in North and West India’s business hubs.

The fast growing vehicle segment is two wheelers (bike taxis), projected at about 17.4% CAGR, driven largely by Rapido’s expansion and the economics of low cost, high frequency rides in densely congested urban areas. Bike taxis offer shorter wait times and lower fares, making them attractive for first /last mile connectivity, student segments, and solo commuters in North, South, and West Indian cities.

Regional Market Insights

North India Taxi Market Trends

North India holds a prominent 34.8% share, anchored by Delhi NCR’s large commuting base, tourism in Rajasthan and Uttarakhand, and strong corporate and government travel demand in Delhi, Haryana and Uttar Pradesh. The Delhi NCR taxi market contributes a multi billion dollar share of national revenues by 2026, with significant volumes from app based ride hailing, airport transfers, and corporate mobility contracts across Delhi, Gurugram, and Noida, supported by metro integration and business travel.

Other key North Indian states, Uttar Pradesh, Haryana, Punjab, and Rajasthan, add substantial demand through Tier 1 and Tier 2 cities such as Lucknow, Kanpur, Chandigarh, Jaipur, and Ludhiana, where growing smartphone penetration and youth demographics drive rapid adoption of bike taxis, autos, and shared cabs.

South India Taxi Market Insights

South India is the fast growing market, with the taxi market value expected to reach 12.6% CAGR, driven by strong IT/ITeS clusters, high digital adoption, and open mobility experimentation in Karnataka, Tamil Nadu and Telangana. States such as Karnataka and Tamil Nadu, with Bengaluru and Chennai as anchors, collectively generate a large and growing share of India taxi revenues, driven by commuter trips, airport traffic, corporate mobility, and growing EV fleets from operators like BluSmart and Namma Yatri linked autos.

Andhra Pradesh, Telangana, and Kerala contribute additional volumes through cities such as Hyderabad, Vijayawada, and Kochi, where ride hailing, bike taxis, and auto aggregation platforms are scaling, supported by relatively progressive state level policies on aggregators and EV adoption.

West India Taxi Market Insights

West India holds around 30.1% share and likely to reach about 11.5% CAGR, reflecting strong demand in Maharashtra and Gujarat, high tourism in Goa, and significant corporate travel in Mumbai, Pune and Ahmedabad. Maharashtra, led by Mumbai and Pune, anchors West India’s taxi market with sizable airport transfers, corporate bookings and app based intra city rides, generating a substantial share of national market revenues by 2026, particularly in the passenger car and bike taxi segments.

Gujarat (Ahmedabad, Surat, Vadodara) and Goa add material demand from business travel, ports, industrial clusters, and tourism, with players such as Red Taxi, Savaari, and regional operators complementing national platforms and offering city centric and intercity services.

Competitive Landscape

India taxi market is concentrated among a few nationwide app based platforms but fragmented across city specific and niche operators, with intensifying competition from bike taxi and EV first players. Key differentiators include network density, dynamic pricing algorithms, driver engagement models, safety features, EV integration and participation in open networks like ONDC’s mobility stack.

Dominant strategic themes include innovation in shared and electric mobility, cost leadership via high asset utilization and lean incentives, and market expansion into Tier 2/3 cities through two wheelers, autos and corporate mobility partnerships, alongside regulatory compliance and enhanced driver and rider protection frameworks.

Key Developments:

- In January 2024, Rapido surpassed Uber in monthly active users in India, reaching about 50 million MAUs vs Uber’s 30 million, driven by bike taxi dominance and expansion into four wheeler cabs, reshaping competitive dynamics in app based ride hailing.

- In April 2024, BluSmart announced crossing INR 500 crore ARR and scaling its all electric fleet to over 7,300 EVs, with a target of 10,000 EVs by end 2024, reinforcing EV centric ride hailing and charging network investments in Delhi NCR and Bengaluru.

- In March 2023, ONDC onboarded Namma Yatri onto its open mobility network, enabling zero commission auto rickshaw rides and supporting open, interoperable ride hailing across Bengaluru and other cities, with plans to extend the model nationally.

- In 2025, MoRTH released updated Motor Vehicle Aggregator Guidelines 2025, strengthening the 2020 framework with enhanced driver protections, mandatory verification, training and greater accountability for app based taxi aggregators such as Ola, Uber and Rapido.

India Taxi Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 14.1 Bn |

|

Current Market Value (2026) |

US$ 23.7 Bn |

|

Projected Market Value (2033) |

US$ 49.9 Bn |

|

CAGR (2026–2033) |

11.2% |

|

Leading Region |

North India - 34.8% |

|

Dominant Service Type |

Ride?Hailing - 68.4% |

|

Top?ranking Booking Type |

Online Booking - 78.6% |

|

Incremental Opportunity |

~US$ 26.2 Bn |

Companies Covered in India Taxi Market

- Ola Cabs

- Uber India Systems Pvt Ltd

- Rapido

- BluSmart Mobility

- Meru Cabs

- Jugnoo

- Namma Yatri

- Mega Cabs

- Savaari Car Rentals

- Red Taxi

- inDrive

Frequently Asked Questions

The India Taxi Market is expected to reach about US$ 23.65 Bn in 2026 and approximately US$ 49.85 Bn by 2033, more than doubling in value over the period.

Growth is driven by rapid urbanization, rising incomes, mass smartphone adoption, app‑based ride‑hailing aggregation, and national policies promoting shared, electric and connected mobility as outlined by NITI Aayog and MoRTH.

From 2026 to 2033, the India Taxi Market is projected to grow at around 11.24% CAGR, in line with independent estimates of roughly 11.2% CAGR over 2025–2032.

Key opportunities include expanding ride‑sharing and pooling, rapid growth in two‑wheeler and three‑wheeler aggregation, EV‑first and corporate mobility platforms, and open‑network models that unlock new price points and business models in Tier‑1 and Tier‑2/3 cities.

Key players include Ola Cabs, Uber India, Rapido, BluSmart Mobility, Meru Cabs, Jugnoo, Namma Yatri, Mega Cabs, Savaari Car Rentals, Red Taxi and inDrive, each with distinct regional footprints, vehicle mixes and service propositions.