- Metals & Minerals

- High Carbon Bearing Steel Market

High Carbon Bearing Steel Market Size, Share, and Growth Forecast, 2026 - 2033

High Carbon Bearing Steel Market by Product Type (High Carbon Chromium Bearing Steel, Tapered Bearing Steel, Others), Product Form (Bars and Rods, Sheets and Plates, Others), Application, End-user Industry, and Regional Analysis for 2026 - 2033

High Carbon Bearing Steel Market Size and Trends Analysis

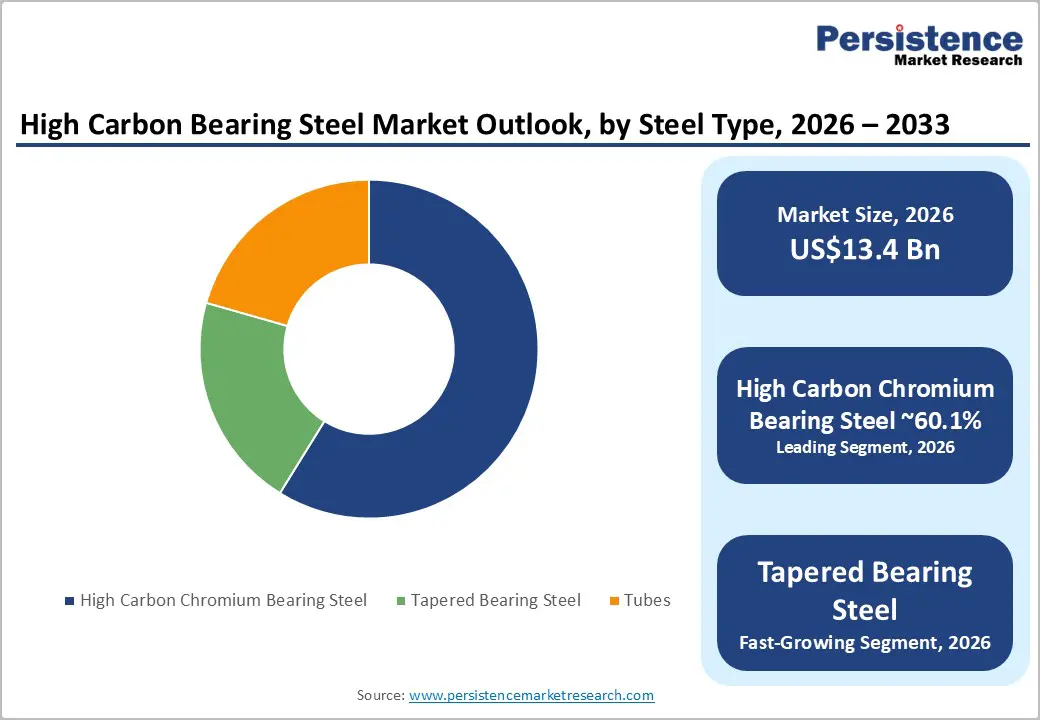

The global high carbon bearing steel market size is likely to be valued at US$13.4 billion in 2026 and is expected to reach US$20.4 billion by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by increasing demand for bearing steels that offer enhanced fatigue strength, dimensional accuracy, wear resistance, and high material cleanliness. The market is also benefiting from the growing adoption of electric vehicles, Industry 4.0 technologies, and advanced industrial equipment, all of which require reliable and long-lasting bearing components capable of operating under demanding conditions.

Key Industry Highlights:

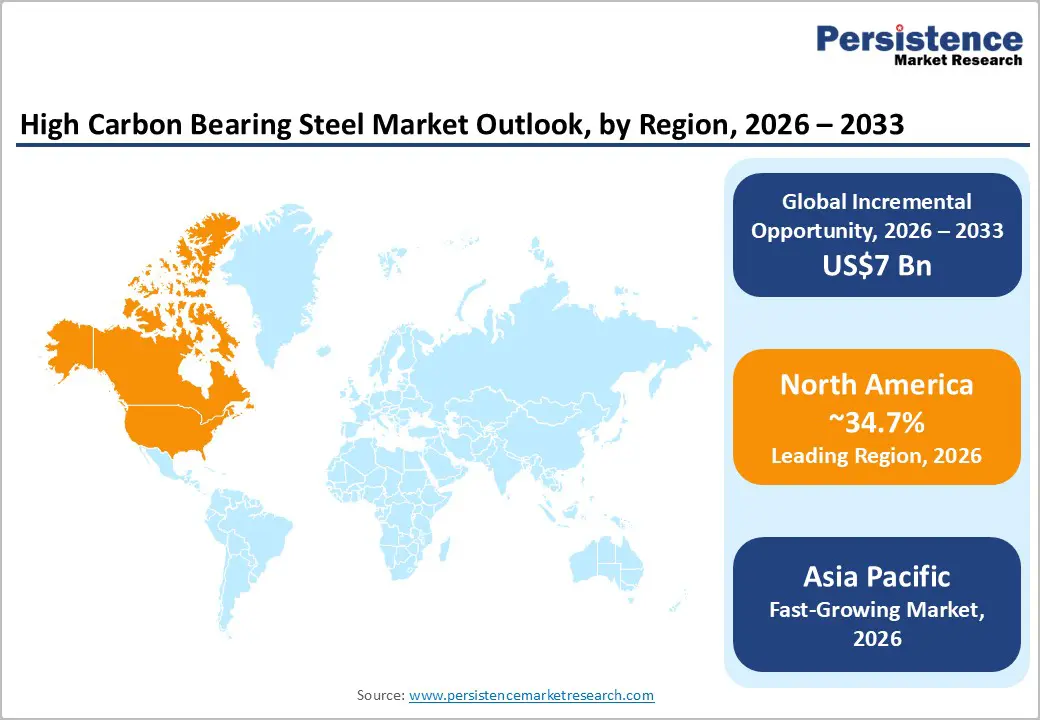

- Leading Region: North America is projected to account for 34.7% of the market share in 2026, driven by a strong automotive manufacturing base, advanced industrial infrastructure, aerospace production, and increasing investments in automation and electric-vehicle supply chains.

- Fastest-growing Region: Asia Pacific is projected to expand at the highest CAGR, supported by rapid industrialization, growing electric vehicle production, expanding infrastructure projects, and rising manufacturing investments across China, India, Japan, and ASEAN countries.

- Dominant Product Type: High Carbon Chromium Bearing Steel is anticipated to have a 60.1% market share, driven by its extensive adoption in high-performance bearings requiring exceptional durability, load-bearing capacity, and operational reliability.

- Leading Product Form: Bars and rods are estimated to account for 51.4% market share in 2026, supported by their widespread use in manufacturing bearing rings, rollers, shafts, and other precision-machined bearing components.

DRO Analysis

Driver - Rising Electrification of Transportation and Advanced Mobility Systems

The rapid adoption of electric vehicles (EVs) is creating substantial demand for high-performance bearing materials. Electric drivetrains operate at higher rotational speeds and require enhanced precision, durability, and thermal stability compared to conventional internal combustion engine systems. High carbon bearing steel plays a critical role in wheel hubs, transmissions, electric motors, and auxiliary drivetrain components due to its exceptional fatigue strength and wear resistance.

Automotive manufacturers are increasingly focusing on efficiency improvements, lightweight designs, and reduced energy losses, which place greater performance requirements on bearing systems. As EV production continues expanding across North America, Europe, and Asia Pacific, demand for premium-grade bearing steel is expected to increase significantly. Suppliers capable of delivering high-cleanliness steel grades and consistent metallurgical properties are positioned to benefit from growing OEM procurement requirements.

Expansion of Industrial Automation and Smart Manufacturing

Industrial automation continues to accelerate across manufacturing sectors, creating strong demand for high-performance bearings and associated steel products. Automated production lines, industrial robots, machine tools, conveyor systems, and precision manufacturing equipment depend heavily on bearings that can withstand repetitive loads, high rotational speeds, and continuous operating cycles.

The growth of Industry 4.0 initiatives and smart factory investments is increasing the installed base of machinery requiring advanced bearing solutions. High carbon bearing steel provides the fatigue resistance and dimensional stability necessary for these demanding applications. As manufacturers prioritize equipment reliability, productivity enhancement, and maintenance reduction, demand for premium bearing materials continues to expand. This trend is particularly evident in automotive manufacturing, semiconductor production, logistics automation, and precision engineering industries.

Restraint - High Production Costs and Decarbonization Challenges

Production of high carbon bearing steel remains energy-intensive and subject to strict quality-control requirements. Manufacturers must maintain precise chemical compositions, inclusion control, and heat-treatment consistency to meet demanding bearing specifications. These requirements increase production complexity and operating costs compared with conventional steel grades.

Environmental regulations and decarbonization initiatives further increase capital expenditures for steel producers. Investments in cleaner production technologies, emissions reduction systems, and energy-efficient manufacturing processes are becoming increasingly necessary. Smaller steel producers often face difficulties absorbing these costs while maintaining competitiveness. Volatility in raw material prices and energy costs can also impact profitability and create supply-chain uncertainties, potentially limiting market expansion in certain regions.

Opportunity - Growing Demand for Low-Carbon Specialty Steel Solutions

Sustainability objectives across manufacturing industries are creating opportunities for low-carbon and environmentally responsible bearing steel production. Automotive manufacturers, industrial equipment suppliers, and renewable energy companies increasingly incorporate sustainability criteria into procurement decisions.

Steel producers investing in energy-efficient manufacturing processes, recycled material utilization, and emissions reduction technologies can differentiate themselves in the marketplace. Advanced bearing steel grades that reduce machining requirements, improve operational efficiency, and extend component life are gaining increased acceptance among end users. As environmental regulations become more stringent, suppliers capable of combining superior performance with sustainability benefits are expected to capture greater market share and premium pricing opportunities.

Expansion of Manufacturing Capacity across Asia Pacific

Asia Pacific continues to emerge as the most attractive growth region for bearing steel manufacturers due to expanding industrialization, automotive production, and infrastructure investments. China, Japan, India, and Southeast Asian countries collectively represent a significant share of global bearing production and machinery manufacturing.

The ongoing localization of supply chains presents opportunities for steel producers to establish regional manufacturing facilities, distribution networks, and technical support centers. Growing investments in electric vehicles, industrial automation, renewable energy equipment, and transportation infrastructure are expected to generate long-term demand for high carbon bearing steel products. Companies that combine local production capabilities with advanced metallurgical expertise are likely to benefit from this regional expansion trend.

Category-wise Analysis

Product Type Insights

High carbon chromium bearing steel is anticipated to remain the dominant segment, accounting for approximately 60.1% of the market share in 2026. Its leadership is attributed to superior hardness, wear resistance, rolling-contact fatigue strength, and excellent dimensional stability, making it the preferred material for high-performance bearing applications. The segment is extensively used in automotive wheel bearings, transmission systems, aerospace components, industrial machinery, and precision equipment. Its ability to withstand heavy loads and prolonged operating cycles while maintaining reliability continues to support widespread adoption across critical end-use industries.

Tubes are projected to be the fastest-growing segment during the forecast period, driven by increasing demand for seamless bearing steel tubes in automotive, industrial machinery, renewable energy equipment, and precision engineering applications. Bearing steel tubes offer material efficiency, reduced machining requirements, and enhanced mechanical performance compared to conventional solid steel products. Their growing use in manufacturing bearing rings, rollers, and high-load rotating components is supporting market expansion. Rising investments in electric vehicles, industrial automation, and advanced manufacturing technologies are expected to further accelerate demand for bearing steel tube products through 2033.

Product Form Insights

Bars and rods are anticipated to hold the largest market share, accounting for approximately 51.4% of total revenue in 2026. Their leadership stems from extensive use in manufacturing bearing rings, rollers, shafts, and other precision-machined components. These products offer excellent dimensional consistency, machinability, and processing efficiency, making them the preferred feedstock for bearing manufacturers. Common applications include automotive wheel bearings, railway bearings, industrial gearboxes, and heavy machinery components.

Wire format is expected to be the fastest-growing product segment during the forecast period, supported by increasing demand for miniature and precision bearings used in electric motors, robotics, medical devices, and consumer electronics. For example, compact bearings used in robotic arms, electric vehicle motors, and high-speed medical equipment increasingly require high-quality wire-based steel products. Forged components are also gaining traction in heavy-duty sectors such as mining equipment and wind turbines, while sheets and plates maintain stable demand for bearing housings and specialized structural applications.

Regional Insights

North America is anticipated to account for approximately 34.7% of the market share in 2026, making it the leading regional market. Growth is supported by a well-established automotive industry, advanced industrial infrastructure, aerospace manufacturing capabilities, and increasing investments in electric vehicles (EVs) and factory automation. The region also benefits from reshoring initiatives that encourage domestic sourcing of critical industrial components, boosting demand for specialty bearing steel products.

U.S. High Carbon Bearing Steel Market Trends

The U.S. dominates the North America market due to its large automotive manufacturing base, strong aerospace sector, and extensive industrial machinery production. Growing investments in EV manufacturing, robotics, and smart factories continue to increase demand for high-performance bearings used in motors, transmissions, and precision equipment. The presence of major bearing manufacturers and specialty steel suppliers further strengthens the country's market position.

Canada High Carbon Bearing Steel Market Trends

Canada contributes through its automotive supply chain, mining equipment manufacturing, and industrial machinery sectors. Demand for high carbon bearing steel is supported by infrastructure development projects and the growing adoption of advanced manufacturing technologies. The country's emphasis on sustainable industrial production is also encouraging the use of premium-grade steel products.

Europe High Carbon Bearing Steel Market Trends

Europe remains a significant market for high carbon bearing steel, driven by its advanced automotive sector, strong industrial engineering capabilities, and focus on sustainable manufacturing practices. Regional growth is supported by increasing production of electric and hybrid vehicles, industrial automation investments, and demand for high-precision engineering components.

Germany High Carbon Bearing Steel Market Trends

Germany represents the largest market in Europe due to its leadership in automotive manufacturing, industrial machinery production, and engineering innovation. The country's strong presence in premium vehicle manufacturing and advanced automation systems generates substantial demand for high-performance bearing steel products. Investments in Industry 4.0 technologies continue to strengthen market growth.

U.K. High Carbon Bearing Steel Market Trends

The U.K. benefits from its aerospace, automotive, and industrial equipment sectors. Increasing adoption of automation technologies and investments in advanced manufacturing are supporting demand for specialized bearing materials. The country's focus on engineering excellence and high-value manufacturing continues to create opportunities for premium steel suppliers.

France High Carbon Bearing Steel Market Trends

France contributes significantly through its automotive, aerospace, and transportation industries. Demand for high carbon bearing steel is supported by modernization initiatives, renewable energy investments, and growing production of advanced machinery. The country's industrial diversification supports stable market expansion.

Spain High Carbon Bearing Steel Market Trends

Spain remains an important automotive manufacturing center within Europe. Strong vehicle production, industrial equipment demand, and ongoing investments in transportation infrastructure continue to support consumption of bearing steel products. The country's manufacturing sector increasingly emphasizes efficiency and quality improvements, driving demand for advanced steel grades.

Asia Pacific High Carbon Bearing Steel Market Trends

Asia Pacific is projected to be the fastest-growing regional market over the forecast period. The region represents the world's largest concentration of automotive production, industrial manufacturing, and bearing consumption. Rapid industrialization, urbanization, infrastructure development, and expanding EV production are creating substantial opportunities for high carbon bearing steel suppliers.

China High Carbon Bearing Steel Market Trends

China is the largest market in the region due to its dominant position in automotive manufacturing, industrial machinery production, and electric vehicle deployment. The country's extensive manufacturing ecosystem and growing investments in automation, robotics, and transportation equipment continue to generate strong demand for bearing steel. China also serves as a major production center for bearings and downstream mechanical components.

Japan High Carbon Bearing Steel Market Trends

Japan remains a global leader in precision engineering, bearing manufacturing, and specialty steel production. Demand is driven by advanced automotive technologies, robotics, machine tools, and industrial automation systems. The country's emphasis on quality, innovation, and high-performance materials supports consistent consumption of premium bearing steel grades.

India High Carbon Bearing Steel Market Trends

India is emerging as one of the region's fastest-growing markets, supported by expanding automotive production, industrialization, and government-led manufacturing initiatives. Increasing investments in railways, infrastructure, industrial machinery, and electric mobility are creating new opportunities for bearing steel manufacturers. Growth in domestic manufacturing capabilities is expected to further strengthen market demand.

Competitive Landscape

The global high carbon bearing steel market is moderately fragmented, characterized by the presence of global steel manufacturers, specialty steel producers, and integrated bearing-material suppliers. Competition is primarily based on product quality, metallurgical expertise, production efficiency, customer relationships, and technological capabilities.

Leading market participants are focusing on product innovation, sustainability, manufacturing efficiency, and geographic expansion. Investments in cleaner steel production, advanced metallurgy, localized supply chains, and application-specific bearing materials are becoming key competitive differentiators. Companies are also increasingly emphasizing lifecycle value, predictive maintenance support, and long-term customer partnerships to strengthen market positioning.

Key Industry Developments:

- In March 2025, NSK Ltd. announced the development of a compact and lightweight deep-groove ball bearing for electric vehicle (EV) drive units, achieving significant reductions in bearing size, weight, and friction.

- In September 2025, NSK Ltd. launched a verification program to promote bearing reconditioning and reuse using proprietary diagnostic technologies.

Companies Covered in High Carbon Bearing Steel Market

- Nippon Steel Corporation

- Ovako AB

- Sanyo Special Steel Co., Ltd.

- JFE Steel Corporation

- Daido Steel Co., Ltd.

- CITIC Pacific Special Steel Group Co., Ltd.

- Dongbei Special Steel Group Co., Ltd.

- Baowu Special Metallurgy Co., Ltd.

- Tata Steel Limited

- ArcelorMittal

- Saarstahl AG

- Swiss Steel Group

- TimkenSteel Corporation

- Acerinox S.A.

- Universal Stainless & Alloy Products, Inc.

- Changzhou Dongfang Special Steel Co., Ltd.

Frequently Asked Questions

The global high carbon bearing steel market is estimated to be valued at US$13.4 billion in 2026.

The high carbon bearing steel market is projected to reach US$20.4 billion by 2033.

The high carbon bearing steel market is expected to grow at a CAGR of 6.2% between 2026 and 2033.

Key market trends include growing adoption of electric vehicles and high-efficiency drivetrains, and increasing industrial automation and robotics deployment.

High carbon chromium bearing steel leads the market, accounting for approximately 60.1% of total market share in 2026, owing to its superior hardness, wear resistance, fatigue strength, and widespread use across automotive, aerospace, industrial machinery, and precision bearing applications.

Major companies include Nippon Steel Corporation, Ovako AB, The Timken Company, SKF Group, and Schaeffler AG.