Industry: Chemicals and Materials

Published Date: December-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 191

Report ID: PMRREP35022

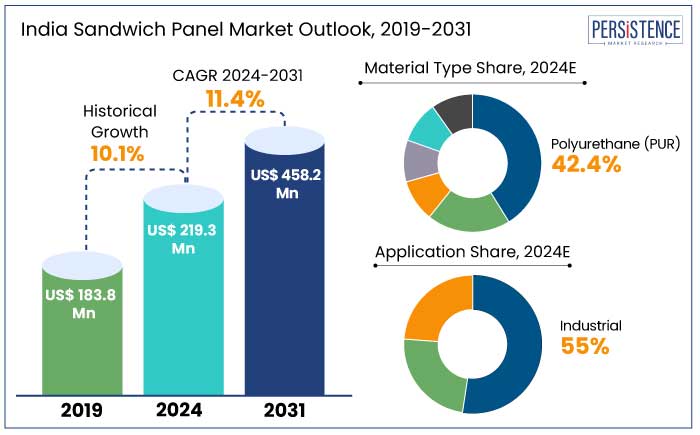

The India sandwich panel market is projected to witness a CAGR of 11.4% during the forecast period from 2024 to 2031. It is anticipated to increase from US$ 219.3 Mn recorded in 2024 to a considerable US$ 458.2 Mn by 2031.

In terms of volume, the market is anticipated to surge from 125,109.3 thousand square feet in 2024 to 231,835.1 thousand square feet by 2031, registering a volume CAGR of 9.2%. This growth is fueled by rising demand for insulated and fire-resistant panels across industrial, commercial, and residential applications.

Infrastructure development initiatives and an increasing focus on energy-efficient construction solutions further boost market expansion. However, the utilization rate is anticipated to gradually decline post-2031 due to market saturation.

The utilization rate of sandwich panels is likely to rise till 2031 and gradually decrease by the end of the assessment year. The country’s market is highly fragmented with key players holding less than 40% of the total share. Several market players are engaging in partnerships and joint ventures to leverage each other’s strengths and extend their geographic presence.

Sustainability is becoming a critical focus for manufacturers. Key players are investing in eco-friendly materials and energy-efficient manufacturing processes to meet the rising demand for green construction solutions, aligning with global environmental standards and regulations.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

India Sandwich Panel Market Size (2024E) |

US$ 219.3 Mn |

|

Projected Market Value (2031F) |

US$ 458.2 Mn |

|

India Market Growth Rate (CAGR 2024 to 2031) |

11.4% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

10.1% |

North India, with a market share of 28.2% in 2024, is anticipated to create new opportunities in the India sandwich panel market. It is set to witness a CAGR of 9.8% through 2031.

Growth is anticipated to be driven by the rapid development of the National Capital Region (NCR). This zone, encompassing Delhi, Noida, Gurugram, Ghaziabad, and Faridabad, serves as an industrial and commercial hub. These mainly host industries like IT, automotive, logistics, and warehousing.

Urbanization, industrial expansion, and real estate booms have created significant demand for insulated construction materials, including sandwich panels. Investments in logistics infrastructure, cold chains, and commercial real estate further fuel this growth. For instance,

The NCR also boasts over 1.2 million tons of cold storage capacity, with anticipated growth supported by e-commerce expansion and government initiatives. Polyurethane (PUR) and Polyisocyanurate panels dominate due to their superior thermal insulation and fire-retardant properties.

West India is anticipated to hold around 26.7% of the India sandwich panel market share in 2024, emerging as another key zone with an estimated CAGR of 12.8% through 2031. It is set to be driven by robust industrial and commercial growth. Urbanization and rising infrastructure projects in cities like Mumbai, Pune, Ahmedabad, and Surat contribute to the increasing demand for sandwich panels.

The zone’s thriving manufacturing, logistics, and warehousing sectors play a pivotal role in this growth. Investments in cold storage and large-scale commercial projects further amplify demand for energy-efficient and durable construction materials.

West India also benefits from its strategic location, supporting export-driven industries and logistics hubs. These developments, coupled with government support for industrial and infrastructure projects, position the zone as a significant market for sandwich panels.

Polyurethane (PUR) leads the market owing to its cost-effectiveness and versatile application in construction. Its lightweight properties make it an ideal choice for projects where reducing structural load is critical. The segment is likely to hold a share of 42.4% in 2024.

Its excellent thermal insulation capabilities contribute to energy efficiency, making it popular in both residential and industrial construction. Builders favor polyurethane for its durability and ease of installation, further driving its adoption.

It is widely used in walls, roofs, and cold storage facilities, supporting a wide range of infrastructure needs. Its adaptability to different climate conditions ensures consistent demand across regions, cementing its position as the most preferred material. Owing to the aforementioned factors, the segment is projected to witness a CAGR of 11.6% through 2031.

The cold storage and refrigeration segment will likely showcase a CAGR of 11.7% through 2031. It is set to be fueled by increasing infrastructure investments and rising need for energy-efficient buildings. The sector has grown significantly due to booming food processing and pharmaceutical industries, which require unique storage solutions.

Cold storage facilities rely heavily on insulated panels to maintain optimal temperatures, making sandwich panels indispensable. Emphasis on reducing energy consumption and carbon emissions further supports demand for high-performance materials. With urbanization and global trade boosting the need for temperature-controlled storage, this segment remains a pivotal driver of market growth.

The India sandwich panel market is gaining traction as industries prioritize lightweight, energy-efficient, and insulated materials to meet sustainability goals and enhance performance. With high demand from the construction, transportation, and cold storage sectors, the market is increasingly shaped by several trends.

A few trends include fire-resistant technologies, eco-friendly manufacturing practices, and government initiatives supporting energy-efficient infrastructure. This dynamic environment is positioning India as a key market for innovative sandwich panel solutions.

Between 2019 and 2023, the India sandwich panel industry demonstrated a steady CAGR of 10.1%. It was driven by rising applications in construction and transportation.

The strong growth trajectory is anticipated to continue, with global sandwich panel sales projected to surge at a CAGR of 11.4% from 2024 to 2031. It will likely be fueled by increasing demand for lightweight insulated materials across industries.

In India, the market mirrors this growing trend, propelled by rapid industrialization, infrastructure development, and rising adoption of energy-efficient construction solutions. Evolving regulatory landscape promoting green building initiatives further underscores the industry’s expansion prospects in the next ten years.

Rising Investments in Infrastructure Projects to Push Demand

India's booming infrastructure sector is significantly accelerating demand for novel building materials such as insulated panels. Rising industrial and infrastructure projects across the country is pushing the need for construction materials that offer durability, insulation, and efficiency. For example,

The constant surge in large-scale projects is creating a robust demand for materials that meet the stringent requirements of modern construction. These include energy efficiency and quick construction times. Sandwich panels are gaining traction due to their excellent thermal and acoustic properties, making these ideal for various commercial and industrial buildings. For instance,

The extensive use of these panels, especially in industrial, commercial, and transport-related constructions, is pushing demand for efficient building materials in India.

The growth, coupled with the National Infrastructure Pipeline (NIP) and government initiatives, positions insulated panels as a critical component in meeting India’s modern infrastructure goals.

Development of Semiconductor and Electronics Industry to Bolster Sales

India’s semiconductor and electronics manufacturing industry is emerging as a key driver for the market. With the government’s push for self-reliance through the Semicon India Program, the country is establishing itself as a key player in the global semiconductor market. Apart from that, substantial investments in domestic manufacturing are creating novel prospects. For example,

The novel manufacturing hubs require cleanroom environments that are tightly controlled in terms of temperature, humidity, and contamination. Sandwich panels, known for their superior insulation and airtight properties, are essential for creating these controlled environments. These are crucial for ensuring the quality of sensitive electronic components.

Global collaborations, such as those with the European Union (EU) and Japan are making India a superior country in terms of semiconductor supply chains. The country is offering fiscal incentives to semiconductor fabs under schemes like the Semiconductor Fab Scheme and Production Linked Incentive (PLI) Scheme.

Such initiatives further stimulate growth of the industry and increase demand for high-performance infrastructure materials. Cleanroom facilities, which need effective insulation, fire resistance, and contamination control, are a prime application for insulated panels. As India’s semiconductor industry rises, demand for unique, energy-efficient, and fire-resistant materials is set to surge, offering ample opportunities for sandwich panel manufacturers.

High Initial Cost of Sandwich Panels to Limit Adoption in Cost-sensitive Sectors

A key restraint for the adoption of insulated sandwich panels in India is their high initial cost, which poses a barrier in cost-sensitive sectors. These panels offer long-term benefits such as energy efficiency, fire resistance, and quick installation. However, the upfront investment is significantly higher compared to traditional building materials like bricks, concrete, and metal sheets.

Various developers, particularly in residential and small-scale industrial projects, often prioritize immediate cost savings over long-term advantages. This makes it difficult for insulated sandwich panels to gain widespread acceptance. Additionally, price fluctuations in raw materials like polyurethane and mineral wool exacerbate pricing challenges, hindering adoption.

Development of Data Center Infrastructure to Create Lucrative Opportunities

India's rapidly developing data center industry presents a significant opportunity for the insulated sandwich panel segment. For example,

As data centers require stringent temperature, humidity, and fire-resistant environments, demand for high-quality sandwich panels is set to surge. Policies introduced by states like Karnataka, Odisha, and Haryana are anticipated to create novel prospects.

The Central Government's initiatives to establish Data Center Economic Zones (DCEZ) and Data Center Parks are further driving investments in these facilities. These developments highlight the rising need for unique construction solutions that align with the specific requirements of hyperscale data centers.

Geographical diversification is anticipated to increase demand for sandwich panels in constructing modern data centers, creating substantial growth opportunities. As India’s digital economy develops, fueled by internet penetration and supportive policies, demand for efficient and durable building materials will continue to surge.

Booming Automotive Industry in India to Open the Door to Success

Rapid expansion of India’s automotive industry is driving adoption of lightweight and insulated materials like sandwich panels. With vehicle production reaching 28.43 million units from 2023 to 2024, demand for novel materials to enhance efficiency and sustainability is rising. India is also emerging as a global leader in manufacturing tractors, buses, and heavy trucks.

Lightweight sandwich panels, offering a high strength-to-weight ratio and superior thermal insulation, are gaining traction. This is because automakers are striving to reduce vehicle weight, improve fuel efficiency, and meet stringent emission norms. For instance,

Demand for insulated sandwich panels is also increasing in cargo transportation, particularly for goods requiring temperature regulation, such as pharmaceuticals, perishables, and electronics. For example,

India’s market is highly fragmented, with domestic and international players operating across diverse segments such as insulated panels, cold storage solutions, and industrial applications. Key players like Rinac India Limited, EPACK Prefab, and Kingspan Jindal dominate the market. They are doing so with robust manufacturing capabilities, extensive distribution networks, and a significant market presence.

Leading players collectively hold around 25% to 30% of the total market share. Small-scale firms, including WonderPUF and BNAL Prefabs, also play key roles in addressing specific needs within regional and niche markets.

Key companies such as Kingspan Jindal and Metecno India are enhancing growth through innovations in insulation technology, particularly in fire-resistant and energy-efficient panels. Strategic partnerships and mergers, like those of ArcelorMittal, further help extend market reach and strengthen production capacities.

Companies are also focusing on sustainability, ensuring eco-friendly solutions to meet the high demand for energy-efficient construction materials. These efforts, along with geographic expansion, enable them to capture a large share of the rapidly evolving market.

A Few Key Companies in India Sandwich Panel Market

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Zones Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Material Type

By Application

By End Use

By Zone

To know more about delivery timeline for this report Contact Sales

The market is projected to witness a CAGR of 11.4% from 2024 to 2031.

Polyurethane is anticipated to showcase a CAGR of 11.6% through 2031.

North India is set to witness a CAGR of 9.8% through 2031.

West India is estimated to witness a significant CAGR of 12.8% through 2031.

Rinac India Limited, EPACK Prefab, Kingspan Jindal, ArcelorMittal Construction-India, and Synergy are a few leading manufacturers.