- Display Technologies

- Flat Panel Displays Market

Flat Panel Displays Market Size, Share, and Growth Forecast 2026 - 2033

Flat Panel Displays Market by Technology (Liquid Crystal Display (LCD), Plasma Display (PDP), Organic Light Emitting Diode (OLED), Quantum Dot (QLED), Others), by Application (Smartphones & Tablets, Television & Digital Signage, PC & Laptop, Smart Wearables, Automotive Displays, Others), by Resolution (HD, Full HD, 4K/Ultra HD, 8K), Industry (Consumer Electronics, Automotive, Healthcare, Retail, BFSI, Military & Defense, Others), and Regional Analysis, 2026 - 2033

Flat Panel Displays Market Size and Trend Analysis

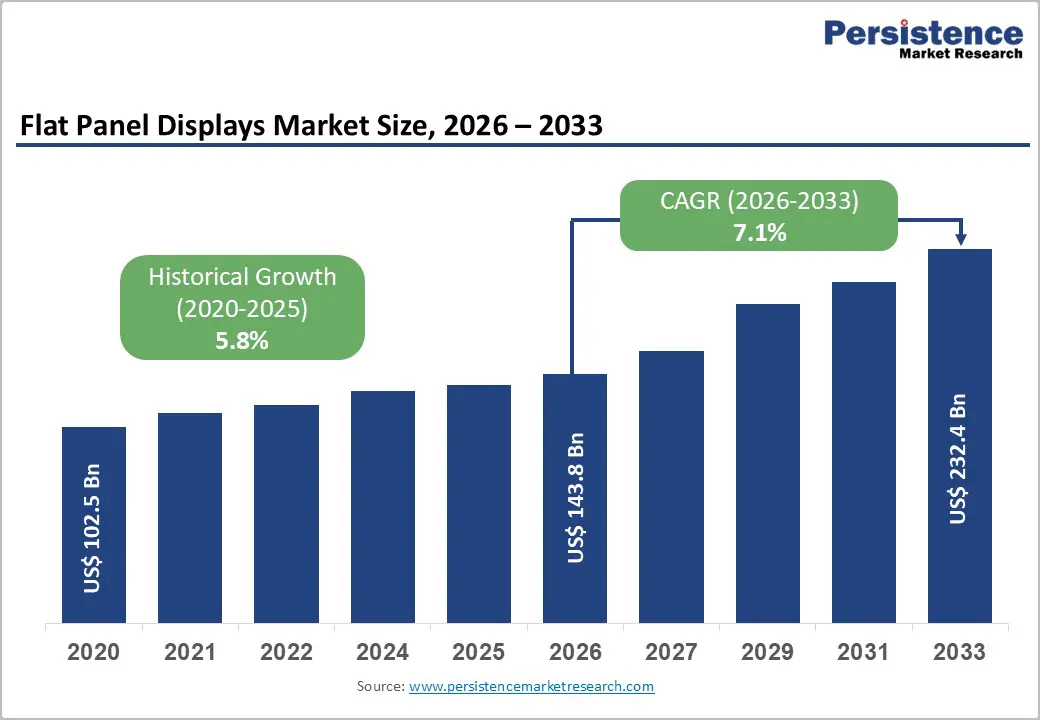

The global flat panel displays market size is expected to be valued at US$ 143.8 billion in 2026 and is projected to reach US$ 232.4 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

The market's robust expansion is primarily driven by surging consumer demand for high-resolution, energy-efficient display solutions across consumer electronics, automotive, and digital signage applications. Rapid adoption of OLED and QLED technologies, proliferation of smartphones and smart wearables, and the accelerating shift to 4K/Ultra HD resolution panels are collectively reinforcing growth. Additionally, expanding automotive cockpit digitalization and the transition toward immersive consumer entertainment experiences continue to sustain demand for advanced flat panel display solutions globally.

Key Industry Highlights:

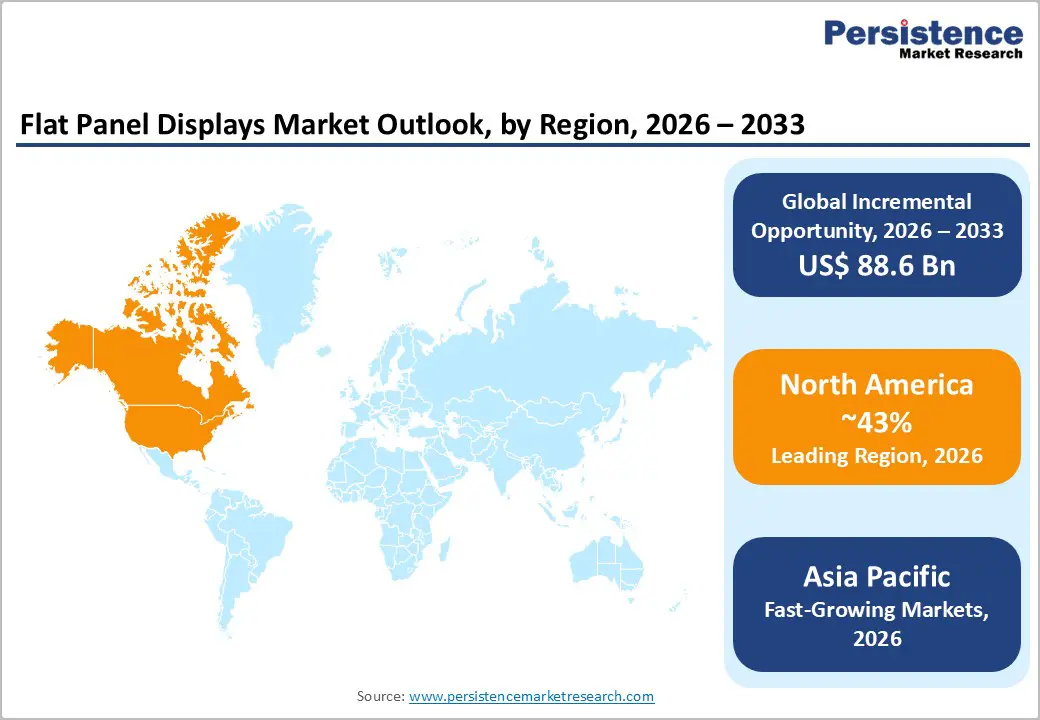

- Leading Region: Asia Pacific dominates the global flat panel displays market with approximately 43% share in 2025, underpinned by China's dominant manufacturing capacity, South Korea's technology leadership, and strong regional consumer electronics demand.

- Fastest Growing Region: North America is projected to register the fastest regional CAGR during 2026 - 2033, driven by accelerated OLED adoption in premium consumer electronics, robust digital signage growth, and high automotive display penetration.

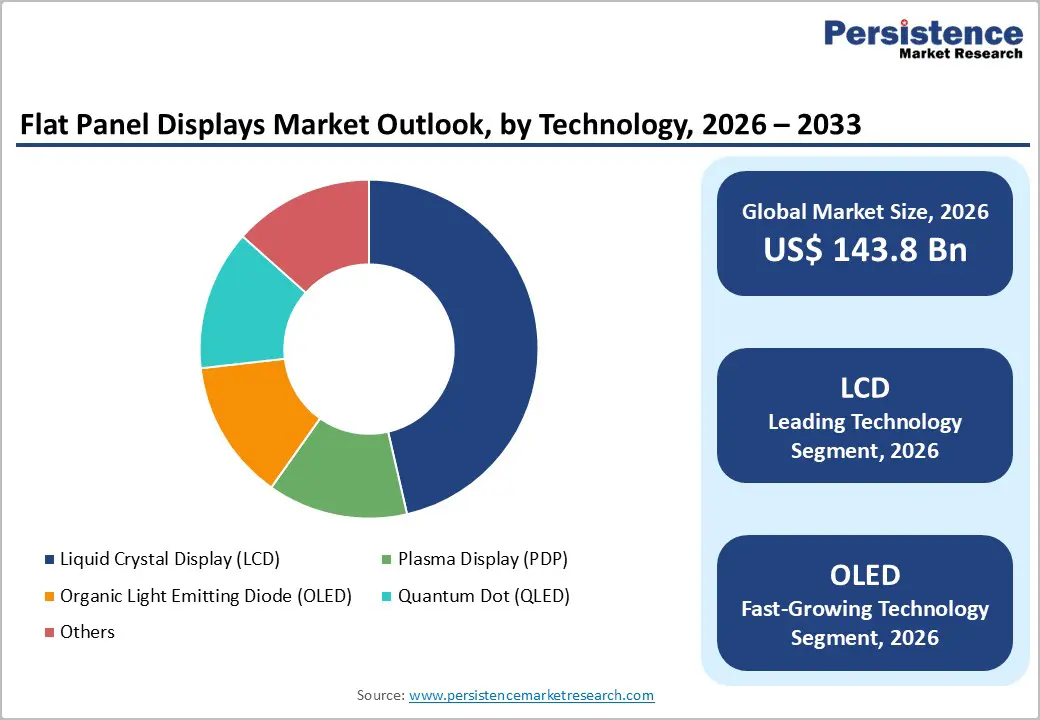

- Dominant Technology: LCD technology leads the global flat panel displays market with approximately 42% share in 2025, supported by cost-efficient manufacturing, broad application coverage, and large-scale Asian production capacity.

- Fastest Growing Application: The Automotive Displays application segment is set to register the highest CAGR during 2026 - 2033, driven by electric vehicle cockpit digitalization, ADAS integration, and global automotive OEM display technology upgrades.

- Key Market Opportunity: The healthcare sector display modernization and industrial automation adoption, with 19% U.S. growth in industrial display demand, present significant, high-margin revenue opportunities for specialized flat panel display manufacturers.

Market Dynamics

Drivers - Rising Adoption of OLED and QLED Technologies Across Premium Consumer Segments

The proliferation of Organic Light Emitting Diode (OLED) and Quantum Dot LED (QLED) technologies is a pivotal catalyst driving flat panel display market growth. Global automotive display panel revenues are projected to reach US$ 15 billion in 2026, representing an 8% year-on-year increase, driven by the premium adoption of OLED and LTPS TFT LCD technologies.

In the consumer electronics domain, OLED overtook LCD as the dominant smartphone panel technology in 2024, commanding a 56% share of smartphone display shipments. Manufacturers including Samsung Electronics Co., Ltd. and LG Display Co., Ltd., are investing heavily, with LG Display committing US$ 925 million through June 2027 to advance OLED production capabilities for smartphones, IT devices, and television panels.

Accelerating Automotive Digitalization and Smart Wearables Driving Display Demand

The accelerating digitalization of automotive cockpits and the exponential growth of smart wearable devices are creating significant incremental demand for advanced flat panel displays. The global automotive display market, valued at US$ 13.6 billion in 2025, is forecast to expand to US$ 18.3 billion by 2030 (Omdia), driven by electrification trends and the integration of multi-display digital cockpits in premium and mid-range electric vehicles.

More than 32 million automotive displays shipped in Q1 2024 alone, reflecting strong regulatory and consumer appetite for digital dashboards and Advanced Driver Assistance Systems (ADAS) interfaces. Simultaneously, flexible and foldable OLED displays are gaining traction in wearable devices, with Samsung shipping over 12.9 million foldable smartphones in 2023, of which 80% incorporated OLED panels, pointing to sustained long-term demand.

Restraints - High Manufacturing Costs of Advanced Display Technologies

One of the primary restraints constraining broader market penetration is the significantly elevated manufacturing cost associated with advanced display technologies, particularly OLED and QLED panels. OLED manufacturing equipment can cost 30-40% more than conventional LCD setups, substantially increasing capex requirements for display manufacturers. These elevated production costs translate into higher average selling prices, limiting adoption among mid-tier device manufacturers and price-sensitive consumer markets, particularly across Latin America, Middle East & Africa, and parts of South Asia, where consumer purchasing power remains constrained.

LCD Oversupply and Intense Price Erosion Pressuring Manufacturer Margins

The global LCD segment continues to face structural challenges arising from chronic oversupply, particularly from China-based manufacturers, which has caused significant average selling price erosion. Companies including BOE Technology Group and CSOT (China Star Optoelectronics Technology) continue to dominate global LCD supply. By 2025, Chinese capacity is projected to account for 76% of global OLED output, reshaping display market geography and compressing margins for established players in South Korea, Japan, and Taiwan, who must accelerate technology differentiation to preserve competitive positioning.

Opportunities - Expanding Digital Signage and DOOH Ecosystem Across Retail and BFSI Sectors

The rapid expansion of digital out-of-home (DOOH) advertising and smart retail environments presents a significant revenue opportunity for flat panel display manufacturers. The growing demand for Television & Digital Signage applications across Retail, BFSI (Banking, Financial Services & Insurance), and corporate verticals is accelerating the deployment of large-format, high-brightness flat panel displays.

With over 1,200 consumer electronics manufacturers and 21% annual growth in digital signage solutions in the U.S. market alone, the commercial display segment is emerging as a high-value, high-growth end market. The push toward cashless and contactless customer interfaces in BFSI and the adoption of interactive flat panel displays in smart retail concepts further reinforce this opportunity. Companies investing in 4K Ultra HD and OLED-based signage solutions stand to gain disproportionate market share.

Healthcare and Industrial Display Modernization Generating New Demand Vectors

The healthcare sector is increasingly adopting high-resolution flat panel displays for diagnostic imaging, patient monitoring, and surgical visualization applications, creating a substantial and recurring demand stream largely insulated from consumer electronics cyclicality. Advanced medical displays require superior color accuracy, high luminance, and consistent calibration, which aligns well with the capabilities of premium LCD and OLED panels.

Concurrently, industrial automation adoption, which recorded 19% growth in industrial-grade display adoption in the U.S. alone, and Military & Defense applications requiring ruggedized, high-brightness displays are opening differentiated revenue streams. Companies like NEC Corporation and Universal Display Corporation are well-positioned to capitalize on these specialized segments, which carry structurally higher margins compared to mainstream consumer display markets.

Category-wise Analysis

Technology Insights

Liquid Crystal Display (LCD) commands the leading position in the technology segment of the global flat panel displays market, holding approximately 42% market share in 2025. The dominance of LCD is underpinned by its well-established and highly cost-efficient manufacturing infrastructure, widespread availability across both high-volume consumer electronics and commercial applications, and continued price competitiveness relative to emerging display technologies.

Geographically, Asia Pacific, particularly China, South Korea, and Taiwan, contributes over 65% of global LCD production, ensuring a consistent low-cost supply globally. Despite growing OLED penetration at the premium end, LCD continues to dominate mid-range televisions, PC monitors, and automotive displays. The fastest-growing technology segment is OLED, driven by premiumization trends in smartphones and expanding automotive display applications.

Application Insights

The smartphones & tablets segment leads the application category with an estimated 34% market share in 2025, establishing itself as the single largest application vertical for flat panel displays globally. This leadership is sustained by the massive, annually refreshing consumer smartphone base, global smartphone shipments exceeded 1.2 billion units annually, and the relentless adoption of superior display technologies, including AMOLED and flexible OLED in both flagship and increasingly mid-range devices.

The Asia Pacific region, with its large and growing middle-class consumer base, is the primary growth engine for this segment. The fastest-growing application segment is Automotive Displays, driven by electric vehicle proliferation, digital cockpit integration, and ADAS system adoption across global automotive OEMs.

Resolution Insights

The full HD resolution segment holds the leading market share at approximately 38% in 2025, reflecting its broad penetration across mainstream smartphones, mid-range televisions, laptop displays, and digital signage applications. Full HD balances display quality, processing requirements, and manufacturing cost, making it the preferred resolution tier for mass-market consumer devices globally. Its affordability supports widespread adoption across price-sensitive markets in Southeast Asia, Latin America, and Africa.

The fastest-growing resolution segment is 4K/Ultra HD, driven by increasing availability of 4K content across streaming platforms, declining panel costs, and expanding consumer preference for immersive home entertainment experiences with ultra-high-definition visual quality.

Industry Insights

The consumer electronics vertical retains dominant market leadership with approximately 48% share in 2025, driven by the pervasive reliance of smartphones, televisions, tablets, laptops, and wearables on flat panel display technologies. Over 80% of electronic consumer gadgets rely on display technology, positioning consumer electronics as the foundational demand pillar of the flat panel display industry. The segment benefits from high device refresh cycles, continuous technological upgrades, and the ongoing shift toward premium display form factors.

The fastest-growing Industry is Automotive, where rapid electrification, digitalization of vehicle interiors, and regulatory mandates for safety systems including ADAS are generating unprecedented demand for advanced, ruggedized flat panel display solutions within modern vehicle cockpits.

Regional Insights

North America Flat Panel Displays Market Trends and Insights

North America accounts for approximately 28% of the global flat panel displays market in 2025, driven by high consumer electronics penetration, advanced digital signage infrastructure, and rising adoption of premium OLED and QLED display technologies. The region is characterized by strong automotive display integration, growing healthcare display demand, and significant enterprise adoption of large-format flat panel displays across corporate and retail environments.

- U.S. Flat Panel Displays Market Size

The U.S. dominates North American flat panel display demand, accounting for approximately 85% of the regional market. With 77% of U.S. households owning at least one flat-panel television, and over 54% of U.S. smartphones featuring OLED or advanced LCD panels, the country represents one of the highest-value demand markets globally for premium flat panel display technologies.

- Europe Flat Panel Displays Market Trends and Insights

Europe holds a significant share in the global flat panel displays market, propelled by strong demand for premium 4K and 8K television panels, robust automotive display adoption across leading vehicle manufacturers, and growing digital signage investments in retail and transportation. The region's stringent energy efficiency regulations under EU Ecodesign Directives are accelerating the transition toward energy-efficient OLED and QLED panels across consumer and commercial applications.

- Germany Flat Panel Displays Market Size

Germany leads the European flat panel display market, holding approximately 22% of regional market share, supported by its strong automotive manufacturing sector and high consumer electronics spending. Automotive display integration in German OEM vehicles, including BMW, Volkswagen, and Mercedes-Benz, is a key demand driver for advanced flat panel display technologies.

- U.K. Flat Panel Displays Market Size

The U.K. represents approximately 17% of European flat panel display demand. High digital content consumption, expanding DOOH adoption in retail environments, and the BBC's push toward 4K broadcast content are reinforcing consumer upgrade cycles and driving sustained demand for premium flat panel televisions and digital signage installations.

- France Flat Panel Displays Market Size

France accounts for approximately 14% of the European flat panel displays market. Government-backed digital transformation initiatives and a growing smart retail ecosystem are driving commercial display deployments. Rising adoption of OLED televisions among French consumers and strong demand from the healthcare sector for medical-grade displays contribute to sustained market growth across premium display technology segments.

Asia Pacific Flat Panel Displays Market Trends and Insights

Asia Pacific is the dominant region in the global flat panel displays market, commanding approximately 43% market share in 2025. The region is both the leading production hub, contributing over 65% of global display manufacturing, and a major consumption center. China alone accounts for 76% of global OLED output capacity as of 2025. South Korea's US$ 19 billion government subsidy plan further reinforces the region's leadership in Gen 8.5+ OLED and next-generation display lines.

- India Flat Panel Displays Market Size

India is an emerging and fast-growing flat panel display market, representing approximately 8% of Asia Pacific demand in 2025. Rising smartphone penetration, government-backed electronics manufacturing incentives under the Production Linked Incentive (PLI) scheme, and growing middle-class consumption are driving robust demand for Full HD and 4K LCD displays across consumer electronics and digital signage segments.

- Japan Flat Panel Displays Market Size

Japan holds approximately 12% of the Asia Pacific flat panel display market, supported by its advanced consumer electronics ecosystem and strong presence of display technology innovators including Sony Corporation, Sharp Corporation, and Japan Display Inc.. Domestic demand for premium 8K and OLED televisions and strong automotive display exports underpin market stability.

- Southeast Asia Flat Panel Displays Market Size

Southeast Asia represents approximately 10% of the Asia Pacific flat panel display market in 2025. Rapid urbanization, rising smartphone adoption, and expanding electronics manufacturing in Vietnam, where Samsung Display is investing US$ 1.8 billion in a new OLED plant, are establishing the sub-region as a critical node in the global display supply chain while fueling domestic market growth.

Competitive Landscape

The global flat panel displays market is moderately consolidated, with a few large manufacturers accounting for a significant share of production, particularly across Asia. Market structure is characterized by high capital intensity, strong entry barriers, and economies of scale, favoring established players. Leading companies focus on continuous R&D investment to advance next-generation technologies such as OLED, QLED, and MicroLED, ensuring product differentiation and premium positioning.

From a strategic standpoint, players are increasingly adopting vertical integration and forming cross-supply partnerships to strengthen control over raw materials and components. Geographic expansion of manufacturing bases is also a key trend to diversify supply chains and reduce geopolitical risks. Additionally, companies are exploring new business models such as display-as-a-service and technology licensing, while smaller participants compete by targeting specialized, high-margin niche applications.

Key Developments:

- April 2026: Nitek launched a next-generation interactive flat panel in Gujarat featuring Android 16, AI-enabled tools, enhanced processing, and improved storage, marking a shift toward smarter, future-ready classroom display solutions in India’s education technology market.

- March 2026: Horion showcased its M6APro V2 interactive flat panel at ISE 2026, featuring a quad-camera system and AI-powered collaboration tools to enhance hybrid meetings, strengthening its position in smart workplace display solutions.

- September 2025: Meta launched its first smart glasses with an integrated display, featuring a micro LCD (LCoS) system, AI capabilities, and in-lens content viewing, signaling early commercialization of wearable display technology beyond traditional flat panels.

Flat Panel Displays Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 102.5 Billion |

| Current Market Value (2026) | US$ 143.8 Billion |

| Projected Market Value (2033) | US$ 232.4 Billion |

| CAGR (2026 - 2033) | 7.1% |

| Leading Region | Asia Pacific, 43% market share (2025) |

| Dominant Technology | Liquid Crystal Display (LCD), 42% market share (2025) |

| Top-ranking Application | Smartphones & Tablets, 34% market share (2025) |

| Incremental Opportunity | US$ 88.6 Billion (Absolute Dollar Opportunity, 2026-2033) |

Companies Covered in Flat Panel Displays Market

- Emerging Display Technologies Corp.

- Innolux Corp.

- Sharp Corporation

- Japan Display Inc.

- Electronics Co. Ltd.

- Universal Display Corporation

- Display Co.

- Sony Corporation

- NEC Corporation

- Samsung Electronics Co., Ltd.

- Crystal Display Systems

- Panasonic Corporation

- Tokyo Electron

- Toshiba Corporation

- LG Display Co., Ltd.

- AU Optronics Corporation

- BOE Technology Group Co., Ltd.

- Tianma Microelectronics Co., Ltd.

- Visionox Technology Inc.

- E Ink Holdings Inc.

Frequently Asked Questions

The market is expected to reach US$ 143.8 billion in 2026.

Demand is driven by OLED and QLED adoption, automotive display growth, foldable smartphones, and expanding digital signage.

Asia Pacific leads the market with around 43% share.

Opportunities lie in digital signage, healthcare displays, and automotive display integration.

Key players include Samsung Electronics, LG Display, Sony, BOE Technology, AU Optronics, and others.