- Industrial Goods & Service

- India Expansion Joints Market

India Expansion Joints Market Size, Share, and Growth Forecast 2026 – 2033

India Expansion Joints Market by Material Type (Metallic [Single Expansion Joints, Hinged Expansion Joints, Gimbal Expansion Joints, Universal Expansion Joints, Pressure-Balanced (Elbow & In-line), Toroidal Expansion Joints], Fabric [Standard Fabric Expansion Joints, Multi-Layer Fabric Expansion Joints], Rubber [Spool-Type, Arch-Type]), Equipment Type (Axial, Lateral, Angular, Universal/Multi-Directional, Pressure Balanced), Industry, and Regional Analysis (North India, South India, West India, East India), 2026–2033

India Expansion Joints Market Size and Trend Analysis

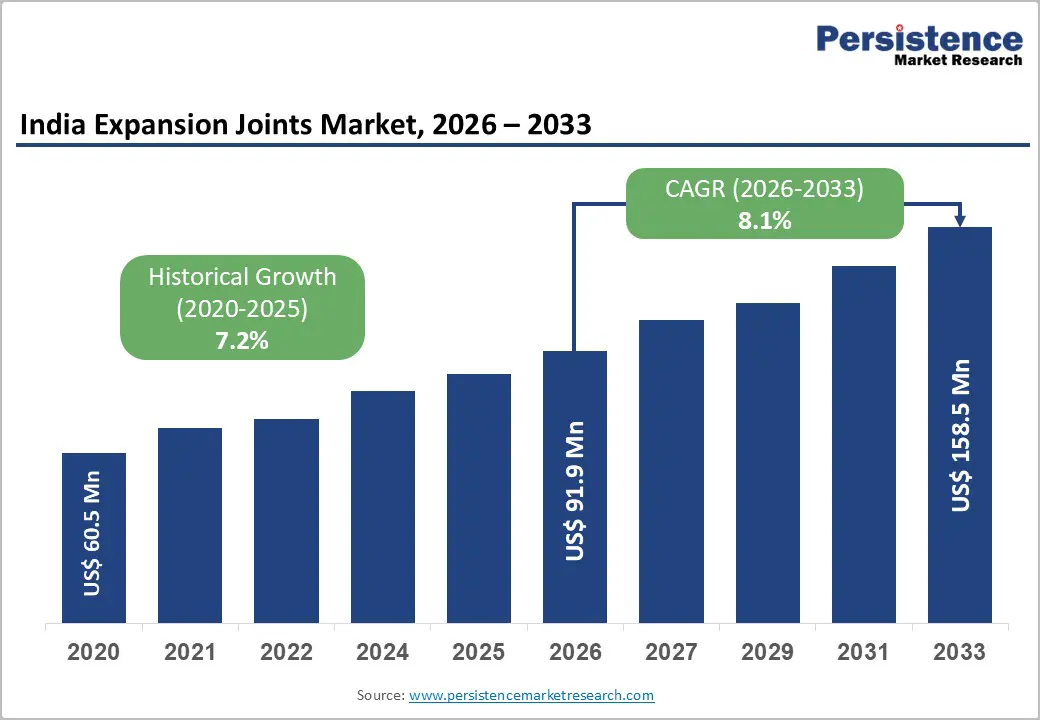

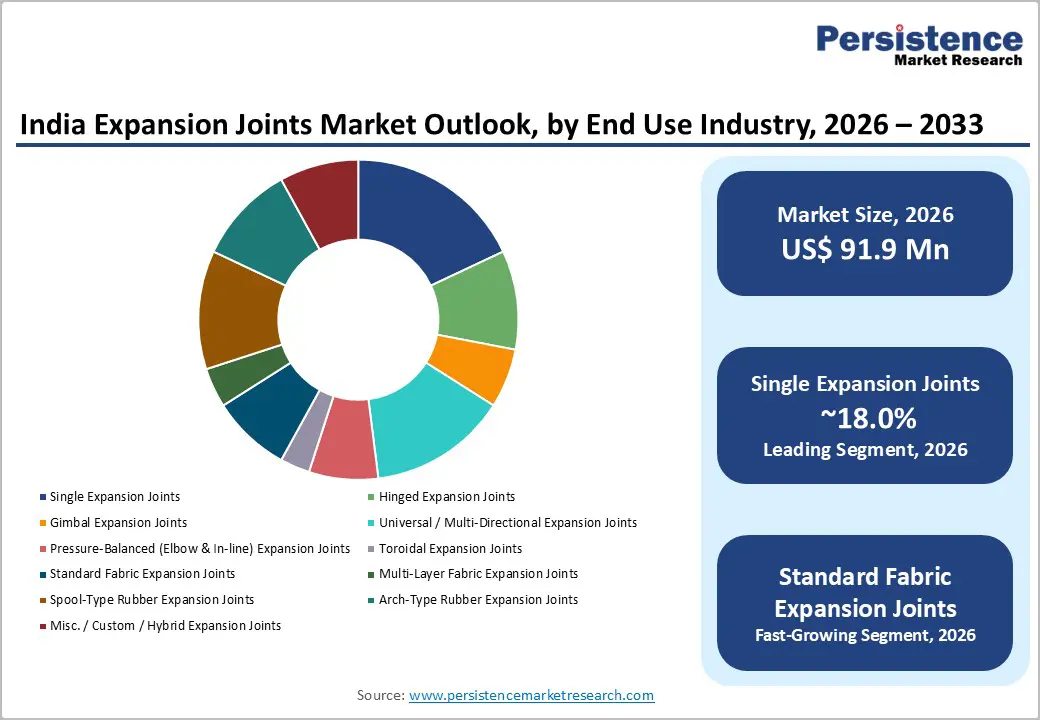

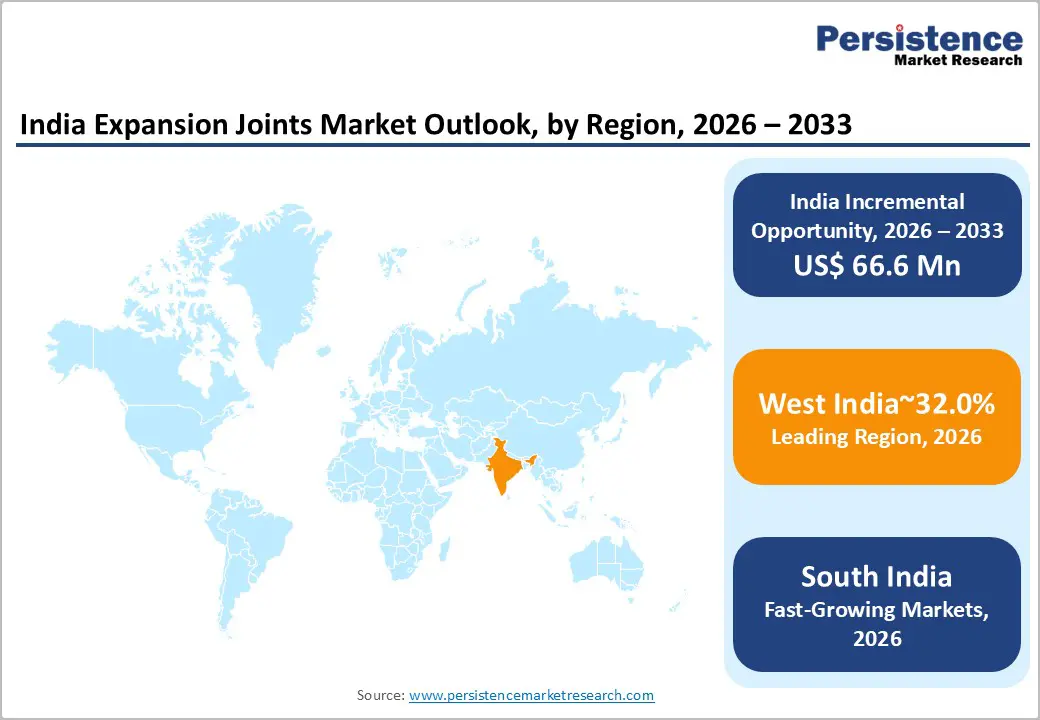

India expansion joints market size is expected to reach US$ 91.9 million in 2026 and US$ 158.5 million, growing at a CAGR of 8.1% between 2026 and 2033. Accelerating investments in energy infrastructure, industrial capacity, and urban utilities will fuel the growth in the coming years.

India's Total Primary Energy Supply (TPES) registered a growth of 2.95% in FY 2024–25, reaching 9,32,816 Kilo Tonnes of Oil Equivalent (KToE), while installed renewable energy capacity surged to 2,29,346 MW as of March 2025. Simultaneously, India's refining capacity reached 258.1 MMTPA in FY25, and domestic consumption of petroleum products stood at 239.2 MMTPA, sustaining high-volume demand for piping components, including expansion joints, across power, oil & gas, and chemical processing assets.

Key Industry Highlights:

- Leading Zone –: West India dominates the India expansion joints market with a 32% share in 2026, anchored by Gujarat's world-scale refinery and petrochemical assets, including the Reliance Jamnagar complex and Dahej LNG terminal infrastructure.

- Fast-Growing Market: North India is projected to record the fastest regional CAGR through 2033, driven by Rajasthan's renewable energy buildout, holding 23.70% of India's renewable potential and strategic petroleum reserve investments under ISPRL, creating sustained capital project demand.

- Dominant Material Type: Single expansion joints account for approximately 18% share in 2026, benefiting from their cost efficiency, installation simplicity, and near-universal deployment in thermal power, refining, and chemical process piping across high-growth industrial corridors.

- Fast-Growing Material Segment: Pressure-balanced expansion joints are likely to be forecast at a 7% CAGR by 2033, propelled by India's 10,805 km gas pipeline expansion plan and rapid CGD network rollout across 295+ PNGRB-authorised geographic areas.

- Key Opportunity: India's target to grow natural gas consumption by 60% by 2030 and deploy 80 CBG plants alongside CSP and waste heat recovery installations provides a well-defined, multi-year demand corridor for certified pressure-balanced and fabric expansion joint suppliers.

DRO Analysis

Drivers - Power Sector Capacity Additions and Thermal Infrastructure Buildout

India's power sector continues to be the single largest end-use driver for expansion joints, owing to the scale of new capacity commissioning and the operational demands of high-temperature steam systems in thermal and combined-cycle plants. India's gross electricity generation from renewable sources alone reached 4,16,823 GWH in FY 2024–25, up from 1,89,314 GWH in FY 2015–16. Both coal-based and gas-fired power stations deploy metallic expansion joints at critical junctions in boilers, flue gas ducts, steam lines, and condensers to absorb thermal elongation and vibration.

The National Electricity Plan mandates substantial capacity addition in gas and renewable-hybrid projects, each requiring carefully engineered bellows and duct expansion assemblies. Transmission and distribution losses declined from ~22% in FY 2015–16 to ~17% in FY 2024–25, reflecting network modernisation activity that also entails piping upgrades where expansion joints are integral components.

Downstream Oil & Gas and Petrochemical Capacity Investments

India's downstream energy segment is witnessing a broad expansion that directly translates to heightened demand for high-performance expansion joints in refineries, gas pipelines, and chemical complexes. India's refining capacity reached 258.1 MMTPA in FY25, with plans to scale further to 309.5 MMTPA by 2028. Crude oil throughput of private sector refineries has grown at a CAGR of 5.64% over the past decade.

In parallel, natural gas consumption is projected to grow by nearly 60% by 2030, reaching 297 million standard cubic metres per day (mmscmd), necessitating an expanded gas pipeline network of an additional 10,805 km. India's speciality chemicals sector was projected to reach US$ 64 billion by 2025, with new chemical and petrochemical investment regions (PCPIRs) integrating dense piping infrastructure, all requiring expansion joints to manage thermal movement, pressure surges, and vibration fatigue throughout plant lifecycles.

Restraints - Dependence on Imported Raw Materials and Alloy Inputs

A significant structural challenge for India's expansion joint manufacturers is their reliance on imported speciality alloys, including Inconel, Hastelloy, and duplex stainless steel, which are essential for high-temperature and corrosive-service bellows.

India's crude oil imports in FY25 stood at 242.4 MT, and LNG imports rose by 15.4%, reflecting strong downstream activity, yet the same import-oriented supply chain creates cost exposure for manufacturers when global metal prices spike or freight rates are elevated. This constrains margin predictability and complicates competitive pricing, particularly for mid-tier domestic producers who lack the scale to hedge raw material procurement effectively.

Lack of Standardisation and Skilled Engineering Talent Deficit

India's expansion joint segment suffers from an absence of a unified national procurement standard, with project specifications varying significantly across utilities, EPC contractors, and private operators.

Unlike in the European Union, where the Expansion Joint Manufacturers Association (EJMA) standards are uniformly referenced, Indian project specifications often rely on a mix of EJMA, ASME B31.3, and in-house OEM requirements. This fragmentation increases engineering lead times, raises qualification costs for manufacturers, and creates entry barriers that favor established global players over domestic SMEs. Compounding the issue, the availability of engineers with specialised knowledge in bellows design, fatigue analysis, and FEA-based qualification remains limited at the sub-contractor level.

Opportunities - Pressure-Balanced Expansion Joint Demand from Gas Pipeline Network Expansion

India's plan to expand its natural gas pipeline network by an additional 10,805 km, supplementing the existing 23,000+ km of gas transmission lines, creates a well-defined demand corridor for pressure-balanced expansion joints, the fastest-growing sub-segment. Pressure-balanced (elbow and in-line) joints are specifically engineered to absorb axial movement while eliminating pressure thrust forces on anchoring structures, making them indispensable at compressor stations, metering points, and directional changes in high-pressure gas networks.

India's PNGRB (Petroleum and Natural Gas Regulatory Board) has actively authorised new City Gas Distribution (CGD) networks across 295+ Geographical Areas (GAs). With natural gas consumption projected to nearly double by 2030, and LNG import infrastructure expanding at 15.4% y-o-y, manufacturers capable of supplying ASME and EJMA-certified pressure-balanced joints to midstream pipeline projects are positioned for sustained order growth through the forecast period.

Renewable Energy, Thermal Infrastructure, and Waste Heat Recovery Systems

Beyond conventional thermal power, India's surging renewable energy installations with solar potential reaching 33,43,378 MW in FY 2024–25, up from 7,48,990 MW just one year prior, are driving a parallel buildout of hybrid energy systems, concentrated solar power (CSP) installations, and waste heat recovery units (WHRUs) across industrial sites. Each of these applications requires fabric and metallic expansion joints in heat exchangers, duct systems, and steam generators.

India's commitment to 80 Compressed Biogas (CBG) plants and 20% ethanol blending by 2025 under the national biofuel mandate introduces new processing infrastructure where corrosion-resistant rubber and fabric expansion joints are critical for handling bio-gas streams. Manufacturers who align product development with these emerging clean energy infrastructure categories, notably flexible fabric joints for moderate-temperature renewable installations, stand to benefit from procurement cycles that are largely untapped by conventional piping suppliers.

Category-wise Analysis

Material Type Insights

Within the material type category, metallic expansion joints are dominant and likely to secure 58% share in 2026. Among metallic sub-types, single expansion joints account for the leading position with an estimated 18% share of the overall market in 2026. Single expansion joints are the most widely deployed bellows configuration across Indian power, refining, and chemical facilities due to their straightforward installation, predictable performance, and compatibility with axial-movement-dominant piping systems.

The Central Electricity Authority (CEA) data confirms that India's installed thermal generation capacity, where single bellows are standard in steam duct and flue gas systems, remains the largest block of power capacity. The dominance of single expansion joints is further reinforced by their cost efficiency relative to complex multi-directional assemblies, making them the default choice for EPC contractors executing large-scale infrastructure projects in India's power and process industries.

Equipment Type Insights

Axial expansion joints hold the leading position in the equipment type category, likely to account for approximately 35% in 2026. Axial joints absorb thermal elongation along the pipe axis and are the most fundamentally required configuration in straight-run pipe systems, which constitute the majority of piping layouts in Indian power stations, refineries, and chemical plants.

Their straightforward design enables standardised engineering and procurement, and they are compatible with virtually all service conditions from sub-zero cryogenic applications to high-temperature steam service. India's active refinery expansion trajectory, with crude throughput growing at a CAGR of 2.84% for public sector refineries and 5.64% for private sector refineries, consistently generates demand for axial bellows in process pipework across crude distillation, hydrocracking, and delayed coking units.

Industry Insights

Power & energy is the dominant end-use segment in the India expansion joints market, contributing approximately 38% of total demand in 2026. India's electricity generation ecosystem encompasses a large fleet of coal-fired, gas-based, and nuclear power stations, each deploying multiple expansion joint assemblies across high-pressure steam lines, feedwater systems, flue gas desulfurization (FGD) ducts, and exhaust stacks.

The Ministry of Power's data confirms India added over 29 GW of new power capacity in FY 2023–24 alone, with thermal plants accounting for a significant share. Renewable energy installations are additionally creating demand for expansion joints in CSP solar thermal loops and gas backup systems. India's per-capita energy consumption has grown at a CAGR of 1.89% over the past decade, reflecting structural growth in electricity demand that sustains continuous investment in generation and transmission assets throughout the forecast period.

Zone Insights

India Expansion Joints Market Trends and Insights

The India expansion joints market reflects the spatial distribution of the country's industrial and energy infrastructure. West India holds the dominant regional share at 32% in 2026, followed by South India at 28%, North India at 25%, and East India at 15%. The regional growth pattern closely mirrors India's industrial investment corridors, with refinery clusters, chemical parks, and power generation hubs driving procurement intensity in each zone.

West India Expansion Joints Market Size

West India commands the largest share at 32% in 2026, equivalent to approximately US$ 24.6 million. This position is underpinned by the concentration of India's refining and petrochemical assets in Gujarat, home to Reliance Industries' Jamnagar complex, the world's largest refining hub, and the Dahej and Hazira LNG terminals. Maharashtra's pharmaceutical and speciality chemicals clusters in Raigad, Pune, and Nagpur also generate sustained procurement of rubber and fabric expansion joints for chemical reactors and process piping.

Gujarat alone accounts for 9.10% of India's total renewable energy potential, and the Petroleum, Chemicals and Petrochemicals Investment Region (PCPIR) at Dahej anchors long-term capital project pipelines that require high-specification metallic bellows assemblies throughout construction and operational phases.

South India Expansion Joints Market Size

South India holds 28% of India expansion joints market in 2026, valued at approximately US$ 21.6 million. Andhra Pradesh and Telangana host major thermal power stations, including the NTPC Simhadri and APGENCO fleet, alongside Chennai's and Puducherry's growing petrochemical corridor.

Andhra Pradesh contributes 9.1% of India's renewable energy potential, and Karnataka contributes 8.59%, together driving significant substation and grid infrastructure activity. EagleBurgmann's inauguration of a Shared Services Center in Chennai in June 2023 reflects the region's growing strategic importance for global expansion and joint suppliers, reinforcing South India's role as both a procurement and manufacturing hub.

North India Expansion Joints Market Size

North India is likely to register 25% share in 2026, valued at approximately US$ 19.3 million. The region's demand is anchored by India's largest thermal power corridor spanning Uttar Pradesh, Rajasthan, and Punjab, alongside major public sector refinery operations of Indian Oil Corporation (IOCL) at Mathura and Panipat. Rajasthan, which holds 23.70% of India's total renewable energy potential, the highest of any state, is undergoing extensive solar park and power evacuation infrastructure development, generating new installation demand for duct expansion joints and heat exchanger bellows. The Union Budget FY26 allocation of INR. 5,597 crore (US$ 640.46 million) to the Indian Strategic Petroleum Reserves Ltd (ISPRL) for underground cavern development in the region further sustains capital project activity requiring specialised piping assemblies.

Competitive Landscape

India expansion joints market is moderately fragmented, with a blend of established multinational players and a growing cadre of domestic manufacturers. Global leaders such as EagleBurgmann, Witzenmann, and Flexicraft Industries compete alongside Indian manufacturers, including Metraflex India and Garg Tube on large EPC and utility contracts.

Key competitive differentiators include EJMA/ASME certification credentials, material traceability documentation, and the ability to supply customised high-temperature assemblies within compressed lead times. Manufacturers are progressively investing in finite element analysis (FEA) design validation and digital twin capabilities for life-cycle management services. Aftermarket oil monitoring and joint inspection services are emerging as value-added revenue streams that global players are leveraging to strengthen long-term relationships with Indian power and refinery operators.

Key Developments:

- February 2026: Indutrade AB completed the acquisition of Belman A/S, a Danish manufacturer of customised metallic and non-metallic expansion joints, expanding its Process, Energy & Water division and strengthening its India production footprint alongside Danish manufacturing sites.

- February 2026: Balco, a subsidiary of CSW Industrials, Inc., achieved an industry first by obtaining UL 2079 listing for its MetaBlock® fire-rated expansion joint barriers for wood-frame assemblies, addressing fire-resistance gaps in multi-family construction and meeting International Building Code (IBC) requirements.

India Expansion Joints Market – Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 60.5 Million |

| Current Market Value (2026) | US$ 91.9 Million |

| Projected Market Value (2033) | US$ 158.5 Million |

| CAGR (2026–2033) | 8.1% |

| Leading Region | West India, 32% share in 2026 |

| Dominant Category-1 (Material Type) | Metallic – Single Expansion Joints, ~18% market share |

| Top-ranking Category-2 (Equipment Type) | Axial Expansion Joints, ~35% market share |

| Incremental Opportunity (2026–2033) | US$ 66.6 Million (absolute dollar opportunity) |

Companies Covered in India Expansion Joints Market

- Trelleborg AB

- Keld Ellentoft India

- Witzenmann India

- Flexatherm Expanllow Pvt Ltd

- SBM Bellows

- EagleBurgmann India

- LBH Expansion Joints India

- Frenzelit Expansion Joint Pvt Ltd

- Shivam Cast Products

- Pliant Bellows

- Flexpert Bellows Pvt Ltd

- Belman Flexibles India

- Excel Bellows

- Aphrodite Polyprene

- Softt Bellows

Vallabh Engineers

Frequently Asked Questions

The India Expansion Joints market is estimated to be valued at US$ 91.9 million in 2026, up from US$ 60.5 million in 2020, and is projected to reach US$ 158.5 million by 2033 at a CAGR of 8.1%, supported by major investments in power generation, refining, and gas infrastructure.

The primary demand drivers are India's large-scale power sector capacity additions with installed renewable capacity at 2,29,346 MW as of March 2025, growing at 10.93% CAGR, and downstream oil & gas expansion, including refining capacity reaching 258.1 MMTPA and the planned 10,805 km gas pipeline network extension, collectively sustaining high-volume procurement of metallic and fabric expansion joints across thermal, chemical, and midstream assets.

West India is the leading regional market, commanding approximately 32% of the total India expansion joint demand in 2026. This dominance is driven by Gujarat's concentration of world-class refinery and petrochemical infrastructure, including the Reliance Jamnagar complex and Dahej LNG terminal, alongside Maharashtra's pharmaceutical and speciality chemicals clusters in Raigad and Pune, creating consistent demand for high-specification metallic and rubber expansion joint assemblies.

The most significant growth opportunity lies in pressure-balanced expansion joint procurement driven by India's natural gas infrastructure scale-up. India targets nearly 60% growth in natural gas consumption by 2030 to 297 mmscmd, requiring 10,805 km of new pipeline and expansion of 295+ City Gas Distribution geographic areas

Leading companies in the India Expansion Joints market include EagleBurgmann India Pvt. Ltd., Witzenmann India Pvt. Ltd., Indutrade AB , Balco (CSW Industrials), Flexicraft Industries, Senior Flexonics India, Trelleborg India Pvt. Ltd., Metraflex India, Garg Tube Export LLP, and Macoga S.A., among others, competing on EJMA/ASME certification, custom engineering capabilities, and after-sales service networks across India's industrial belt.